- Automotive Components & Materials

- Automotive Collision Repair Market

Automotive Collision Repair Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Collision Repair Market by Product type (Parts and Components, Paints and Coatings and Spare Parts), Service Provider (DIY, DIFM (Do it for Me) and OE (Handled by OEM)), Vehicle Type (Passenger Car, Light Commercial Vehicles and Heavy Commercial Vehicles) and Regional Analysis for 2026 - 2033

Automotive Collision Repair Market Size and Trends Analysis

The global automotive collision repair services market was valued at US$ 220.4 billion in 2026 and is projected to reach US$ 265.1 billion by 2033, growing at a CAGR of 2.7% between 2026 and 2033.

Growth is driven by increasing vehicle ownership, accident frequency, technological complexity requiring specialized repair expertise, and consolidation, which creates scale efficiencies.

Key Industry Highlights:

- Product segmentation: Spare parts dominate at ~64% share, while paints and coatings are fastest growing at 2.7% CAGR, driven by advanced refinishing technology and sustainability regulations.

- Service channel mix: OE (OEM-handled) services capture ~57.4% (collision) to 69.2% (broader aftermarket), while DIY is fastest-growing at 2.5% CAGR, reflecting rising e-commerce access to parts and online repair tutorials

- Vehicle type dynamics: Passenger cars account for ~65.4% of collision repair demand. In contrast, light commercial vehicles are the fastest-growing segment, driven by the expansion of e-commerce logistics and rising pickup truck/SUV market share.

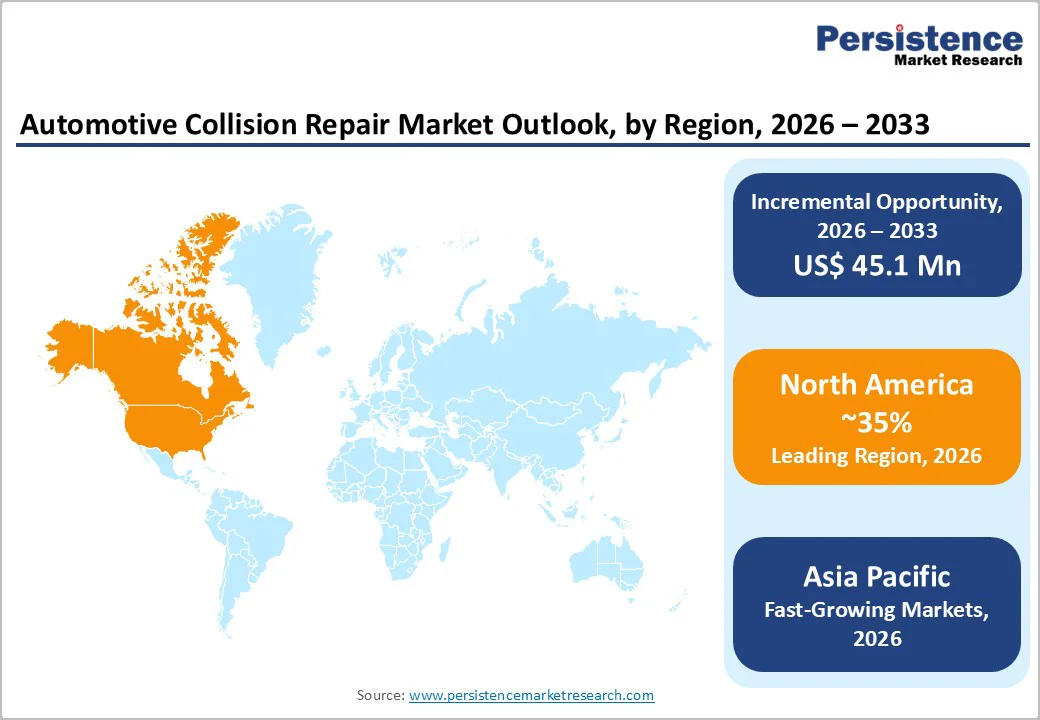

- Regional performance: North America leads the market with 35% global share, and Asia Pacific is the fastest-growing at 1.9% CAGR, particularly in China and emerging markets.

