- Processed Food

- Plant-based Bars Market

Plant-based Bars Market Size, Share, and Growth Forecast 2026 - 2033

Plant-based Bars Market by Product Type (Protein Bars, Granola/Cereal Bars, Energy Bars, Fruit and Nut Bars, Others), by Nature (Organic, Conventional), by Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail), by Regional Analysis, 2026 - 2033

Plant-based Bars Market Share and Trends Analysis

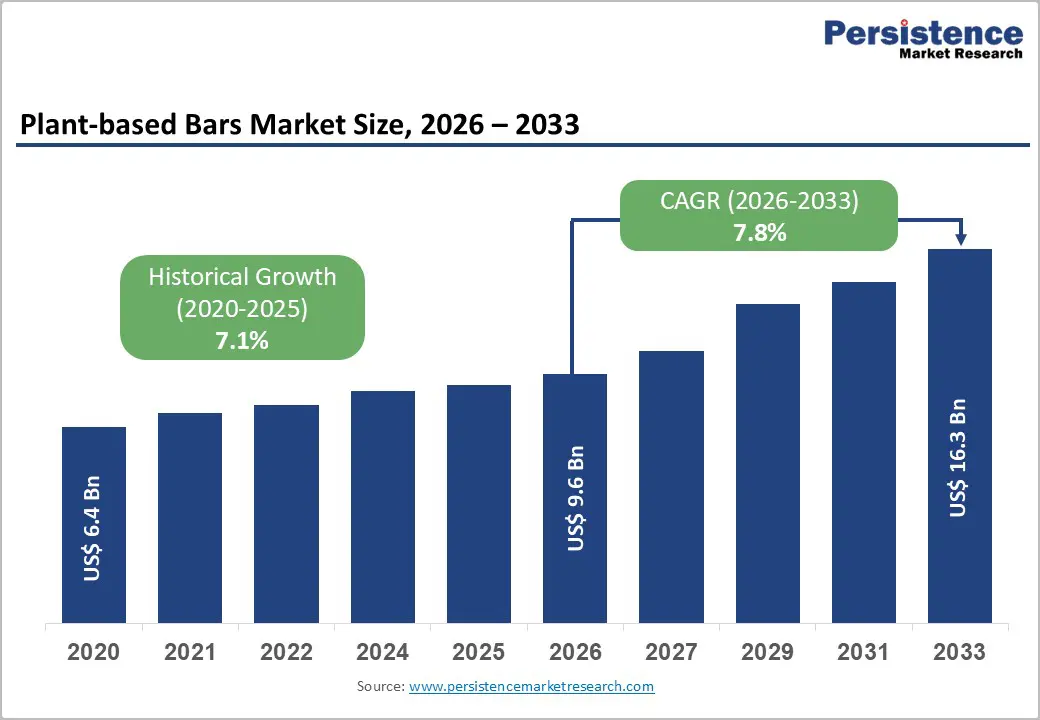

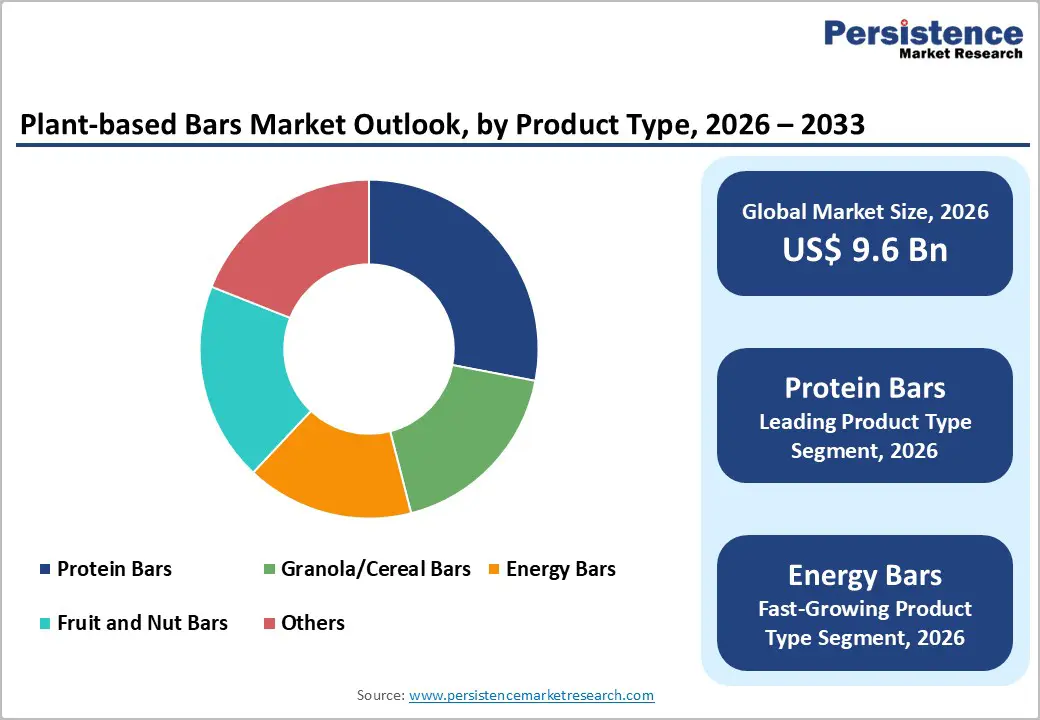

The global plant-based bars market size is expected to be valued at US$ 9.6 billion in 2026 and projected to reach US$ 16.3 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033. Market expansion is driven by rising consumer adoption of plant-forward diets, preference for convenient high-protein snacks, and the mainstreaming of vegan and flexitarian lifestyles in both developed and emerging economies. At the same time, brands are shifting toward clean-label recipes, free-from claims, and functional ingredients such as plant proteins, fibers, adaptogens, and probiotics, helping plant-based bars move from niche health-food channels into mass retail and e-commerce baskets.

Industry data from the Plant Based Foods Association (PBFA) and the Good Food Institute (GFI) show that U.S. retail sales of plant-based foods reached around US$ 8.0 billion in 2022, with plant-based bars alone growing about 13% in value to approximately US$ 202 million, outpacing many conventional snack segments. This performance underscores strong consumer loyalty and repeat purchasing of plant-based products even amid inflationary pressure, supporting the sustained mid-single to high-single-digit growth assumed for plant-based bars through 2033.

Key Market Highlights:

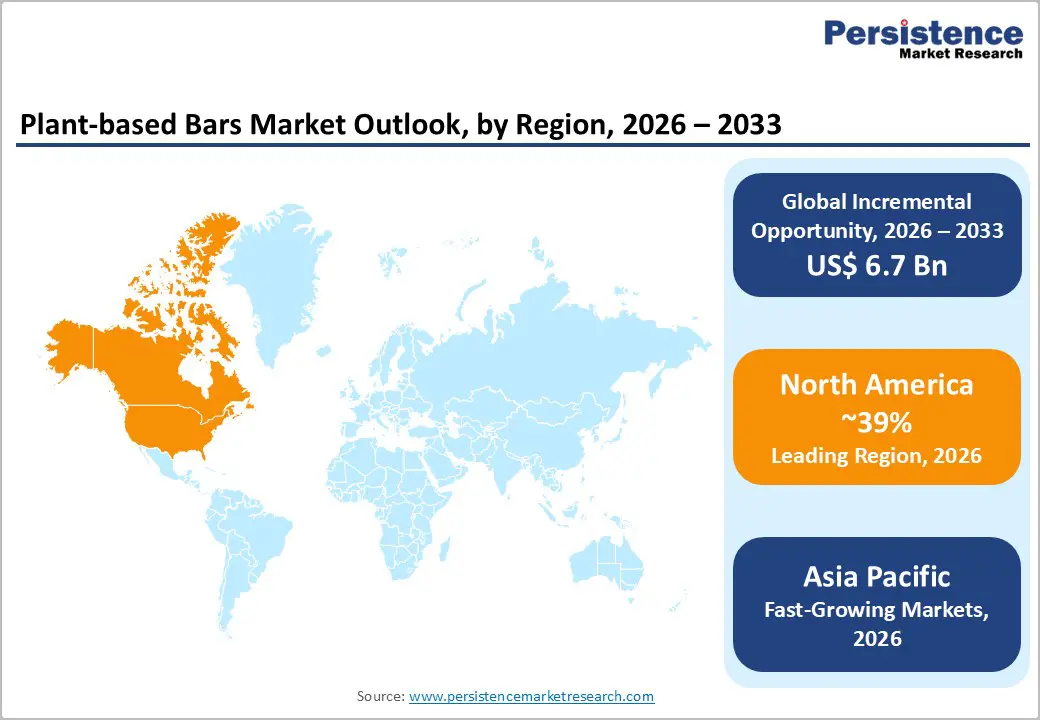

- North America is the leading region in the plant-based bars market, accounting for around 39% of global revenues in 2025, supported by high snack bar penetration, well-developed natural and organic retail channels, and strong consumer engagement with plant-forward, high-protein snacking.

- Asia-Pacific is the fastest-growing region, with the regional snack and confectionery sector valued at about US$ 64 billion and growing around 10% annually, as consumers in China, India, Japan, and ASEAN adopt convenient, healthier snacks, including plant-based bars, alongside the rapid expansion of e-commerce and quick-commerce platforms.

- Among product types, plant-based protein bars dominate with an estimated 28% share in 2025, driven by the convergence of sports nutrition, weight-management, and flexitarian eating trends that favor high-protein, clean-label, and dairy-free bar formats tailored to active lifestyles.

- By nature and channel, conventional plant-based bars and supermarket/hypermarket distribution lead in value share today, while organic bars and online retail are the fastest-growing segments as consumers seek certified, sustainable products and increasingly shift snack purchases to digital channels.

- A key market opportunity lies in developing premium plant-based bars that integrate functional benefits such as energy, gut health, or immune support with organic or sustainably sourced ingredients, low-sugar recipes, and recyclable or compostable packaging, supported by omnichannel go-to-market strategies.

| Key Insights | Details |

|---|---|

|

Plant-based Bars Market Size (2026E) |

US$ 9.6 billion |

|

Market Value Forecast (2033F) |

US$ 16.3 billion |

|

Projected Growth CAGR (2026–2033) |

7.8% |

|

Historical Market Growth (2020–2025) |

7.1% |

DRO Analysis

Drivers - Rising Health Consciousness and Demand for Plant-based, High-protein Snacking

A primary growth driver for the plant-based bars market is the rapid shift toward healthier, high-protein, on-the-go snacks as consumers juggle busy work and lifestyle patterns. Snacking now exceeds US$ 135 billion annually worldwide, with “better-for-you” products growing faster than traditional snacks, according to NielsenIQ (NIQ)’s State of Snacking analysis. Within this context, consumers increasingly prefer snacks rich in protein, fiber, and natural ingredients, which directly benefits plant-based bars positioned around sustained energy, satiety, and weight-management support. In parallel, PBFA and GFI data show that plant-based categories, including bars, have outpaced total food in value growth as shoppers trade from indulgent confectionery toward nutritionally dense alternatives. Plant-based bars using pea, soy, nut, seed, and oat proteins are therefore well-placed to capture demand from fitness-oriented consumers seeking portable, non-dairy protein sources.

