- Automotive

- Automotive Tire Market

Automotive Tire Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Automotive Tire Market by Product Type (Radial, Bias, Run Flat / Specialty), Season (Summer Tire, Winter Tire, All Season Tire), Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle, Offroad & Other Vehicle), Sales Channel (OEM, Aftermarket), and Regional Analysis from 2026 - 2033

Automotive Tire Market Share and Trends Analysis

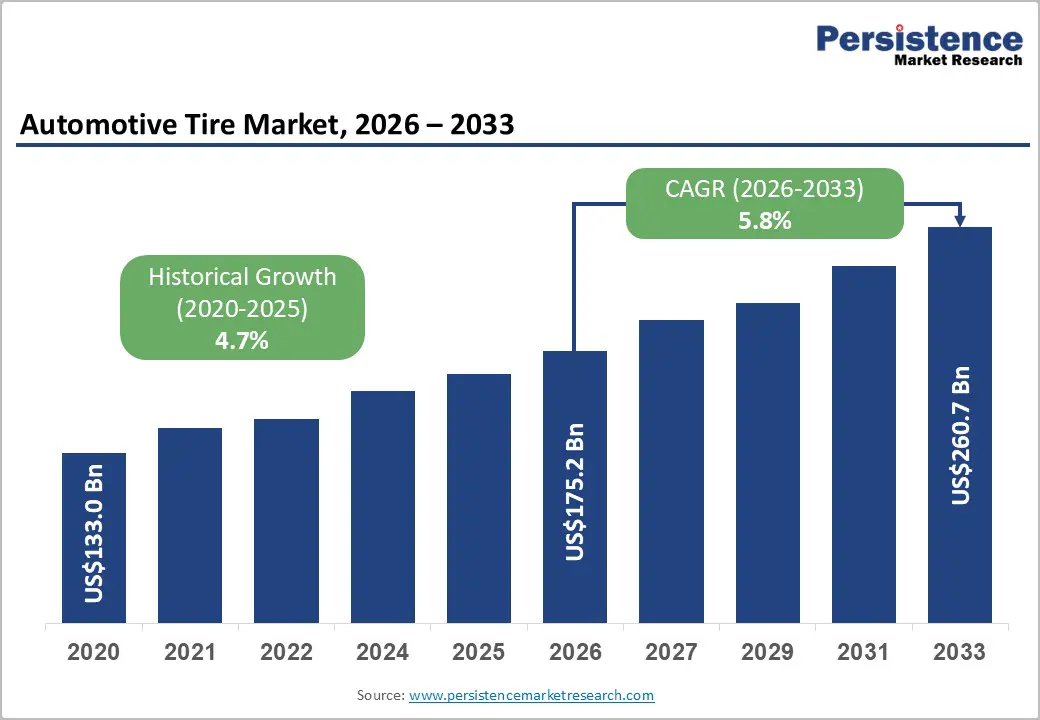

The global automotive tire market size is anticipated at US$ 175.2 billion in 2026 and is projected to reach US$ 260.7 billion by 2033, growing at a CAGR of 5.84% between 2026 and 2033.

