- Automotive Components & Materials

- Automotive Fuel Level Sensors Market

Automotive Fuel Level Sensors Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Fuel Level Sensors Market by Technology Type (Resistive Fuel Level Sensors, Others), Vehicle (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Others), and Regional Analysis for 2026 - 2033

Automotive Fuel Level Sensors Market Size and Trends Analysis

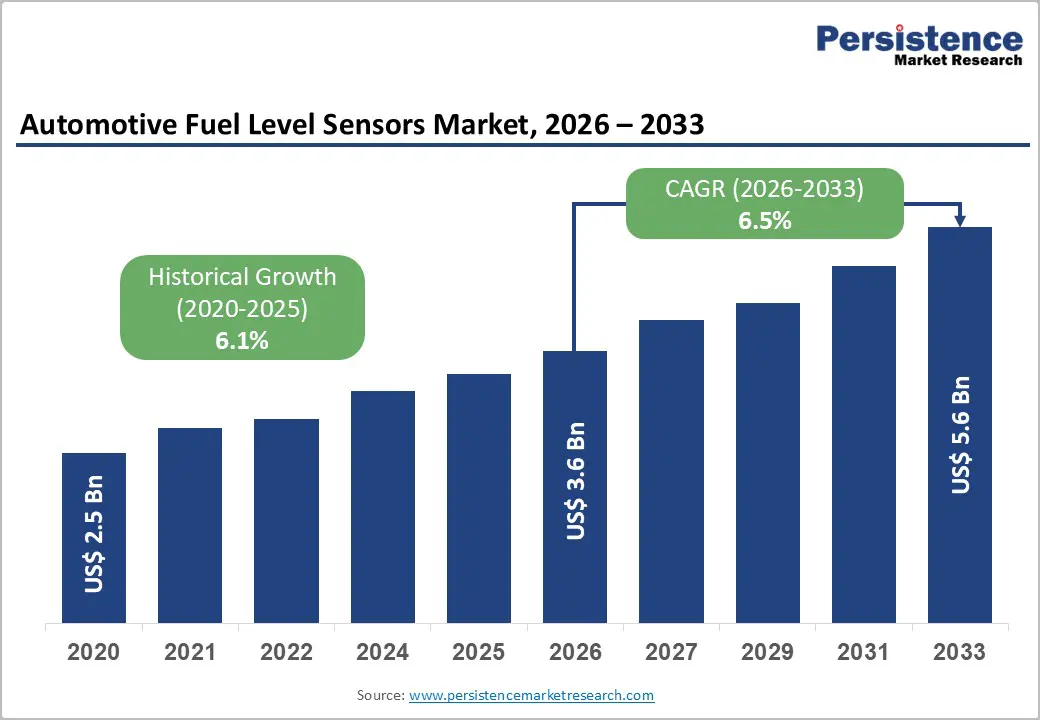

The global automotive fuel level sensors market size is likely to be valued at US$3.6 billion in 2026 and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by sustained automotive production volumes and rising demand from both passenger and commercial vehicle segments.

Growing connected vehicle adoption and fleet management systems are driving demand for real-time fuel monitoring to prevent theft, optimize consumption, and support predictive maintenance. While EVs reduce fuel reliance, hybrid and plug-in hybrid vehicles sustain demand for advanced capacitive, ultrasonic, and digital fuel sensors with improved precision and ECU integration.

Key Industry Highlights:

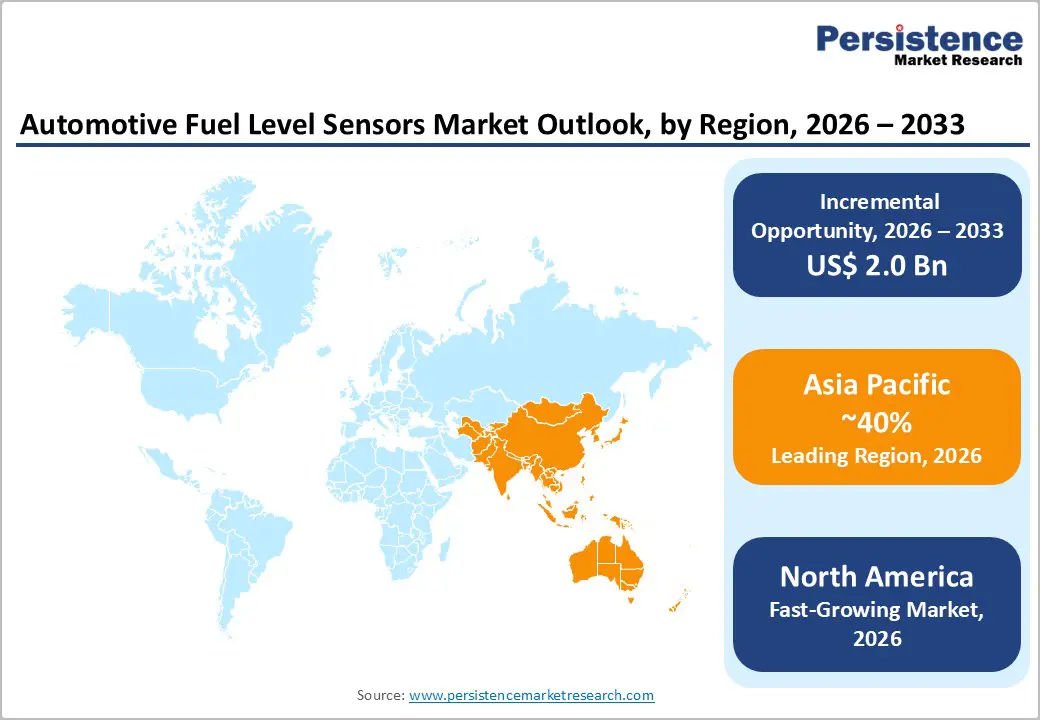

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong automotive manufacturing activity, high vehicle production volumes in China, Japan, and India, expanding middle-class demand, and increasing adoption of advanced vehicle sensor technologies.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the automotive fuel level sensors in 2026, supported by strong U.S. vehicle demand, stringent emission regulations, advanced automotive technologies, and a well-established aftermarket ecosystem.

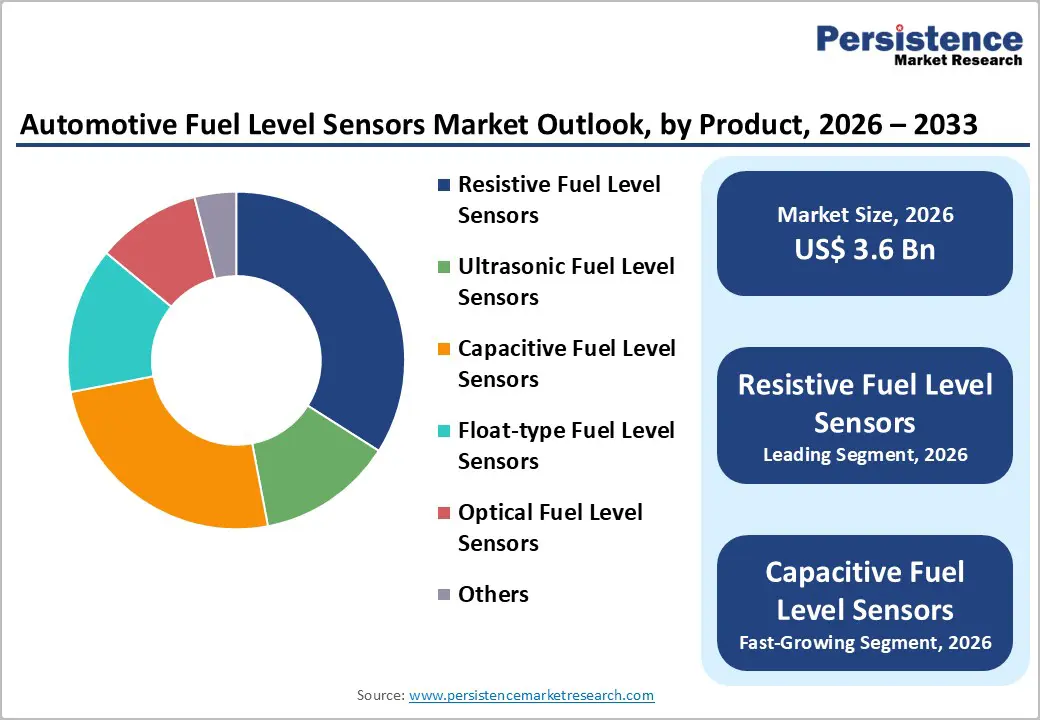

- Leading Technology Type: Resistive fuel level sensors are projected to represent the leading technology type in 2026, accounting for 40% of the revenue share, driven by their low cost, reliability, and widespread use in conventional vehicles.

