- Automotive

- Automotive Trailer Market

Automotive Trailer Market Size, Share & Forecast 2032

Automotive Trailer Market By Vehicle Type (Two-wheeler and Bike, Passenger Car, Commercial Vehicle), Trailer Type (Dry Van and Box, Refrigerator, Chemical and Liquid), Axle Type (Single, Tandem), and Regional Analysis for 2025 - 2032

Automotive Trailer Market Size and Trends Analysis

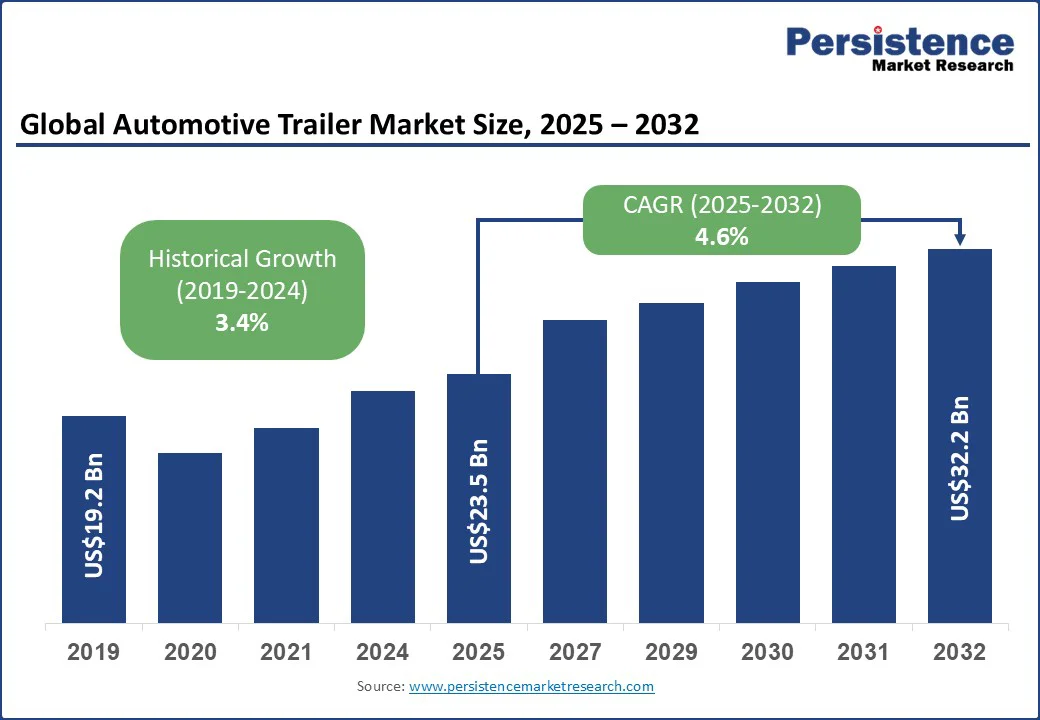

The automotive trailer market size is likely to be valued at US$23.5 Bn in 2025 and reach US$32.2 Bn by 2032 growing at a CAGR of 4.6% during the forecast period from 2025 to 2032.

The automotive trailer market growth is driven by shifting consumer demand, strict environmental norms, and developments in digital technology.

The launch of connected smart trailers that deliver real-time telematics as well as electric refrigerated units made for low-emission delivery zones supplement its need. As companies face the complexities of e-commerce-backed logistics, trailers are considered a decisive factor in operational efficiency.

