- Automotive Components & Materials

- Automotive Interconnecting Shaft Market

Automotive Interconnecting Shaft Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Interconnecting Shaft Market by Product Type (Single piece propeller shaft, Multi piece propeller shaft), by Design Type (Hollow shaft, Solid shaft), by Axle Position type (Front axle, Rear axle), by Application (Passenger vehicle, Light commercial vehicle, Heavy commercial vehicle), by Regional Analysis, 2026-2033

Automotive Interconnecting Shaft Market Size and Trend Analysis

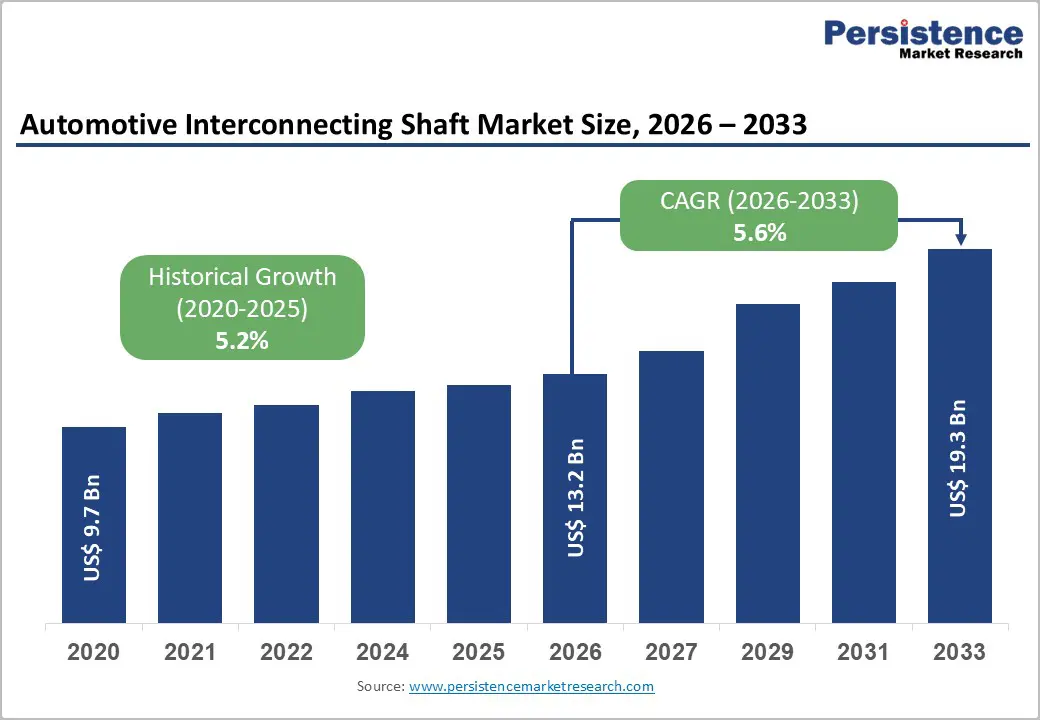

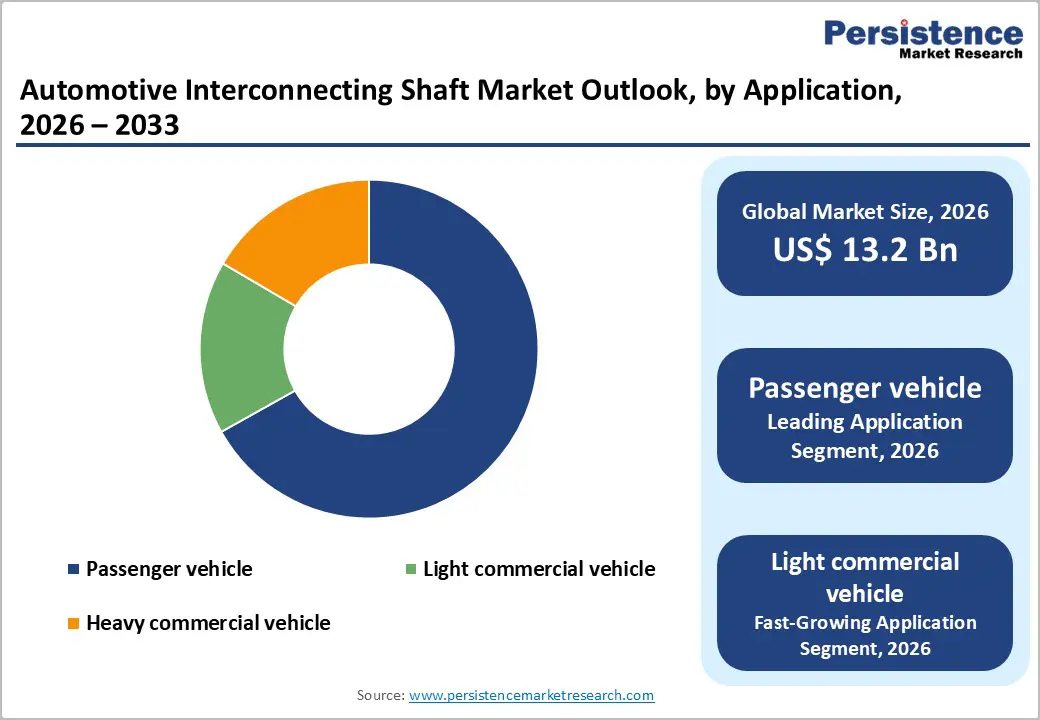

The global Automotive Interconnecting Shaft market size is expected to be valued at US$ 13.2 billion in 2026 and projected to reach US$ 19.3 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The automotive interconnecting shaft market is experiencing steady growth driven by sustained vehicle production, widespread electric vehicle adoption requiring specialized driveline architectures, and escalating demand for lightweight materials to improve fuel efficiency and reduce emissions. The transition toward electrification is fundamentally transforming traditional propeller shaft designs, with electric vehicles increasingly deploying direct-drive systems and integrated e-axles requiring specialized interconnecting shaft solutions engineered for unique torque characteristics and dimensional constraints. Regulatory mandates including EPA emission standards, Euro 6 compliance requirements, and accelerating investments in lightweight composite materials are creating sustained demand for advanced propeller shaft solutions incorporating carbon fiber and aluminum alloys designed to maximize performance while minimizing vehicle mass.

