- Smart Packaging

- Wooden Pallet Market

Wooden Pallet Market Size, Share, and Growth Forecast, 2026 - 2033

Wooden Pallet Market by Material (Softwood, Recycled/Engineered Wood, Other), Product Type (Stringer Pallets, Block Pallets, Others), End-user, and Regional Analysis for 2026 - 2033

Wooden Pallet Market Size and Trends Analysis

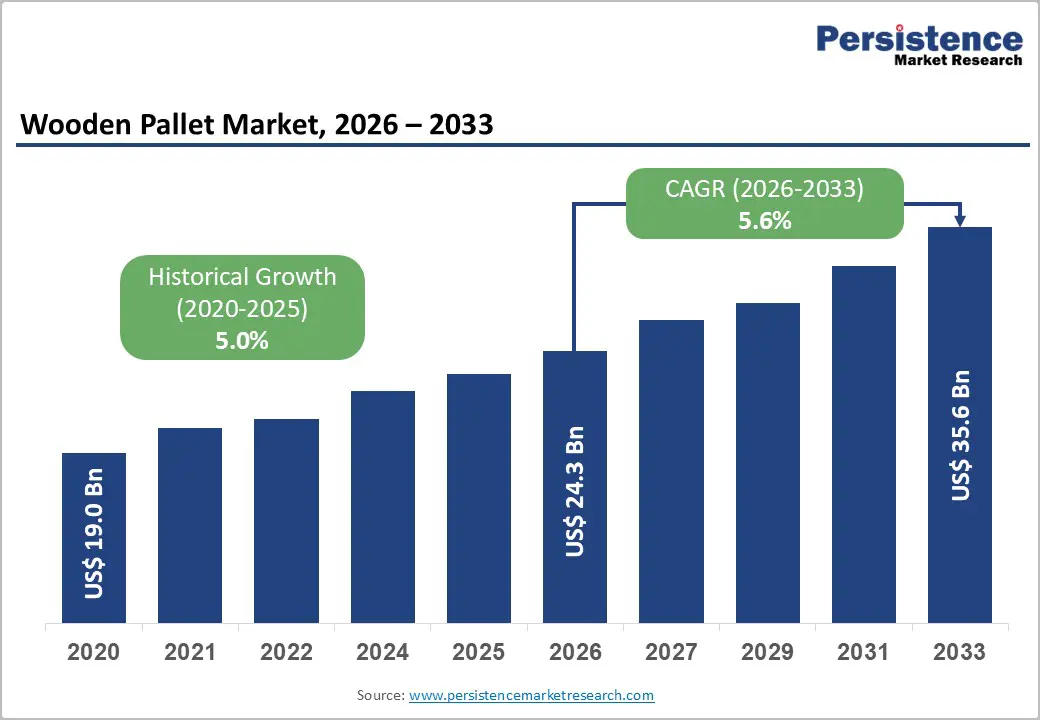

The global wooden pallet market size is likely to be valued at US$ 24.3 billion in 2026 and is expected to reach US$35.6 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, driven by rising e-commerce activity, expansion of third-party logistics networks, and increasing adoption of automated warehousing systems requiring standardized pallet formats.

At the same time, sustainability mandates and international phytosanitary regulations are reshaping supply chains, favoring certified, repairable, and reusable wooden pallet solutions while creating barriers for non-compliant suppliers.

Key Industry Highlights:

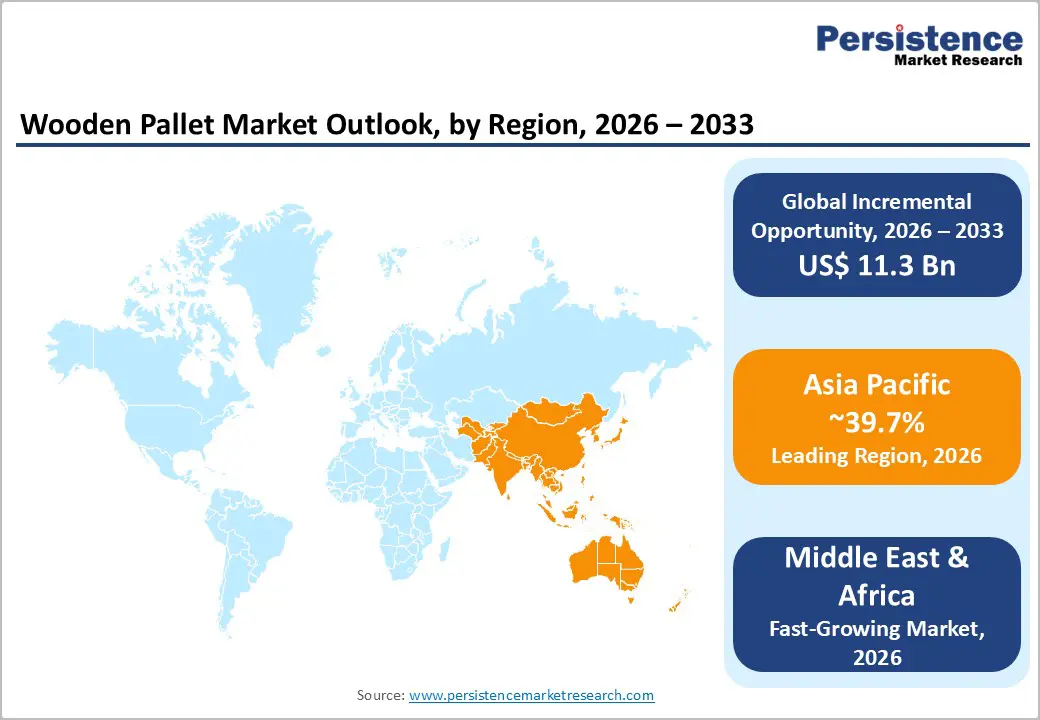

- Leading Region: Asia Pacific is projected to hold the dominant position with 39.7% market share, driven by strong manufacturing output, export activity, and expanding logistics infrastructure across China, India, and ASEAN.

- Fastest-growing Region: The Middle East & Africa is the fastest-growing region, supported by infrastructure development, port modernization, and rising regional trade.

- Investment Plans: Increasing investments in pallet pooling networks, repair and refurbishment hubs, and RFID-enabled tracking systems, particularly in North America and Asia Pacific, with service-based models gaining traction for long-term cost efficiency and sustainability.

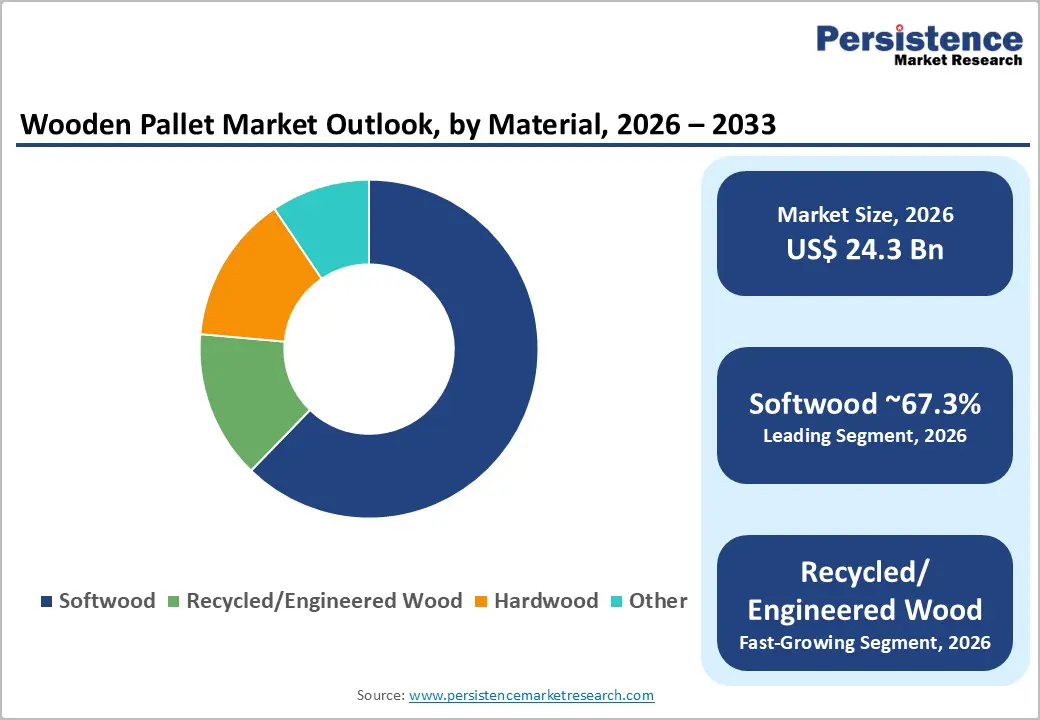

- Dominant Material: Softwood is anticipated to lead with approximately 67.3% market share, owing to its cost efficiency, wide availability, and strong suitability for high-volume logistics and pooling systems.