- Leading Vehicle: Passenger cars are anticipated to be the leading vehicle type, accounting for over 60% of the revenue share in 2026, supported by high production volumes and increasing demand for fuel-efficient and connected features.

| Key Insights | Details |

|---|---|

|

Automotive Fuel Level Sensors Market Size (2026E) |

US$3.6 Bn |

|

Market Value Forecast (2033F) |

US$5.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Vehicle Production and Fleet Expansion

Automotive manufacturing continues to expand across both developed and emerging economies, supported by population growth, urbanization, and rising disposable incomes. Passenger car production is increasing steadily due to demand for personal mobility, while SUVs and light trucks gain popularity for their versatility and comfort. Each newly manufactured vehicle integrates at least one fuel level sensor, directly linking production volumes to sensor demand. OEMs are focusing on improving dashboard accuracy and vehicle diagnostics, strengthening the need for advanced fuel sensing solutions. Stricter fuel efficiency and emission regulations compel automakers to deploy more precise fuel level sensors to support optimized fuel management and compliance reporting.

Expanding vehicle fleets, particularly in commercial transportation, logistics, and ride-sharing sectors, accelerate demand for automotive fuel level sensors. Growth in e-commerce, last-mile delivery, public transportation, and construction activities has significantly increased the number of light and heavy commercial vehicles in operation. Fleet operators rely on accurate fuel level monitoring to reduce fuel theft, optimize consumption, and improve operational efficiency, driving the adoption of advanced sensor technologies. Fleet expansion in developing regions is supported by infrastructure development and industrialization, creating sustained aftermarket demand for replacement sensors.

Impact of Electric Vehicle (EV) Adoption on Traditional Fuel Level Sensor Demand

Governments worldwide are actively promoting EV adoption through incentives, subsidies, and stricter emission regulations aimed at reducing dependence on fossil fuels. Automakers are increasingly shifting production portfolios away from internal combustion engine (ICE) vehicles toward pure electric platforms. As fuel level sensors are inherently linked to liquid fuel monitoring, their demand declines proportionally with the reduction in gasoline and diesel-powered vehicle production. This structural shift creates long-term pressure on traditional fuel sensor manufacturers, particularly those heavily dependent on resistive or float-type technologies designed exclusively for ICE vehicles.

The transition to EVs does not eliminate demand but reshapes it unevenly across the market. Hybrid and plug-in hybrid vehicles still rely on fuel tanks and therefore require accurate fuel level sensors, partially offsetting the decline from pure EVs. Fleet electrification initiatives in public transport, logistics, and corporate mobility reduce large-volume demand from commercial vehicles, traditionally a strong contributor to sensor sales. Suppliers face added challenges from longer EV lifecycles and reduced mechanical wear, which lowers aftermarket replacement rates. Regional disparities in EV adoption mean that emerging markets continue to rely heavily on internal combustion and hybrid vehicles, sustaining baseline demand for fuel level sensors.

Emergence of Advanced Non-Contact Technologies

Technologies such as ultrasonic, capacitive, and optical sensors eliminate direct mechanical contact with fuel, improving measurement accuracy, durability, and resistance to wear and contamination. These solutions are increasingly favored in modern vehicles due to their ability to provide stable readings under varying temperature, vibration, and fuel composition conditions. Automakers integrate more electronic and digital systems, non-contact sensors align well with vehicle ECUs, digital instrument clusters, and connected platforms, supporting real-time fuel monitoring and diagnostics. Their higher reliability and longer service life also make them attractive for premium vehicles and commercial fleets focused on minimizing maintenance costs and downtime.

Growing demand for connected vehicles, telematics, and advanced driver assistance systems further amplifies the adoption potential of non-contact fuel level sensors. Fleet operators increasingly prefer ultrasonic and capacitive sensors for accurate fuel tracking, theft prevention, and predictive maintenance applications. Hybrid and alternative-fuel vehicles benefit from non-contact technologies that can adapt to varying fuel properties without recalibration. Regulatory pressure for improved fuel efficiency and emission monitoring also supports the shift toward high-precision sensing solutions. Manufacturing costs decline, and sensor miniaturization advances, non-contact fuel level sensors are expected to penetrate mass-market vehicles, creating new revenue streams for suppliers investing in innovation and smart sensing platforms.

Category-wise Analysis

Technology Type Insights

Resistive fuel level sensors are expected to lead the automotive fuel level sensors market, accounting for approximately 40% of revenue in 2026, due to their cost-effectiveness, simple design, and long-standing adoption across traditional internal combustion engine vehicles. These sensors operate using a float connected to a variable resistor, translating fuel level changes into electrical signals that are easily interpreted by vehicle dashboards. Their compatibility with existing fuel tank designs allows automakers to avoid costly system redesigns. For example, Pricol, which supplies resistive fuel level sensors extensively used by Indian and Asian passenger vehicle manufacturers, supports high-volume production platforms.

