- Inks, Coatings, Adhesives & Sealants (ICAS)

- North America Paints and Coatings Market

North America Paints and Coatings Market Size, Share, and Growth Forecast 2026–2033

North America Paints and Coatings Market by Resin Type (Epoxy, Acrylic, Polyester, Alkyd, Polyurethane, Others), Technology (Water-borne, Solvent-borne, Powder), Industry (Architectural, Automotive, Protective Coating, Industrial, Wood Coating, Traffic Paints, Paper, Others), and Country Analysis for 2026–2033

North America Paints and Coatings Market Size and Trend Analysis

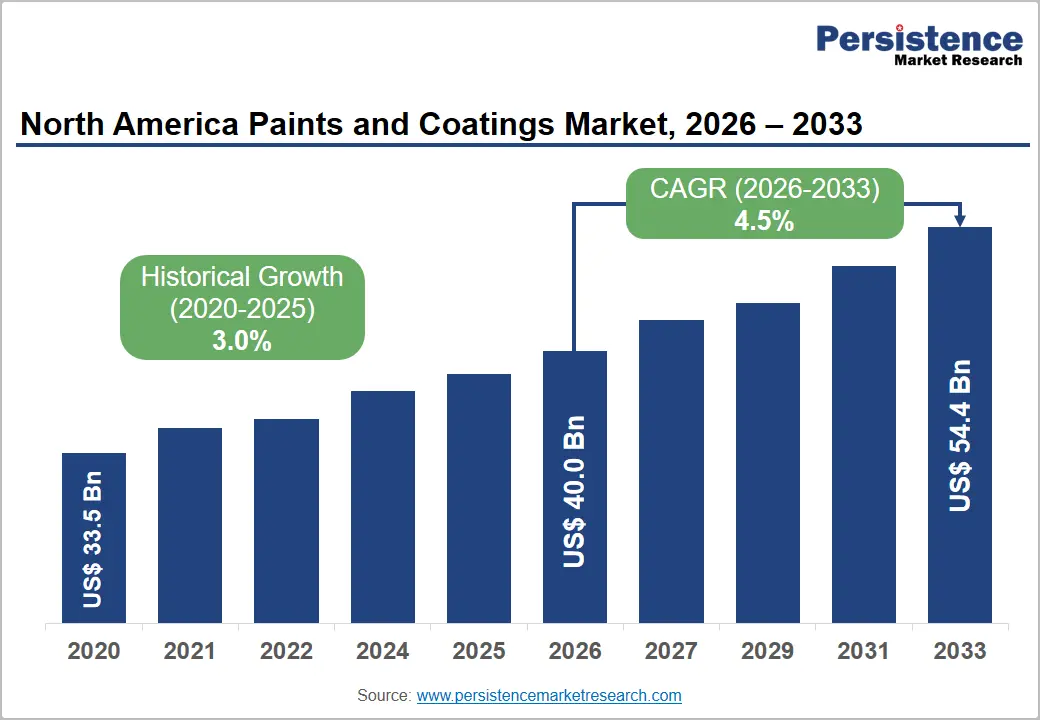

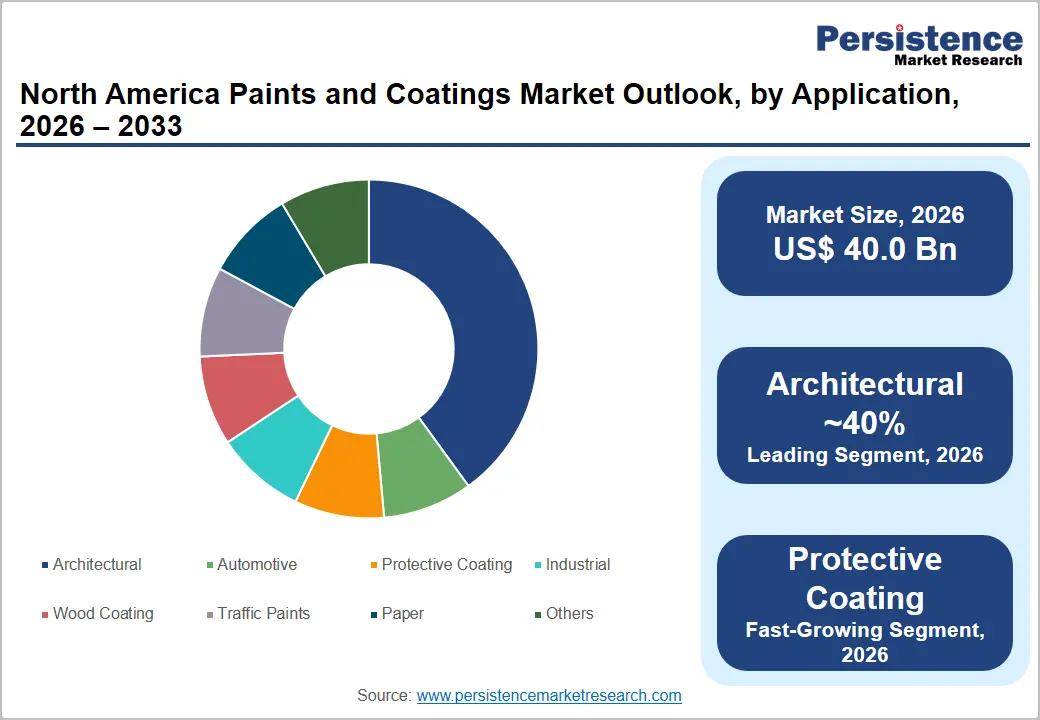

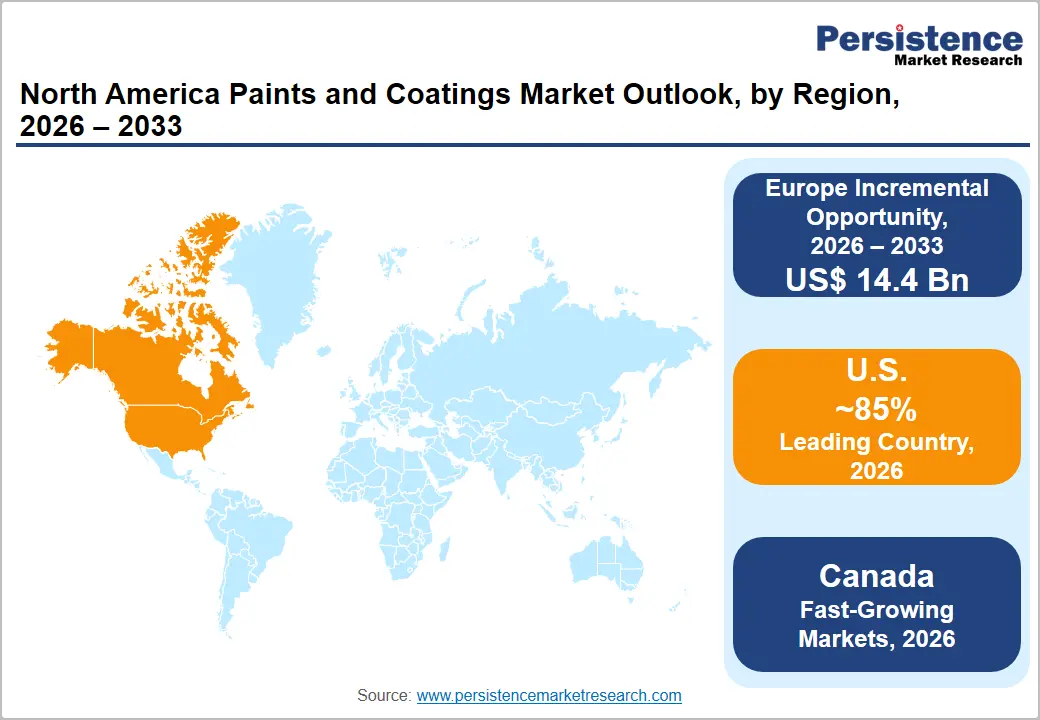

North America paints and coatings market size is valued at US$ 40 billion in 2026 and is projected to reach US$ 54.4 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

