- Home Care & Utilities

- Bamboo Market

Bamboo Market Size, Share, and Growth Forecast, 2025 - 2032

Bamboo Market by Bamboo Type (Raw Bamboo, Processed Bamboo), Application (Construction & Infrastructure, Flooring & Interior Design, Furniture & Home Décor, Paper & Pulp Industry, Textiles & Apparel, Food & Beverages, Energy & Fuel), and Regional Analysis for 2025 - 2032

Bamboo Market Size and Trends Analysis

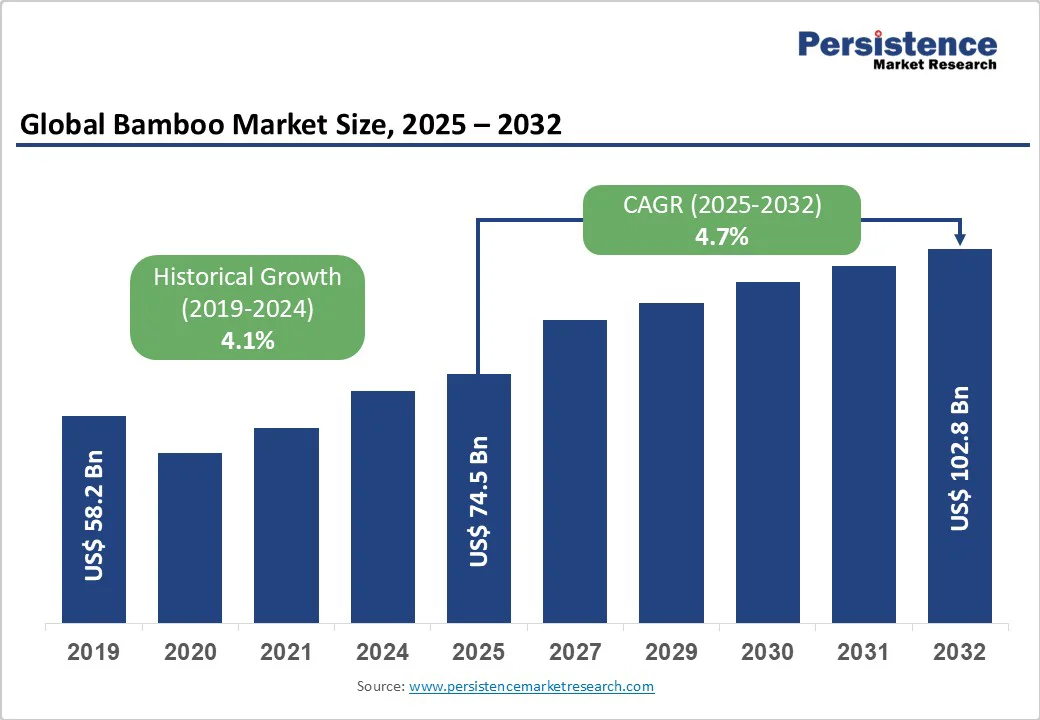

The global bamboo market size is likely to be valued at US$74.5 billion in 2025 and is projected to reach US$102.8 billion by 2032, growing at a CAGR of 4.7% from 2025 to 2032.

This growth is underpinned by expanding applications across construction, infrastructure, textiles, and packaging, as well as sustained policy support for sustainable materials and robust demand from emerging economies.

Key Industry Highlights:

- Leading Bamboo Type: Raw bamboo is expected to lead with a 60% share in 2025, driven by its widespread availability and established procurement programs.

- Fast-growing Bamboo Type: Processed bamboo is the fastest-growing segment, expanding at 40% in 2025, driven by advances in engineered product innovation.

