- Automotive Components & Materials

- Trailer Axle Market

Trailer Axle Market Size, Share, and Growth Forecast for 2025 - 2032

Trailer Axle Market by Capacity (Upto 8,000 lbs, 8,000 - 15,000 lbs and Above 15,000 lbs), Axle type (Single Axle, Tandem Axle and three or more than three Axle), Application (Lightweight Trailers, Medium-Weight Trailers, and Heavy Trailers), Sales Channel (OEM and Aftermarket), and Regional Analysis for 2025 - 2032

Trailer Axle Market Size and Trends Analysis

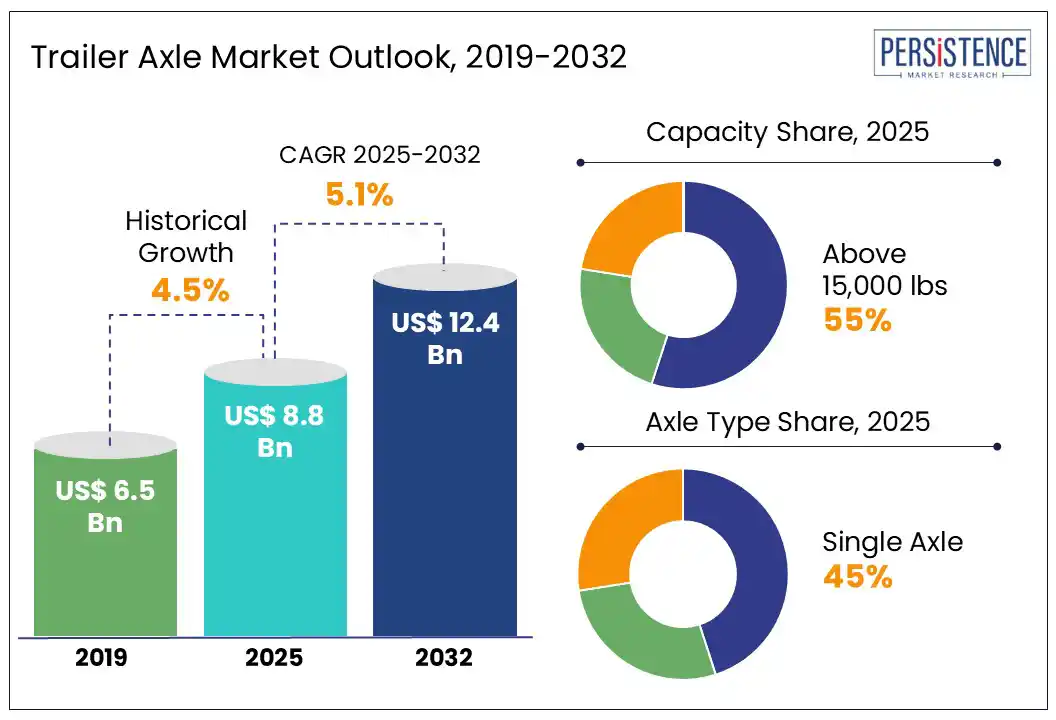

The global trailer axle market size is likely to value at US$ 8.8 Bn in 2025 and reach US$ 12.4 Bn by 2032, growing at a CAGR of 5.1% by 2032. The global market is experiencing significant growth due to the expansion of the automotive and transportation industries, the rising adoption of e-axles in trailers, and stringent emission regulations for transport refrigeration units. However, fluctuating raw material prices pose a challenge to market growth. On the other hand, increasing use of lightweight materials in axle production presents a promising opportunity for market expansion during the forecast period.

Generally, axles are categorized into front, rear, and stub types, and are influenced by the vehicle’s steering mechanism. In trailers, two primary axle types are used, leaf spring axles, that use springs for support and are cost-effective and easy to maintain; and torsion axles, consisting of a square spindle surrounded by rubber that offers smoother rides and reduced maintenance.