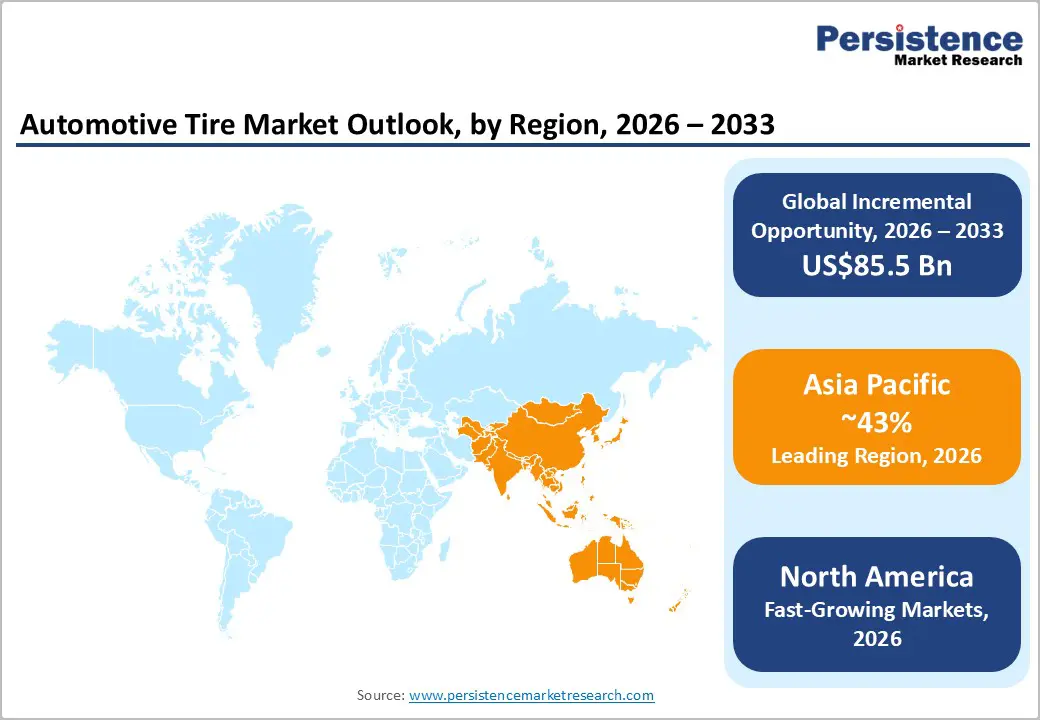

Market expansion is driven by rising vehicle ownership and fleet growth sustaining replacement demand, accelerating electric vehicle adoption with EV tires growing at 10.2% CAGR and the EV segment at 23% CAGR, and smart tire IoT integration enabling real-time monitoring. North America grows at 5.2% CAGR, Europe holds 23% share, and Asia Pacific leads with 43% market share.

Key Industry Highlights:

- Radial tires command 79% market share reflecting superior performance characteristics, while Run-flat/specialty tires expand at 7.8% CAGR, supporting premium safety-conscious and luxury vehicle segments.

- All-season tires dominate at 47% share, reflecting convenience and cost-effectiveness, while Winter tires expand at 5.9% CAGR driven by regulatory requirements and climate considerations.

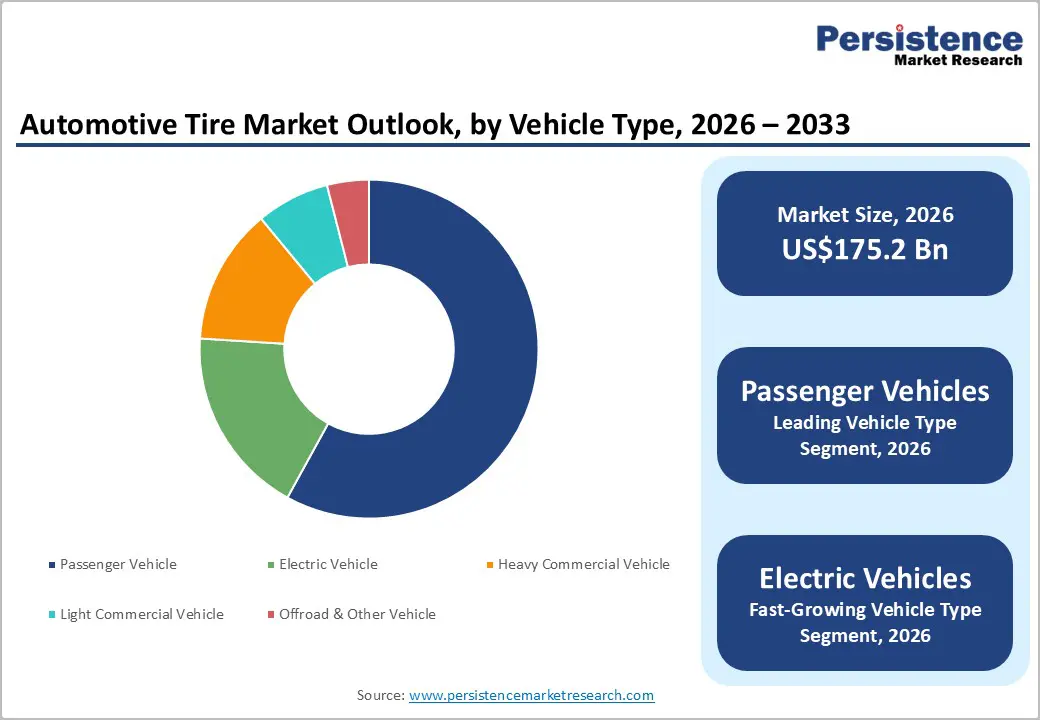

- Passenger vehicles lead with 58% market share, while electric vehicles are rapidly expanding, with the EV tire segment growing at a strong 10.2% CAGR, reflecting significant market potential and rising demand for specialized EV tires by 2025.