Expansion of flexitarian, vegan, and allergy-aware consumer segments

Another powerful driver is the expansion of flexitarian, vegetarian, and vegan populations, as well as heightened awareness of food allergies and intolerances. Global health organizations estimate that hundreds of millions of people live with food allergies, while lactose intolerance is particularly prevalent in East Asian populations, encouraging shifts away from dairy-based products. Industry and advocacy reports referenced by PBFA and GFI indicate that more than 60% of U.S. households now purchase at least one plant-based food item annually, with over 80% of these households returning to buy again, reflecting strong repeat behavior. For many of these shoppers, plant-based bars offer a convenient way to avoid common allergens such as dairy and, in some cases, gluten or peanuts, while still obtaining satisfying taste and texture. Brands are increasingly marketing bars as vegan, gluten-free, non-GMO, and allergen-friendly, broadening the addressable consumer base and reinforcing long-term category growth.

Restraints - Premium Pricing and Affordability Gaps Vs Conventional Snacks

Despite increasing interest in plant-based snacking, premium pricing remains a key restraint on mass adoption, particularly in price-sensitive markets. Data from PBFA’s retail audits show that plant-based products across various categories typically command higher average unit prices than their animal-based counterparts due to elevated ingredient costs, certification expenses, and smaller manufacturing scale. During periods of inflation, consumers often trade down from premium items to lower-priced conventional snack bars or confectionery, which can temporarily slow plant-based bar volume growth even as value sales hold up. This affordability gap is particularly evident in emerging markets, where per-capita snack spending is lower and shoppers are more price-conscious, limiting penetration beyond affluent urban consumers.

Taste, texture, and sugar-content concerns in plant-based formulations

Taste and texture parity with established brands is another challenge, especially for first-time buyers. Early generations of plant-based protein bars sometimes exhibited dense or chalky textures and off-flavors linked to certain plant protein isolates, which discouraged repeat purchases. At the same time, many high-protein bars have relied on added sugars or sugar alcohols to improve palatability, raising concerns among health-conscious consumers focused on blood-sugar management and digestive comfort. NIQ and other snack category analyses highlight growing scrutiny of sugar content, with shoppers increasingly reading labels and seeking lower-sugar options. Manufacturers must therefore invest in R&D to optimize flavor and texture while reducing total sugars, which can increase formulation complexity and cost.

Opportunities - E-commerce, Omnichannel Retail, and Direct-to-Consumer Models

The rapid expansion of e-commerce and omnichannel grocery is one of the most attractive opportunities for plant-based bar brands. PBFA’s latest State of the Marketplace findings show that e-commerce sales of plant-based foods reached about US$ 394 million in 2023, representing 16.4% growth over three years, compared with US$ 8.1 billion in total retail plant-based food sales. Online channels command an estimated 6.8% market share for plant-based foods, significantly higher than in brick and mortar and are growing faster than overall retail. For plant-based bar manufacturers, direct-to-consumer websites, subscription boxes, and online marketplaces enable broader SKU variety, discovery packs, personalization, and storytelling around sustainability and functional benefits. These models help overcome the shelf-space constraints of physical retail, allowing challenger brands to scale nationally or globally with comparatively lower listing fees and more agile marketing.

Premiumization, functional ingredients, and emerging market penetration

A second major opportunity lies in premiumizing plant-based bars through functional ingredients and tailoring offerings to high-growth emerging markets. NIQ’s snacking analyses show that “better-for-you” snack products exhibit a higher multi-year velocity CAGR than conventional items, as consumers increasingly seek snacks that deliver specific health outcomes such as energy, satiety, gut health, or mood support. In parallel, PBFA data confirm robust growth in plant-based categories like creamers, protein powders, and ready-to-drink beverages, many of which emphasize added functional benefits. Bar brands can leverage similar ingredients such as prebiotic fibers, probiotics, plant-based omega sources, and adaptogens to differentiate on performance and justify premium price points. In fast-growing markets across China, India, Japan, and ASEAN, rising middle-class incomes, urbanization, and fitness culture are increasing demand for convenient nutrition solutions, creating headroom for localized plant-based bar flavors that incorporate regional grains, pulses, and botanicals while leveraging competitive regional ingredient supply chains.