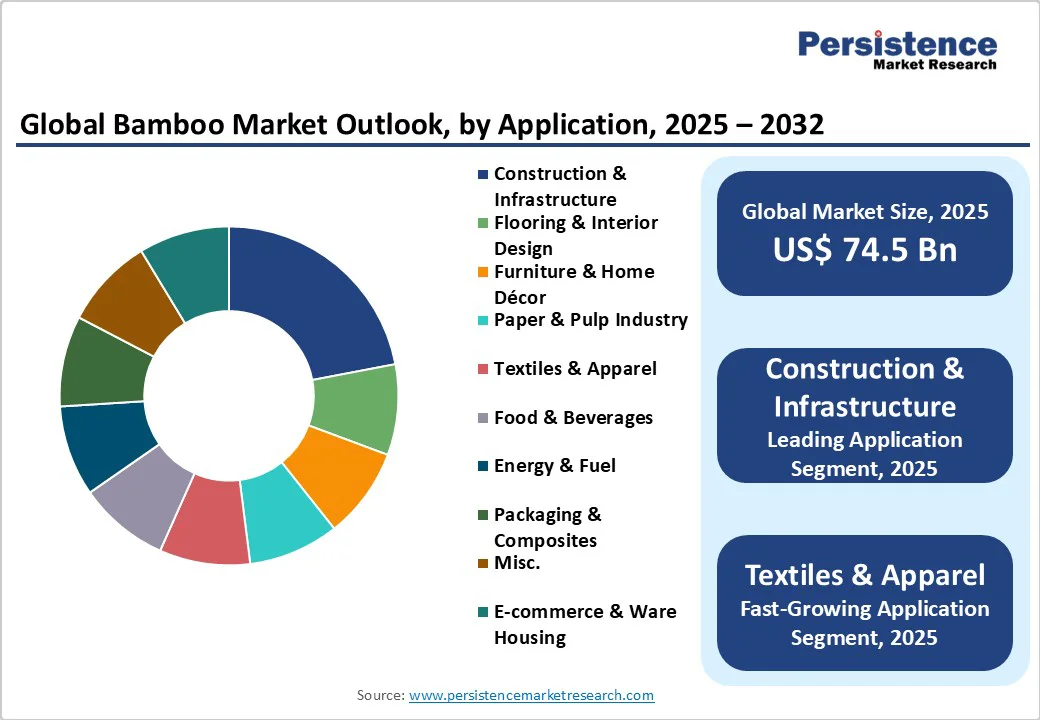

- Leading Application: Construction and infrastructure hold a 25% application share, driven by government mandates that integrate bamboo into public projects.

- Fast-growing Application: Textiles & apparel command 10% market share, fueled by rising consumer preference for sustainable, high-performance fabrics.

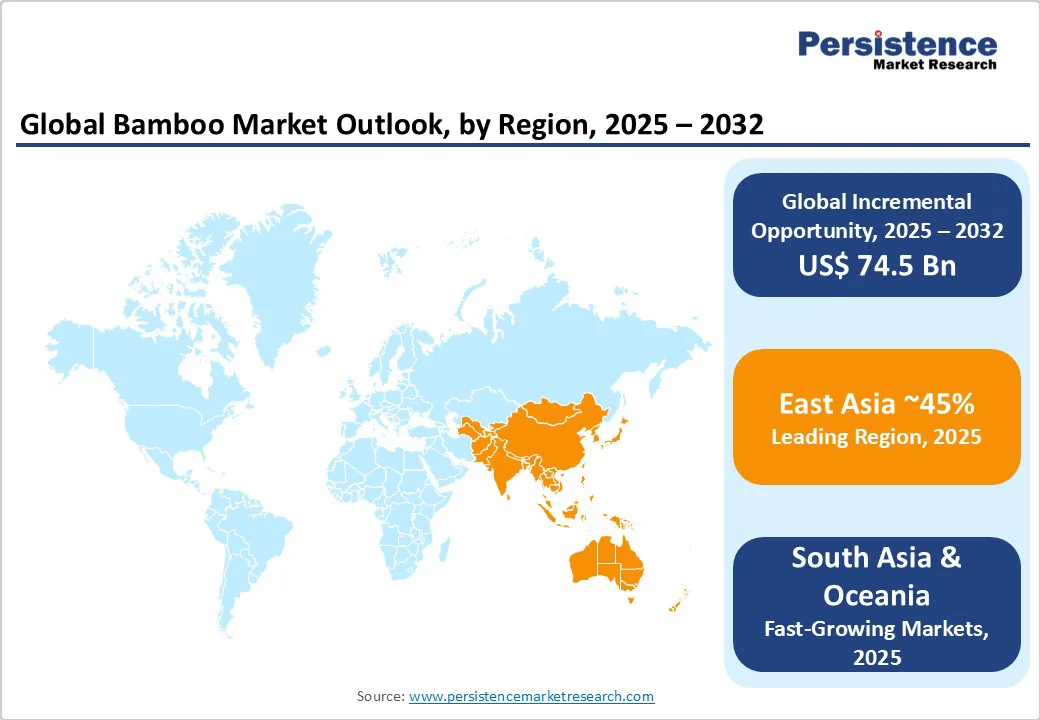

- Leading Region: East Asia accounts for 45% of the global market, primarily driven by China’s extensive cultivation area and robust export infrastructure.

