- Transportation & Logistics

- Europe Logging Trailer Market

Europe Logging Trailer Market Size, Trends, Share, Regional Forecasts for 2026 - 2033

Europe Logging Trailer Market by Size/Capacity (Small (upto 15 Ton), Medium (16 to 30 Ton), Large (Above 30 Ton)), Trailer Type (Off-road Trailers, Highway Trailers), Application (Forestry Operations, Timber Transport / Logistics, Construction & Infrastructure, Others), and Regional Analysis for 2026 - 2033

Europe Logging Trailer Market Share and Trends Analysis

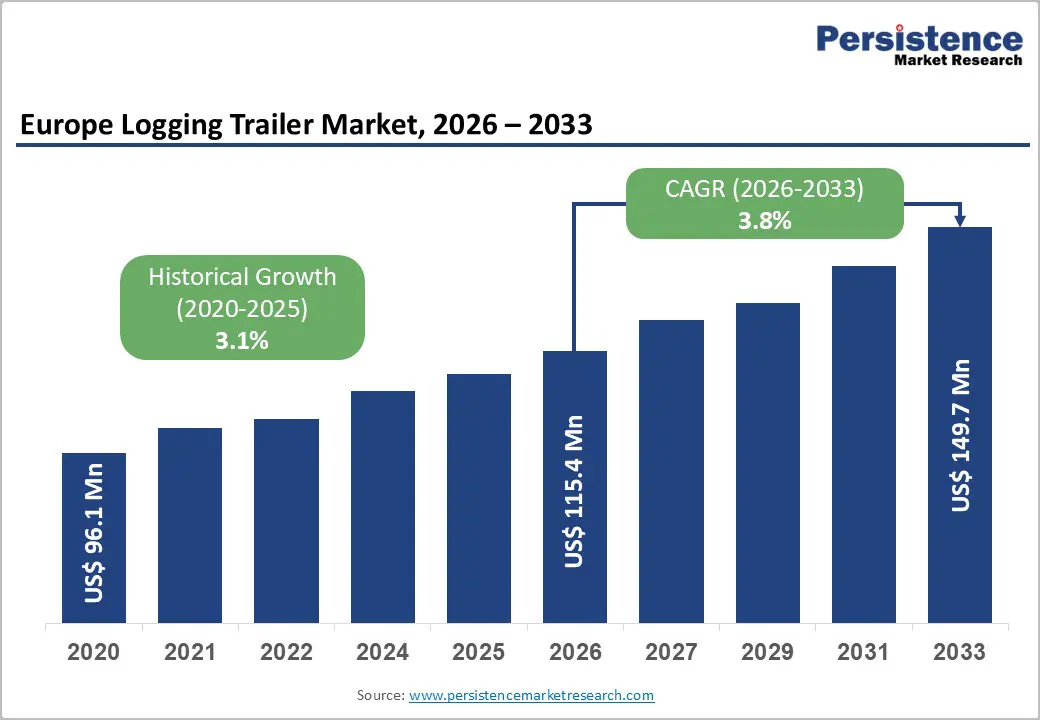

Europe logging trailer market is likely to be valued at US$ 115.4 million in 2026 and is projected to reach US$ 149.7 million by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

