- Technology

- Automotive Predictive Analytics Market

Automotive Predictive Analytics Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Predictive Analytics Market By Application (Predictive Maintenance, Vehicle Telematics, Driver & Behavior Analytics, Others), Component (Software, Services, Hardware), Vehicle Type (Passenger Cars, Commercial Vehicles, Others), and Regional Analysis for 2025 - 2032

Automotive Predictive Analytics Market Share and Trends Analysis

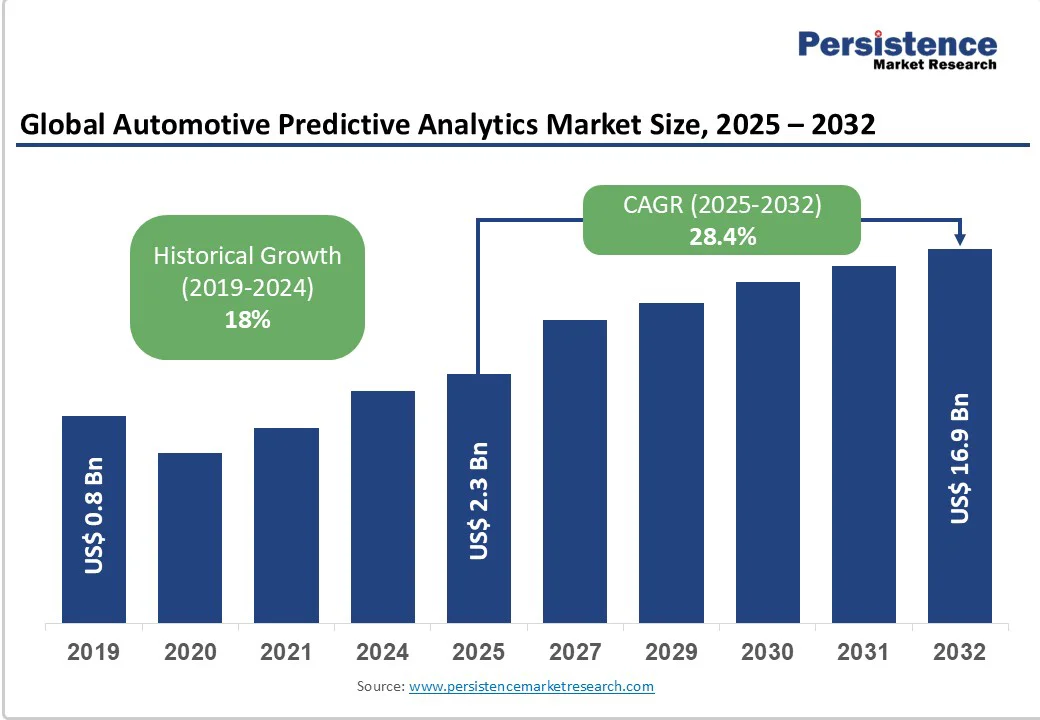