Category-wise Analysis

Product Type Insights

Within product types, protein bars are the leading segment in the plant-based bars market, accounting for about 28% share of global revenues in 2025. Their dominance reflects the strong link consumers make between protein intake, satiety, and fitness or weight-management goals, particularly in markets with high levels of gym and sports participation. Innovation tracking from sources such as Innova Market Insights shows that protein-positioned bars account for a significant share of new snack bar launches in key markets, often exceeding 20% of total new bar SKUs. Plant-based protein bars leverage ingredients such as pea, soy, brown rice, nuts, and seeds to deliver double-digit grams of protein per serving, frequently marketed as vegan and dairy-free, aligning with both ethical and health-driven consumer priorities. As mainstream shoppers become more familiar with plant proteins and seek to reduce reliance on animal sources without compromising performance, this segment is expected to retain its leadership.

Distribution Channel Insights

Supermarkets and hypermarkets are the leading distribution channels for plant-based bars, reflecting broader snack bar purchasing patterns in which large-format grocery stores capture the majority of retail value. NIQ’s snacking data indicate that traditional brick and mortar outlets still anchor the global snack market, with shoppers relying on these stores for weekly and top-up missions even as online channels expand. Wide assortments, shelf visibility in both ambient and health-focused aisles, and prominent end-cap or checkout displays support high impulse-purchase rates for bars. Convenience stores also play an important role in immediate consumption and on-the-go occasions, particularly in North America, Europe, and urban Asia. Nevertheless, online retail is the fastest-growing channel for plant-based foods overall; PBFA’s data show plant-based e-commerce sales growing faster than physical retail, reaching US$ 394 million in 2023. For plant-based bars specifically, an omnichannel strategy anchored in supermarkets and hypermarkets, but also aggressively building direct-to-consumer and marketplace presence, is critical to maximizing reach and consumer engagement.

Regional Insights

North America Plant-Based Bars Market Trends and Insights

North America is currently the leading regional market for plant-based bars, with an estimated share of around 39% of global revenues in 2025. The United States accounts for the majority of this value, thanks to high snack bar penetration, strong health and wellness awareness, and mature natural and organic retail infrastructure. PBFA and GFI data show that U.S. retail sales of plant-based foods reached nearly US$ 8.0 billion in 2022, with plant-based bars growing about 13% in value during the same period, one of the fastest-growing plant-based categories. High household penetration and strong repeat rates for plant-based foods underscore the region’s pivotal role in driving innovation and scaling new plant-based bar formats.

The regulatory and innovation ecosystem further strengthens North America’s leadership. The U.S. Food and Drug Administration (FDA) provides labeling oversight for plant-based products, while the USDA Organic seal underpins trust in certified organic snack bars. Large multinationals and agile start-ups coexist in this environment, deploying advanced R&D capabilities and co-manufacturing partnerships to develop bars with novel plant proteins, reduced sugar content, and functional claims. Sustainability initiatives, such as flexible packaging for store-drop-off or recycling, used by brands like Nature Valley, are increasingly adopted, aligning with corporate ESG goals and retailer packaging mandates. Together, these factors position North America as both the largest and one of the most influential markets for plant-based bars globally.

Asia Pacific Plant-Based Bars Market Trends and Insights

Asia Pacific is the fastest-growing region for plant-based bars, underpinned by rapid urbanization, rising disposable incomes, and the proliferation of modern retail and e-commerce channels. NIQ’s Asia Pacific State of Snacking 2024 highlights that the regional snack and confectionery market valued at about US$ 64 billion is experiencing around 10% growth in both value and volume, driven by a strong preference for convenient, healthier, and mood-boosting snacks. Consumers in markets such as China, Japan, and Singapore are increasingly open to trying new snack brands and products, with more than 70% of surveyed consumers eager to experiment with novel offerings. Within this context, plant-based and dairy-free bars appeal to health-conscious urban professionals and students who use them as breakfast replacements, study snacks, and post-workout nutrition.