Capacitive fuel level sensors are likely to represent the fastest-growing segment in 2026, driven by increasing demand for higher accuracy, reliability, and seamless integration with modern vehicle electronics. Unlike mechanical systems, capacitive sensors measure fuel levels based on changes in electrical capacitance, enabling precise readings regardless of fuel sloshing, temperature variation, or tank shape. Automakers increasingly prefer capacitive sensors to support advanced fuel management strategies, emission optimization, and enhanced driver information systems. These sensors maintain reliable performance across various fuel types, including ethanol blends, facilitating regulatory compliance and global vehicle standardization. For instance, Bosch provides capacitive fuel sensing solutions that are integrated into advanced fuel management systems for OEMs.

Vehicle Insights

Passenger cars are projected to lead the market, capturing around 60% of the revenue share in 2026, supported by high global production volumes and strong consumer demand for reliable fuel monitoring systems. This segment benefits from widespread ownership, frequent vehicle replacement cycles, and continuous feature upgrades aimed at improving efficiency and driving comfort. The dominance of passenger cars is reinforced by expanding urban populations and sustained demand for personal mobility in both developed and emerging economies. For example, Toyota, which integrates fuel level sensors across its passenger car lineup, including sedans and compact cars, ensures consistent performance and regulatory compliance.

Electric hybrid vehicles are expected to be the fastest-growing segment in 2026, driven by the increasing adoption of hybrid and plug-in hybrid powertrains that combine electric propulsion with traditional liquid fuel systems. Unlike fully battery-electric vehicles, hybrids rely on highly accurate fuel level sensors to enable efficient energy management, precise range estimation, and smooth coordination between fuel and battery systems. As vehicle designs evolve and fuel tanks become smaller, sensors must maintain reliable performance under complex operating conditions. For instance, Honda’s hybrid lineup, including models such as the Accord Hybrid, integrates conventional fuel systems with electric propulsion and depends on precise fuel level sensing to optimize overall power management.

Regional Insights

North America Automotive Fuel Level Sensors Market Trends

North America is expected to be the fastest-growing market for automotive fuel level sensors in 2026, driven by advanced vehicle technologies and stringent regulatory standards. The region’s large fleet of passenger cars, pickup trucks, and commercial vehicles creates strong demand for accurate fuel monitoring to enhance efficiency and ensure compliance. Regulations such as CAFE standards and EPA emission norms are encouraging automakers to adopt more precise and reliable fuel sensing solutions. The increasing integration of digital instrument clusters, vehicle diagnostics, and connected car platforms is boosting demand for sensors that provide stable, real-time fuel data across diverse operating conditions, supporting both OEM and aftermarket growth.

Technological innovation is a key trend, with manufacturers shifting toward capacitive and non-contact sensors to improve accuracy and durability. Fleet operators are also driving demand for solutions that enable fuel optimization, theft prevention, and predictive maintenance through telematics. Companies such as Continental AG are supplying advanced fuel level sensors with enhanced electronic integration and system reliability, further supported by the growing adoption of connected, hybrid, and plug-in hybrid vehicles, which require precise fuel monitoring to optimize energy management.

Europe Automotive Fuel Level Sensors Market Trends

Europe is expected to be a key market for automotive fuel level sensors in 2026, driven by stringent emission regulations, advanced vehicle engineering, and a strong emphasis on fuel efficiency and sustainability. Standards such as Euro 6 and the upcoming Euro 7 require precise fuel monitoring to support emission control and optimized consumption, boosting demand for accurate sensing technologies. European OEMs prioritize high-quality components and system reliability, encouraging the integration of advanced fuel level sensors with vehicle ECUs and digital dashboards. The region’s mature automotive industry, along with steady demand for passenger cars and commercial vehicles, underpins consistent OEM and aftermarket growth.

Technological innovation is a major trend, with manufacturers increasingly adopting capacitive and non-contact sensors to enhance accuracy and durability. These solutions are particularly suited for premium vehicles and hybrid models, which remain a focus during Europe’s gradual shift toward electrification. Companies such as Valeo supply advanced sensing and electronic solutions to leading OEMs, supporting efficient fuel management and seamless system integration. Rising hybrid adoption, fleet modernization, and continued R&D investments are sustaining stable growth opportunities for fuel level sensor suppliers across Europe.