| Key Insights | Details |

|---|---|

| Bamboo Market Size (2025E) | US$ 74.5 Bn |

| Market Value Forecast (2032F) | US$102.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Dynamics

Driver - Demand for Sustainable Construction Materials

Global infrastructure development is increasingly seeking renewable, low-carbon solutions, driving the adoption of bamboo for housing, bridge-building, and disaster response. Engineered bamboo products, including laminated mats, composite boards, and prefabricated components, meet international standards for strength and durability, supported by mandatory procurement targets, e.g., India’s Assam Cabinet directive for 5% bamboo-based materials in public projects and integration of bamboo into public works schedules.

Technological advances in processing and product innovation enable bamboo to substitute for timber, steel, and plastics, reducing ecological impacts and enhancing climate resilience. The sector’s integration into government construction schedules signals further market expansion and investment in sustainable infrastructure.

Supportive Regulatory and Policy Frameworks

National agencies and international organizations are investing in formalizing bamboo market systems, enhancing cultivation, and improving quality standards. India’s Ministry of Agriculture, through the National Bamboo Mission, links growers and artisans, supports MSMEs, and promotes standardized value chains with intervention from the Bureau of Indian Standards (BIS).

China’s 12th Five-Year Plan and forestry policies designate bamboo as a strategic resource, driving research in bamboo genetics, industrialization, and the development of managed plantations. INBAR, with 45 member states, coordinates standardization and policy harmonization for global trade, facilitating sustainable growth and international export compliance. Regulatory clarity and benchmarks accelerate adoption, enhance export readiness, and foster stable supply chains.

Environmental Sustainability and Climate Initiatives

Bamboo’s environmental advantages, including rapid regeneration, high carbon sequestration, and significant oxygen release, align with global climate mitigation and land restoration agendas.

Large-scale bamboo plantations absorb substantial amounts of greenhouse gases, restore degraded soils, and stabilize landscapes, thereby supporting the United Nations Sustainable Development Goals (SDGs) and national climate strategies in India, China, and Brazil.

Programs such as the Deendayal Antyodaya Yojana in India and sustainability-themed research and development initiatives in Brazil and China position bamboo as an ecological solution to soil erosion, water pollution, and resource scarcity. This alignment with green growth policies is driving investment in bamboo as a climate-smart material and boosting its market credibility.

Restraint - Structural Cost Barriers to Limit the Adoption

High initial investment requirements and limited mechanization within bamboo cultivation and processing restrict entry for small producers and MSMEs, impeding scalability. Most enterprises, especially in China, operate below 5 million CNY annual revenue, reflecting low labor productivity and inefficient resource utilization.

Energy consumption and lack of specialized talent challenge competitive pricing, resulting in constrained profitability and slower technological adoption. These cost barriers increase risk for new ventures, reduce accessibility for emerging market players, and could limit the pace of industry modernization.

Regulatory and Supply Chain Constraints

Despite policy support, fragmented supply chains and compliance requirements such as BIS standards in India or INBAR export regulations present hurdles for local producers seeking market entry.

Variability in domestic recognition, certification burdens, and the need to meet specifications for export restricts uptake, particularly among rural and smallholder groups. Inconsistent product standards and limited awareness of bamboo’s diverse applications pose additional supply chain risks, potentially resulting in limited product diversity and hindered market expansion.

Opportunity - Integration with Modern Industrial Applications

Bamboo integration into modern industrial sectors such as composites, prefabricated buildings, energy production, and sustainable packaging creates significant commercial and innovation opportunities.

The material’s structural properties enable high-value applications, with increasing demand from construction, furniture, and interior design industries seeking cost-effective and renewable alternatives. The expansion of bamboo products into mainstream markets supports further diversification, increased R&D investments, and the potential for technology partnerships with leading engineering firms, thereby stimulating both domestic production and export volumes.

Efforts by national missions and international organizations such as INBAR and USAID collaborations are supporting innovation and skill development, opening pathways for local producers to participate in global supply chains. Standardized bamboo products are entering retail and wholesale channels via dedicated bazaars, e-commerce platforms, and direct procurement programs. Enhanced access to digital marketplaces and traceable supply chains is unlocking new opportunities for certified, value-added products, supporting scaling and market penetration.

