- Transportation & Logistics

- Flatbed Trailers Market

Flatbed Trailers Market Size, Share, Trends, Growth, Forecasts 2026-2033

Flatbed Trailers Market by Trailer Type (Standard Flatbed Trailers, Step-Deck Flatbed Trailers, Lowboy Flatbed Trailers, Extendable Flatbed Trailers, Other Specialty Trailers), Capacity (Below 25 Tons, 25.1 to 50 Tons, 50.1 to 100 Tons, Above 100 Tons), Number of Axles (Less than 3 Axles, 3 to 4 Axles, Above 4 Axles), and Regional Analysis from 2026 to 2033

Market Overview

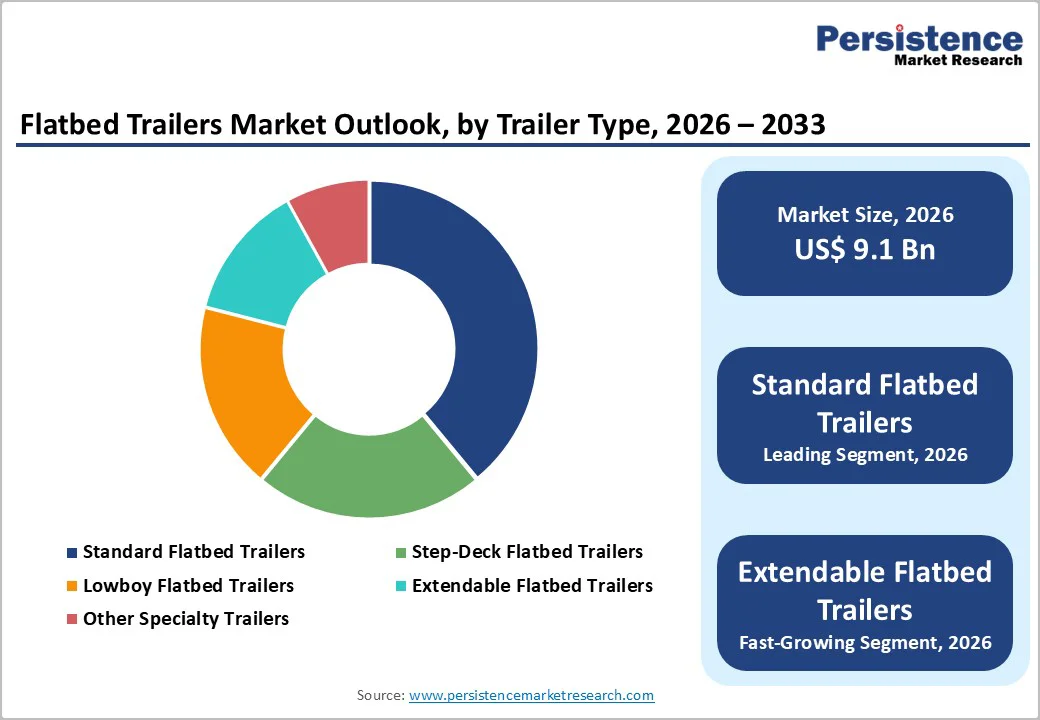

The global Flatbed Trailers Market size is anticipated at US$9.1 billion in 2026 and is projected to reach US$11.0 billion by 2033, growing at a CAGR of 2.7% between 2026 and 2033. Market expansion is driven by global infrastructure projects projected at USD 10 trillion by 2030, accelerating e-commerce, last-mile delivery, and construction requiring heavy-duty transport.

