- Automotive

- Semi-Trailer Market

Semi-Trailer Market Size, Share, and Growth Forecast, 2025 - 2032

Semi-Trailer Market By Trailer Type (Dry Van/Box, Refrigerated, Others), Capacity (≤25 Ton, 25-50 Ton), Application, Acquisition Model, and Regional Analysis for 2025 - 2032

Semi-Trailer Market Size and Trends Analysis

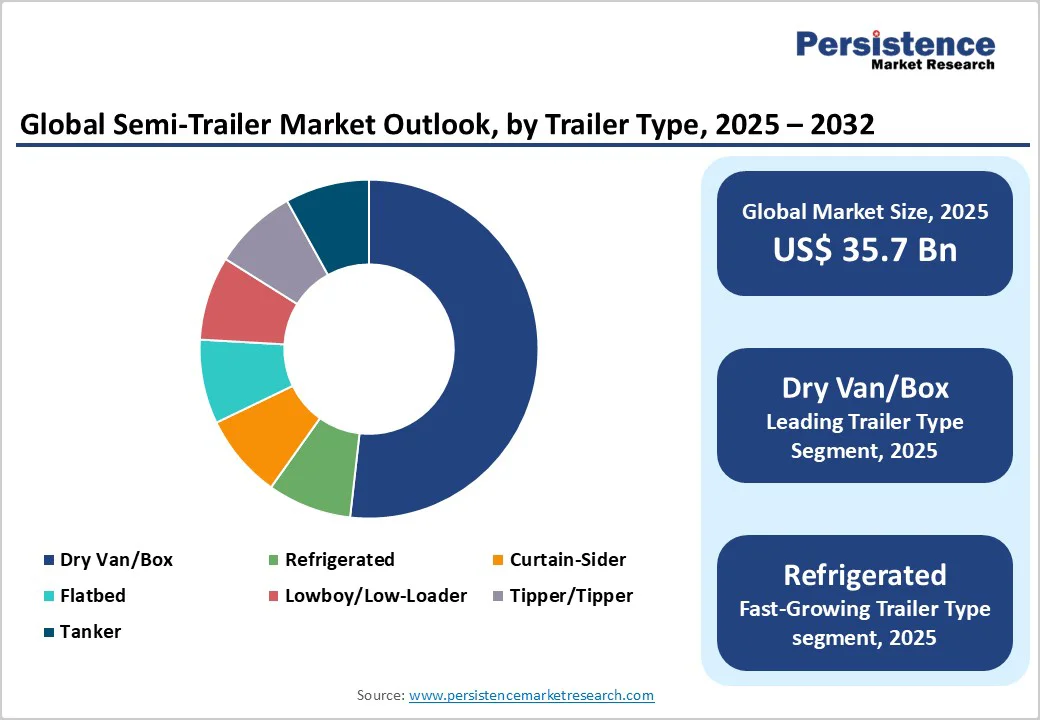

The global semi-trailer market size is likely to be valued at approximately US$35.7 billion in 2025. It is expected to reach about US$52.1 billion by 2032, growing at a CAGR of around 5.7% during the forecast period from 2025 to 2032, driven by expanding e-commerce and logistics demand, fleets’ investment in lighter, digitally-enabled trailer platforms, and regulatory imperatives for upgraded safety and efficiency equipment.

Rising trailer specification standards driven by emerging markets and growing cold-chain refrigeration demand indicate a steady, moderate growth trajectory rather than rapid expansion.