Key Industry Highlights

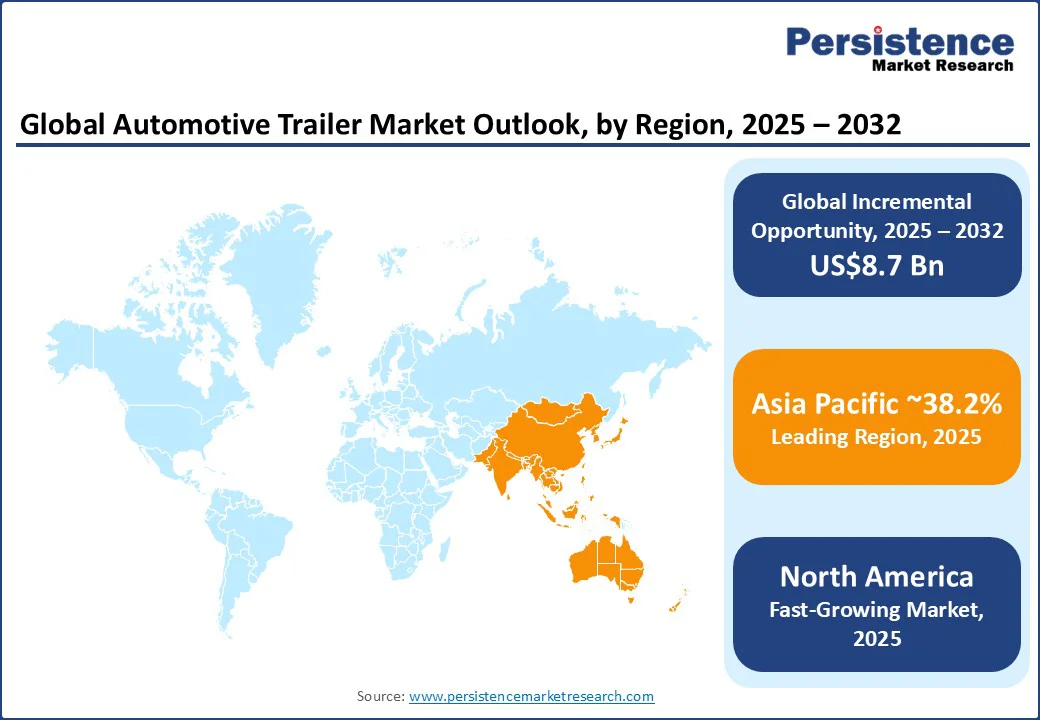

- Leading Region: Asia Pacific with around 38.2% market share in 2025, due to infrastructure upgrades, including new expressways, to support long-haul transport.

- Fastest-growing Region: North America, owing to the rising adoption of smart trailer technologies to improve efficiency and attract investments.

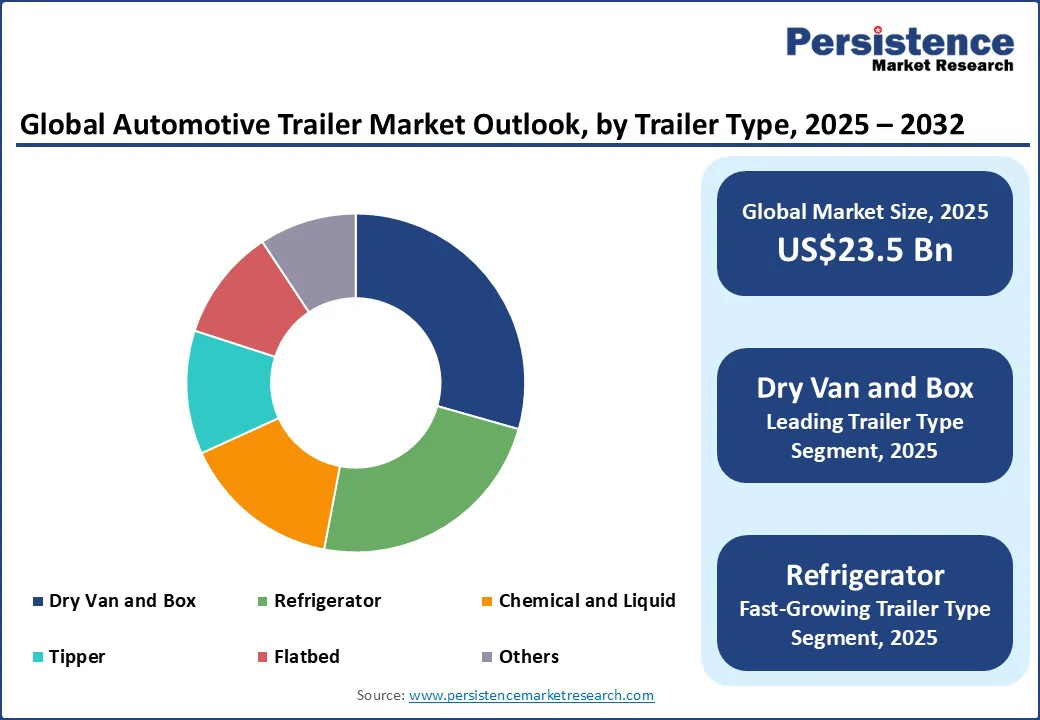

- Dominant Trailer Type: Dry van and box, approximately 29.4% market share in 2025, backed by their surging demand from retail distribution networks in urban areas for better cargo protection.

- Leading Axle Type: Tandem axle holds nearly 30.2% market share in 2025, fueled by regulatory weight compliance in Europe and North America.

- New Product Launch: Propel Industries launched the 4×2 EV Tractor Trailer Truck - 470 eTR at bauma CONEXPO India 2024. With this launch, the company aims to promote the use of electric vehicles to meet the sustainability requirements of the logistics and construction industry in India.

|

Global Market Attribute |

Key Insights |

|

Automotive Trailer Market Size (2025E) |

US$23.5 Bn |

|

Market Value Forecast (2032F) |

US$32.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.4% |

Market Dynamics

Driver - Rising Demand for Perishables Fuels Adoption

The high demand for perishable goods is pushing automotive trailer manufacturers and logistics companies to rethink both design and technology. Perishables require strict temperature control, short transit times, and reliable monitoring. This trend has propelled the demand for refrigerated trailers or reefers, which are now being built with unique insulation materials, hybrid cooling systems, and IoT integration. Pharmaceuticals have become a key driver for high-tech reefer trailers.