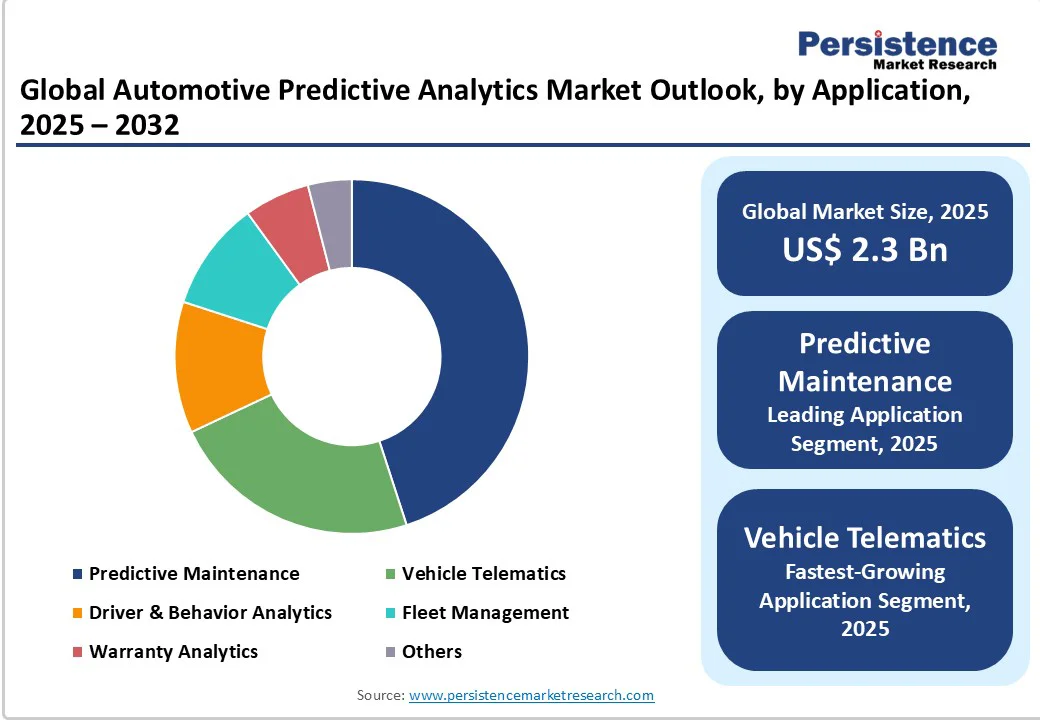

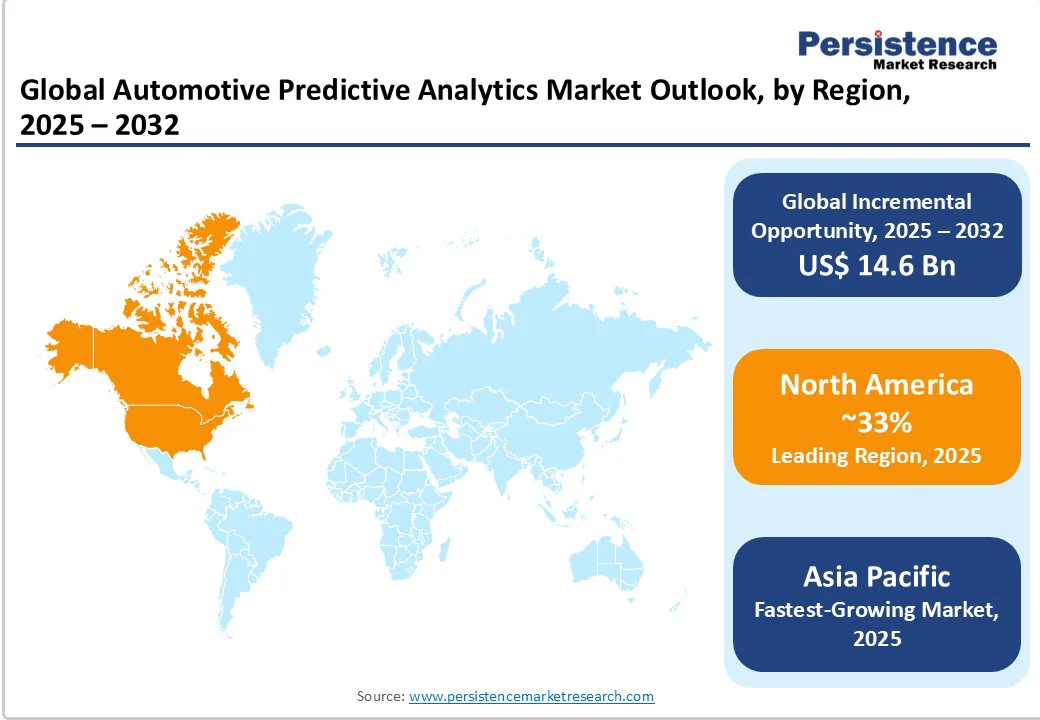

The global automotive predictive analytics market size is likely to be valued at US$2.3 Billion in 2025. It is estimated to reach US$16.9 Billion by 2032, growing at a CAGR of 28.4% during the forecast period 2025 - 2032, driven by the increasing integration of AI and machine learning (ML) in connected vehicles, escalating adoption of predictive maintenance solutions, and expanding telematics and usage-based insurance models.