Key Industry Highlights:

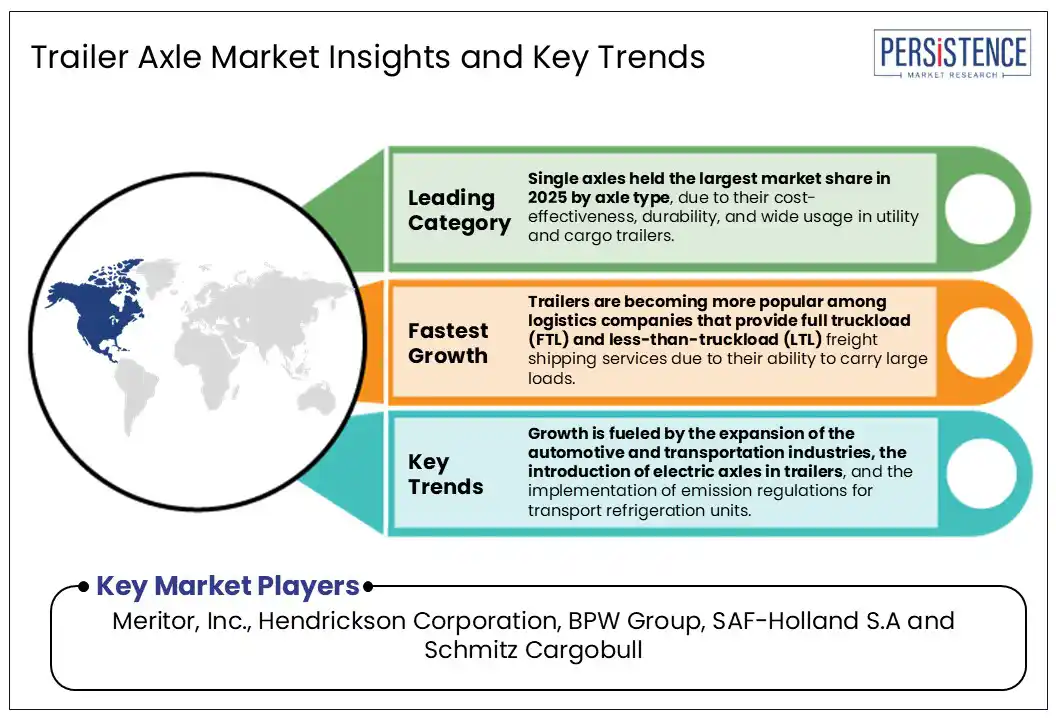

- Global trailer axle market growth is due to the expansion of the automotive and transportation industries, the introduction of electric axles in trailers, and the implementation of emission regulations for transport refrigeration units.

- Trailers are becoming more popular among logistics companies that provide full truckload (FTL) and less-than-truckload (LTL) freight shipping services due to their ability to carry large loads.

- Spring axles held the largest market share in 2025 by axle type, due to their cost-effectiveness, durability, and wide usage in utility and cargo trailers.

- By application, the heavy trailers segment led the market in 2025, owing to the rising need for high-load capacity trailers across the construction and industrial sectors.

- OEM sales channels accounted for the majority of the market in 2025, supported by increased trailer production and direct axle integration at manufacturing levels.

- The 8,000 - 15,000 lbs segment is projected to witness the fastest growth during 2025-2032, supported by demand from agricultural and mid-weight commercial trailers.

- Torsion axles are gaining traction in North America and Europe due to their superior ride quality, reduced maintenance, and better performance in lightweight and medium trailers.

- The aftermarket segment is expected to expand steadily, driven by replacement demand, fleet upgrades, and retrofitting of axles with smart/telematics systems.

| Global Market Attribute | Key Insights |

| Trailer Axle Market Size (2025E) | US$ 8.8 Bn |

| Market Value Forecast (2032F) | US$ 12.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.5% |

Market Dynamics

Driver- Trailer Axle Sales to Accelerate with Growth of Construction Industry

Trailers find a wide range of applications in the construction industry and are used for the transportation of machinery, equipment, and raw materials. The growing construction industry output is expected to be one of the most significant drivers assisting the growth of trailer axle market.

Construction industry is likely to hit the US$ 15 Trn mark by the end of 2025, which will create significant opportunities for manufacturers of trailers and, thus, trailer axles. High load-bearing capacity that facilitates transportation will remain the strongest factor influencing demand for trailer axles within the construction industry.

Freight vehicles are a significant source of emissions, fuel consumption, and climate change. BRICS countries are experiencing a widespread transition to three-axle trailers in the age of industrialization due to an increase in long-distance transportation.