- Europe maintains 23% market share with regulatory winter tire requirements emphasis, Asia Pacific dominates 43% with vehicle production leadership and emerging market momentum, and North America grows at 5.2% CAGR with technology and EV adoption.

- CEAT launches calm-technology EV-ready tires with foam inserts, Pirelli launches P Zero Winter 2 for BMW 7 Series EV range enhancement, and Continental declares a complete EV-compatible portfolio serving 9 top 10 EV manufacturers (2023-2024) demonstrating technology advancement and EV market penetration momentum.

| Key Insights | Details |

|---|---|

|

Automotive Tire Market Size (2026E) |

US$ 175.2 billion |

|

Market Value Forecast (2033F) |

US$ 260.7 billion |

|

Projected Growth CAGR (2026-2033) |

5.8% |

|

Historical Market Growth (2020-2025) |

4.7% |

Market Dynamics Analysis

Drivers - Vehicle Ownership Growth and Fleet Replacement Cycles Driving Sustained Tire Demand

Vehicle ownership and fleet expansion are systematically driving tire market growth, with global vehicle production exceeding 85 million units annually and typical tire replacement cycles of three to five years sustaining recurring replacement demand. Expanding vehicle population directly increases tire consumption across passenger cars, commercial fleets, and two-wheel mobility ecosystems. Fleet modernization initiatives are accelerating replacement rates as operators prioritize fuel efficiency, safety compliance, and lifecycle cost optimization. Commercial vehicle expansion, supported by logistics growth and infrastructure development, further strengthens volume demand. Emerging market vehicle ownership continues to rise with improving income levels and urbanization. Ride-sharing and mobility services scaling increase vehicle utilization intensity, while urban transportation investments and road infrastructure expansion collectively reinforce long-term tire demand stability globally worldwide.

Electric Vehicle Adoption Supporting Specialized EV Tire Segment Expansion

Electric vehicle adoption and specialized tire requirements are systematically driving EV tire market growth, with the EV tire market growing at 10.2% CAGR globally. Rising demand centers on low-rolling-resistance tires that optimize driving range, reduced noise profiles suited for quiet electric cabins, and higher torque-handling capability supporting instant acceleration characteristics. Tire engineering increasingly addresses unique EV weight distribution, higher load-bearing requirements, and advanced thermal management essential for battery cooling efficiency and durability. Smart tire integration with EV systems enables real-time condition monitoring, efficiency optimization, and predictive maintenance across connected platforms. Manufacturer standardization efforts and deepening OEM collaboration accelerate large-scale adoption, ensure regulatory compliance, improve supply chain alignment, and reinforce long-term performance reliability across passenger and commercial electric vehicle segments worldwide.

Restraint - Volatile Raw Material Prices and Supply Chain Disruptions Affecting Margins

Tire market expansion is constrained by significant rubber, steel, and chemical component price volatility, creating margin pressure and cost unpredictability for manufacturers while limiting affordability in price-sensitive markets. Natural rubber prices fluctuate with weather patterns and supply concentration, while steel cord and wire pricing remains exposed to energy and capacity cycles. Chemical compound costs vary with feedstock availability and petroleum derivative movements. Ongoing supply chain disruptions amplify procurement risk, while logistics cost inflation raises landed costs. Geopolitical supply constraints, trade barriers, and regional conflicts further destabilize sourcing strategies, complicating long-term pricing contracts, inventory planning, and profitability management across tire operations.

Intense Competition and Market Commoditization Pressuring Pricing Power

Tire market expansion is constrained by intense competition from emerging manufacturers, particularly Chinese and Indian brands, creating sustained pricing pressure and commoditization risk across mid-range and budget segments. Cost-competitive Chinese manufacturers leverage scale and supply chain efficiency, while Indian brands expand aggressively through value positioning. Private label alternatives further dilute brand premiums, while e-commerce platforms disrupt traditional distribution models and intensify price transparency. Rising low-cost imports compress margins for established players, limiting pricing power and profitability. Simultaneously, market consolidation reduces supplier diversity but heightens rivalry among remaining players. Brand differentiation challenges persist as performance gaps narrow, increasing reliance on marketing.