This growth trajectory is driven by several key demand factors. There is a robust pipeline for residential and commercial construction, alongside accelerated modernization of infrastructure supported by the U.S. Infrastructure Investment and Jobs Act (IIJA). Additionally, the stringent regulations from the U.S. Environmental Protection Agency (EPA) are encouraging a market-wide transition toward water-borne and powder coating technologies.

The primary architectural and industrial sectors in the region are also experiencing benefits from increased renovation activities, rising automotive production, and a growing adoption of high-performance functional and protective coatings across manufacturing and infrastructure applications

Key Industry Highlights:

- Leading Region: The United States dominates the North America Paints and Coatings market with approximately 85% of regional revenue, anchored by the world's largest construction spending base, robust industrial activity, and a deeply established architectural coatings retail ecosystem.

- Fast-Growing Market: Canada demonstrates solid growth fundamentals supported by government-backed infrastructure investment, a robust residential construction sector, and growing industrial coating demand from energy, mining, and manufacturing sectors.

- Dominant Segment: Acrylic resins lead the resin type category with approximately 35% revenue share, underpinned by their dominant role in water-borne architectural formulations, superior weatherability performance, and broad compatibility with low-VOC regulatory requirements.

- Fast-Growing End-use Category: The protective coatings are the fast-growing, propelled by US$ 1.2 trillion in IIJA infrastructure investment, driving demand for corrosion-resistant coating systems across bridges, pipelines, and industrial structures.

- Key Opportunity: Smart and functional coatings, including anti-microbial, heat-reflective, and self-cleaning formulations, represent the highest-value growth opportunity, supported by ENERGY STAR incentives, CDC-acknowledged healthcare infection control imperatives, and premium pricing potential across commercial and institutional applications.

DRO Analysis

Drivers - Rising Construction Activity and Infrastructure Spending Driving the Demand

The sustained expansion of residential and commercial construction across the United States and Canada constitutes the foremost structural driver of North America Paints and Coatings demand. The U.S. Census Bureau reported that total U.S. construction spending reached approximately US$ 2.1 trillion in 2023, with residential construction alone exceeding US$ 900 Bn. Concurrently, the U.S. Infrastructure Investment and Jobs Act (IIJA), allocating US$ 1.2 trillion in infrastructure investment over five years, is generating sustained demand for protective and traffic paints across bridges, highways, and public infrastructure assets.

The American Institute of Architects (AIA) Architecture Billings Index registered consistent positive billings throughout 2023–2024, signaling a healthy forward pipeline for commercial construction and renovation activity. These dynamics collectively reinforce strong, multi-year demand for architectural and protective coatings, the market's highest-volume segments, across both new construction and maintenance repaint applications.

Environmental Regulations Accelerating Low-VOC Coating Adoption

Progressively stringent U.S. EPA volatile organic compound (VOC) emission regulations, complemented by state-level mandates from bodies such as the California Air Resources Board (CARB) and the South Coast Air Quality Management District (SCAQMD), which enforce among the world's most restrictive VOC limits for architectural coatings, are driving accelerating adoption of water-borne and powder coating technologies across all application segments.

The U.S. Green Building Council (USGBC) reports that LEED-certified buildings in the U.S. have surpassed 105,000 projects, encompassing over 11 billion square feet of construction space, with interior and exterior coating specifications increasingly mandating low- or zero-VOC products. Manufacturers are responding by expanding water-borne resin platforms and bio-based coating formulations, creating a regulatory-driven replacement cycle that sustains incremental volume demand and supports premium pricing for compliant, environmentally responsible coating solutions.