- Consolidation and strategic developments: Big Five operators now control 31.7% revenue and 13.3% of shop locations (4,019+ facilities); private equity capital exceeding US$ 9 billion entered since November 2023; 450+ locations acquired in 2024; major moves include Trive Capital's Chilton acquisition (20-shop platform), Gerber's L&M expansion, and 3M's Repairify investment, all signaling industry shift toward technology-enabled, scale-optimized collision repair.

| Key Insights | Details |

|---|---|

| Automotive Collision Repair Market Size (2026E) | US$ 220.4 Bn |

| Market Value Forecast (2033F) | US$ 265.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 2.7% |

| Historical Market Growth (CAGR 2020 to 2024) | 2.1% |

Market Dynamics

Drivers - Rising Global Vehicle Fleet and Accident Frequency

Global vehicle ownership continues expanding, particularly in emerging markets, with the international automotive fleet expected to exceed 1.4 billion units by 2030, up from approximately 1.2 billion in 2024. This larger installed base mechanically increases the number of collision incidents requiring professional repair services. In addition, urban congestion, increased road traffic, and variable enforcement of traffic regulations, particularly in the Asia-Pacific region, have led to higher accident frequency and severity in many areas.

Global automotive insurance subscriptions have grown substantially, with penetration increasing from 42% of vehicles in 2020 to approximately 58% by 2024, creating more insured repair demand. Studies estimate that 8% of insured vehicles are involved in collisions annually, with average repair costs ranging from US$2,500 to US$5,500 per incident, depending on severity and regional labor and parts costs. This combination of fleet growth, accident frequency, and insurance penetration creates a durable, non-discretionary demand base for collision repair services.

Technological Complexity and ADAS/Autonomous Features Calibration

Modern vehicles increasingly incorporate advanced driver-assistance systems (ADAS), including cameras, radar, and ultrasonic sensors, along with autonomous emergency braking, lane-keeping assist, and adaptive cruise control features that require post-collision calibration and verification. Repairing and recalibrating these systems requires specialized equipment (diagnostic scan tools, camera calibration rigs, LIDAR alignment systems) and certified technicians, significantly increasing repair complexity and labor content per collision incident.

ADAS calibration can add US$ 500-3,000 to repair costs, creating incremental revenue opportunities and barriers to entry that protect established service providers. As ADAS penetration rises (currently present in ~70% of new vehicles in developed markets), the proportion of collision repairs requiring specialized sensor and electronic system work will escalate, directly supporting demand for skilled technicians and technology-enabled repair facilities.

Restraints- Rising Total Cost of Repair (TCOR) and Insurance Pressure

Total cost of repair (TCOR) across the industry has risen sharply due to increased labor rates, parts scarcity, specialized equipment costs, ADAS calibration expenses, and extended repair cycle times. Parts availability challenges, semiconductor shortages affecting sensors and control modules, and volatile precious metal prices (for catalytic converters in exhaust aftertreatment) have constrained supply and elevated parts costs by 15% above pre-pandemic levels in many markets. Simultaneously, insurance carriers have tightened negotiations on labor rates, parts markups, and total loss thresholds, with many insurers raising total loss thresholds from 75% to 80% of vehicle value, reducing the pool of vehicles repaired versus scrapped. For independent and small-chain repair shops lacking the scale to negotiate leverage, margin compression is acute, forcing consolidation or exit.

Market Fragmentation and Digital/Tech Infrastructure Investment Barriers

While consolidation is accelerating, the market remains highly fragmented, with independent shops and small regional chains still representing approximately 68.7% of shop locations as of mid-2025. Independent operators lack the capital and expertise to invest in ADAS calibration equipment (US$ 50,000-150,000 per installation), cloud-based repair management systems, digital diagnostics, and certified technician training programs, which are increasingly expected by insurance carriers and OEMs.

Small operators struggle to compete with consolidators on pricing, service quality, and technology, creating a "technology divide" that accelerates consolidation by attrition or forced acquisition at unfavorable terms. For the broader market, this consolidation dynamic can obscure underlying demand fundamentals by masking unit-level shop closures behind revenue concentration at larger operators.

Opportunity - ADAS Calibration and Advanced Repair Service Specialization

With ADAS present in 70% of new vehicles in North America and Europe, and rising penetration in the Asia Pacific, ADAS-capable repair centers can command premium pricing and higher margins on specialized services. Global ADAS repair and calibration services are estimated to generate US$9 billion in annual revenue, growing at a 16% CAGR as the installed base of ADAS-equipped vehicles expands. Independent shops partnering with tier-1 technology providers (e.g., Caliber's partnership with Protech for ADAS solutions) or investing in dedicated calibration bays can differentiate and capture premium clientele. This specialization opportunity is particularly attractive in high-value vehicle segments, fleet maintenance operations, and warranty- and recall-driven repair programs.