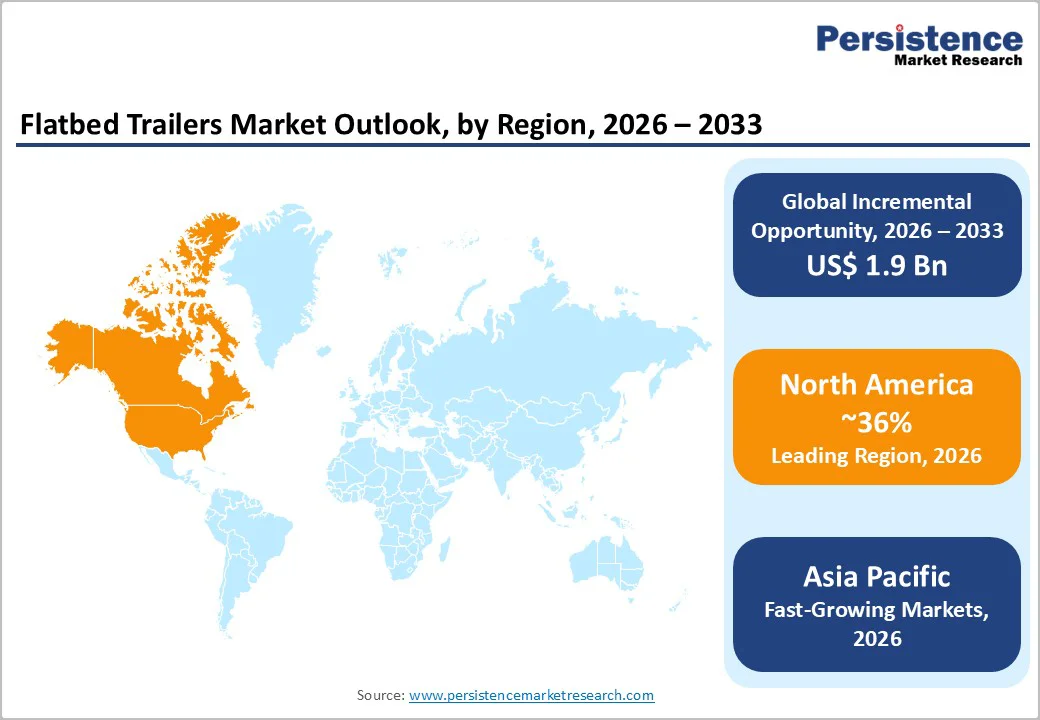

North America holds 36% market share supported by strong freight infrastructure and regulations, Europe contributes 28%, anchored in manufacturing excellence and sustainability, while Asia Pacific grows at 3.2% CAGR with emerging infrastructure and industrial development driving demand.

Key Highlights Summary

- Standard flatbed trailers command 39% market share, reflecting versatility and cost-effectiveness, while Extendable flatbeds expand at 3.9% CAGR as the fastest-growing variant, supporting specialized heavy-load and oversized cargo transport applications.

- 25.1-50 ton capacity commands 35% market share as the industry standard for mid-range freight, while above 100-ton capacity expands at 4% CAGR, supporting heavy equipment and specialized logistics segments.

- 3-4 axle configuration dominates with 42% market share, reflecting regulatory compliance and industry standardization, while above-4-axle systems expand at a 3.5% CAGR for extreme-load applications.

- North America maintains 36% market share with regulatory leadership and technology innovation, Europe contributes 28% share with a sustainability emphasis, and Asia Pacific expands at 3.2% CAGR with emerging market infrastructure development momentum.

- Great Dane advances FleetPulse telematics integration (2024-2025), launches 74% brighter energy-efficient lighting systems (2024), and industry-wide modular design adoption supports rapid customization, demonstrating technology advancement and customer-focused market evolution.

| Key Insights | Details |

|---|---|

|

Flatbed Trailers Market Size (2026E) |

US$ 9.1 billion |

|

Market Value Forecast (2033F) |

US$ 11.0 billion |

|

Projected Growth CAGR (2026-2033) |

2.7% |

|

Historical Market Growth (2020-2025) |

2.4% |

Market Dynamics Analysis

Market Drivers

Global Infrastructure Development and Construction Sector Expansion Supporting Equipment Demand

Global infrastructure investment and construction sector expansion are systematically driving flatbed trailer demand, with infrastructure development projects globally projected to reach USD 10 trillion through 2030, supporting sustained demand for specialized flatbed trailers capable of transporting heavy construction materials, machinery, and prefabricated components across diverse geographic markets and construction segments. Highway and bridge construction requires heavy-load transport. Airport and port modernization supporting infrastructure hubs. Renewable energy projects require specialized equipment transport. Rail and transit system development supporting the movement of construction materials. Building and commercial development requiring construction material delivery. Industrial facility expansion supporting manufacturing infrastructure. Government-funded infrastructure programs accelerating project initiation and equipment demand.