Key Market Highlights

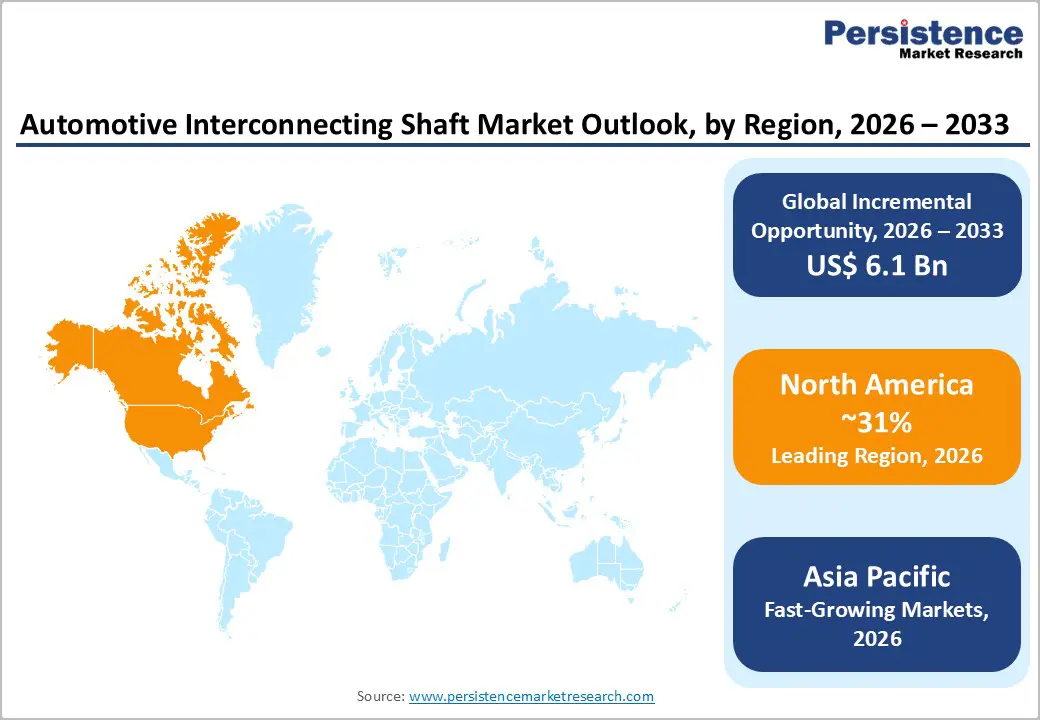

- Leading Region: North America maintains significant market position with approximately 31% regional share, driven by substantial vehicle production, advanced manufacturing capabilities, stringent regulatory standards, and strong emphasis on lightweight component adoption supporting interconnecting shaft market expansion.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market with CAGR of 7.4% during 2026-2033, fueled by explosive vehicle production growth, government manufacturing incentives, aggressive electric vehicle adoption, and establishment of propeller shaft manufacturing facilities throughout China, India, and Southeast Asia.

- Dominant Segment: Hollow Shaft designs capture the largest design segment with approximately 68% market share in 2025, reflecting automotive industry-wide emphasis on weight reduction, improved fuel efficiency, and superior performance characteristics achievable through hollow propeller shaft architectures.

- Fastest Growing Segment: Multi-piece Propeller Shafts represent the fastest-growing product segment with CAGR of 7.2% during 2026-2033, driven by manufacturing flexibility, cost-effectiveness, and modular design approaches enabling efficient production across diverse vehicle platforms.

- Key Market Opportunity: Integration of Advanced Materials and Smart Monitoring Technologies represents the most significant opportunity, enabling manufacturers developing lightweight interconnecting shaft solutions incorporating carbon fiber composites, AI-driven design optimization, and IoT-based predictive maintenance capabilities addressing EV and commercial vehicle electrification requirements.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 13.2 Billion |

| Market Value Forecast (2033F) | US$ 19.3 Billion |

| Projected Growth CAGR (2026-2033) | 5.6% |

| Historical Market Growth (2020-2025) | 5.2% |

Market Dynamics

Market Growth Drivers

Rising Global Vehicle Production and Electric Vehicle Transition

Global vehicle production continues expanding with ASEAN manufacturing representing particularly high-growth opportunity as production facilities relocate from mature markets seeking lower-cost manufacturing regions with favorable regulatory environments. The Asia-Pacific automotive propeller shaft market currently accounts for 56% of global production volume, driven by Chinese manufacturing