- Food Ingredients & Additives

- Vegan Protein Bars Market

Vegan Protein Bars Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Vegan Protein Bars Market is segmented by Ingredient Type (Nuts, Seeds, Pea, Soy, Multigrain, and Others), Nature (Organic and Conventional), Form (Hypermarkets/Supermarkets, Convenience Stores, Pharmacies, Specialty stores, Online Retail, and Others), and Regional Analysis, 2026 - 2033

Vegan Protein Bars Market Share and Trends Analysis

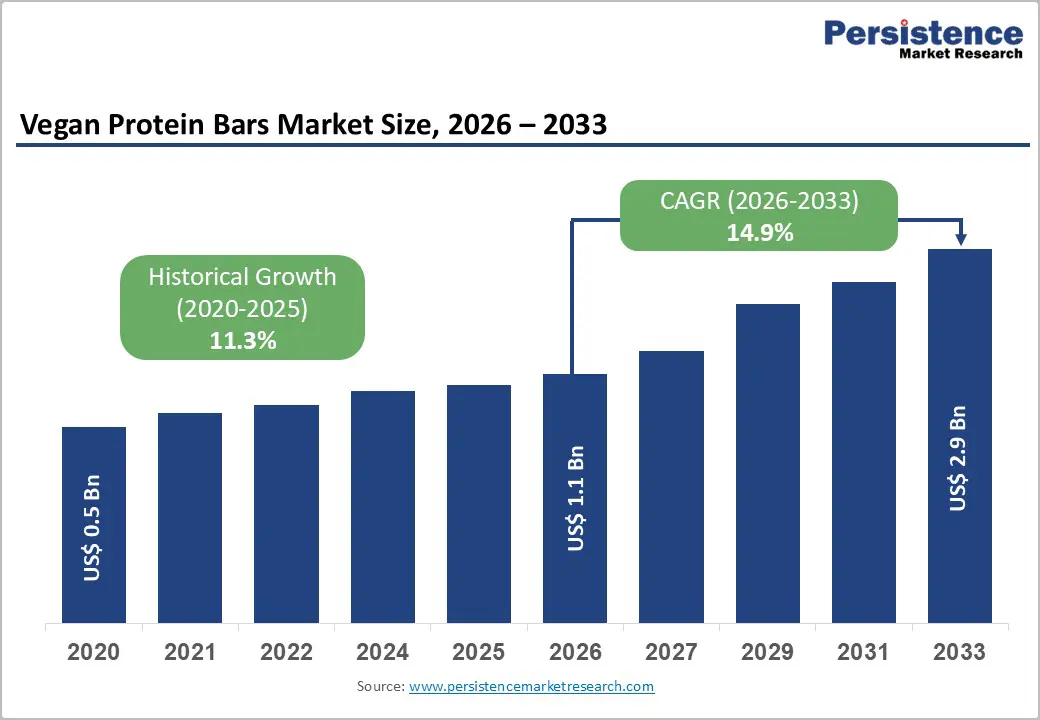

The global vegan protein bars market size is expected to be valued at US$ 1.1 billion in 2026 and projected to reach US$ 2.9 billion by 2033, growing at a CAGR of 14.9% between 2026 and 2033. The market is primarily driven by the rising global transition toward plant-forward diets and increasing consumer awareness regarding animal welfare and environmental sustainability.

A structural shift in the fitness industry has led to increased demand for portable, meat-free protein sources that meet both performance and ethical standards. Furthermore, recent regulatory clarity from the U.S. Food and Drug Administration (FDA) on the labeling of plant-based alternatives has bolstered consumer trust, while innovations in flavor masking and texture enhancement by companies such as Glanbia plc and Mondelez International have made these bars more palatable to a broader flexitarian audience.

Key Industry Highlights:

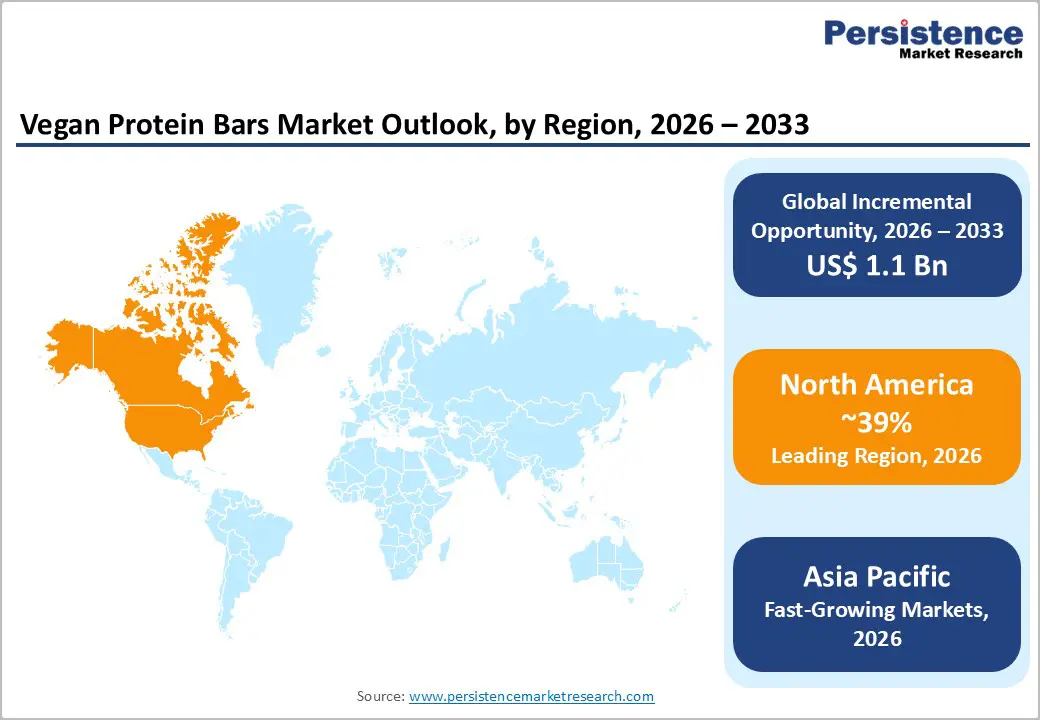

- Leading Region: North America held the largest market share of 39% in 2025, supported by a robust fitness culture and early regulatory clarity on plant-based labeling.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, driven by rapid urbanization and a high natural preference for vegetarianism in India and China.

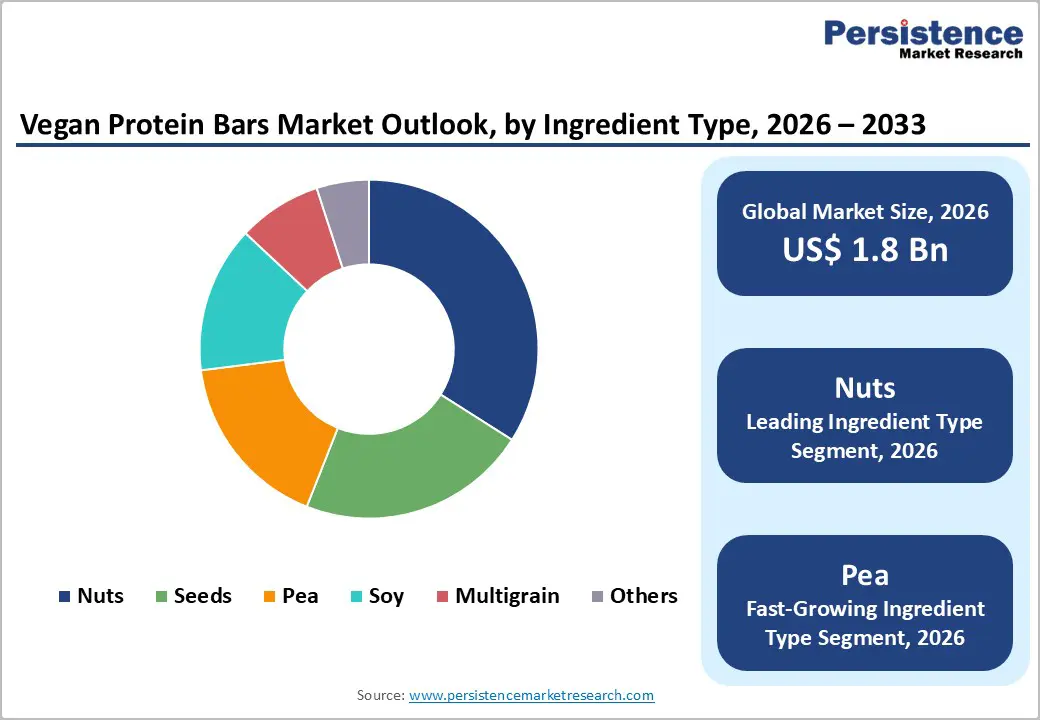

- Dominant Segment: Nuts remain the leading ingredient source with a 35% share in 2025, favored for their whole-food perception and high satiety levels.