Rural Livelihood Initiatives and MSME Cluster Expansion

Governments are leveraging bamboo cultivation to promote rural development and women’s economic empowerment. Programs like India’s MSME clusters and National Rural Livelihood Mission (DAY-NRLM), in collaboration with USAID and Industree Foundation, have mobilized over 10,000 women in producer collectives, resulting in $3 million in market orders since 2019.

The deployment of digital tools such as the UGAO app streamlines supply chain tracking and compliance, positioning smallholder bamboo growers for stable income streams and long-term market participation.

Recent handbook launches and app-based support for regional language accessibility enhance farmer education, facilitate traceability and quality-verified supply chains, and foster the adoption of best practices for improved yield and market access.

Category-wise Analysis

Bamboo Type Segment Insights

Raw bamboo leads the market, commanding a 60% share in 2025. Its role is central in construction, scaffolding, and traditional implements, reflecting mature supply chains and established farming practices among smallholders and cottage industries.

Governments in Asia, particularly China and India, maintain extensive plantations and promote raw bamboo due to its adaptability, renewability, and economic value, thereby supporting resilient income streams and broad-based employment.

Processed bamboo, with a 40% share in 2025, represents the fastest-evolving segment. Its adoption is spurred by modern manufacturing trends, particularly engineered flooring, mat panels, and high-end furniture, which drive export growth and domestic value addition.

Strategic standards, such as BIS guidelines and government procurement mandates, enhance the credibility and market penetration of processed bamboo. Investment in processing infrastructure and mechanization across East Asia, India, and Brazil pivots industry growth toward durable, quality-verified products for global trade.

Application Insights

Construction and infrastructure are the dominant applications, holding a 25% market share in 2025. This segment leverages bamboo's tensile strength, rapid regrowth, and eco-credentials, earning policy-driven support in public works procurement, such as mandated material quotas in Indian and Chinese government building schedules. The accelerated uptake in green building certifications and disaster-resilient structures reflects robust demand for bamboo construction materials across the East and South Asian regions.

Textiles and apparel are the fastest-moving application segment, with a 10% share in 2025. Eco-labeling, technical innovation in bamboo fibers, and the rise of sustainable fashion have amplified bamboo’s profile as a textile substrate.

Value-chain mobilization, certified supply chains, and premium textile collaborations offer new growth vectors, especially in digitally enabled MSME clusters and export-driven manufacturing hubs, contributing to sectoral diversification.

Regional Insights

East Asia Bamboo Market

East Asia leads the global bamboo market, accounting for 45% of the total share in 2025. The region’s dominance is rooted in China’s status as both the “Bamboo Kingdom” and a leader in resource development, with 6.73 million hectares under cultivation and a 67% share of the global export market. Performance metrics include an annual production of 40 million tons and sophisticated supply chain integration that spans cultivation, processing, and export.

Policy frameworks, such as China’s Five-Year Plans and provincial investments in bamboo nurseries and R&D, underpin innovation and value addition. Meanwhile, government standards, including timber and paper pulp categorization, streamline production and trade.

The competitive landscape is marked by high industrial integration but fragmented enterprise scale, with investments in improving mechanization, product diversity, and export capacity.

Investment opportunities lie in expanding engineered bamboo, scaling panel and flooring production, and leveraging government-industry partnerships for high-value exports and domestic adoption.

South Asia and Oceania Bamboo Market

South Asia & Oceania hold a combined share of 28% in 2025, bolstered by India’s 15 million hectares of bamboo resources and robust government support via the National Bamboo Mission and MSME clusters.

Key country metrics include an annual production of 14.6 million tons and the engagement of approximately 8.6 million people in the bamboo value chain. The regulatory environment reflects harmonized standards (BIS), targeted incentives, and integration with rural development missions.

Investment trends emphasize support for women-owned enterprises, livelihood creation, and digital value chain transparency. The competitive landscape is defined by emerging producer collectives, supported by programs like DAY-NRLM, which focus on inclusivity and sustainable income generation.

Opportunities exist in scaling export capacity, market formalization, and enhanced traceability, leveraging digital platforms and government-backed aggregation to facilitate broader participation and impact.

Latin America Bamboo Market

Latin America is expected to command a 10% share in 2025, primarily driven by Brazil’s powerhouse of bamboo biodiversity and cultivation. Brazil boasts over 300 species of bamboo across 5.26 million hectares, with a notable presence in furniture, crafts, and innovative product applications.