Key Industry Highlights

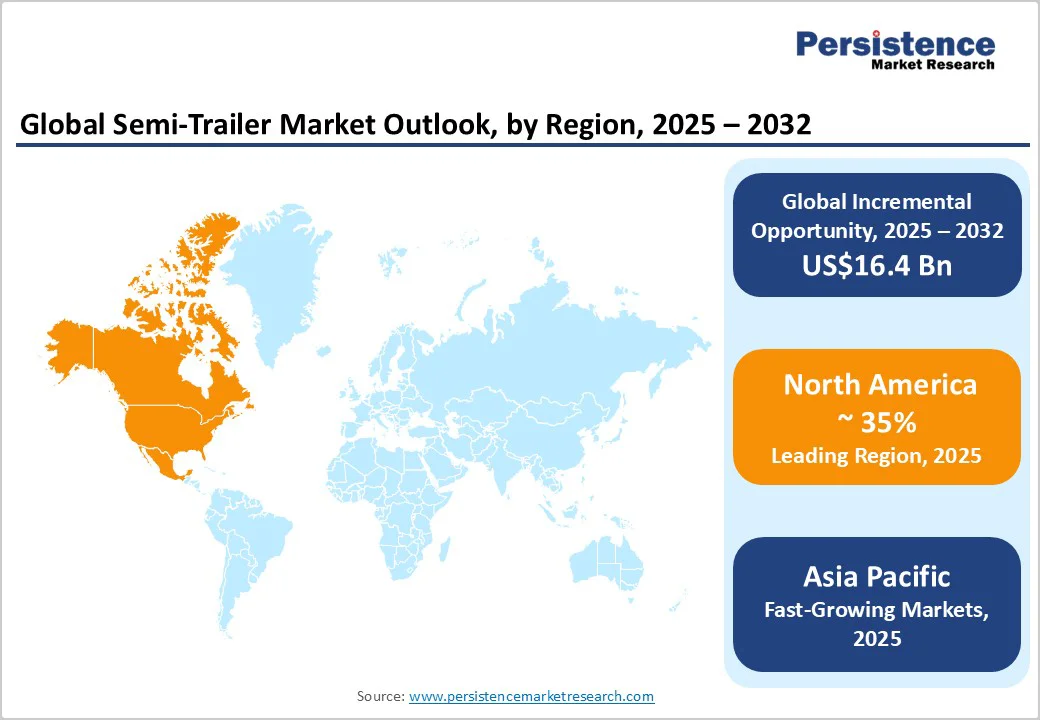

- Leading Region: North America, accounting for around 35% of global market value in 2025, driven by large fleet modernization cycles, advanced telematics integration, and strong replacement demand in the U.S. and Canada.

- Fastest-growing Region: Asia Pacific, supported by logistics infrastructure investment, e-commerce expansion, and rising adoption of refrigerated trailers across China, India, and ASEAN.

- Investment Plans: Global OEMs such as Wabash National, CIMC Vehicles, and Schmitz Cargobull are investing in electric refrigerated trailer technologies, digital telematics platforms, and regional production expansions, with collective planned R&D and capacity investments exceeding US$500 Million through 2026.

- Dominant Trailer Type: Dry Van / Box Trailers hold the leading market share, representing over 60% of global trailer production volume in 2025, supported by broad use in retail, e-commerce, and general freight logistics.

- Leading Capacity: Refrigerated (Reefer) Trailers are the fastest-growing product segment, expected to register a CAGR above 7% during 2025 - 2032, driven by global cold-chain expansion and higher average selling prices due to smart temperature-control systems.

| Key Insights | Details |

|---|---|

| Semi-Trailer Market Size (2025E) | US$35.7 Bn |

| Market Value Forecast (2032F) | US$52.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce Expansion and 3PL Logistics Growth

As online retail and contracted logistics (3PL) build out networks globally, demand for semi-trailers rises. Trailer manufacturers report higher orders for dry-van and curtain-sider configurations in response to increased palletized and parcel freight volumes.

These shifts boost both unit volumes and spec levels (e.g., telematics, higher-durability materials), which in turn raise average selling prices (ASPs) for trailers. This driver is particularly significant in regions where distribution centers, last-mile hubs, and regional freight corridors are being invested in at scale.

Fleet Modernization, Lightweight Materials & Digitalization

Operators are upgrading their fleets to gain payload efficiency, lower fuel cost per ton-km, and improve uptime via digital connectivity. Trailer OEMs are introducing high-strength steel, aluminum, and composite panels, plus factory-fitted telematics, tire-pressure monitoring, and onboard-weighing systems. These trends raise per-unit value and enable recurring service revenue streams. Such enhancements help offset unit-volume growth constraints.