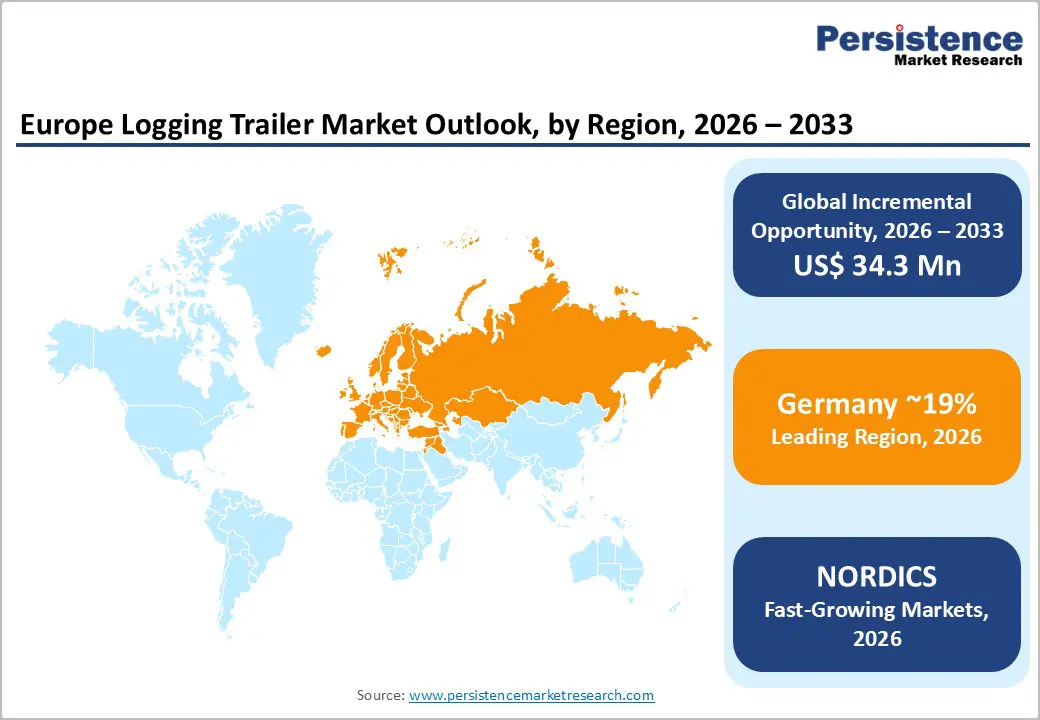

Market expansion is driven by sustained European timber demand supporting renewable construction materials adoption, advancing forestry mechanization requiring sophisticated trailer capabilities for complex terrain navigation, and progressive environmental regulations mandating low-carbon logistics solutions across timber supply chains. Germany maintains market dominance with 19% regional share, leveraging advanced manufacturing and premium vehicle production, while France and Nordic countries demonstrate strong momentum driven by sustainable forestry practices and electrification initiatives supporting decarbonization objectives across the continent.

Key Industry Highlights:

- Capacity Dynamics: Medium-capacity trailers (16-30 ton) lead with 46% market share, while large-capacity variants grow fastest at 3.6% CAGR, driven by timber logistics optimization and rising long-haul, inter-regional transport requirements.

- Trailer Type Trends: Highway trailers dominate with 58% share, while off-road trailers expand at 3.7% CAGR, reflecting continued forest mechanization and demand for equipment capable of operating across complex and uneven terrain.

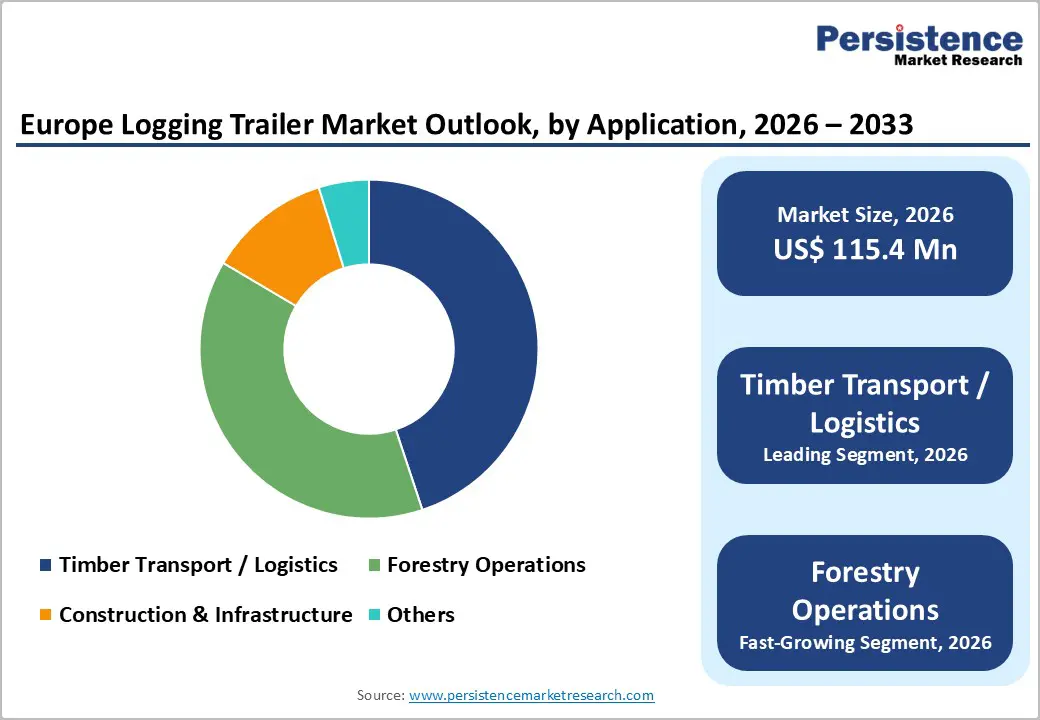

- Application Mix: Timber transport and logistics hold 45% market share, while forestry operations register 3.4% CAGR growth, supported by mechanized forest management and increased mobility needs for harvesting equipment.