Asia Pacific Automotive Fuel Level Sensors Market Trends

The Asia Pacific region is expected to lead the market in 2026, capturing a 40% share, driven by high vehicle production, a growing middle-class population, and increasing adoption of fuel-efficient and connected vehicle technologies. Key markets such as China, Japan, and India dominate the region, supported by a strong OEM presence and extensive manufacturing hubs that enable high-volume production. Rising demand for passenger cars, SUVs, and commercial vehicles is fueling the need for precise fuel monitoring systems to optimize consumption, improve range estimation, and meet regional fuel efficiency regulations. Fleet growth in logistics, ride-sharing, and public transportation is creating further aftermarket opportunities for advanced fuel sensors. For example, Denso Corporation, a leading Japan-based automotive supplier, develops and supplies advanced fuel level sensing and electronic components to major OEMs across Asia, supporting passenger cars, hybrids, and commercial vehicles.

Advanced non-contact and capacitive sensor technologies are gaining traction in Asia Pacific due to their accuracy, durability, and compatibility with modern fuel systems. For instance, Pricol Ltd., an Indian automotive component manufacturer, supplies fuel level sensors to major OEMs and aftermarket clients across Asia, supporting both passenger and commercial vehicles. The market is also influenced by trends such as digital dashboards, hybrid vehicle integration, and smart fleet monitoring, driving investments in sensor R&D and system optimization. As hybrid adoption rises alongside conventional vehicles, the Asia Pacific region presents significant growth opportunities for fuel level sensor manufacturers through technological innovation, scalable production, and evolving regulatory compliance.

Competitive Landscape

The global automotive fuel level sensors market exhibits a moderately fragmented structure, driven by the presence of numerous regional and global players offering a wide range of sensor technologies to OEMs and the aftermarket. This fragmentation is due to varied regional automotive production footprints, diverse sensor technology requirements, and the coexistence of both established multinational corporations and specialized local suppliers. Growth in connected vehicles, rising hybrid adoption, and fleet telematics creates demand for advanced sensor solutions, encouraging new entrants and collaborations.

With key leaders including Robert Bosch GmbH, Continental AG, Valeo, Melexis, Bourns, and Pricol Ltd., the competitive landscape reflects a balance between global scale and regional specialization. These players compete through ongoing innovation, strategic partnerships with automakers, and expansion of manufacturing footprints in high-growth regions. They also focus on enhancing sensor accuracy, durability, and cost-efficiency to meet stringent emission and fuel economy regulations worldwide.

Key Industry Developments:

- In August 2025, Soji Electronics (LIGO), a fuel management technology provider, launched LIGO AIR, a next-generation wireless fuel level sensor designed for high accuracy, long-term durability, and reliable performance in modern fuel monitoring applications. Built with automotive-grade components, LIGO AIR operates consistently under extreme environmental conditions, supporting fleet operations, fuel depots, and industrial use cases. It features one of the longest battery lifespans in its class, offering 8–10 years of operation on a single replaceable battery, significantly reducing maintenance needs and system downtime.

- In September 2025, Jimi IoT introduced the KL100 Fuel Tracking System, a next-generation solution designed to help fleet operators combat rising fuel costs, theft, and inefficiencies through real-time visibility and control. The KL100 is positioned as an all-in-one GPS-enabled fuel tracking system, combining precise fuel level sensing, live location tracking, and advanced anti-theft alerts within a single, rugged device tailored for demanding fleet environments. The KL100 addresses critical fleet challenges by delivering high-precision fuel measurement with minimal error, enabling operators to accurately monitor consumption patterns and identify inefficiencies.

Companies Covered in Automotive Fuel Level Sensors Market

- Gentech

- Melexis

- Standex‑Meder

- Bourns

- Hamlin

- Pricol

- Omnicomm

- WemaUSA

- Soway

- MI Sensor

- Dongguan Zhengyang Electronic Mechanical Co., Ltd

- General Motors

Frequently Asked Questions

The global automotive fuel level sensors market is projected to reach US$3.6 billion in 2026.

The automotive fuel level sensors market is driven by growing vehicle production, stricter fuel efficiency and emission regulations, and the rising adoption of connected vehicles and fleet management systems that demand precise fuel monitoring.

The automotive fuel level sensors market is expected to grow at a CAGR of 6.5% from 2026 to 2033.

Key market opportunities include the increasing adoption of advanced non-contact sensor technologies, the growth of connected and fleet telematics systems, the rising production of hybrid vehicles, and expanding aftermarket demand in emerging automotive markets.

Gentech, Melexis, Standex‑Meder, Bourns, Hamlin, Pricol, Omnicomm, WemaUSA, and Soway are the leading players.