- Healthcare Services

- Healthcare Quality Management Market

Healthcare Quality Management Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Healthcare Quality Management Market by Software (Business Intelligence & Analytics Solutions, Physician Quality Reporting Solutions, Clinical Risk Management Solutions, Provider Performance Improvement Solutions), Delivery Mode (Cloud, On-premise), Application (Data Management, Risk Management), End-user (Hospitals, Ambulatory Care Centers, Payers, ACOs, Others), Regional Analysis, from 2026 to 2033

Healthcare Quality Management Market Share and Trends Analysis

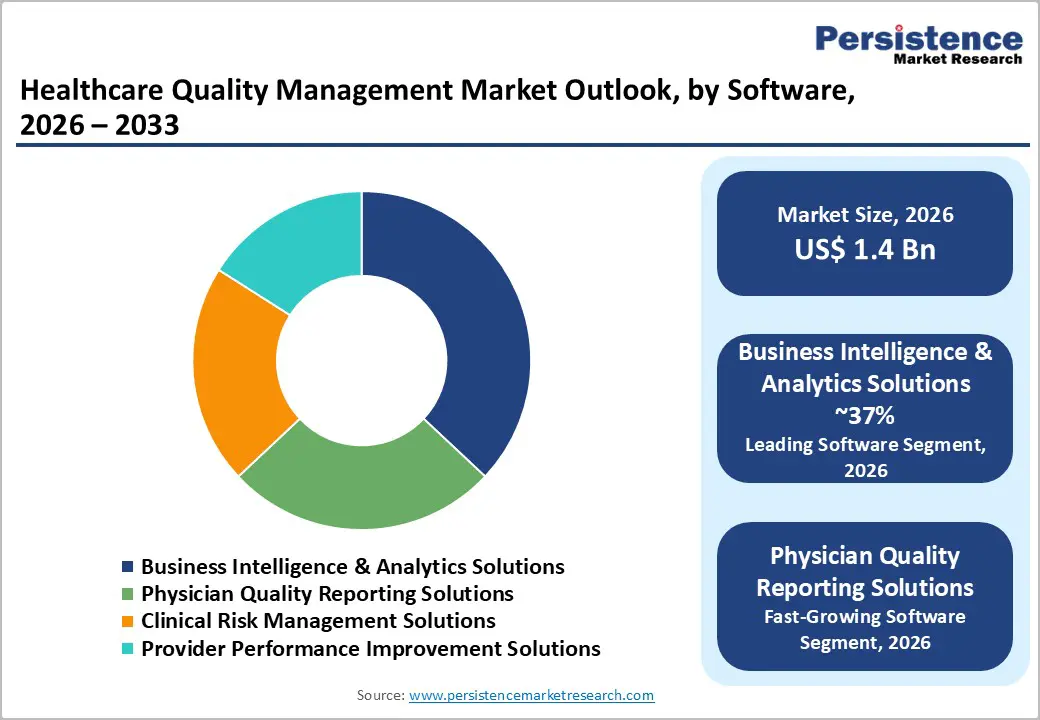

The global healthcare quality management market size is likely to be valued at US$ 1.4 billion in 2026 and US$2.9 billion, growing at a CAGR of 11.6% during the forecast period from 2026 to 2033.

As providers focus on improving clinical outcomes, reducing care variability, and meeting stringent regulatory expectations, the need for quality management in healthcare is widely evident. Growing volumes of patient data and the need to manage it efficiently have encouraged healthcare facilities to adopt structured quality systems. These solutions enable performance benchmarking, error reduction, and compliance with standardized care protocols. Hospitals remain the primary adopters due to high patient volume and operational complexity, while ambulatory care centers are increasing their use. Business intelligence and analytics platforms dominate, supporting data-driven decision-making and continuous improvement initiatives, thereby strengthening overall care quality and operational accountability.

Key Industry Highlights

- Leading Region: North America remains the largest market, driven by advanced EHR adoption, strong CMS value-based programs, and performance improvement tools among hospitals and payers.

- Fastest Growing Region: Asia Pacific is projected to grow at the quickest pace, driven by investment in digital health, telemedicine, and cloud-native analytics that underpin large-scale quality measurement and improvement.

- Dominant Segment: The business Intelligence & Analytics Solutions segment dominates by solution, with around 37% share in 2025, reflecting its central role in aggregating data, computing quality indicators, and delivering actionable performance dashboards to clinical and executive teams.