- Regional Insights: Germany leads with 19% share due to premium manufacturing strength, while France (15%) and Nordic countries grow at 4.9% CAGR, supported by sustainable forestry leadership and electrification initiatives such as Sweden’s TREE program.

- Competitive Landscape: FTG Group leads the Nordic market through product innovation and customer depth, while Scania’s electric logging truck deployments and TREE program participation highlight accelerating electrification across forestry logistics.

| Key Insights | Details |

|---|---|

| Europe Logging Trailer Market Size (2026E) | US$ 115.4 million |

| Market Value Forecast (2033F) | US$ 149.7 million |

| Projected Growth CAGR (2026 - 2033) | 3.8% |

| Historical Market Growth (2020 - 2025) | 3.1% |

Market Dynamics Analysis

Drivers - Sustainable Forestry Management and Renewable Timber Demand Growth

European sustainable forestry practices and rising demand for renewable construction materials are primary growth catalysts, as global wood production exceeds 2.1 billion cubic meters annually and European forestry generates nearly 80 million tonnes of raw materials transported each year, sustaining demand for specialized logging trailer infrastructure enabling efficient timber logistics. European Union circular economy initiatives, green building certification requirements, and shifting consumer preferences toward sustainable timber products are systematically increasing demand for certified wood transportation solutions. Forestry management emphasizing sustainable yield optimization, reforestation, and carbon sequestration ensures stable harvest volumes requiring advanced logistics capabilities. Major forestry regions across the Nordics, Germany, France, and Central Europe maintain extensive managed forest estates supporting commercial operations under balanced conservation policies. Investments in certified transportation assets are becoming competitive differentiators, with logistics providers adopting specialized trailers supporting traceability, load integrity, and supply chain movement.

EU Climate Targets and Electrification of Forest Transport Operations

European Union climate law mandating a 55% net emissions reduction by 2030 and decarbonization of heavy transport are creating opportunities for forestry trailer suppliers developing electric and hybrid propulsion solutions and low-carbon logistics capabilities. Nordic countries, Finland and Sweden, are advancing pilot electrification initiatives, with Sweden’s TREE program targeting 50% of new forest trucks to be electric by 2030 alongside charging network investments across timber regions. Scania’s deployment of electric logging trucks demonstrates technical feasibility, with pilot operations delivering annual CO2 reductions of around 170 tonnes versus diesel alternatives. European automotive suppliers and forestry equipment manufacturers are progressing electric and hybrid trailer concepts enabling the transition toward zero-emission logistics. Government innovation funding, including Swedish Vinnova support and EU-funded Accelerating Climate Efforts programs, is reducing commercialization risk. Corporate sustainability commitments from timber producers and logistics operators reinforce electrification as essential for EU compliance.

Restraints - High Capital Investment Requirements and Equipment Cost Barriers

Logging trailer manufacturing and deployment involve high capital requirements, as specialized forestry trailers command premium pricing due to advanced engineering, reinforced structures, and features exceeding conventional highway trailer capabilities, constraining replacement cycles among cost-sensitive operators. Electric timber truck programs add further capital intensity, with Scania’s electrified logging truck requiring significant R&D and pilot investments that deter adoption by smaller forestry firms. Charging infrastructure for electrified timber transport presents additional cost barriers, lagging vehicle rollout. Financing constraints facing small contractors delay upgrades despite performance benefits. Supply chain disruptions and volatility in steel, hydraulics, and electronics elevate production costs, compressing margins and sustainability.

Regulatory Compliance Complexity and Equipment Standardization Requirements

European logging trailer operations face complex regulatory frameworks covering transport rules, vehicle safety standards, environmental compliance, and forestry-specific protocols, creating high compliance burdens and limiting manufacturing flexibility across diverse markets. EU vehicle approval and homologation processes extend development timelines and raise engineering costs tied to regulatory adherence. National forestry regulations, timber transport restrictions, weight limits, and axle-load rules vary widely, forcing manufacturers to design multiple product variants. Environmental requirements covering emissions, noise, and fuel efficiency impose lifecycle compliance costs. Equipment standardization initiatives and industry technical specifications restrict differentiation, reducing pricing autonomy within increasingly commoditized market segments across European forestry logistics.