The rising penetration of electric and autonomous vehicles, which rely heavily on real-time data analytics for performance optimization and safety, is significantly driving demand for advanced analytics in automobiles across price segments.

Key Industry Highlights

- Dominant & Fastest-growing Applications: Predictive maintenance is poised to lead with a 2025 revenue share near 45%, while vehicle telematics is the fastest-growing segment at a CAGR of approximately 31% through 2032.

- Leading & Fastest-growing Components: The software component dominates with about 51.7% market share in 2025; services are the fastest-growing, expected to see CAGR above 29% during 2025 - 2032.

- Dominant & Fastest-growing Vehicle Types: Passenger cars command around 40% of the market in 2025, while EVs are set to grow the fastest from 2025 to 2032.

- Regional Leadership: North America leads with about 33% of the market share in 2025, whereas the Asia Pacific market will grow the fastest at over 31% CAGR between 2025 and 2032.

- Governmental Incentives: U.S. federal investments of US$800 Million underpin connected vehicle pilot programs, enhancing V2X adoption and predictive analytics deployment in traffic management.

- Regulatory Push: Europe’s regulatory harmonization and AI safety oversight strengthen market expansion, with Germany’s and the U.K.’s initiatives advancing intelligent vehicle systems.

- Key Developments: Major industry moves include the engineering of advanced analytics, forging of cloud platform partnerships, and increasing regional infrastructure investments in North America and APAC.

- July 2025: Malaysia Automotive Robotics and IoT Institute (MARii) partnered with Petronas Global Technical Solutions to introduce ADaPTiV, an AI-powered predictive maintenance platform that collects real-time vehicle data from IoT sensors to forecast component failures and recommend preventive actions, enabling condition-based maintenance.

| Key Insights | Details |

|---|---|

| Automotive Predictive Analytics Market Size (2025E) | US$2.3 Bn |

| Market Value Forecast (2032F) | US$16.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 28.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 18% |

Market Environment & Opportunity Analysis

Integration of V2X Communication Enabling Enhanced Predictive Capabilities

The integration of vehicle-to-everything (V2X) communication, including vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) technologies, is emerging as a niche yet highly impactful driver of the market. Enabled by dedicated short-range communications (DSRC) and cellular V2X (C-V2X), these technologies facilitate real-time data exchange among vehicles and surrounding infrastructure, significantly broadening the data pool used for predictive modeling.

For instance, the U.S. Department of Transportation has invested millions in state-level pilot programs to test V2X communication systems, which have demonstrated quantifiable reductions in accident rates through improved traffic flow forecasting and incident avoidance.

The development of such a data-rich environment enables predictive analytics platforms to anticipate events, such as sudden braking or hazardous road conditions, well before traditional sensors detect them, thereby enhancing both safety and operational efficiency.

The impact of V2X extends beyond accident prevention to congestion mitigation and environmental benefits by optimizing route planning and reducing idle times. Regulatory encouragement, including state mandates for V2X adoption in several U.S. states and pilot projects worldwide, is accelerating the market’s growth trajectory.

Data Privacy and Cybersecurity Regulatory Hurdles

A formidable restraint on market growth is heightened regulatory scrutiny of data privacy and the complexities of cybersecurity management, which introduce operational and compliance challenges. Predictive analytics systems inherently require continuous collection and processing of sensitive vehicle and driver data, including geolocation, biometric information, and real-time behavioral patterns, making them susceptible to breaches and misuse.

Governments and regulatory bodies, such as the U.S. Federal Trade Commission (FTC) and the General Services Administration (GSA), have issued stringent frameworks mandating encryption, anonymization, and secure communication protocols.

Compliance with these evolving regulations entails substantial investment in cybersecurity infrastructure and stringent data governance policies, potentially increasing operational costs for analytics providers. The risk of data breaches or non-compliance penalties could undermine consumer trust and slow adoption rates, particularly in cloud-based analytics environments.

Incorporation of Predictive Analytics into Electric Vehicle (EV) Battery Management

The rapidly growing EV segment presents a lucrative and niche opportunity within the automotive predictive analytics market, especially in battery health diagnostics and energy optimization. EV battery performance substantially influences vehicle range, charging behavior, and the overall lifecycle costs, making predictive analytics an indispensable tool for manufacturers, fleet operators, and end users.