Flatbed Trailer Versatility and Load Flexibility Supporting Diverse Industry Applications

Flatbed trailer versatility and open-deck design providing exceptional load flexibility are systematically driving adoption across diverse industrial segments, with construction, agriculture, manufacturing, and logistics sectors requiring specialized transport for oversized, heavy, and irregularly-shaped loads, supporting sustained demand for platform trailers and specialized variants, including step-deck, lowboy, and extendable configurations. Transportation of construction materials and equipment across project sites. Agricultural machinery and produce movement support farm operations. Manufacturing and industrial equipment relocation and redistribution. Specialized load accommodation for oversized items. Cost-effective transport solutions compared to specialized alternatives. Rapid loading and unloading enable high-throughput operations. Regional freight movement supporting inter-modal transportation networks.

Market Restraints

High Initial Capital Investment and Operating Cost Pressures Limiting Fleet Expansion

Flatbed trailer market expansion is constrained by substantial upfront capital investment requirements with commercial flatbed trailers typically ranging USD 15,000-25,000 depending on specifications and materials, creating adoption barriers particularly for small logistics operators and regional transportation companies limiting market penetration in price-sensitive segments. Financing and leasing challenges for small operators. Maintenance and operational costs increase due to fuel and labor inflation. Regulatory compliance costs for vehicle standards and safety. Insurance and liability expenses for specialized cargo. Driver training requirements for handling oversized loads. Depreciation and equipment lifecycle management challenges. Technology integration costs for telematics and tracking systems.

Regulatory Complexity and Weight/Dimension Restrictions Affecting Vehicle Deployment

Flatbed trailer market expansion is constrained by complex and varying regulatory frameworks governing vehicle weight, dimensions, and load specifications, with state and federal regulations, oversized load permitting requirements, and compliance documentation creating operational complexity and limiting vehicle deployment flexibility, affecting customer adoption and cross-border transportation viability. Weight restriction enforcement varies by jurisdiction. Oversized load permitting requirements and costs. Bridge and infrastructure weight limitations affecting route planning. Driver licensing and certification requirements for heavy loads. Insurance and bonding requirements for oversized transport. Cross-border regulatory harmonization challenges. Dimension restrictions on vehicle length and height.

Market Opportunities

Specialized Flatbed Variants and Customization Enabling Premium Market Positioning

Specialized flatbed trailer development and customization services represent an emerging opportunity, with extendable flatbeds expanding at 3.9% CAGR and the above 100-ton capacity segment growing at 4% CAGR, supporting emerging high-margin segments for specialized applications, including heavy equipment transport, modular construction, and oversized cargo requiring premium solutions. Extendable flatbed technology enabling variable-length configurations. Low-profile lowboy trailers for equipment transport. Modular trailer platforms supporting flexible applications. Customized tie-down systems for specialized loads. Integrated automation and monitoring systems. Advanced materials reducing tare weight. Sustainability-focused designs supporting environmental compliance.

Logistics Technology Integration and Telematics Enabling Service Differentiation

Advanced telematics and logistics technology integration represent emerging opportunity, with IoT and real-time asset tracking systems enabling fleet optimization, predictive maintenance, and operational transparency supporting premium service positioning and customer retention through enhanced visibility and performance monitoring capabilities. Real-time GPS tracking enabling fleet visibility. Predictive maintenance systems reducing downtime. Automated load documentation improves compliance. Driver behavior monitoring enhancing safety. Fuel consumption optimization reducing operating costs. Integration with logistics platforms enabling seamless data exchange. Analytics and insights supporting operational improvements.