- Leading Product Type: Stringer pallets are estimated to dominate with around 53.4% share, supported by their low production cost, ease of repair, and widespread use across FMCG, retail, and general logistics industries.

| Key Insights | Details |

|---|---|

| Wooden Pallet Market Size (2026E) | US$24.3 Bn |

| Market Value Forecast (2033F) | US$35.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-Commerce Growth and Warehouse Automation Accelerating Pallet Demand

The rapid expansion of e-commerce has significantly increased pallet throughput in distribution centers, particularly in large-scale fulfillment networks. Automated storage and retrieval systems (AS/RS), conveyor systems, and high-density racking solutions require standardized and durable pallets, particularly block and engineered designs. These systems operate at higher speeds and volumes, increasing wear and replacement cycles. As warehouse automation adoption continues to rise globally, pallet demand benefits from higher utilization rates. This structural shift contributes to incremental annual growth in pallet demand, especially in developed logistics markets, where automation investments are accelerating.

Sustainability and Circular Economy Initiatives Boosting Wooden Pallet Adoption

Environmental regulations and corporate sustainability commitments are driving increased adoption of wooden pallets due to their renewable, repairable, and recyclable nature. Compared to plastic alternatives, wooden pallets offer lower lifecycle emissions when repaired and reused multiple times. Large retailers and logistics providers are increasingly implementing closed-loop pallet systems, emphasizing reuse, refurbishment, and recycling. This trend enhances the economic value of pallets over their lifecycle, enabling suppliers to generate recurring revenue through repair and reverse logistics services. As sustainability reporting becomes mandatory in many regions, demand for eco-friendly load carriers continues to strengthen.

Compliance with Phytosanitary Standards Supporting Certified Suppliers

International trade regulations, particularly phytosanitary standards such as ISPM 15, require wooden pallets to undergo heat treatment or fumigation to prevent pest transmission. Compliance ensures safe cross-border movement of goods but increases operational complexity and cost. Certified pallet manufacturers and pooling providers benefit from this environment, as they can guarantee compliance and traceability. This regulatory framework encourages consolidation among suppliers and shifts demand toward organized players capable of meeting global standards, particularly in export-driven industries such as food & beverage and pharmaceuticals.

Barrier Analysis - Raw material price volatility and supply constraints

The wooden pallet industry is highly dependent on timber availability and pricing. Fluctuations in lumber prices, driven by seasonal harvesting, construction demand, and trade policies, can significantly impact production costs. A sustained 10-20% increase in timber prices can compress margins for manufacturers, particularly smaller players with limited pricing power. Supply chain disruptions also lead to longer lead times and increased inventory holding costs, affecting operational efficiency.

Fragmented market structure and inconsistent quality standards

The market remains fragmented, with numerous small and regional manufacturers operating alongside larger organized players. This fragmentation results in variability in product quality and compliance levels, especially regarding treatment standards for export pallets. Buyers sourcing from non-certified suppliers may incur additional costs related to inspection, rework, or re-treatment. This can increase total logistics costs by 10-20%, creating inefficiencies and limiting scalability for smaller manufacturers lacking certification infrastructure.

Opportunity Analysis - Expansion of pallet pooling models in emerging markets

Pallet pooling systems, which operate on a pay-per-use and asset-sharing model, are gaining traction beyond developed markets. In regions such as Asia Pacific and the Middle East & Africa, rapid growth in retail, FMCG, and e-commerce sectors is creating strong demand for efficient pallet management solutions. Pooling reduces upfront capital expenditure for end users while enabling standardization, higher asset utilization, and reduced pallet loss rates. It also generates recurring revenue streams for service providers, improving business predictability. Investment in regional pooling networks, repair hubs, and reverse logistics infrastructure presents a significant opportunity, particularly in emerging logistics corridors where organized pallet systems are still underpenetrated.

Growth of engineered and high-performance wooden pallets

Engineered wooden pallets are witnessing increased adoption in industries that require high load stability, dimensional consistency, and compatibility with automated handling systems. These pallets use advanced construction techniques such as laminated wood structures and precision fastening methods to enhance strength while reducing overall weight. They are particularly in demand in sectors such as pharmaceuticals, chemicals, electronics, and export logistics, where product safety and regulatory compliance are critical. Their ability to withstand repeated use and harsh transport conditions improves lifecycle value. Manufacturers offering customized, certified, and application-specific engineered solutions can command premium pricing while strengthening long-term customer relationships and differentiation in a competitive market.