Restraints - Raw Material Price Volatility and Supply Chain Disruptions

The North America Paints and Coatings industry is heavily exposed to price volatility in key raw materials, including titanium dioxide (TiO?), the industry's primary white pigment, petroleum-derived resins, solvents, and specialty additives, all of which demonstrated significant cost inflation during 2021–2023. TiO? prices experienced increases exceeding 30% during pandemic-era supply disruptions, with limited domestic production capacity amplifying import dependency.

The U.S. Bureau of Labor Statistics recorded double-digit producer price index (PPI) increases for paint and coating manufacturing in multiple consecutive quarters through 2022. Compounding this, the imposition of broad-based U.S. tariffs on Chinese chemical intermediates and pigments in 2025 further elevated input costs, constraining margin recovery for mid-tier manufacturers with limited pricing power and restricting their ability to invest in product innovation and capacity expansion.

Consolidation Barriers and High Compliance Costs for Smaller Manufacturers

While market leaders benefit from economies of scale, smaller and mid-sized paints and coatings manufacturers face a disproportionate compliance burden under an expanding regulatory framework. EPA enforcement of the Toxic Substances Control Act (TSCA) and state-level VOC regulations necessitates ongoing reformulation investment that can consume a significant share of smaller manufacturers' research budgets.

According to the American Coatings Association (ACA), the U.S. coatings industry invests over US$ 1.0 Bn annually in environmental, health, and safety compliance, a disproportionate burden on sub-scale producers. These compliance costs, combined with the capital intensity of transitioning production lines to water-borne or powder technologies, are accelerating consolidation and disadvantaging smaller competitors relative to integrated multinationals with dedicated compliance and R&D infrastructure.

Opportunities - Expansion of Powder Coating Technology Across Industrial and Electric Vehicle Applications

Powder coatings represent one of the fastest-growing technology segments within the North America Paints and Coatings market, driven by their zero-VOC profile, superior film durability, corrosion resistance, and operational efficiency advantages relative to liquid coating systems. The accelerating North American electric vehicle (EV) production cycle is generating particularly strong demand for powder coatings applied to battery enclosures, structural aluminum components, and underbody assemblies requiring lightweight, corrosion-resistant finishes. According to the Edison Electric Institute (EEI), EV sales in the U.S. exceeded 1.4 million units in 2023, a trajectory expected to continue under the U.S. Inflation Reduction Act's (IRA) EV tax credit provisions.

Furthermore, the IIJA-funded expansion of pipeline, bridge, and transmission infrastructure is creating expanded end-markets for high-performance industrial powder coatings. Manufacturers investing in next-generation thermosetting and UV-curable powder platforms are well-positioned to capture this structural growth opportunity through the forecast horizon.

Smart and Functional Coatings Innovation

Rapidly advancing functional coating technologies, including anti-microbial, self-cleaning, heat-reflective, and anti-corrosion smart coating systems, represent a high-value growth opportunity for North American coating manufacturers capable of investing in materials science innovation. The U.S. Centers for Disease Control and Prevention (CDC) estimates that healthcare-associated infections (HAIs) affect approximately 1 in 31 hospital patients on any given day, creating substantial demand for EPA-registered antimicrobial coatings across healthcare facilities, public transit systems, and commercial spaces.

Concurrently, heat-reflective 'cool roof' coatings are gaining regulatory support through ENERGY STAR certification programs and building codes in high-temperature states, driven by energy efficiency mandates under the IRA. Coating manufacturers that develop and scale certified functional coating platforms will be positioned to command meaningful price premiums while addressing urgent sustainability and public health imperatives across North American commercial and institutional markets.

Category-wise Analysis

Resin Type Insights

Acrylic resins represent the dominant segment within the resin type category, accounting for approximately 35% revenue share. Acrylics' market leadership is anchored in their versatility across water-borne formulations, superior UV stability, color retention, and adhesion performance across both interior and exterior architectural applications, the market's highest-volume end-use segment. The American Coatings Association (ACA) notes that water-based acrylic formulations now represent the majority of architectural coating sales in the U.S., driven by their low-VOC profiles and broad applicability across residential repaint and new construction applications.