Vaccines, biologics, and temperature-sensitive drugs require precise control, often with temperature ranges below freezing. It has encouraged firms to collaborate with fleets in North America and Asia Pacific to deploy trailers with active real-time temperature monitoring and backup power systems. These trailers are also being adapted with Good Distribution Practice (GDP) compliance features. These are now mandatory for pharmaceutical logistics in Europe, creating a premium segment in the trailer industry.

Restraint - Aerodynamic Drag Emerges as a Barrier to Long-haul Efficiency

Fuel efficiency has become a defining metric in fleet operations, and trailers are now under scrutiny for the role they play in raising fuel costs. The added weight from refrigerated units, multi-axle designs, and heavy-duty steel frames directly increases fuel consumption. This makes long-haul trips less economical.

Fleet managers in North America are reluctant to expand with aging or traditional trailer models, as high diesel expenses erode already tight margins in logistics. The concern is rising in Europe, where high fuel taxes accelerate the cost burden. Consequently, a few operators are holding back trailer purchases until lightweight and more aerodynamic options are widely available.

Aerodynamic drag presents another bottleneck, specifically for trailers on long-haul routes. A poorly designed box trailer can generate substantial aerodynamic drag, resulting in increased fuel consumption per 100 kilometers. In the U.S., the Environmental Protection Agency’s SmartWay Program exhibited the drag impact of flat-front trailers. It has led several operators to retrofit with side skirts or tail fairings.

Opportunity - Manufacturers Embed Telematics as Standard to Generate Share

Smart trailer integration is creating opportunities by turning trailers from passive carriers into active assets that generate data and support operational decisions. Fleets that once viewed trailers as interchangeable boxes now see them as platforms for efficiency.

Wabash National’s smart trailer system, launched with telematics partners in 2023, enables operators to monitor cargo temperature, trailer health, and tire pressure in real time. This transforms maintenance from reactive to predictive, reducing downtime and creating new service contracts for manufacturers.

Another opportunity is being created by compliance-heavy industries such as pharmaceuticals and food. Smart trailers equipped with IoT sensors and geofencing provide full traceability, which is important for meeting GDP regulations in Europe or FDA guidelines in the U.S.

Logistics companies handling biologics or high-value fresh produce are paying premiums for connected trailers that ensure regulatory compliance. The trend has prompted manufacturers to embed telematics systems as standard, giving them a competitive advantage with large grocery chains and pharma distributors.

Category-wise Analysis

Trailer Type Insights

Based on trailer type, the market is segregated into dry van and box, refrigerator, chemical and liquid, tipper, flatbed, and others. Among these, dry van and box trailers are expected to account for approximately 29.4% of the automotive trailer market share in 2025, owing to their versatility in accommodating the fragmented demands of modern logistics.

They can move packaged food, electronics, furniture, and apparel without requiring special handling equipment. This flexibility makes them a default choice for retailers and e-commerce giants that require reliable and enclosed transport for mixed loads.

Refrigerated trailers are seeing steady growth as cold chain logistic is no longer limited to frozen food. It now spans pharmaceuticals, high-value fresh produce, specialty beverages, and floriculture. The pandemic highlighted how fragile vaccine and biologic transport can be, pushing regulators and distributors to invest in trailers with precise temperature controls. The boom in online grocery and meal-kit deliveries is another driver.

Axle Type Insights

By axle type, the market is trifurcated into single axle, tandem axle, and three or more axles. Out of these, the tandem axle is poised to account for nearly 30.2% of the share in 2025, as it strikes a balance between payload capacity and maneuverability. This makes it suitable for both regional and long-haul operations. Tandem axles also help distribute loads evenly without compromising fuel efficiency too heavily. Hence, fleets in industries such as retail distribution and construction often standardize on this configuration.

Single axle trailers are gaining traction due to their suitability for urban and regional distribution. London, Paris, and Amsterdam are tightening restrictions on vehicle size and emissions. Logistics companies are adopting single axle box and reefer trailers that can navigate narrow streets and access low-emission delivery zones easily. Weight restrictions and toll regulations are another reason behind this shift.

Regional Insights

Asia Pacific Automotive Trailer Market Trends - China Shifts from Low-cost Supply to Integrated Platforms

In 2025, Asia Pacific is estimated to account for approximately 38.2% of the share, due to China’s mass manufacturing and fast-rising logistics demand. The country’s trailer firms have moved from low-cost supply to platform builders.