- Fastest Growing Segment: Cloud deployment is the fastest-growing and leading model with about 58% share in 2025, supported by broader growth in healthcare cloud-based analytics, scalability advantages, and easier regulatory content updates.

| Key Insights | Details |

|---|---|

| Healthcare Quality Management Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.4% |

Market Dynamics

Driver - Rising Need for Data-driven Performance Improvement and Clinical Risk Reduction

The healthcare ecosystem is transitioning toward evidence-based operations, in which large volumes of patient, clinical, and financial data are leveraged for real-time decision-making. Providers are increasingly incorporating business intelligence platforms to gain deeper visibility into treatment patterns, cost drivers, and service outcomes. By integrating electronic health records, claims information, and operational data, these systems enable decision-makers to benchmark performance, identify quality gaps, and streamline workflows. Hospitals deploying analytics-supported dashboards have reported measurable benefits, including lower ICU complications, improved adherence to clinical pathways, and better throughput management, thereby strengthening long-term care delivery outcomes.

As quality management evolves toward predictive models, healthcare organizations are using advanced algorithms for risk stratification, early detection of deterioration, and identification of high-risk patient cohorts. Predictive intelligence supports bed-capacity planning, clinical prioritization, infection risk monitoring, and faster escalation of critical cases. Payers are also using such solutions to detect fraudulent claims, reduce readmission-related costs, and track variations in physician-level outcomes. This shift toward analytics-based decision support significantly accelerates the adoption of structured quality platforms across hospitals, integrated delivery networks, and insurance organizations.

Restraints - Cost Constraints and Shortage of Analytics-Savvy Workforce

Despite substantial advantages, many healthcare organizations face financial and workforce-related barriers when transitioning to advanced quality management platforms. Small hospitals, community care centers, and providers in emerging regions face implementation costs for licenses, integrations, data migration, and staff training. Budget limitations slow adoption and reduce their ability to scale systems across departments. Furthermore, meaningful outcomes from analytics require domain-skilled staff capable of interpreting insights and supporting change programs. However, shortages of clinical informaticists, quality specialists, and data analysts limit organizations' ability to utilize installed solutions fully. Without adequate expertise, analytics remain under-leveraged, delaying measurable quality gains and discouraging reinvestment in advanced systems. These constraints particularly affect resource-constrained settings, reducing the adoption speed of next-generation quality technologies.

Opportunity - Growing Use of Quality Analytics Across Supply Chain, Telehealth, and Population Health

Opportunities are emerging as quality analytics expand beyond inpatient quality metrics into newer domains, such as healthcare supply chain optimization, telehealth outcomes tracking, and population-level monitoring. Quality intelligence platforms are increasingly used to predict essential drug stockouts, reduce wastage, and track variations in vendor-level performance. Improved supply availability and lower procurement risks directly enhance patient safety and operational quality. Hospitals are incorporating predictive supply algorithms to reduce surgical delays and ensure uninterrupted treatment continuity.

Rapid expansion of remote care and community-based management presents another high-value opportunity. Telehealth programs produce vast patient-generated datasets from wearables, diagnostics apps, and remote monitoring platforms. Integrating this information into unified quality dashboards allows providers to evaluate virtual-care success, track adverse outcomes, and measure adherence in real time. Additionally, public health agencies and payers can use population-wide analytics to assess disease progression trends, vaccination effectiveness, and community risk patterns. This opens growth avenues for analytics vendors, documentation systems, and quality-reporting platforms across hospitals, ambulatory networks, and insurers.

Category-wise Analysis

By Solution Insights

Business intelligence and analytics solutions are anticipated to account nearly for 37% share in 2025, positioning them as the most influential software category. These platforms allow healthcare providers to merge data from multiple clinical and administrative systems, evaluate standardized quality indicators, and compare performance across departments in real time. Large academic hospitals adopting these systems have documented improvements in intensive care outcomes, reductions in complications, and measurable gains in operational efficiency. Predictive models supported by BI frameworks help providers lower readmission risks, manage patient flow, and optimize resource use. As health systems shift toward outcome-based reimbursement and value-based programs, the role of analytics-driven quality monitoring continues to grow in importance. This sustained reliance on insight-rich platforms allows BI-centered solutions to outperform traditional reporting modules, reinforcing their dominant market position.

By Deployment Insights

Cloud deployment is set to account for nearly 55% of healthcare quality management installations in 2025, surpassing legacy on-premise systems as the most preferred delivery mode. Growth in cloud adoption across broader analytics and digital health platforms reflects increasing acceptance of subscription-based deployment models among hospitals and payers. Cloud-enabled quality systems reduce capital expenditure, support rapid deployment across multi-facility networks, and simplify updates related to measure definitions, reporting standards, and regulatory changes. This flexibility frequently drives quality compliance programs. Additionally, cloud architectures facilitate integration with complementary platforms, including telehealth, population health analytics, and enterprise clinical data warehouses. The ability to scale storage capacity, process high-volume data streams, and provide real-time dashboards to geographically dispersed users strengthens the market’s shift toward cloud-based offerings, enabling coordinated enterprise-wide quality performance management.