With global EV sales surging every year and with EVs expected to command a rising share of new vehicle sales over the next few years, market estimates suggest that battery management-related predictive analytics could represent business opportunities in the range of US$1.5 billion to US$2 billion.

Analytics tools optimize battery thermal management, forecast degradation, and enable dynamic charging schedules, directly enhancing vehicle reliability and customer satisfaction. Government incentives for EV adoption and investments in charging infrastructure further accelerate digital integration.

Category-wise Analysis

Application Insights

Predictive maintenance currently dominates the application landscape, holding an estimated 45% market share in 2025. This dominance stems from the mounting need for cost savings through reduced unplanned downtime and optimized vehicle servicing schedules.

Fleet operators and OEMs are increasingly relying on predictive maintenance solutions powered by AI and machine learning, which analyze sensor data to anticipate component failures before they occur. The impact of this application is especially pronounced in commercial vehicle fleets, where operational efficiency is critical.

In contrast, vehicle telematics is identified as the fastest-growing application segment, with an anticipated CAGR nearing 31% from 2025 through 2032. Telematics leverages real-time data to monitor driver behavior, fuel consumption, and vehicle location, enabling usage-based insurance models and tailored fleet management solutions.

This surge is propelled by insurers seeking refined risk assessment tools and fleet managers aiming for enhanced safety compliance. Driver and behavior analytics also gain momentum by integrating biometric and environmental data to improve safety protocols.

Component Insights

Software is expected to command approximately 51.7% of the automotive predictive analytics market revenue share in 2025. This segment encompasses core data analytics platforms, AI algorithms, and cloud computing infrastructure, all essential for handling vast volumes of sensor-generated data.

Software platforms are evolving toward modular, scalable architectures, enabling OEMs and tier-1 suppliers to deploy solutions seamlessly across vehicle models and geographies.

The services segment is likely to be the fastest-growing, with a high CAGR during 2025 - 2032. Services include system integration, predictive algorithm customization, deployment consulting, and lifecycle support, reflecting the growing complexity of automotive digital ecosystems.

As vehicle data generation intensifies and regulatory compliance becomes more stringent, industry players are increasingly demanding end-to-end managed services to ensure system robustness and continuous optimization.

Vehicle Type Insights

Passenger cars will remain the largest vehicle segment, with an estimated 40% share in the 2025 automotive predictive analytics market. This leadership is attributed to the broad consumer base adopting connected-car technologies and advanced safety systems enabled by predictive analytics. OEMs are embedding multiple sensor clusters in passenger vehicles to improve diagnostics, driver assistance, and infotainment services.

EVs are anticipated to be the fastest-growing segment, with an exceedingly high CAGR through 2032, owing to their reliance on complex battery systems that necessitate advanced predictive analytics for battery management, energy optimization, and predictive thermal regulation.

The accelerating adoption of EVs, driven by environmental policies and incentives, reinforces this growth trajectory. Commercial vehicles, while maintaining a decent market share in 2025, benefit substantially from predictive analytics through enhanced fleet management, optimized routing, and reduced maintenance costs, positioning them as strategic adopters of intelligent analytics solutions to improve operational efficiency.

Regional Insights

North America Automotive Predictive Analytics Market Trends

North America dominates the automotive predictive analytics market, driven mainly by robust investments and technological advancements in the U.S. The region is anticipated to account for approximately 33% of global market revenue in 2025. The U.S. federal government’s commitment to funding connected vehicle programs, such as the US$800 million initiative supporting V2X technology pilots, fuels this growth.

North America benefits from a mature innovation ecosystem, characterized by a high concentration of technology giants, OEMs, and telematics service providers that collaboratively advance connected vehicle software and predictive analytics solutions. Regulatory frameworks favoring V2X adoption, cybersecurity mandates, and data privacy laws create an environment that balances innovation with risk management.

Private-sector ventures and startups focusing on AI-driven telematics and predictive maintenance are attracting significant venture capital and strategic partnerships. Investment trends reveal an increasing allocation toward cloud infrastructure upgrades and edge computing to support real-time analytics and enhance data processing speed.