Segmentation Analysis

Trailer Types Analysis

Standard flatbed trailers command 39% of market share, representing dominant trailer type reflecting versatile design accommodating diverse cargo types and cost-effective solution for general freight transportation across construction, agriculture, manufacturing, and logistics sectors supporting broad market adoption. Platform configurations supporting flexible load arrangements. Steel and aluminum material options balancing durability and payload. Tie-down systems enabling secure cargo securement. Ramp compatibility supporting loading flexibility. Modular design enabling configuration customization. Regulatory compliance across jurisdictions. Cost-effectiveness supporting broad adoption.

Extendable flatbed trailers are the fastest-growing segment at 3.9% CAGR, driven by variable-length capability for oversized loads and flexible transport solutions. Demand is fueled by equipment transport, modular construction, and heavy logistics, supported by advanced securement systems, heavy-duty payload capacity, specialized equipment handling, premium pricing, niche market focus, and technology advancements enabling new operational capabilities.

Capacity Analysis

25.1-50 ton capacity segment commands 35% of market share, representing established standard for mid-range freight transportation supporting general construction materials, machinery, and logistics applications across diverse industries and geographies. General freight compatibility across industries. Weight distribution optimization supporting safety. Bridge and road compatibility across networks. Regulatory compliance across jurisdictions. Cost-effectiveness supporting broad adoption. Operational flexibility for diverse applications. Proven technology maturity and reliability.

The above 100-ton capacity segment is the fastest-growing at 4% CAGR, driven by heavy equipment and oversized load transport for mining, energy, and industrial applications. Growth is supported by modular facility relocation, specialized design for extreme loads, regional fleet specialization, technology-enabled safe transport, and premium pricing, reflecting emerging demand for high-capacity solutions in heavy-duty logistics and infrastructure projects.

Number of Axle Analysis

3-4 axle configuration commands 42% of market share, representing industry standard for commercial flatbed trailers supporting typical freight loads and bridge weight distribution across general freight, construction, and agricultural applications with proven regulatory compliance and operational reliability. Weight distribution optimization supporting safety standards. Bridge and road compatibility across networks. Regulatory compliance across jurisdictions. Operational efficiency and fuel consumption. Maintenance simplicity reducing downtime. Spare parts availability supporting service networks. Industry standardization enabling interchangeability.

The above 4-axle configuration is the fastest-growing category at 3.5% CAGR, driven by heavy-load transport for mining, infrastructure, and specialized equipment. Growth is supported by weight capacity expansion, optimized load distribution, bridge compliance flexibility, regional axle regulation adaptation, technology-enabled safe operation, and premium pricing, reflecting emerging demand for high-capacity, specialized logistics solutions in heavy-duty transport applications.

Regional Market Insights

North America

North America maintains significant 36% market share, driven by robust freight transportation infrastructure, construction sector strength, regulatory frameworks supporting equipment standardization, and advanced logistics networks supporting market leadership and innovation across commercial transportation segments. U.S. freight transportation dominance supporting sustained demand. Interstate highway system enabling efficient logistics. Construction sector expansion requiring equipment transport. Agricultural sector strength supporting rural logistics. Federal and state regulations enabling standardization. Advanced logistics networks supporting efficiency. Technology innovation ecosystem supporting advancement.

North American market characterized by regulatory clarity and technology leadership with established manufacturers maintaining competitive advantages through scale and innovation. Strong equipment standardization supporting interoperability. Robust supply chains and service networks enabling rapid deployment. Competitive pricing dynamics supporting market accessibility for diverse operator segments.

Europe

Europe maintains significant 28% market share with considerable growth pace, driven by stringent regulatory frameworks, sustainability emphasis, advanced manufacturing heritage, and established logistics networks supporting technology advancement and environmental compliance focus. Germany's manufacturing strength supports industry leadership. UK logistics excellence enabling advanced operations. France's regulatory framework supports compliance standards. Spain distribution hubs supporting regional logistics. EU emission standards driving sustainability focus. Environmental regulations supporting green technology. Advanced manufacturing supporting quality standards.