Integration of digital tracking and IoT technologies

The integration of RFID, IoT sensors, and digital tracking platforms into wooden pallets is transforming traditional pallet management into a data-driven system. These technologies enable real-time tracking, location visibility, and condition monitoring, significantly improving asset utilization and reducing loss or theft. Such capabilities are increasingly critical for high-value and time-sensitive supply chains, including pharmaceuticals, food distribution, and cold-chain logistics. Digitalization also supports predictive maintenance, inventory optimization, and supply chain transparency, helping companies reduce operational inefficiencies. As adoption increases, pallet service providers can offer value-added services and analytics-driven solutions, creating new revenue streams and enhancing customer retention.

Category-wise Analysis

Material Insights

Softwood is anticipated to dominate the market, accounting for approximately 67.3% of the market share in 2026. Its widespread use is driven by cost efficiency, abundant availability, and ease of processing, particularly in regions with strong forestry industries such as North America and parts of Europe. Softwood pallets are extensively used in FMCG, retail, agriculture, and general logistics, where high-volume, cost-sensitive shipments are common. For example, large retail distribution chains and beverage companies rely heavily on softwood pallets for daily inventory movement. Their ease of repair, recyclability, and compatibility with pooling systems further strengthen their position as the preferred material for standardized pallet applications.

Recycled and engineered wood are anticipated to be the fastest-growing segment. Growth is supported by increasing sustainability regulations, circular economy initiatives, and demand for higher-performance pallets in automated environments. Recycled wood pallets help reduce landfill waste and lower carbon footprints, making them attractive to companies with ESG commitments. Engineered wood pallets, which incorporate laminated structures or composite wood elements, offer enhanced load-bearing capacity, uniform dimensions, and resistance to warping, making them suitable for export logistics and high-precision industries. For instance, pharmaceutical distributors and electronics manufacturers increasingly adopt engineered pallets for secure, contamination-controlled, and automation-compatible transport solutions.

Product Type Insights

Stringer pallets are anticipated to lead the market with an estimated 53.4% share in 2026. Their dominance stems from low production costs, simple construction, and widespread compatibility with conventional material handling equipment, such as forklifts and pallet jacks. These pallets are widely used across industries that prioritize affordability and operational simplicity, including food & beverage, consumer goods, and light manufacturing. For example, grocery distribution centers and packaging warehouses commonly use stringer pallets for short-haul and domestic transportation. Their ease of repair and availability of replacement components further enhance their lifecycle value, particularly in high-turnover environments.

Block pallets are anticipated to be the fastest-growing segment. Their four-way entry design, superior structural integrity, and compatibility with automated storage and retrieval systems (AS/RS) make them increasingly preferred in modern logistics operations. These pallets are widely used in automated warehouses, export shipments, and high-density racking systems, where stability and precision are critical. For instance, large e-commerce fulfillment centers and pharmaceutical supply chains are rapidly transitioning toward block pallets to reduce product damage, improve handling efficiency, and support robotics-based operations.

Regional Insights

North America Wooden Pallet Market Trends - Automation-Driven Pooling and Recycling Ecosystem

North America represents a mature and high-value market, characterized by advanced logistics infrastructure, strong regulatory compliance, and widespread adoption of pallet pooling systems. The U.S. leads the region, supported by well-established retail, e-commerce, and manufacturing sectors. The presence of major pooling and logistics providers such as Brambles Limited (CHEP) and PECO Pallet has accelerated the shift toward closed-loop pallet systems and standardized pallet usage. High levels of warehouse automation, particularly among large retailers and e-commerce companies, are driving increased demand for block and engineered pallets that can integrate seamlessly with automated storage and retrieval systems. Key growth drivers include continued e-commerce expansion, sustainability initiatives, and automation investments.

For example, companies such as Amazon and Walmart are investing heavily in automated fulfillment centers across the region, increasing pallet throughput and accelerating replacement cycles. Regulatory frameworks emphasize compliance with heat treatment standards and environmental sustainability practices, particularly for export packaging. Investment activity is increasingly focused on repair and refurbishment networks, as well as digital tracking technologies such as RFID. Industry players such as UFP Industries are expanding pallet recycling and remanufacturing operations, while consolidation among regional manufacturers is improving supply chain efficiency and service coverage.