Opportunity - Premium Product Development and Advanced Forestry Technology Integration

Forestry equipment manufacturers developing premium logging trailers with advanced suspension systems, automated loading mechanisms, telemetry capabilities, and specialized features addressing high-value timber operations and complex terrain challenges represent significant market opportunities supporting differentiated positioning and improved profit margins. Telematics and real-time fleet monitoring capabilities are emerging as value-added features supporting remote timber operations, improving operational efficiency, and enabling predictive maintenance, reducing downtime.

Automated securing and lashing systems represent feature differentiation opportunities, improving safety, reducing operator exposure to hazardous environments, and supporting competitive positioning among safety-conscious operators. Lightweight composite materials and advanced steel alloys enable weight reduction improving fuel efficiency and load carrying capacity without sacrificing structural integrity, creating performance differentiation opportunities. Specialized trailer configurations supporting specific timber types, regional harvesting patterns, and supply chain requirements enable customization supporting premium pricing and long-term customer relationships.

Cross-Border Timber Trade and Regional Supply Chain Development

European timber trade expansion, driven by renewable construction material adoption and deeper cross-border supply chain integration, creates opportunities for logistics providers developing trailer solutions enabling international timber transportation, customs compliance, and multimodal logistics connectivity. Growing intra-European timber flows require trailers compatible with road, rail, and port handling systems, supporting efficient cross-border movement. German, French, and Central European timber regions, supported by extensive forest estates, sawmills, and processing infrastructure, represent major demand centers for specialized trailer suppliers serving regional supply chains. Compliance with EU Timber Regulation, including illegal logging prevention, chain-of-custody verification, and sustainable sourcing documentation, is increasing demand for trailers supporting traceability, digital documentation, and inspection readiness across distribution networks. These requirements favor modern trailer platforms enabling transparency, regulatory compliance, and reliable integration within increasingly complex European timber trade ecosystems. This dynamic supports investment and capacity expansion across logistics operators.

Category-wise Analysis

Size/Capacity Insights

Medium capacity logging trailers representing 16 to 30 ton payload capacity command 46% of European market share, representing the dominant specification for diverse forestry operations balancing load capacity, terrain mobility, and operational flexibility across varied European forestry regions. Medium-capacity trailers enable efficient timber transport from forest harvesting sites to intermediate processing facilities, supporting standard forestry workflows and conventional forest road infrastructure. This capacity class demonstrates broad suitability across forestry operation scales from small family-owned operations to larger commercial timber producers, creating a substantial installed base and high replacement demand.

Large-capacity trailers exceeding 30-ton payloads are emerging as a key growth segment, expanding at 3.6% CAGR, driven by logistics efficiency gains, direct long-haul transport from forests to processing facilities, and cost pressures favoring higher payloads per trip. Expanding inter-regional timber trade and applications such as wood-chip transport and industrial processing further support demand for specialized ultra-high-capacity highway trailer configurations globally.

Trailer Type Insights

Highway logging trailers command 58% share, driven by emphasis on long-distance timber transport, integrated European timber supply chains, and highway infrastructure supporting efficient inter-regional wood product movement across the continent. Modern European forestry supply chains incorporate substantial long-haul transport components, with timber moving from regional harvesting operations toward central processing facilities and export terminals, requiring highway-capable trailers optimized for road infrastructure and regulatory compliance.

Off-road timber trailers expand at 3.7% CAGR, driven by forestry mechanization, growing use of specialized forest equipment requiring transport, and complex terrain forestry operations in Alpine, Scandinavian, and Central European regions requiring robust off-road capabilities. Sustainable forestry practices emphasizing selective harvesting and integrated forest management create sustained demand for mobile equipment transportation and specialized terrain navigation.

Application Insights

Timber transport and logistics represents the dominant application, commanding 45% volume, as the fundamental logistics function connecting forest harvesting operations with regional and international timber markets, sawmills, and processing facilities. European timber logistics infrastructure is systematically modernizing to support efficient supply chains, renewable material adoption, and cross-border trade facilitation, creating sustained trailer demand across diverse geographic regions.

Forestry operations represent the fastest-growing application segment, expanding at 3.4% CAGR, driven by mechanized forestry practices, equipment mobilization requirements, and specialized machinery transport supporting modern timber harvest and forest management operations. Advanced forestry equipment including harvesting machines, forwarding equipment, and specialized processing systems require specialized transport solutions supporting operational mobility and regional deployment flexibility.