Industrial and automotive application demand further reinforces acrylic's dominance, as polymer technology advancements continue to extend performance capabilities, including chemical resistance and weatherability, into application segments traditionally reliant on solvent-borne systems. Polyurethane resins represent the second-largest segment, valued for high-durability protective and floor coating applications.

Technology Insights

Water-borne coatings represent the dominant technology segment, commanding approximately 60% of the North America Paints and Coatings market revenue and continuing to expand share at the expense of solvent-borne alternatives. This dominance is directly attributable to the regulatory framework established by the U.S. EPA and state-level authorities, particularly CARB and SCAQMD, which impose restrictive VOC emission limits compelling formulators and applicators to transition to water-borne systems across architectural, industrial, and automotive refinish segments. The U.S. Green Building Council reports that LEED certification standards increasingly mandate the use of low-VOC water-borne interior coatings in certified construction projects.

Continued investment by major manufacturers in water-borne resin technology, improving film hardness, block resistance, and application characteristics, is steadily closing the performance gap with solvent-borne systems, further accelerating market transition. Powder coatings represent the fastest-growing technology sub-segment, particularly in industrial and automotive applications.

Industry Insights

Architectural is the dominant industry, accounting for approximately 40% of total market revenue in North America. This leadership reflects the sheer scale of residential and commercial construction and repaint activity across the U.S. and Canada, where the existing housing stock of approximately 140 million units generates persistent maintenance repaint demand estimated at repainting cycles of 5 to 7 years. The National Association of Home Builders (NAHB) reported over 1.4 million housing starts in the U.S. in 2023, each representing direct new-construction architectural coating demand.

Renovation and remodeling activity, bolstered by the Joint Center for Housing Studies of Harvard University's Leading Indicator of Remodeling Activity (LIRA), adds substantial incremental coating volume from the existing building stock. Protective Coatings and Automotive segments represent the second and third-largest end-use categories, respectively, with the Automotive segment benefiting from growing OEM production volumes.

Regional Analysis

U.S. Paints and Coatings Market Insights

The United States represents by far the dominant national market within North America Paints and Coatings, accounting for approximately 85% of regional revenue with an estimated market value of US$ 34.0 Bn in 2026. The U.S. Census Bureau reported annual U.S. construction spending exceeding US$ 2.1 trillion in 2023, generating persistent architectural coating demand from both new builds and the approximately 140 million existing residential and commercial units requiring periodic maintenance and repaints.

The reimposition and expansion of broad-based U.S. tariffs by the Trump Administration in 2025, including 10–25% tariffs on Chinese chemical imports encompassing titanium dioxide (TiO?) pigments, specialty resins, and chemical additives, has materially elevated raw material procurement costs for U.S. coating manufacturers reliant on Chinese supply chains. The escalating U.S.-Iran geopolitical tensions and broader Middle East instability have contributed to petrochemical feedstock price volatility, given the region's significance to global oil and chemical supply chains.

Canada Paints and Coatings Market Trends

Canada represents approximately 15% with an estimated market value of US$ 6 billion in 2026. The Canadian market demonstrates solid growth fundamentals supported by government-backed infrastructure investment, a robust residential construction sector, and growing industrial coating demand from energy, mining, and manufacturing sectors. The Canadian government's Investing in Canada infrastructure plan, committing over CAD 180 Bn over twelve years, supports long-term demand for protective and traffic coatings across bridges, transit systems, and public infrastructure assets.

Canada faces distinctive trade disruption risks arising from U.S. tariff policies, given the deep integration of Canada-U.S. trade flows under the United States-Mexico-Canada Agreement (USMCA). The imposition of U.S. tariffs on Canadian aluminum and steel products, critical substrate materials for industrial coating customers, has created downstream demand uncertainty for protective coating suppliers serving the manufacturing and construction sectors. Petrochemical feedstock price escalation linked to Middle East geopolitical volatility also presents supply cost challenges for Canadian coating manufacturers, given the country's reliance on imported specialty chemical intermediates.