dominance, Indian market expansion, and ASEAN nations increasingly attracting foreign direct investment through competitive labor costs and government incentives. Electric vehicle production is accelerating exponentially with EV sales projected to represent 35-40% of total vehicle sales by 2030 in developed markets, creating specialized demand for interconnecting shaft solutions optimized for electric drivetrain architectures. The EV transition creates opportunities for propeller shaft manufacturers to develop innovative solutions addressing unique challenges including reduced drivetrain noise, simplified single-speed transmission requirements, and integrated e-axle designs combining motors, power electronics, and drivetrain functionality in compact assemblies. Commercial vehicle electrification is advancing rapidly with heavy commercial vehicle manufacturers including Volvo, Scania, and Daimler introducing electric models requiring specialized interconnecting shaft designs engineered for maximum torque delivery from electric motors.

Escalating Demand for Lightweight Materials and Fuel Efficiency

Automotive manufacturers face intensifying pressure to reduce vehicle mass to achieve stringent emission regulations and improve fuel efficiency across model portfolios, creating exceptional opportunities for lightweight interconnecting shaft solutions. Carbon fiber and advanced aluminum alloys are increasingly replacing traditional steel in propeller shaft manufacturing, with research demonstrating 12% weight reduction achievable through optimized lightweight design while maintaining structural integrity and meeting durability requirements. Premium and luxury vehicle manufacturers are prioritizing lightweight driveline components as differentiation strategy, supporting premium pricing justifications for sophisticated interconnecting shaft designs incorporating composite materials and advanced manufacturing processes. Lightweight interconnecting shaft solutions reduce overall vehicle mass, improving acceleration performance, extending driving range for electric vehicles, and reducing fuel consumption across traditional internal combustion engine platforms. Government regulations including CAFE standards in the United States, EU emission regulations, and emerging carbon pricing mechanisms are establishing economic incentives supporting widespread adoption of lightweight components throughout vehicle architectures.