Hybrid and Electric Vehicle Repair Expertise

As electrified vehicles (BEVs and plug-in hybrids) reach a 10% global sales share and rising, collision repair facilities require specialized capabilities for high-voltage battery pack inspection, thermal runaway safety protocols, electric motor diagnosis, and repair of battery thermal management systems. Repair shops developing EV-specific expertise command premium positioning and can serve as OEM-preferred vendors for vehicle recall and warranty work. Training programs, tooling, and safety equipment for EV repair represent incremental investment barriers, creating competitive moats for early-adopting shops. The global EV collision repair market is estimated at US$ 2.5 billion in 2024, expanding at 22% CAGR through 2033, substantially above the baseline collision market CAGR, and offering high-margin growth opportunities.

Emerging Market Expansion and Regulatory Catch-Up

Asia Pacific collision repair markets (especially China, India, and ASEAN) are experiencing rapid fleet growth and increasing accident frequency, yet remain underserved relative to North America and Europe in terms of modern repair infrastructure. Regulatory frameworks mandating vehicle safety inspections, emission compliance verification, and standardized repair practices are progressively implemented, creating opportunities for technology providers, training platforms, and consolidation platforms targeting regional markets. Asia-Pacific collision repair is expected to grow at a 3.5% CAGR through 2030, substantially above European and North American rates. Operators establishing early-mover positions in China, India, and Vietnam through local partnerships, technology licensing, or greenfield investments can capture multi-billion-dollar market opportunities in emerging markets, where competition is less entrenched than in mature Western markets.

Category-wise Analysis

Product Type Insights

Spare parts account for about 64% of the automotive collision repair market, driven by the frequent replacement of body panels, bumpers, structural components, mirrors, lights, and electronic modules after accidents. OEM parts command higher premiums, while aftermarket parts offer cost savings but varying quality. This segment will remain dominant, though growth will moderate as recycled and refurbished parts gain adoption.

Paints and coatings are the fastest-growing category, supported by a 4.7% CAGR. Growth is fueled by advanced refinishing technologies, stricter VOC regulations, and increasingly complex multilayer automotive coatings used in EVs and modern vehicles. Innovations such as self-healing and temperature-responsive paints, along with sustainability certifications, are boosting demand for high-value refinishing services.

Service Provider Channel Insights

OEM-authorized service centers account for about 57.4% of collision repair revenue, driven by strong consumer trust, warranty protection, access to genuine parts, and OEM-approved repair and ADAS calibration procedures. They remain the preferred choice for safety-critical or warranty-related repairs, especially for premium vehicles, though high labor costs and fixed facility networks limit their growth.

DIY repair services are the fastest-growing channel, expanding at 4.5% CAGR as online tutorials, affordable diagnostic tools, and easy e-commerce access to parts empower consumers. Cost-conscious owners increasingly perform minor repairs, such as bumper fixes or light replacements, without visiting workshops. High insurance deductibles and more flexible personal schedules are further accelerating the adoption of DIY in mature automotive markets.

Vehicle Type Insights

Passenger cars account for about 65.4% of collision repair revenues, driven by their large global vehicle parc and the frequency of low-to-moderate collision incidents. These vehicles create steady demand for body repair, paint refinishing, and glass replacement and benefit from higher insurance penetration, making them a consistent, high-volume segment for repair providers.

Light commercial vehicles, vans, pickups, and utility models are the fastest-growing segment, supported by expanding e-commerce, last-mile delivery, and rising LCV adoption across developed and emerging markets. LCV repairs are typically more complex and costly due to heavier-duty structures, higher payload demands and increasing use of ADAS. As fleet electrification accelerates, the value of LCV collision repair is expected to grow further, enhancing margins for service providers.

Regional Market Insights

North America Automotive Collision Repair Market Trends

North America represents the largest market, estimated at US$ 129.54 billion in 2026, with projected growth to US$ 182.09 billion by 2032, reflecting a modest 1.9% CAGR. The U.S. market dominates regionally, driven by high vehicle ownership, extensive road networks, and mature collision insurance penetration (~85% of vehicles). North American collision repair is characterized by well-developed consolidation (Big Five operators’ control ~31.7% revenue), high ADAS adoption in new vehicles, and advanced diagnostic and calibration infrastructure.