Regional Market Insights

Germany Logging Trailer Market Share and Insights

Germany maintains a significant share within Europe's logging trailer market, driven by sophisticated manufacturing capabilities, premium vehicle production traditions, and substantial Central European timber supply chains supporting integrated forestry-to-processing workflows. German automotive and commercial vehicle manufacturers leverage precision engineering expertise and advanced manufacturing infrastructure supporting premium forestry trailer development. German timber processing industry, concentrated in Bavaria and other forest-rich regions, creates sustained demand for specialized logistics equipment optimizing supply chain efficiency. German regulatory framework emphasizing vehicle safety, environmental compliance, and equipment standardization supports premium product positioning for suppliers meeting rigorous German quality standards. Industry partnerships between forestry associations, equipment manufacturers, and logistics providers create collaborative ecosystem supporting technology advancement and market development. Investment in electrification initiatives and sustainable transport infrastructure positions Germany as innovation leader supporting emerging zero-emission forestry logistics technologies.

France Logging Trailer Market Trends

France holds approximately 15% of the European logging trailer market, underpinned by sustainable forestry management practices, extensive managed forest estates, and consistent timber production across regions such as Nouvelle-Aquitaine, Grand Est, and Bourgogne-Franche-Comté. The country benefits from a well-established forestry and wood-processing ecosystem encompassing harvesting, sawmilling, pulp, and bioenergy applications, supporting steady demand for specialized timber transport equipment. France’s domestic forestry equipment manufacturing and engineering capabilities strengthen local supply chains, reduce dependence on imports, and enable adaptation to national transport and safety regulations. Public policies emphasizing sustainable forest management, reforestation, and renewable construction materials reinforce long-term timber harvesting stability. Growing inter-regional timber flows within France and cross-border trade with neighboring European markets further support demand for high-capacity, highway-compliant logging trailers optimized for efficiency, traceability, and regulatory compliance, and resilient investment outlook across public and private forestry logistics stakeholders nationwide growth.

Nordic Countries Logging Trailer Market Trends

Nordic countries including Sweden, Finland, and Norway demonstrate the strongest growth momentum at 4.9% CAGR, supported by world-leading sustainable forestry practices, extensive managed forest estates, and high, stable timber harvest volumes. The region benefits from early adoption of mechanized harvesting, digital fleet management, and advanced trailer engineering tailored to harsh operating conditions. FTG Group, through its Moheda, Mowi, and Källefall brands, holds a dominant market position as the clear regional leader in forest trailers, serving domestic forestry operations and European export demand. Strong government backing further reinforces growth, with Sweden’s TREE program and Finland’s electrification pilot initiatives accelerating development of electric, hybrid, and low-emission forestry transport solutions. These coordinated policy, industrial, and innovation ecosystems position the Nordics as Europe’s primary testbed and commercialization hub for next-generation forestry logistics technologies, supporting long-term competitiveness and sustained capital investment across regional supply chains.

Competitive Landscape

Europe logging trailer market shows moderate consolidation, led by Nordic specialists and supported by German and Central European manufacturers serving varied forestry applications. FTG Group dominates Nordic regions through strong relationships, broad portfolios, and technical expertise. German players leverage precision engineering, while independent regional manufacturers compete through customization, service excellence, and niche application specialization supporting diverse forestry requirements.

Strategic Developments:

- In December 2024, Sweden’s TREE (Transition to Efficient Electrified Forestry Transport) program, funded by Vinnova and led by Skogforsk with Scania and forestry partners, launched seven pilot projects targeting 50% electric timber truck adoption by 2030 under demanding Nordic operating conditions.

- In December 2024, Scania deployed the world’s first electric logging truck in Sweden, achieving approximately 170 tonnes of annual CO2 reduction versus diesel alternatives, while integrating charging solutions enabling trailer operations and establishing proof-of-concept for battery-electric forestry transport systems.

Companies Covered in Europe Logging Trailer Market

- FTG Group (Moheda, Mowi, Källefall)

- Kässbohrer

- Balzer

- Brouwer Trailers

- Schwarzmüller

- Chieftain

- FLIEGL

- Stoll

- Binderholz GmbH

- Meuser Trailers

- Scania

- Volvo Trucks

- Holz Reimann

- Rettenmeier

- Smurfit Kappa Group

Frequently Asked Questions

Europe logging trailer market was valued at US$115.4 million in 2026 and is projected to reach US$149.7 million by 2033.

Growth is fueled by sustainable forestry and renewable timber demand, increasing mechanization for complex forest operations, and EU climate policies accelerating low-emission and electric timber transport solutions.

The market is expected to grow at a 3.79% CAGR from 2026 to 2033.

Electrification-ready trailers, premium technology integration such as telematics and automation, and expanding cross-border timber trade offer strong opportunities for differentiation and margin growth.

The market is led by FTG Group in the Nordics, supported by German specialists like Kässbohrer and Schwarzmüller, with Scania and Volvo Trucks driving integrated and electric timber transport solutions.