Europe Automotive Predictive Analytics Market Trends

Europe is expected to account for around 24% of the automotive predictive analytics market revenue in 2025, led by Germany, the U.K., France, and Spain. The European Union (EU)’s regulatory harmonization initiatives provide consistent AI safety standards, data protection regulations, mainly GDPR compliance, and cybersecurity directives across member states, facilitating a unified market for automotive OEMs and technology suppliers.

Programs such as Germany’s Digital Testbed Autobahn emphasize real-world implementation of predictive analytics in connected vehicles, ensuring scalability and safety validation. The increasing adoption of EVs in Europe, driven by stringent emissions targets and financial incentives, further elevates demand for predictive analytics tailored to battery and energy management.

Asia Pacific Automotive Predictive Analytics Market Trends

Asia Pacific is the fastest-growing regional market for automotive predictive analytics, with a CAGR of close to 31% through 2032. China leads this growth, supported by aggressive government policies promoting smart city infrastructure, EV adoption, and vehicle connectivity aligned with the country’s New Energy Vehicle (NEV) mandates.

Japan’s focus on mobility innovation and advanced testing of autonomous and connected vehicles in real-world corridors further supports the adoption of analytics. India and ASEAN nations contribute through rapidly growing automotive markets and the adoption of telematics in commercial fleets.

The regional market also benefits from manufacturing advantages, local supply chains for sensors and semiconductors, and growing digitization of transport systems. Investment trends indicate increased funding in sensor technology, cloud computing capabilities, and AI-based analytics startups.

Infrastructure developments promoting V2X communication and integrated vehicle-road-cloud ecosystems are fostering advanced predictive analytics platforms, particularly for fleet management and electric mobility solutions across market segments.

Competitive Landscape

The global automotive predictive analytics market features a moderately consolidated structure, with the top 10 players commanding approximately 65% market share. Leading multinational technology corporations such as IBM Corporation, Microsoft Corporation, and SAP SE dominate through comprehensive AI, cloud computing, and analytics service portfolios that cater to OEMs and fleet operators alike.

Tier-1 automotive suppliers such as Continental AG, Robert Bosch GmbH, and ZF Friedrichshafen AG leverage deep industry expertise to embed predictive capabilities directly into vehicle components and telematics systems. Market competition is characterized by strategic collaborations aiming for technological convergence, enhanced data interoperability, and bundled offerings combining software and managed services.

Key Industry Developments

- In August 2025, RuggON, a subsidiary of Ubiqconn Technology, launched the Vortex VMC, a rugged vehicle-mount computer for real-time data processing and predictive fleet analytics. Powered by Intel’s Raptor Lake Core i5 processor, it supports 5G, LTE, Wi-Fi, and Iridium satellite connectivity. The device features built-in IMU sensors, runs Windows 11 IoT Enterprise, and enables AI-driven driver behavior and asset protection analytics.

- In August 2025, Force Motors, in partnership with Intangles, launched Force iPulse, an AI-driven connected vehicle platform delivering real-time fleet intelligence and predictive diagnostics for its commercial vehicles. Factory-installed or available as an aftermarket solution, it provides insights into driver behavior, fuel efficiency, and system health to prevent unplanned downtime.

- In July 2025, Vinli partnered with Stellantis to launch a connected-car platform that provides real-time insights into vehicle health, driver behavior, and predictive maintenance, enabling proactive service and efficient fleet management.

Companies Covered in Automotive Predictive Analytics Market

- IBM Corporation

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- PTC, Inc.

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- SAS Institute Inc.

- Cloud Software Group, Inc.

- NXP Semiconductors

- Aptiv PLC

Frequently Asked Questions

The automotive predictive analytics market is projected to reach US$2.3 Billion in 2025.

The increasing integration of AI and machine learning (ML) in connected vehicles, escalating adoption of predictive maintenance solutions, and expanding telematics and usage-based insurance models are driving the predictive analytics market.

The predictive analytics market is poised to witness a CAGR of 28.4% from 2025 to 2032.

The rising penetration of electric and autonomous vehicles, which rely extensively on real-time data analytics for performance optimization and safety, is creating unprecedented market opportunities.

IBM Corporation, SAP SE, and Microsoft Corporation are some of the key players in the predictive analytics market.