Market Restraints

Structural Industry Challenges and Supply Chain Vulnerabilities

The automotive interconnecting shaft market faces substantial challenges from supply chain disruptions affecting raw material availability, specialized manufacturing capabilities, and labor constraints limiting production capacity expansion. Rising costs for carbon fiber, aluminum alloys, and specialty steels create pricing pressure on manufacturers already confronting compressed margins through intense competitive rivalry among established suppliers. Small and medium-sized manufacturers struggle to invest in specialized equipment required for carbon fiber manufacturing and advanced composite processing, constraining market entry and limiting competitive differentiation opportunities within concentrated supplier landscape. Raw material price volatility, particularly for high-strength steel and carbon fiber, creates uncertainty in cost structures and margin management, forcing manufacturers to implement complex hedging strategies and long-term supply agreements to stabilize procurement costs.

Electric Vehicle Transition Disruption and Traditional Drivetrain Displacement

The accelerating shift toward electric vehicles equipped with direct-drive systems and integrated e-axles fundamentally disrupts traditional propeller shaft market by eliminating interconnecting shaft requirements from conventional rear-wheel-drive architectures. EV adoption is displacing traditional multi-piece propeller shaft designs with simplified single-piece solutions or complete elimination of separate interconnecting shafts through integrated drivetrain architectures. The automotive drive shaft market faces structural headwinds as EV penetration increases, with manufacturers requiring substantial technology investment and product portfolio transformation to remain competitive amid shifting platform architecture requirements.

Market Opportunities

Integration of Advanced Materials and Smart Monitoring Technologies

Advanced material science innovations including carbon fiber reinforced polymers (CFRP), aluminum-lithium alloys, and ceramic composite materials present substantial opportunities for manufacturers developing next-generation interconnecting shaft solutions optimized for extreme performance and lightweight requirements. Manufacturers implementing AI-driven design optimization and machine learning algorithms can accelerate product development cycles, optimize performance characteristics, and achieve superior manufacturing efficiency compared to traditional engineering approaches.

Smart interconnecting shafts incorporating embedded sensors, wireless communication capabilities, and integrated diagnostics are emerging as differentiated solutions commanding premium positioning within high-performance and commercial vehicle segments. The integration of Industry 4.0 technologies including digital twins, artificial intelligence, and advanced analytics enables manufacturers to optimize production efficiency, reduce defects, and accelerate new product introduction supporting market expansion within fast-growing EV and commercial vehicle segments.

Expansion into Commercial Vehicle and Specialized Applications

Commercial vehicle operators increasingly prioritize reliability, extended maintenance intervals, and superior performance characteristics, creating opportunities for advanced interconnecting shaft solutions engineered specifically for demanding operational environments. Heavy commercial vehicle manufacturers including Volvo, Scania, MAN, and Daimler are investing substantially in electric powertrain development, requiring specialized propeller shaft solutions optimized for electric motor torque characteristics, integration with advanced transmission systems, and enhanced reliability supporting demanding vocational applications.

Off-road vehicle and specialized vehicle applications including construction equipment, mining machinery, and agricultural vehicles require durable interconnecting shaft solutions tolerating extreme operational conditions and substantial angular misalignment. Regional manufacturing expansion in India, Vietnam, Thailand, and Indonesia supported by government incentives and infrastructure development is creating opportunities for propeller shaft manufacturers establishing localized production capacity supporting growing regional demand. Defense and aerospace applications demanding precision engineering, extreme reliability, and specialized material specifications represent high-margin market segments where advanced manufacturers can establish premium positioning through specialized capabilities and compliance with stringent security requirements.