Opportunity - Emerging Market Vehicle Proliferation and Tire Aftermarket Growth

Emerging market vehicle ownership expansion and aftermarket tire replacement represent a substantial opportunity, driven by Asia Pacific dominating 43% market share as China, India, and ASEAN economies record accelerating vehicle ownership growth. Rising personal vehicle penetration and expanding commercial fleets are generating sustained replacement demand across urban and semi-urban markets. Aftermarket tire demand is surging due to increasing vehicle parc age, higher road usage, and cost-conscious consumer behavior. Asia benefits from manufacturing cost advantages, localized supply chains, and scalable production ecosystems supporting competitive pricing. OEMs and tire manufacturers continue developing local production facilities to reduce logistics costs and improve responsiveness. Government-led infrastructure development, logistics corridor expansion, and economic growth further support vehicle investment, fleet expansion, and aftermarket tire demand stability.

Run-Flat and Advanced Tire Technology Supporting Premium and Safety Markets

Run-flat and advanced tire technology represent an emerging market opportunity, with run-flat and specialty tires expanding at a 7.8% CAGR, supporting premium positioning for safety-conscious consumers and luxury vehicle manufacturers. Run-flat technology emphasizes enhanced safety by enabling continued mobility after punctures, reducing roadside risk and downtime. Continuous mobility capability aligns with emergency response requirements and fleet reliability expectations. Luxury vehicle integration is accelerating as OEMs prioritize ride stability, space optimization, and premium performance attributes. Specialty tire innovation also supports expanding all-terrain capability for SUVs and crossovers, addressing diverse driving conditions. Performance tier differentiation allows manufacturers to command higher margins through advanced materials, reinforced sidewalls, and intelligent design, strengthening brand value and technology leadership across premium and high-performance vehicle segments globally.

Category-wise Analysis

Product Type Insights

Radial tires command 79% of market share, representing dominant tire type reflecting superior fuel efficiency, durability, and performance characteristics supporting broad adoption across passenger vehicles, commercial vehicles, and fleet applications globally. Fuel efficiency advantage. Durability and lifespan superiority. Heat dissipation performance. Load capacity capability. Comfort and ride quality. Safety performance standards. Global market standardization.

Radial tires remain the fastest-growing category, while run-flat and specialty tires are expanding prominently at a 7.8% CAGR, driven by luxury OEM requirements and rising safety awareness. Continuous mobility capability enables emergency operation without immediate replacement, enhancing consumer confidence. Growing technology integration, premium pricing justification, and adoption by affluent buyers further strengthen positioning, while autonomous and advanced vehicle platforms increasingly favor run-flat solutions for reliability and safety assurance.

Season Insights

All-season tires command 47% of market share, representing dominant seasonal segment reflecting convenience, cost-effectiveness, and versatility supporting broad consumer adoption across diverse climates and vehicle types eliminating seasonal changeover requirements. Year-round performance. Convenience advantage (no changeover). Cost-effectiveness vs multiple sets. Balanced performance across conditions. Emerging market preference. Rental and fleet standard. Consumer preference dominance.

All-season tires represent the fastest-growing seasonal category, while winter tires are expanding steadily at a 5.9% CAGR, driven by European regulatory mandates and rising climate volatility. Mandatory compliance, improved safety in snow, superior traction, and regional climate adaptation support adoption. Growing consumer awareness of winter performance, insurance premium incentives, and professional positioning further reinforce demand in cold-climate markets globally worldwide.

Vehicle Type Insights

Passenger vehicles command 58% of market share, representing dominant vehicle category reflecting highest global vehicle production volume and broad consumer adoption across diverse geographic markets and demographic segments. Highest production volume globally. Diverse consumer segments. Multiple tire options. Mass-market penetration. Affordability focus. Global distribution networks. Market leadership segment.

Electric vehicles expand as fastest-growing vehicle category by 10.2% CAGR, driven by accelerating EV adoption requiring specialized low-rolling-resistance, low-noise, and high-torque tires supporting emerging high-growth segment with unique tire requirements reflecting fundamental vehicle technology transformation. EV-specific requirements. Low rolling resistance optimization. Noise reduction emphasis. High torque handling. Weight distribution optimization. Range extension focus. Emerging market leadership opportunity.

Sales Channel Insights

Aftermarket channel commands 65% of market share, representing dominant sales channel reflecting replacement tire demand cycles, independent service provider networks, and direct consumer purchasing supporting broad market penetration across geographic markets. Tire replacement cycle demand. Independent service provider networks. Direct consumer purchasing. Regional distribution networks. Online retail expansion. Competitive pricing environment. Service integration capability.