Restraint - Raw Material Price Fluctuations and Stringent Emission Regulations in Automotive Sector

Trailer axle manufacturers are facing significant challenges due to fluctuating prices of raw materials such as steel, aluminum, and composites. These price variations are increasing production costs and reducing overall profitability. Additionally, intense competition, particularly from low-cost Asian manufacturers is pressuring global players to innovate and enhance their product offerings to maintain market share. Economic downturns also reduce demand for new trailers, directly impacting on the need for trailer axles and slowing market growth.

Moreover, strict regulations related to performance, emissions, and safety are making compliance more difficult and costly for manufacturers. These combined pressures from volatile materials pricing to regulatory burdens are hindering the overall stability and growth of the trailer axle market.

Opportunity - Introduction of E-axle in Trailers Create Numerous Growth Opportunities

Electric axles are increasingly being adopted in medium and heavy-duty vehicles, including trailers, due to their benefits such as reduced maintenance costs, lower fuel consumption, and decreased emissions. These e-axles capture energy generated when a trailer rolls freely, converting it into electricity to charge onboard lithium-ion batteries. Driven by growing environmental concerns, manufacturers worldwide are focusing on vehicle electrification, leading to the integration of e-axles in trailers to minimize carbon footprints.

A notable example is Primary Connect, Woolworths Group’s logistics arm, which launched an e-axle trailer in Australia in March 2022. This trailer harnesses kinetic energy from its axle and wheels to generate electricity, supporting Woolworths’ commitment to sustainable supply chain operations. The development and adoption of electric axles in trailers are key factors propelling growth in the trailer axle industry during the forecast period.

Category-wise Analysis

Axle type Insights

Single-axle trailers are generally more affordable to produce, purchase, and maintain, given their lighter weight and fewer components. This makes them especially appealing for budget-sensitive buyers and small enterprises. Single Axle offer better handling in tight spaces ideal for residential areas and urban environments and incur lower rolling resistance, leading to improved fuel efficiency.

Single axles are well-matched to light-weight applications such as landscaping, small transport tasks, camping, and local deliveries, which form a significant and growing segment of the market. Single-axle configurations dominate in uses such as homeowner trailers, small business utility trailers, and lower-load operations segments projected to grow steadily. With fewer tires, brakes, and suspension parts, these trailers reduce the upkeep, which is an appealing feature for commercial fleets and private users alike.

Capacity Insights

The capacity segment dominating the trailer axle market is the Above 15,000 lbs category. The heavy-duty sector maintains the largest share, driven by its critical role in construction, mining, and industrial trailer applications where robustness and load-bearing capacity are essential. While the Upto 8,000 lbs segment retains importance in light trailers and consumer use, and the 8,000-15,000 lbs tier serves medium-duty applications such as regional freight, it’s the above 15,000 lbs capacity range that leads.

The dominance stems from booming infrastructure development, cross-border heavy transport, and equipment hauling needs. Manufacturers prioritize heavier axles for superior durability, higher payload requirements, and better integration with high-power towing vehicles. Consequently, investment, innovation, and production capacity concentrate most heavily on the Above 15,000 lbs segment, making it the primary revenue driver in the trailer axle market.

Regional Insights and Trends

Asia Pacific Trailer Axle Market Trends - Fastest-Growing Market Driven by Logistics and Industrial Expansion

The Asia Pacific trailer axle market has witnessed rapid growth, driven by robust expansion in logistics, construction, and infrastructure sectors across China, India, and Japan. As of 2025, China alone contributes over 50.5% of global trailer production, making it a key growth hub. The region benefits from local axle manufacturing, which keeps production costs and import tariffs low, enhancing affordability and supply efficiency. In recent years, global players like SAF-Holland and BPW have strengthened their presence through joint ventures and greenfield investments with local manufacturers, capitalizing on rising regional demand. For example, SAF-Holland’s partnership with Dongfeng in China aims to expand trailer axle production for heavy-duty applications.