Regulatory & Safety Imperatives

In developed markets (North America, Europe), regulatory regimes concerning vehicle safety (e.g., braking systems, underride protection), emissions-indirect efficiency (weight limits, axle optimization), and digital reporting are pushing fleets to purchase upgraded trailers. These compliance mandates force replacement of legacy units and create demand for higher-spec trailers, supporting revenue growth beyond mere volume expansion.

Barrier Analysis - Freight-cycle Dependence and CAPEX Volatility

Trailer purchases are tightly linked to the freight-transport cycle. During economic slowdowns or freight demand contractions, new trailer orders often defer, and an extension of tractor/trailer life occurs. This leads to softer unit shipments and under-utilized manufacturing capacity. Some forecasts indicate that near-term growth may lag prior estimates by 1-2 percentage points due to such cyclicality.

Input-cost Pressure and Supply-chain Constraints

The trailer value chain is exposed to volatility in steel, aluminum, and electronics prices, and to lead-time risks for telematics/semiconductor components. Rising material or component costs erode OEM margins or force price increases, which may suppress demand-sensitive buyers in cost-conscious markets. Supply bottlenecks can delay deliveries, damaging fleet planning and OEM revenue realization.

Opportunity Analysis - Electrified Trailers & High-efficiency Refrigeration

The shift toward zero-emission logistics and cold-chain freight opens a sub-market for electric semi-trailers (e-axles, battery-powered reefers) and advanced refrigeration units. Trailer OEMs that move into commercial deployments of electric or hybrid refrigerated trailers can capture premium pricing and service models (battery swaps, energy management). By 2030, electrified reefers could unlock an addressable incremental market worth several hundred million dollars across North America and Europe.

Telematics Services, Trailer-as-a-Service (TaaS), and Aftermarket Monetization

Factory-fitted connectivity enables OEMs to offer uptime guarantees, predictive maintenance, and asset-tracking services. These shift revenue models from one-time unit sales to recurring service streams, improving lifetime value. Analysts estimate advanced connectivity and service revenue could amount to 10-20% of new unit value for leading OEMs over the next decade.

Emerging-market Upgrading and Specialty Trailers

Emerging markets (Asia Pacific, parts of Latin America) are investing in logistics infrastructure, cold-chain networks, and heavier/longer haul capacity. That creates demand both for trailer quantity expansion and for upgraded specification (reefers, low-loaders, and specialized heavy-haul). This represents a dual opportunity, volume growth and specification uplifts.

Category-wise Analysis

Trailer Type Insights

Dry van or box trailers dominate the market with a 58% share, driven by their versatility across retail, FMCG, and general freight sectors. Offering enclosed protection against weather, theft, and contamination, they remain the preferred choice for contract logistics, 3PLs, and e-commerce operators.

Leading OEMs such as Great Dane LLC, Utility Trailer Manufacturing, and Wabash National prioritize dry vans due to scale efficiencies and standardized designs that enhance cost competitiveness. In Europe, Krone and Schmitz Cargobull report that box trailers account for nearly two-thirds of their total output, underscoring their strong market position.

Refrigerated trailers represent the fastest-growing segment, fueled by the global expansion of cold-chain logistics for pharmaceuticals, frozen foods, and temperature-sensitive goods. Regulatory standards such as Europe’s GDP and the U.S. FDA’s FSMA are intensifying the need for reliable temperature control.

Manufacturers such as Thermo King and Carrier Transicold have reported double-digit growth in refrigeration unit demand. OEMs are increasingly integrating telematics, real-time monitoring, and energy-efficient technologies, such as Krone’s Smart Refrigeration Trailer and Lamberet’s Eco-Energy series, to improve temperature consistency, reduce emissions, and enhance operational reliability, reflecting the segment’s rapid technological and commercial advancement.

Capacity Insights

The 25-50 ton payload category leads the global trailer market, serving as the core range for most fleet operators. This class offers an optimal balance of load capacity, maneuverability, and operating cost, making it ideal for regional distribution and cross-border logistics across North America, Europe, and China.