Competitive Landscape

The North America Paints and Coatings market exhibits a highly consolidated competitive structure, with a small group of multinational leaders commanding a dominant revenue share. Market leaders differentiate through proprietary color technology platforms, sustainability certification portfolios, and vertically integrated raw material positions.

Strategic acquisitions, digital color-matching tools, and premium product line extensions represent dominant growth strategies, while emerging competitive pressure from Asian multinationals, including Nippon Paint Holdings and Kansai Paint, is intensifying in industrial and automotive coating segments through targeted North American market entries and joint ventures.

Key Developments

- May 2026: WEG inaugurated a new coatings manufacturing facility and two distribution centers in the United States as part of its North American expansion strategy. The investment strengthens production of high-performance industrial coatings, enhances logistics efficiency, and expands WEG’s presence in key sectors, including HVAC, oil & gas, and water treatment applications.

- April 2026: Axalta announced the launch of the Zencore™ Cabinet Coating System for high-volume North American manufacturers. Built on Zenamel™ technology, the new system combines primer and enamel functionality into a two-step process, helping reduce production complexity, improve throughput, minimize waste, and enhance coating efficiency across industrial applications.

- May 2026: PPG introduced the PPG SELEMIX® 7-140 2K acrylic high-solids topcoat, expanding its industrial coatings portfolio to address rising demand for durable, high-performance finishes. The coating offers enhanced resistance to UV exposure, chemicals, humidity, and mechanical wear, improving long-term protection and application efficiency for industrial equipment and machinery applications.

Companies Covered in North America Paints and Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Axalta Coating Systems

- RPM International Inc.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Akzo Nobel N.V.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Hempel Group

- Benjamin Moore & Co.

- Asian Paints

Frequently Asked Questions

The North America Paints and Coatings market is valued at US$ 40.0 Bn in 2026 and is projected to reach US$ 54.4 Bn by 2033, growing at a CAGR of 4.5% during the forecast period.

The primary growth drivers include the robust residential and commercial construction activity, with the U.S. Census Bureau reporting total U.S. construction spending exceeding US$ 2.1 trillion in 2023, the U.S. Infrastructure Investment and Jobs Act (IIJA) allocating US$ 1.2 trillion for infrastructure rehabilitation, driving protective and traffic coating demand, and tightening U.S. EPA and CARB VOC regulations, accelerating market-wide adoption of water-borne and powder coating technologies.

Acrylic resins dominate the Resin Type segment with approximately 35% market revenue share. Their leadership is driven by superior performance in water-borne architectural formulations, offering excellent UV stability, color retention, and adhesion, combined with broad compatibility with low-VOC regulatory requirements. The American Coatings Association (ACA) confirms that water-based acrylic formulations represent the majority of architectural coating sales in the U.S., reflecting their dominant position in the market's highest-volume end-use segment.

The United States leads the North America Paints and Coatings market with approximately 85% of regional revenue, representing an estimated market value of US$ 34.0 Bn in 2026. The U.S. market's dominance is underpinned by the world's largest construction spending base, substantial automotive and industrial manufacturing activity, and a deeply established architectural coatings retail and professional applicator ecosystem anchored by The Sherwin-Williams Company and PPG Industries, Inc.

The key growth opportunities are powder coating technology expansion for EV components and industrial applications, benefiting from zero-VOC compliance advantages and growing IIJA-driven infrastructure demand and smart and functional coatings, including anti-microbial, heat-reflective, and self-cleaning systems, supported by ENERGY STAR incentives, CDC-acknowledged healthcare infection control imperatives, and the ability to command significant pricing premiums in commercial and institutional markets.

Leading companies include The Sherwin-Williams Company, PPG Industries, Inc., Axalta Coating Systems, RPM International Inc., Benjamin Moore & Co., BASF SE, Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, Hempel Group, and Asian Paints, collectively spanning architectural, industrial, automotive, and protective coating segments across the U.S. and Canada.