They now push product families, export networks, and integrated value chains rather than one-off components. Logistics and e-commerce are the market’s locomotive. Large parcel and cold-chain networks in China and Southeast Asia are upgrading to purpose-built trailers and refrigerated units as online grocery and fresh-food delivery volumes skyrocket.

Leading carriers that run huge vehicle fleets are simultaneously investing in digital operations and specialized trailer types to protect perishable cargo and speed handling. Those fleet moves are transforming demand away from generic box trailers toward temperature-controlled and telematics-ready units.

In India, fleet owners and large logistics integrators are adopting tractor-trailer combos. At the same time, they are experimenting with road-train concepts to cut unit costs on long highway hauls. OEM partnerships are common as logistics firms expand route density on core corridors.

North America Automotive Trailer Market Trends - Recreational Vehicle Boom in the U.S. Adds Momentum

The market is evolving in North America as logistics, agriculture, and construction sectors expand their operations. A key driver is the growth of e-commerce and the resulting pressure on last-mile delivery systems. It has pushed the requirement for light-duty and medium-duty trailers.

Firms such as Utility Trailer Manufacturing Company and Great Dane are responding by developing fuel-efficient and durable models made for regional hauls. Several trailer makers have already introduced lightweight aluminum designs to help fleet operators cut fuel costs while meeting sustainability targets.

A key trend in the U.S. automotive trailer market is the rising integration of digital monitoring systems. Fleets are increasingly adopting telematics and IoT-enabled trailers to monitor cargo temperature, track vehicle health, and prevent theft.

This shift toward connected trailers improves efficiency and allows operators to comply with strict safety and reporting norms. The Recreational Vehicle (RV) boom also plays a key role in pushing demand. The U.S. has seen a rising interest in travel trailers and camper trailers since the pandemic, as more families opt for road trips over air travel.

Europe Automotive Trailer Market Trends - Decarbonization Norms Accelerate Electrification of Trailers

In Europe, the market growth is driven by strict decarbonization norms and the ongoing electrification of freight. Europe-based regulators are compelling fleet operators to cut emissions at every level of the supply chain.

It has led manufacturers to experiment with electric axle systems that can partially power refrigerated trailers or regenerate energy during braking. In 2024, Schmitz launched its S.KOe COOL electric reefer trailer across Germany and the Benelux region. It showed how electrified trailers are moving from pilot projects to large-scale adoption.

Digitization is also a defining trend in Europe’s market. Telematics are no longer an add-on but a standard requirement for most fleets. For instance, Krone Telematics solutions are now integrated into rental trailers. These deliver real-time insights into load conditions, driver behavior, and asset location to fleet managers. This is important as domestic operators balance strict EU Mobility Package compliance with the rising demand for just-in-time delivery.

Competitive Landscape

The global automotive trailer market consists of global full-line manufacturers and regionally specialized players. Key companies dominate with expansive portfolios covering dry vans, reefers, flatbeds, and intermodal solutions. Their strength lies in integrating digital technologies and sustainable designs that enable them to serve multinational logistics firms operating globally. Regional players compete through customization and niche expertise. They focus on heavy-duty trailers ideal for long-haul and high-load conditions where ruggedness matters more than telematics integration.

Key Industry Developments

- In February 2025, Volvo Trucks flagged off India’s first Road Train in Nagpur \ and operated by Delhivery, for long-haul transportation, improving efficiency and capacity in the logistics industry. Road Train features the industry-leading Volvo FM 420 4x2 tractor, a 24-ft containerized intermediate trailer, and a 44-ft semi-trailer.

- In January 2025, EKA Mobility launched an electric tractor-trailer at Auto Expo 2025. The tractor-trailer is equipped with a lithium phosphate battery and has a peak power of 330 kW.

Companies Covered in Automotive Trailer Market

- Böckmann Fahrzeugwerke GmbH

- Dennison Trailers Limited

- China International Marine Containers (Group) Co., Ltd.

- Humbaur GmbH

- Great Dane

- Schmitz Cargobull AG

- Hyundai Motor Group

- Ifor Williams Trailers

- Wabash National Corp.

- Utility Trailer Manufacturing Company

Frequently Asked Questions

The automotive trailer market is projected to reach US$23.5 Bn in 2025.

Rising cold chain demand in the pharmaceutical sector and the expansion of last-mile logistics are key drivers of market growth.

The automotive trailer market is expected to grow at a CAGR of 4.6% from 2025 to 2032.

Key opportunities include integration of telematics and development of solar-powered refrigeration units.

Böckmann Fahrzeugwerke GmbH, Dennison Trailers Limited, and China International Marine Containers (Group) Co., Ltd. are a few key market players.