- Fastest Growing Segment: Pea protein is the fastest-growing ingredient segment, valued for its high nutritional density and low allergen profile.

- Key Market Opportunity: The integration of nootropics and adaptogens into vegan bars offers a high-margin opportunity to target the mind-body wellness consumer segment.

| Key Insights | Details |

|---|---|

| Vegan Protein Bars Market Size (2026E) | US$ 1.1 Bn |

| Market Value Forecast (2033F) | US$ 2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.3% |

Market Dynamics

Driver - Rising Adoption of Flexitarian and Vegan Lifestyles

Dietary identity is evolving from rigid labels to fluid food choices, creating fertile ground for vegan protein bars. Flexitarian consumers increasingly seek plant-based options that align with health, sustainability, and ethical values without committing to full veganism. Vegan protein bars fit seamlessly into this shift, offering familiar snack formats with plant-forward credentials. As consumers reduce their intake of animal protein, demand for convenient, protein-rich alternatives that support active lifestyles, weight management, and clean-eating goals is rising.

In the United States, brands such as RXBAR Plant and GoMacro have capitalized on this behavioral shift by positioning vegan protein bars as everyday snacks rather than niche health products. Grocery retailers and fitness-oriented outlets increasingly merchandise these bars alongside mainstream nutrition products, reinforcing mass acceptance. This normalization accelerates repeat purchases, expands consumer demographics, and supports long-term market growth as flexitarian eating becomes an enduring lifestyle pattern.

Restraint - Sensory Barriers and Texture Consistency Issues

Taste expectations remain uncompromising in the snack bar category, placing pressure on vegan protein bar formulations. Plant proteins often introduce earthy notes, dryness, or chalky mouthfeel, which can deter first-time buyers. Texture inconsistencies caused by protein crystallization, moisture migration, or fat separation further affect consumer satisfaction, especially compared with traditional dairy-based bars.

Maintaining consistent sensory quality across batches remains a challenge for manufacturers. Natural binders, clean-label sweeteners, and reduced processing limits formulation flexibility, increasing the risk of hardness or crumbliness over shelf life. These sensory barriers elevate product development costs and slow repeat adoption. For many consumers, a single poor eating experience outweighs ethical or nutritional benefits, making texture and flavor optimization critical hurdles for sustained market penetration.

Opportunity - Expansion into Sports Nutrition and Performance Snack Segments

Performance-driven nutrition is redefining perceptions of vegan protein bars. Athletes, gym-goers, and endurance enthusiasts increasingly demand plant-based products that support muscle recovery, energy release, and sustained satiety. Vegan protein bars enriched with complete amino acid blends, functional carbohydrates, and electrolytes are gaining relevance as training-friendly snacks.

This shift opens opportunities for both established brands and startups to reposition vegan protein bars beyond lifestyle snacking. Partnerships with fitness communities, endurance events, and digital training platforms strengthen credibility within sports nutrition. Compact formats, targeted macros, and performance-led messaging allow brands to compete with traditional sports bars. As plant-based performance nutrition gains legitimacy, vegan protein bars can capture incremental demand from consumers seeking clean, ethical, and functional fuel for active routines.

Category-wise Analysis

Sales Channel Insights

Online retail is expected to grow at a CAGR of 17.2% in the vegan protein bars market, reshaping how consumers discover and purchase functional snacks. Digital platforms enable brands to communicate ingredient transparency, nutritional benefits, and sustainability narratives directly to shoppers. Subscription models, bundle offerings, and personalized recommendations drive repeat purchases while reducing dependence on physical shelf space.

Direct-to-consumer websites and online marketplaces support rapid product launches and limited-edition flavors, accelerating innovation cycles. Data-driven insights from online sales allow brands to refine formulations and messaging in real time. Hypermarkets and supermarkets continue to provide scale and visibility for mainstream adoption. Convenience stores support impulse purchases tied to mobility. Pharmacies attract health-focused buyers, while specialty stores reinforce premium and plant-based positioning across targeted consumer segments.

Ingredient Type Insights

Nuts hold approximately 35% market share as of 2025 in the global Vegan Protein Bars Market, driven by their natural protein content, healthy fats, and familiar taste profiles. Almonds, peanuts, and cashews contribute to creamy textures and indulgent mouthfeel, improving consumer acceptance. Their nutritional halo supports positioning as a source of sustained energy and satiety.