North America Leads Trailer Axle Market Trends - Strong OEM Presence and Advanced Technology Adoption

North America has long been the dominant region in the global trailer axle market and is projected to hold the largest share of 37.3% in 2025. This leadership is driven by the strong transportation and logistics sectors in the U.S. and Canada. The presence of major trailer and commercial vehicle manufacturers like Utility Trailer, Wabash National, Great Dane, Versatile, and Manac has established a well-developed supply chain for trailer axles in the region.

Additionally, global axle manufacturers such as Meritor, Hendrickson, Dexter, and Axle Tech maintain significant production facilities across North America, enabling them to meet large-scale OEM demands efficiently. The region’s early adoption of advanced trailer technologies such as lift axles and independent suspension systems has further fueled market growth by accelerating the transition from traditional rigid axles to more innovative and performance-enhancing alternatives, solidifying North America’s leadership in the trailer axle industry.

Europe Trailer Axle Market Trends - Emphasis on Sustainability and Advanced Axle Technologies

The Europe trailer axle market continues to hold a dominant position, driven by strict emission regulations, a mature logistics industry, and early adoption of advanced trailer technologies. In 2025, Europe is expected to account for a significant share of the global market, with countries such as Germany, France, and the Netherlands leading in production and innovation. The European Union’s focus on zero-emission transportation and road safety has spurred demand for lightweight, intelligent axle systems with integrated telematics, air suspension, and regenerative braking capabilities.

Key regional manufacturers such as BPW Bergische Achsen KG and SAF-Holland are at the forefront of innovation. In 2024, BPW launched its iC Plus intelligent chassis system, enhancing predictive maintenance and fleet efficiency through telematics. Similarly, SAF-Holland expanded its electric axle (SAF TRAKr) production in Germany, aimed at supporting carbon-free refrigerated transport. These advancements solidify Europe’s leadership in sustainable and tech-driven trailer axle solutions.

Competitive Landscape

Cost sensitivity and increasing operational expenses are forcing manufacturers to reduce production, maintenance, and repair costs, which are higher for conventional and older versions of trailer axles. The complexity of axles with braking and suspension systems makes them relatively difficult to handle and maintain. Apart from that, they demand high maintenance, including but not limited to regular lubrication.

The manufacturing and installation costs of a trailer axle vary based on its potential application. Customized trailer applications require more resources and raw materials. Owing to the high input cost, the cost of a customized trailer axle is more than that of an ordinary trailer axle.

Manufacturers are thus focusing on providing the best quality products with maximum efficiency at minimal costs, which marks one of the prominent trends and drivers associated with the global trailer axle market over the forecast period.

Key Industry Developments

- In January 2024, DexKo Global Inc., a US-based manufacturer of trailer running gear, acquired Cerka Industries Ltd. for an undisclosed sum. This acquisition is intended to enhance DexKo’s presence in the trailer component market throughout Canada. Cerka Industries, a Canadian company, specializes in the production of trailer axles and the distribution of components to dealers and OEMs.

- In August 2024, BPW’s ePower generator axle, paired with Thermo King’s refrigeration, proved its real-world reliability: over 350,000 km of testing showed it can power refrigerated trailers using recovered kinetic energy, earning type approval mid-2024 and winning the European Transport Award for Sustainability 2024.

Companies Covered in Trailer Axle Market

- Meritor, Inc.

- Hendrickson Corporation

- BPW Group

- SAF-Holland S.A

- DexKo Global Inc

- Guangdong Fuwa Engineering Group Co., Ltd.

- Schmitz Cargobull

- Gigant - Trenkamp & Gehle GmbH

- Guangzhou TND Axle Co., Ltd.

- Redneck Trailer Supplies

- JOST Axle Systems

- York Transport Equipment (Asia) Pte Ltd.

- H D TRAILERS PVT LTD

- Rogers Willex

- Dexter Axle Company

Frequently Asked Questions

The Trailer Axle market is estimated to be valued at US$ 8.8 Bn in 2025.

Expansion of Logistics & Commercial Transportation and Tech Advancements & Efficiency Push are the major growth drivers.

The trailer axle market is estimated to rise at a CAGR of 5.1% through 2032.

Electrification & E-Axles, and Smart Axles with Telematics & IoT Integration are the key market opportunities.

The global Trailer Axle market is dominated by major players such as Meritor, Inc., Hendrickson Corporation, BPW Group, SAF-Holland S.A and Schmitz Cargobull.