Major manufacturers such as CIMC Vehicles Group, Hyundai Translead, and Schmitz Cargobull produce large volumes of medium-duty trailers suited for both regional and long-haul freight. CIMC reported that about 70% of its 2024 trailer sales were in this payload range, reflecting fleet preference for versatility and efficiency.

The growing use of lightweight materials such as high-tensile steel and aluminum enhances payload efficiency while maintaining durability, reinforcing this segment’s dominance.

The heavy-haul and specialized trailer category, exceeding 50 tons, is the fastest-growing segment, propelled by infrastructure, renewable energy, and mining projects. Demand is rising for low-bed, extendable, and modular trailers capable of transporting wind turbine blades, bridge components, and heavy machinery.

Companies such as Goldhofer, Nicolas Industrie, and Faymonville lead this niche, offering advanced hydraulic and multi-axle systems for payloads over 200 tons. Rapid infrastructure expansion in India, Southeast Asia, and the Middle East, alongside Europe’s wind energy projects, continues to drive strong growth in this high-value segment.

Regional Insights

North America Semi-Trailer Market Trends - Digitalization, Fleet Modernization, and Telematics Integration

North America accounts for 35% of the market, making it one of the largest and most mature regions worldwide. Its strength lies in extensive logistics networks, high replacement cycles, and demand for premium trailer specifications.

Major OEMs such as Wabash National Corporation, Great Dane LLC, and Utility Trailer Manufacturing anchor a robust production ecosystem. Canada and Mexico add momentum through cross-border logistics and manufacturing synergies under the USMCA, with Mexico’s expanding role as an export hub boosting demand for trailer and container chassis.

Market growth is fueled by e-commerce logistics, temperature-controlled food distribution, and fleet modernization, emphasizing lightweight materials and advanced telematics.

Evolving business models are transforming operations, as fleet operators increasingly adopt rental and Trailer-as-a-Service (TaaS) models for capital efficiency. Regulatory frameworks, including FMVSS and state-specific size and weight limits, shape design innovation, while underride protection and lighting upgrades spur replacements. North American OEMs are also investing in digitalization and electrification.

In 2025, Wabash National acquired FleetPulse Technologies, enhancing its AI-driven telematics and cargo security platform, while Great Dane partnered with Phillips Connect to expand smart trailer solutions. Utility Trailer Manufacturing introduced its 4000D-X Composite TBR model, offering improved corrosion resistance and weight efficiency, reinforcing the region’s technological leadership.

Europe Semi-Trailer Market Trends - Regulatory Compliance, Electrification, and Premium Engineering Innovation

Europe ranks among the world’s highest-value semi-trailer markets, driven by premium specifications, strict safety standards, and dense intra-EU logistics activity. Leading OEMs such as Schmitz Cargobull AG, Krone Commercial Vehicle Group, and Kögel Trailer GmbH collectively hold 20-30% market share within their categories, solidifying Europe’s status as a manufacturing and export hub.

Germany dominates production and exports, while the UK, France, and Spain serve as major demand centers for dry vans, curtain-siders, and refrigerated trailers supporting retail and distribution. Market growth is propelled by cross-border freight integration, fleet digitalization, and environmental compliance.

EU regulations such as the Vehicle General Safety Regulation (EU) 2019/2144 are driving the adoption of advanced safety systems, while Fit-for-55 climate targets encourage aerodynamic and lightweight trailer innovations.

Competition remains consolidated yet highly innovative. In 2024, Schmitz Cargobull launched the S.KOe COOL, a fully-electric refrigerated trailer featuring an electrified axle with regenerative braking.

In 2025, Krone expanded its Smart Connect telematics ecosystem, offering predictive maintenance, and real-time fleet monitoring. Kögel’s NOVUM platform introduced modular, recyclable designs, enhancing flexibility and sustainability. These advancements highlight Europe’s leadership in electric trailer technology, telematics integration, and low-carbon, high-performance logistics solutions.