Key country metrics include annual exports of US$3.61 million and imports totaling US$32.26 million in 2023, indicating strong domestic demand and development potential. The competitive landscape benefits from R&D investment, creative product diversification, and increasing alignment with global sustainability trends.

Manufacturing advantages stem from the availability of raw materials, skilled craftsmanship, and advanced processing technology. Investment opportunities are thriving in local manufacturing, high-value products, and export-oriented innovation, supporting trade diversification and economic development.

North America Bamboo Market Trends

North America’s bamboo market comprises 5.5 of % global share. The United States, without native commercial bamboo, capitalizes on a robust nursery, processing, and import segment.

Premium product demand, engineered construction applications, and innovative landscaping solutions steer market expansion. The competitive landscape is characterized by a strong import dependency, niche product development, and a growing sustainability movement that supports the adoption of bamboo in green building, textiles, and packaging.

Europe Bamboo Market Trends

Europe represents 6.5% of the global market share. As there are no native bamboo stands, the market relies entirely on imported raw material and localized processing for landscaping, construction, and textile applications.

Innovation is centered on engineered products and premium furniture, while competitive positioning favors smaller, specialized players with advanced product design. Regulatory support emphasizes green building codes, eco-labeling, and circular economy principles, thereby promoting the role of bamboo in low-carbon construction and sustainable urban development.

Competitive Landscape

The bamboo market is characterized by fragmented industry concentration, with regional pockets of integration, especially in China and India. Leading players capture significant shares in panels, flooring, and engineered materials, while hundreds of MSMEs and cluster-based enterprises contribute to diverse product categories. Integration across cultivation, processing, retail, and export fosters competitive positioning; however, barriers to entry and technology adoption persist for small producers.

Market leaders focus on product innovation, process formalization, cost reduction through mechanization, and expansion into new geographic and product segments. Differentiators include certified product lines, digital platforms for traceability, and government-backed mandates for public procurement.

Emerging models stress inclusivity, especially empowering women and rural producers, and integration with broader sustainability, climate, and rural development strategies.

Key Industry Developments

- In 2025, Miami Herbert student Jimmy Ayash co-founded Kong Rolls, an eco-friendly bamboo toilet paper brand that offers a sustainable alternative to conventional paper products, aiming to challenge major industry players while promoting forest conservation.

- In 2024, Colgate Company launches the Bamboo Toothbrush with Recyclable Packaging.

- In 2023, Solo, one of Türkiye’s most popular toilet paper brands, introduced its Bamboo-Infused Toilet Paper, offering an eco-conscious and affordable hygiene solution designed to bring sustainable comfort to households nationwide.

- In 2020, Bamboo specialist MOSO International BV has acquired Bambeau Becker & Großgarten GmbH, located in Frechen, Germany. For the time being, the brands and sales structures of both companies remain unchanged.

Companies Covered in Bamboo Market

- Moso International BV

- Shanghai Tenbro Bamboo Textile Co. Ltd

- Dasso Industrial Group Co. Ltd.

- Cali Bamboo

- Tengda Bamboo-Wood Co. Ltd.

- Higuera Hardwoods LLC

- Kerala State Bamboo Corporation

- Epitome bamboowood products (Mutha Industries)

- EcoPlanet Bamboo Group

- Guadua Bamboo

- Zhejiang Senhe Bamboo & Wood Co. Ltd

- Bamboo India Pvt Ltd

Frequently Asked Questions

The global Bamboo market is projected to be valued at US$ 74.5 Bn in 2025.

The Construction & Infrastructure segment is expected to hold a 25% share in 2025, driven by government mandates integrating bamboo into public projects and infrastructure standards.

The bamboo market is poised to witness a CAGR of 4.7% from 2025 to 2032.

The bamboo market growth is driven by its proven sustainability credentials and supportive regulatory frameworks promoting renewable, low-carbon materials.

Key market opportunities lie in the expansion of engineered bamboo applications across industrial sectors, unlocking high-value product development and export potential.

Leading bamboo companies include MOSO International B.V., Dasso Industrial Group Co. Ltd., Cali Bamboo, Kerala State Bamboo Corporation, Epitome Bamboowood Products (Mutha Industries), EcoPlanet Bamboo Group, and Guadua Bamboo.