Region-wise Insights

North America Healthcare Quality Management Market Trends

North America, particularly the U.S., is projected to account for the largest share of the healthcare quality management market, nearly 38% of total value in 2025. The region benefits from mature digital health systems, widespread use of electronic health records, and strong payer and regulatory emphasis on improving quality outcomes. Federal initiatives such as value-based purchasing, readmission reduction policies, and accountable care arrangements link reimbursement directly to measurable performance indicators, compelling providers to adopt advanced platforms capable of tracking and improving quality scores in real time.

Technology maturity also plays a central role in sustaining the leadership. Major solution developers, including Cerner Corp. and Premier, Inc., maintain significant footprints in the U.S. and continue to enhance their offerings with integrated analytics and benchmarking capabilities. Hospitals that have implemented these systems have reported stronger closure of care gaps and enhanced visibility into supply chain risks. In addition, consistent investment in artificial intelligence, cloud-enabled analytics, and digital care platforms is creating a favourable environment for next-generation quality tools. With healthcare systems increasingly prioritizing outcome transparency, network-wide performance monitoring, and financial accountability, North America remains the most attractive market for scalable, analytics-driven quality management solutions.

Asia and Pacific Healthcare Quality Management Market Trends

Asia Pacific is emerging as one of the fastest-growing markets for healthcare quality management, driven by large-scale investments in hospital infrastructure, digitization programs, and connected care platforms. Countries including China, India, Japan, and South Korea continue to expand their use of electronic medical records, teleconsultation systems, and cloud-based data platforms, creating a strong foundation for technology-enabled quality monitoring. Telemedicine usage in the region is forecast to increase substantially through the decade, while remote diagnostic tools, wearable monitors, and AI-supported triage systems are becoming widely adopted. Integrating these digital tools with quality reporting systems enables providers to track outcomes, patient experience, and adherence in both hospital and remote environments.

A major competitive advantage for the Asia Pacific is its strong software development ecosystem and cost-efficient IT capabilities, which support the rapid deployment of scalable cloud solutions. Private hospital groups, corporate healthcare networks, and specialty chains are increasingly pursuing centralized quality dashboards to standardize performance across locations. National health programs that emphasize transparency, benchmarking, and accountability are also accelerating adoption. As processes become more structured, demand for advanced analytics, risk assessment solutions, and standardized documentation platforms tailored to domestic regulatory frameworks is expected to increase significantly.

Competitive Landscape

The healthcare quality management market is moderately fragmented, featuring a mix of large healthcare IT vendors, specialist quality and analytics providers, and niche solution developers. Key players such as Cerner Corp., McKesson Corp., Premier, Inc., Nuance Communications, Inc., and others compete on breadth of integrated capabilities, including clinical documentation, performance benchmarking, clinical risk management, and real-time reporting. Strategic priorities include expansion of cloud-native platforms, integration of AI and natural language processing into quality workflows, and broader interoperability with EHRs, payer systems, and population health tools. Many vendors pursue partnerships and acquisitions to add niche capabilities such as advanced analytics, telehealth quality monitoring, or supply chain quality insights while focusing on configurable, role-based dashboards and embedded improvement methodologies as key differentiators.

Key Industry Developments:

- In May 2025, Oracle, the Cleveland Clinic, and G42 formed a strategic partnership to develop an AI-driven global healthcare delivery platform.

- In June 2025, Wolters Kluwer introduced enhancements to Sentri7, improving clinical workflows, medication oversight, and operational efficiency for pharmacy and nursing teams in hospital settings.

Companies Covered in Healthcare Quality Management Market

- Cerner Corp.

- McKesson Corp.

- Premier, Inc.

- Nuance Communications, Inc.

- Altegra Health, Inc.

- CitiusTech Inc.

- Dolbey Systems, Inc.

- Surescripts, LLC

- Medisolv, Inc.

- Quantros, Inc.

- Truven Health Analytics

- Others

Frequently Asked Questions

The global healthcare quality management market is projected to be valued at US$ 1.4 Bn in 2026.

Increasing demand for data-driven performance improvement, regulatory compliance, patient safety, reduced treatment variability, and hospital-wide operational accountability.

The global market is poised to witness a CAGR of 11.6% between 2026 and 2033.

Expansion into telehealth quality analytics, predictive supply chain management, population health monitoring, and cloud-based enterprise-wide reporting platforms.

Major players include Cerner Corp., McKesson Corp., Premier, Inc., Nuance Communications, Inc., Altegra Health, Inc., and CitiusTech Inc.