Asia Pacific Semi-Trailer Market Trends - Rapid Industrialization, Smart Logistics, and Cost-Efficient Fleet Expansion

Asia Pacific is the fastest-growing regional market for semi-trailers, driven by rapid industrialization, expanding infrastructure, and evolving logistics networks. China leads both production and consumption, supported by its vast manufacturing base and strong domestic freight demand. Japan remains a mature market emphasizing high-specification, automated, and durable trailers.

India, Indonesia, Thailand, and Vietnam are experiencing the fastest unit growth, fueled by e-commerce expansion, logistics modernization, and major infrastructure investments.

India’s market is projected to grow at a 5.5% CAGR from 2026 to 2033, supported by the Gati Shakti Master Plan and rising domestic manufacturing. Key trends include the adoption of lightweight, telematics-enabled trailers and regulatory reforms such as China’s stricter axle load and safety standards and India’s shift to multi-axle configurations, improving freight efficiency.

The regional market remains fragmented yet highly dynamic. CIMC Vehicles Group (China), Hyundai Translead (Korea), Tata DLT (India), and TRAILX (Malaysia) lead innovation across sub-markets.

Competitive strategies focus on localized production, cost efficiency, and reefer fleet development. In 2025, CIMC announced a 15% capacity expansion at its Qingdao facility to boost Southeast Asian exports, while Mahindra Logistics and Tata Motors launched solar-assisted refrigerated trailers, underscoring the region’s growing emphasis on sustainability and energy-efficient cold-chain transport.

Competitive Landscape

The global semi-trailer market is moderately concentrated, with leading OEMs such as Schmitz Cargobull, Krone, Wabash National, and Great Dane dominating premium-value segments, while regional manufacturers capture broad unit volumes. Competition centers on lightweight design, connectivity, and service-network strength.

Key strategies include digitalization, Trailer-as-a-Service (TaaS), telematics, and premiumization through electric and lightweight models. Market leaders focus on integrated data services and uptime guarantees, whereas challengers pursue cost efficiency and rapid expansion in emerging markets.

Key Industry Developments

- In March 2025, Wabash National Corporation unveiled its next-generation EcoNex refrigerated trailer series equipped with advanced composite panels and electric cooling systems to enhance thermal efficiency and reduce CO2 emissions by up to 30%.

- In February 2025, CIMC Vehicles Group Co., Ltd. introduced its Smart Trailer 2.0 lineup with integrated IoT sensors and predictive maintenance capabilities, enhancing safety and operational data analytics for logistics operators across Asia.

Companies Covered in Semi-Trailer Market

- Wabash National Corporation

- Schmitz Cargobull AG

- Great Dane LLC

- Krone Group

- Hyundai Translead

- CIMC Vehicles Group Co., Ltd.

- Kögel Trailer GmbH

- Utility Trailer Manufacturing Company

- Stoughton Trailers LLC

- Lamberet SAS

- Fontaine Trailer Company

- Tirsan Treyler Sanayi ve Ticaret A.Ş.

- Kässbohrer Fahrzeugwerke GmbH

- Dennison Trailers Ltd.

- Fruehauf Trailer Corporation

- Schwarzmüller Group

- Doepker Industries Ltd.

- MAN Truck & Bus SE (Trailer Division)

- Humbaur GmbH

- East Manufacturing Corporation

Frequently Asked Questions

The semi-trailer market size was valued at approximately US$35.7 Billion in 2025.

By 2032, the semi-trailer market is projected to reach US$52.1 Billion.

Key market trends include digitalization and telematics integration for real-time trailer monitoring and predictive maintenance and electrification of refrigerated trailers (reefer units) to reduce emissions and fuel dependency.

The dry van/box trailer segment remains the leading category, accounting for the largest market share in 2025, due to its universal use in general freight and retail logistics.

The semi-trailer market is expected to grow at a compound annual growth rate (CAGR) of 5.7% from 2025 to 2032.

Major players include Schmitz Cargobull AG, Wabash National Corporation, Krone Commercial Vehicle Group, CIMC Vehicles Group Co., Ltd., and Great Dane LLC.