OEM channel expands at 5.3% CAGR, driven by new vehicle production growth and long-term supply contracts supporting sustained revenue generation from vehicle manufacturers preferring factory-fitted tires ensuring quality consistency. New vehicle production growth. Long-term contracts stability. Quality control assurance. Volume commitments predictability. Technology collaboration. Premium positioning. Integrated supply relationships.

Regional Insights

North America Automotive Tire Market Trends

North America automotive tire market is likely to reach 5.2% CAGR, driven by vehicle replacement cycles, EV adoption acceleration, technology innovation leadership, and aftermarket demand supporting market development and premium technology integration. North American market characterized by technology leadership and aftermarket channel dominance with consumers investing in replacement tire quality and performance. Strong emphasis on safety and performance supporting premium product adoption. Established supply chains and service networks enabling rapid new product deployment. Advanced consumer awareness supporting technology and sustainability adoption.

Europe Automotive Tire Market Trends

Europe maintains 23% market share with considerable growth pace, driven by regulatory winter tire requirements, emission standards, sustainability emphasis, and EV adoption supporting technology advancement and regulatory compliance focus. Winter tire regulation compliance. European market characterized by regulatory compliance emphasis and sustainability consciousness with manufacturers focusing on eco-friendly and energy-efficient designs. Strong emphasis on winter tire regulations supporting seasonal tire adoption. Technical standards supporting reliability and performance. Premium positioning attracting high-value customers and specialized tire development.

Asia Pacific Automotive Tire Market Trends

Asia Pacific dominates at 43% market share, driven by vehicle production leadership, emerging market vehicle ownership expansion, manufacturing scale advantages, and EV adoption acceleration supporting market growth exceeding global averages. Asia Pacific market characterized by rapid growth, vehicle production dominance, and emerging market opportunities with China leading through massive EV and tire manufacturing scale. India emerging as high-growth vehicle and tire production hub. Cost-competitive production attracting global supply chain development. Government EV incentive programs accelerating adoption and infrastructure investment momentum.

Competitive Landscape

The automotive tires market is consolidated with multinational leaders like Michelin, Bridgestone, Goodyear, and Continental driving growth through technology innovation, OEM partnerships, and global distribution. Regional specialists such as Pirelli, Sumitomo, Hankook, and Yokohama focus on geographic and product specialization, while emerging Chinese and Indian manufacturers capture opportunities through cost competitiveness and EV tire development.

Strategic Developments:

- In Feb 2025, Hyundai and Michelin announced extended research and development partnership focusing on next-generation tire optimization specifically designed for premium electric vehicles, supporting advanced EV performance and technology integration capabilities.

- In April 2025, Bridgestone announced Turanza 6 tire with ENLITEN technology reducing weight and rolling resistance, selected as OEM equipment for NEW MG S5 EV launch in Thailand, featuring UN R117-04 certification supporting energy efficiency and EV range optimization.

- In August 2025, Pirelli's Cyber Tyre technology embedding sensors in tire tread collecting real-time pressure, temperature, wear data and communicating with vehicle electronics won Vehicle-to-Everything Innovation of the Year award, marking technology leadership in smart connected tires.

Companies Covered in Automotive Tire Market

- Michelin Group

- Bridgestone Corporation

- Goodyear Tire & Rubber

- Continental AG

- Pirelli Tires

- Sumitomo Rubber/Falken

- Hankook Tire

- Yokohama Rubber

- Zhongce Rubber (ZC)

- Sailun Group

- Toyo Tires

- Maxxis/Cheng Shin

- Apollo Tyres

- MRF Tyres

Frequently Asked Questions

The global Automotive Tire Market is anticipated at US$ 175.2 Billion in 2026 and is projected to reach US$ 260.7 Billion by 2033.

Market growth is fueled by recurring replacement cycles from an expanding global vehicle parc, rapid EV adoption requiring specialized tires, and smart tire technologies enabling predictive maintenance and efficiency gains.

The market is projected to expand at a 5.8% CAGR between 2026 and 2033.

Key opportunities lie in high-growth emerging markets, sustainable and circular tire innovations, and premium run-flat and advanced tire technologies supporting safety- and EV-driven demand.

The market is led by Michelin, Bridgestone, Goodyear, Continental, and Pirelli, with strong EV positioning, OEM alliances, sustainability initiatives, and continuous smart-tire technology advancements.