Manufacturing and sourcing advantages also underpin Asia Pacific’s growth trajectory. The region is a major producer of pulses, grains, nuts, and seeds that serve as core ingredients in plant-based bars, enabling local and multinational firms to develop cost-competitive, regionally tailored products. Government nutrition and wellness initiatives in China, India, and ASEAN, many of which emphasize reduced sugar intake and higher consumption of whole grains and plant proteins, indirectly support plant-based snack innovation. As cross-border e-commerce, quick-commerce, and specialty health-food platforms continue to expand, plant-based bar brands gain access to a wide range of consumers across urban and semi-urban areas, solidifying Asia Pacific’s status as the fastest-growing regional market for plant-based bars.

Competitive Landscape

The plant-based bars market is highly competitive and fragmented, driven by strong consumer demand for healthier, convenient snack options. Market players compete through continuous product innovation, focusing on clean-label ingredients, high plant-protein content, and functional benefits such as energy and digestive health. Sustainability, including eco-friendly packaging and ethical sourcing, has become a key differentiator. The rise of e-commerce and direct-to-consumer channels has intensified competition by enabling new entrants to scale quickly.

Key Developments:

- In July 2025, MOSH extended its brain-focused bar line with the introduction of a vegan protein bar collection. It targets physical and cognitive health through its formulation. The vegan bars contain the company’s signature brain blend, which includes flaxseed, organic lion’s mane, Cognizin Citicoline, ashwagandha, and other ingredients.

- In March 2025, Vybey extended its presence in the snacking category with the launch of its Complete Nutrition bar range, its new plant-based protein bars. The range was added to the company’s existing portfolio, which includes a nootropic coffee alternative blend and meal replacement shakes.

- In February 2026, Ingredion launched a new pea protein solution, VITESSENCE® Pea 100 HD, specifically designed for cold-pressed plant-based bars to address texture-related challenges such as hardness and gritty mouthfeel. The innovation helps maintain softness throughout shelf life, while improving taste, smooth texture, and sensory appeal.

Companies Covered in Plant-based Bars Market

- Kellogg Company

- Greens Gone Wild, LLC

- 88 ACRES

- General Mills Inc.

- MadeGood

- Rise Bar

- GNC Holdings, LLC

- GoMacro, LLC

- Clif Bar & Company

- Växa Bars

- LoveRaw

- ALOHA

- RXBAR

- Kind LLC

- ONE Brands

- LÄRABAR

Frequently Asked Questions

The global plant-based bars market size is expected to reach approximately US$ 9.6 billion in 2026, up from about US$ 6.4 billion in 2020, reflecting a historical CAGR of around 7.1% and establishing a solid base for continued growth through 2033.

Key demand drivers include rising health and wellness awareness, higher protein and fiber intake goals, growth in flexitarian and vegan populations, increased concern about food allergies and intolerances, and the need for convenient, on‑the‑go snacks that align with ethical, environmental, and clean‑label expectations.

North America currently leads the global plant-based bars market, accounting for roughly 39% of total revenues in 2025, supported by high snack bar consumption, advanced natural and organic retail infrastructure, a strong innovation ecosystem, and substantial contributions from the United States to overall plant-based foods sales.

A major opportunity lies in combining functional nutrition (for example, bars supporting energy, gut health, or immune function) with organic or sustainably sourced ingredients, low‑sugar formulations, and recyclable or compostable packaging, particularly when delivered through fast‑growing e‑commerce and omnichannel grocery models that enhance discovery and repeat purchases.

Prominent players include Kellogg Company, Greens Gone Wild, LLC, 88 ACRES, General Mills Inc., MadeGood, Rise Bar, GNC Holdings, LLC, GoMacro, LLC, Clif Bar & Company, Växa Bars, and LoveRaw, alongside other brands such as ALOHA, RXBAR, Kind LLC, ONE Brands, and LÄRABAR that are strengthening their plant-based or better‑for‑you bar portfolios.