The regulatory environment emphasizes vehicle safety standards (NHTSA FMVSS requirements) and state-level insurance regulations, which mandate adequate repair quality and insurer communication standards. Tesla's expansion into company-owned collision repair (51 facilities by end-2024) signals OEM strategies to integrate collision repair and control customer experience and data vertically. Competitive dynamics are dominated by Caliber Collision (1,800+ locations), Crash Champions, Joe Hudson's, Gerber, Classic Collision, and numerous independent operators and smaller regional consolidators.

Europe Automotive Collision Repair Market Trends

Europe is a significant regional collision repair market globally, accounting for approximately 41.69% of global revenues with an estimated US$ 85.11 billion in 2024, projected to reach US$ 123.17 billion by 2034 at a 2.2% CAGR. Germany leads European markets with approximately 28.28% share driven by strong automotive manufacturing, high vehicle quality standards, and well-established collision repair infrastructure. The U.K., France, and Spain contribute meaningfully but exhibit lower growth rates, reflecting mature market saturation and aging vehicle fleets.

The European regulatory environment is highly structured, with EU harmonized vehicle safety standards, ADAS calibration requirements, environmental regulations on VOC emissions in refinishing, and data protection (GDPR) rules governing customer and vehicle data. Germany's automotive collision repair sector is experiencing investment in R&D and technology adoption, with companies deploying computerized measurement systems, frame-straightening and alignment technology, and digital appraisal tools to enhance repair precision and cycle time efficiency.

Asia Pacific Automotive Collision Repair Market Trends

Asia Pacific is the fastest-growing regional collision repair market, with expected growth from approximately US$ 90 billion in 2025 to over US$ 160 billion by 2033, reflecting 1.5% CAGR or higher. China dominates the region, with an estimated US$45 billion market and the largest growth in vehicle fleet, though collision repair services remain fragmented and unsophisticated relative to Western markets. Japan maintains approximately US$ 10 billion annual market, characterized by high technical standards and ADAS adoption in OEM service networks. India and ASEAN represent emerging high-growth opportunities, with rapidly expanding vehicle ownership, rising accident frequency due to inadequate enforcement and road infrastructure, and nascent collision repair infrastructure.

The regulatory environment varies significantly: China is implementing national safety inspection and repair standards to improve consistency in collision repair quality; Japan enforces high-quality OEM standards; and India and the ASEAN markets face limited regulatory enforcement, creating opportunities for quality-focused operators to differentiate. The competitive landscape includes emerging Chinese consolidators, Japanese OEM-affiliated service centers, multinational operators (Caliber, Belron, Gerber) establishing regional platforms, and numerous independent operators.

Competitive Landscape

Market leaders pursue scale-driven consolidation with technology integration, combining organic growth with M&A to achieve economies of scale in procurement, labor training, and technology investment. Differentiation strategies emphasize ADAS and EV repair specialization, digital repair management platforms, customer experience through transparency and convenience (pickup/dropoff, loaner vehicles, online scheduling), insurance carrier and OEM partnerships, and sustainability positioning.

Emerging business models include performance-based contracting with insurance carriers (guaranteeing cycle times and quality), subscription-based ADAS calibration and diagnostics services, and specialized EV battery repair and recycling programs. Consolidators increasingly invest in data analytics, predictive maintenance, and supply chain optimization to improve margins amid labor cost inflation and parts availability challenges.

Key Industry Developments:

- In July 2023, BMW North America joined Sustaining Partner Program by I-CAR. The program helps fund support initiatives and collision repair education that reduce training redundancies. It is also designed to help partners demonstrate advocacy and provide funding for industry-wide efforts by I-CAR.

- In July 2023, Classic Collision announced the acquisition of the Dayton Collision Center in Dayton, Tennessee, enabling the company to expand its operations in the state. This follows the company’s successful operational expansion in other states, including Minnesota, Georgia, Texas, Colorado, and Florida, in 2023

Companies Covered in Automotive Collision Repair Market

- 3M

- Service King

- BASF

- Robert Bosch

- Gerber Collision & Glass

- Continental AG

- AMM Collision

- Abra Auto Body & Glass

- Honeywell International Inc.

- Denso Corporation.

- Others Key Players

Frequently Asked Questions

The Automotive Collision Repair market is estimated to be valued at US$ 220.4 Mn in 2026.

The key demand driver for the Automotive Collision Repair market is the high and growing volume of vehicles on the road combined with increasing accident rates.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Collision Repair market.

Among the Product Type, Spare Parts holds the highest preference, capturing beyond 64% of the market revenue share in 2026, surpassing other Product Type.

The key players in Automotive Collision Repair are 3M, Service King, BASF and Robert Bosch.