The European market is characterized by strict regulatory compliance and sustainability emphasis, with manufacturers focusing on environmentally friendly design and operational efficiency. Strong emphasis on fuel efficiency and emission reduction. Established technical standards supporting reliability and safety. Partnership ecosystems supporting innovation and market development.

Asia Pacific

Asia Pacific expands at a prominent 3.2% CAGR, driven by rapid industrialization, urbanization acceleration, emerging market infrastructure development, and construction sector expansion, supporting growth exceeding developed market rates and reflecting emerging market momentum. China's industrial expansion is driving equipment demand. India's infrastructure development supports logistics modernization. Japan's manufacturing supports regional leadership. ASEAN urbanization driving construction growth. Government infrastructure programs supporting capital investment. Manufacturing cost advantages enable competitive pricing. Emerging market growth supporting sustained expansion.

The Asia Pacific market is characterized by rapid growth and infrastructure development, with emerging market operators driving equipment adoption faster than developed markets. Manufacturing presence enabling local production and cost advantages. Government support programs are accelerating infrastructure and equipment investment. Supply chain development creates employment and economic opportunities.

Competitive Landscape

The global flatbed trailers market exhibits moderate consolidation, with multinational leaders including Utility Trailer Manufacturing Company, Great Dane Trailers, and Wabash National Corporation leveraging integrated manufacturing, distribution, and service networks. Regional manufacturers such as Dorsey Trailers and Trailmobile emphasize geographic focus and product specialization, while emerging and customization-focused players capture niche opportunities through innovation, flexible manufacturing, and technology-driven competitive differentiation.

Strategic Developments

- In July 2022, Cox Automotive completed the acquisition of Trudell Holdings, including Trudell Trailer Sales and Northeast Great Dane, covering the Midwest and Northeast.

- April 2025, Trudell rebranded to Midwest Great Dane, expanding Cox's fleet services ecosystem and dealer network consolidation, supporting integrated trailer sales and service capabilities.

Business Strategies

Market leaders drive growth through technology differentiation with advanced telematics and asset tracking, geographic expansion via regional manufacturing and service networks, product customization, sustainability through lightweight materials, supply chain optimization, and customer service excellence. Large multinationals focus on integrated solutions, regional players on cost competitiveness, and specialized manufacturers on niche markets, leveraging technology partnerships and expanded service networks for rapid innovation and accessibility.

Companies Covered in Flatbed Trailers Market

- Utility Trailer Manufacturing Company

- Great Dane Trailers

- Wabash National Corporation

- Trailmobile LLC

- Dorsey Trailers

- Fruehauf Trailer Corporation

- K-Way Trailers

- East Manufacturing Corporation

- Cottrell Trailers

- Hyster-Yale Materials Handling

- Fontaine Commercial Trailers

- Transcraft

Frequently Asked Questions

The global Flatbed Trailers Market is anticipated at US$ 9.1 Billion in 2026 and is projected to reach US$ 11.0 Billion by 2033.

Growth is fueled by global infrastructure and construction expansion, e-commerce and logistics modernization, and flatbed versatility accommodating diverse cargo across construction, agriculture, manufacturing, and logistics sectors.

The market is projected to expand at a 2.7% CAGR between 2026 and 2033.

Strategic growth lies in emerging market infrastructure development, high-margin specialized trailers such as extendable and above 100-ton variants, and logistics technology integration including IoT and telematics for fleet optimization and customer differentiation.

Market leadership is held by Utility Trailer Manufacturing, Great Dane Trailers, and Wabash National, supported by Trailmobile, Dorsey, Fruehauf, and regional specialists, leveraging technology innovations such as FleetPulse telematics, energy-efficient lighting, and modular flatbed design for rapid customization and market expansion.