Category-wise Insights

Product Type Analysis: Multi-piece Propeller Shaft

Multi-piece propeller shafts are the fastest-growing product segment, projected to expand at a CAGR of 7.2% during 2026–2033 and reach about 58% market share by 2033. Growth is driven by OEM preference for modular driveline designs that improve packaging flexibility and manufacturing efficiency. These shafts effectively accommodate transmission misalignment, suspension movement, and assembly tolerances through slip joints and spline mechanisms. Widely adopted in passenger and light commercial vehicles, multi-piece designs offer an optimal balance of cost, durability, and performance. Advances in precision welding, spline machining, and dynamic balancing allow multi-piece shafts to meet stringent performance standards while reducing inventory complexity and supporting efficient aftermarket supply.

Design Type Analysis: Hollow Shaft

Hollow shaft designs dominate the market with approximately 68% share in 2025, reflecting industry focus on vehicle weight reduction and efficiency improvement. By lowering rotational mass, hollow shafts enhance drivetrain responsiveness and reduce power losses compared to solid alternatives. High-strength steel and alloy materials enable superior strength-to-weight ratios while achieving weight savings of 15–20%. Adoption is widespread across vehicle segments due to proven durability and scalable manufacturing processes. Precision balancing and advanced quality control requirements also create competitive differentiation for manufacturers with strong production capabilities.

Application Analysis: Passenger Vehicle

The Passenger Vehicle segment represents the leading application category, capturing approximately 62% market share in 2025, driven by global vehicle production concentration in passenger car platforms serving consumer markets across developed and emerging economies. Passenger vehicle manufacturers prioritize cost-effectiveness, lightweight design, and refined drivetrain characteristics, establishing interconnecting shaft specifications balancing performance, durability, and manufacturing efficiency. The global passenger vehicle market includes diverse platforms from compact city cars through luxury sedans and high-performance sports vehicles, each with specialized interconnecting shaft requirements reflecting platform architecture, performance targets, and cost structures. The transition toward electric passenger vehicles is accelerating adoption of specialized interconnecting shaft designs optimized for direct-drive systems, integrated e-axles, and simplified drivetrain architectures differentiating EV platforms from traditional internal combustion engine vehicles.

Regional Insights

North America Automotive Interconnecting Shaft Market Trends and Insights

North America maintains a significant market position with approximately 31% regional share, driven by substantial vehicle production, advanced manufacturing capabilities, and regulatory pressures supporting lightweight component adoption. The United States automotive industry centered in Michigan, Ohio, and Texas maintains sophisticated manufacturing infrastructure, advanced engineering capabilities, and strong supply chain integration enabling competitive positioning in interconnecting shaft manufacturing. EPA emissions standards and CAFE fuel economy regulations create regulatory tailwinds supporting adoption of lightweight interconnecting shaft solutions across domestic and imported vehicle portfolios sold throughout the North American market.

Mexican manufacturing expansion including establishment of major automotive assembly facilities by Ford, General Motors, Stellantis, and foreign OEMs is driving sustained demand for propeller shaft components from regional suppliers. Canadian automotive sector including major manufacturing hubs in Ontario and Quebec supports interconnecting shaft production through integrated supply chains and established OEM relationships. The region’s emphasis on electric vehicle adoption driven by Biden administration policies and Canada’s net-zero commitments is creating demand for advanced propeller shaft solutions addressing EV drivetrain requirements and supporting market expansion through technological differentiation.

Europe Automotive Interconnecting Shaft Market Trends and Insights

Europe represents a mature and technologically advanced interconnecting shaft market with approximately 22% regional share, characterized by stringent emissions standards, emphasis on lightweight materials, and advanced manufacturing capabilities concentrated in Germany, Italy, and France. Germany maintains dominant position as global automotive engineering center with Mercedes-Benz, BMW, Volkswagen, Audi, and Porsche driving innovation in advanced interconnecting shaft design, lightweight materials, and specialized EV drivetrain solutions. European Union emission regulations including Euro 6 standards and future zero-emission requirements create regulatory pressure supporting adoption of lightweight interconnecting shaft solutions throughout regional vehicle markets.