Seeds such as pumpkin and sunflower add micronutrients and crunch, though usage remains secondary. Pea protein continues gaining traction for its neutral flavor and amino acid profile. Soy retains functional importance in cost-sensitive formulations, while multigrain blends support fiber-rich positioning. Despite emerging alternatives, nuts remain central due to sensory appeal, nutritional density, and strong consumer trust, anchoring product formulations across premium and mass-market vegan protein bars.

Regional Insights

North America Vegan Protein Bars Market Trends and Insights

North America holds approximately 39% market share in the vegan protein bars market, reflecting deep-rooted health awareness and strong demand for plant-based convenience foods. Consumers increasingly seek high-protein snacks aligned with fitness, weight management, and ethical eating habits. Brands focus on clean ingredients, minimal processing, and indulgent flavors to appeal beyond core vegans. Innovation centers on texture improvement, functional benefits, and premium positioning within everyday snacking occasions across retail, digital, and specialty nutrition channels.

In the United States, demand is shaped by gym culture, on-the-go lifestyles, and growing acceptance of flexitarian diets. Direct-to-consumer brands leverage subscriptions and influencer marketing to build loyalty. Canada shows rising interest in organic, allergen-free, and sustainably packaged bars, supported by strong natural food retail networks. Cross-border brand expansion and product localization continue accelerating category maturity across North America, especially within urban centers and premium grocery formats, serving active consumers seeking plant-based nutrition solutions.

Asia Pacific Vegan Protein Bars Market Trends and Insights

Asia Pacific is expected to show promising growth of 18.1% CAGR, driven by rapid urbanization, rising disposable incomes, and expanding health consciousness. Younger consumers increasingly adopt plant-forward snacking as fitness culture and Western-style convenience foods spread. Brands emphasize affordable formats, localized flavors, and functional nutrition to suit diverse preferences. Digital commerce and social media play a central role in product discovery and brand education across the region, especially among urban millennials and Gen Z consumers.

In India, demand rises from gym-goers and busy professionals seeking convenient protein sources. China shows interest in plant-based nutrition tied to weight management and modern lifestyles. Japan favors clean formulations with subtle flavors and portion control. South Korea sees growth driven by fitness influencers and trendy wellness foods. Regional manufacturers increasingly partner with e-commerce platforms to scale reach and accelerate mainstream acceptance while adapting pricing, taste profiles, and formats for local consumers across markets.

Competitive Landscape

The global vegan protein bars market remains moderately fragmented, characterized by a mix of established nutrition brands and agile plant-based startups. Competition centers on formulation quality, brand storytelling, and lifestyle alignment rather than price alone. Leading players emphasize clean-label ingredients, natural sweeteners, and short ingredient lists to build trust among health-conscious consumers.

Flavor innovation plays a central role, with dessert-inspired and globally influenced profiles enhancing trial rates. Brands increasingly collaborate with athletes, fitness influencers, and sports communities to strengthen performance credibility. Sustainable packaging, third-party certifications, and transparent sourcing reinforce brand values. Many companies prioritize direct-to-consumer channels to control messaging, gather consumer data, and improve margins. This competitive environment rewards agility, authenticity, and continuous product differentiation.

Key Developments:

- In November 2025, ETI Gida Sanayi ve Ticaret A.S. signed a definitive agreement to acquire TRUBAR Inc., strengthening its presence in the global better-for-you and functional protein bar segment through an established U.S. brand.

- In October 2025, L-Nutra expanded its nutrition portfolio with the ProLon L Bar, a plant-based protein bar designed to support muscle health, healthy ageing, and workout performance, aligning science-led nutrition with active lifestyle demand.

- In June 2025, MOSH introduced a new vegan protein bar collection, extending its brain-health positioning into plant-based formats and tapping into rising consumer interest in clean, functional, and ethically aligned snacking.

Companies Covered in Vegan Protein Bars Market

- Kellogg's

- Mondelez International

- Glanbia plc

- PepsiCo Inc.

- The Hain Celestial Group

- Nestlé S.A.

- No Cow

- BellRing Brands Inc.

- NuGo Nutrition

- Warrior

- MisfitBar

- GoMacro

- Others

Frequently Asked Questions

The global vegan protein bars market is projected to be valued at US$ 1.1 Bn in 2026.

Rising Adoption of Flexitarian and Vegan Lifestyles is driving demand for Vegan Protein Bars market.

The Global Vegan Protein Bars market is poised to witness a CAGR of 14.9% between 2026 and 2033.

Expansion into Sports Nutrition and Performance Snack Segments is key opportunity in the vegan protein bar market.

Key industry leaders include Kellogg's, Mondelez International, Glanbia plc, PepsiCo Inc., The Hain Celestial Group, Nestlé S.A., and Others