Middle East & Africa Wooden Pallet Market Trends - Infrastructure-Led Growth and Export Logistics Expansion

The Middle East & Africa region is the fastest-growing market, driven by rapid infrastructure development, expanding retail networks, and increasing trade flows. Key growth markets include the UAE, Saudi Arabia, and South Africa, where logistics modernization and industrial diversification are accelerating demand for palletized transport solutions. Strategic investments in logistics hubs such as Jebel Ali Port have significantly improved cargo handling capacity, increasing the need for export-grade, ISPM-compliant wooden pallets. Demand in the region is driven by port modernization, cold-chain expansion, and regional trade integration, particularly in food exports and pharmaceutical distribution.

For instance, the growth of retail chains and food distribution networks in Saudi Arabia, supported by companies such as Almarai, is increasing demand for high-volume pallet usage and standardized logistics systems. However, regulatory inconsistencies across countries create challenges, especially in enforcing phytosanitary standards. This creates opportunities for global players such as Brambles Limited and regional logistics firms to introduce standardized pooling models and compliant pallet solutions. Investment opportunities are concentrated in repair hubs, pallet pooling systems, and export packaging infrastructure, particularly along emerging trade corridors connecting Africa to Middle Eastern markets.

Asia Pacific Wooden Pallet Market Trends - Manufacturing Scale and E-commerce Fueled Volume Leadership

Asia Pacific is projected to lead the market, accounting for 39.7% of market share in 2026, driven by its extensive manufacturing base, export-oriented economies, and rapidly expanding logistics infrastructure. Major contributors include China, India, Japan, and key ASEAN economies such as Vietnam and Indonesia. The region’s dominance is closely tied to its role as a global manufacturing hub, where large volumes of goods require cost-effective and compliant pallet solutions for both domestic distribution and export. Growth is supported by industrial production, e-commerce expansion, and increasing investments in logistics infrastructure.

For example, e-commerce leaders such as Alibaba Group and Flipkart are expanding warehouse networks, driving demand for standardized pallets compatible with automation. At the same time, pallet pooling providers such as Loscam are strengthening their presence across Asia by expanding service networks and introducing reusable pallet solutions. Governments across the region are also investing in logistics corridors and cold-chain infrastructure, which further increases pallet demand.

Regulatory compliance for export packaging, particularly adherence to phytosanitary standards, remains critical for countries, including China and India. Increasing adoption of repair, reuse, and pooling systems reflects a shift toward more organized and sustainable supply chains. These developments are reinforcing Asia Pacific’s position as the primary growth engine and volume leader in the global wooden pallet market.

Competitive Landscape

The global wooden pallet market is highly fragmented, with numerous small manufacturers operating alongside large pooling and service providers. While manufacturing remains decentralized, the service segment shows increasing consolidation, driven by the need for scale, certification, and logistics integration. Competitive differentiation is based on geographic reach, service offerings, and compliance capabilities. Key strategies include expansion of pooling services, investment in automation-compatible pallet designs, adoption of digital tracking technologies, and focus on sustainability initiatives. Companies are also pursuing vertical integration and geographic expansion to strengthen market presence.

Key Industry Developments:

- In December 2025, Brambles Limited (CHEP) announced the rollout of its “Climate Smart Partners Program”, aimed at reducing Scope 3 emissions across its supply chain, strengthening its sustainability leadership, and reinforcing demand for reusable wooden pallet pooling systems.

- In October 2025, Mubadala Investment Company completed the acquisition of a significant stake in Loscam, enhancing Loscam’s financial capacity to expand pallet pooling infrastructure across Asia Pacific and the Middle East.

Companies Covered in Wooden Pallet Market

- Brambles Limited

- PalletOne

- Loscam

- PECO Pallet

- UFP Industries

- Kamps Pallets

- Millwood Inc.

- Falkenhahn AG

- PGS Group

- Nefab Group

- Craemer GmbH

- Rehrig Pacific Company

- Menasha Packaging Company

- John Rock Inc.

- CHEP

- CABKA Group

Frequently Asked Questions

The global wooden pallet market is estimated to be valued at US$24.3 billion in 2026.

The wooden pallet market is projected to reach US$ 35.6 billion by 2033.

Key trends include rising adoption of pallet pooling systems, increasing use of engineered and recyclable wood pallets, integration of RFID and IoT tracking technologies, and growing demand from automated warehouses and e-commerce fulfillment centers.

The softwood segment leads the market, accounting for approximately 67.3% share, due to its cost-effectiveness, availability, and suitability for high-volume logistics operations.

The wooden pallet market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Some of the major players include Brambles Limited, PalletOne, Loscam, PECO Pallet, and UFP Industries.