United Kingdom, France, and Spain contribute significant manufacturing capacity supporting diverse vehicle platforms and specialized applications including Jaguar, Bentley, Rolls-Royce, and regional Renault, PSA, and Seat production. Regulatory harmonization throughout the European Union enables manufacturers to establish regional supply chain capabilities supporting efficient cross-border production and distribution. The region’s aggressive electric vehicle adoption targets, supported by government incentives and charging infrastructure investment, are accelerating demand for specialized interconnecting shaft solutions addressing unique EV powertrain architecture requirements.

Asia Pacific Automotive Interconnecting Shaft Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with CAGR of 7.4% during 2026-2033, projected to capture 54% global market share by 2033 driven by explosive vehicle production growth, government manufacturing incentives, and accelerated electric vehicle adoption. China dominates regional production with 56% global propeller shaft manufacturing capacity, serving both domestic market demand and supplying international OEM supply chains. India’s rapidly expanding automotive sector supported by Make in India and Production-Linked Incentive (PLI) programs is driving accelerated interconnecting shaft manufacturing capacity development supporting domestic and export-oriented production.

Japan maintains advanced manufacturing capabilities with major suppliers including JTEKT Corporation, NTN Bearing, and Sumitomo Heavy Industries producing high-specification interconnecting shafts for domestic OEMs and global supply chains. ASEAN manufacturing expansion in Vietnam, Thailand, and Indonesia is attracting foreign direct investment and supporting establishment of propeller shaft manufacturing facilities serving regional vehicle producers. The region’s emphasis on cost-effective manufacturing, established supply chain infrastructure, and government support for automotive sector development position Asia Pacific as global center for interconnecting shaft production supporting continued market expansion through forecast periods.

Competitive Landscape

Market Structure Analysis

The automotive interconnecting shaft market exhibits a moderately consolidated structure, with a limited group of global suppliers complemented by numerous regional and specialized manufacturers. Competition is largely driven by long-term OEM relationships, global manufacturing scale, and the ability to support multiple vehicle platforms across conventional and electric drivetrains. Leading suppliers focus on lightweight material adoption, advanced forging and machining processes, and EV-optimized shaft designs to meet evolving efficiency and performance requirements.

Strategic priorities include cost optimization through vertically integrated supply chains, localization of production near OEM hubs, and continuous investment in process automation. Market consolidation remains active as larger suppliers acquire niche capabilities and expand capacity in high-growth regions to strengthen regional presence. Meanwhile, emerging manufacturers in Asia are gaining share through competitive pricing and proximity to expanding vehicle production bases. Smaller players remain relevant by targeting niche applications, offering customization, and delivering specialized

Key Market Developments

- April 2023: RSB Transmissions (I) Ltd. announced establishment of 13th world-class manufacturing facility at Sri City, Andhra Pradesh, strengthening manufacturing capacity and positioning company to capture growing Indian and regional propeller shaft demand from expanding vehicle production platforms.

Companies Covered in Automotive Interconnecting Shaft Market

- GKN Automotive

- Bum Woo Precision

- Eco Shaft

- NTN Bearing

- Manufacturing Technology

- Hyundai Wia

- Changzhou Yirui Machining

- Bharat Forge

- SKF

- Neapco

- Dana Incorporated

- JTEKT Corporation

- Sumitomo Heavy Industries

- RSB Transmissions

- Meritor Inc.

- Schaeffler AG

- ZF Friedrichshafen AG

- Aisin Seiki Co., Ltd.

- Nexteer Automotive

- Magna International

Frequently Asked Questions

The global Automotive Interconnecting Shaft Market is expected to reach approximately US$ 13.2 billion in 2026.

Key drivers include rising vehicle production, electric vehicle adoption, emissions regulations, and demand for lightweight materials to improve fuel efficiency.

Asia Pacific is expected to lead the market with about 54% share by 2032.

The largest opportunity lies in advanced lightweight materials and smart monitoring technologies tailored for electric and electrified vehicles.

Major players include GKN Automotive, Dana, JTEKT, Sumitomo Heavy Industries, Hyundai Wia, Bharat Forge, and several regional specialists.