- Healthcare Services

- Mental Health Apps Market

Mental Health Apps Market Size, Share, and Growth Forecast, 2026 - 2033

Mental Health Apps Market by Platform (iOS, Android, Others), Application (Depression & Anxiety Management, Mindfulness & Meditation, Stress Management, Others), Subscription Model (Free Apps, Paid Subscription), and Regional Analysis for 2026 - 2033

Mental Health Apps Market Share and Trends Analysis

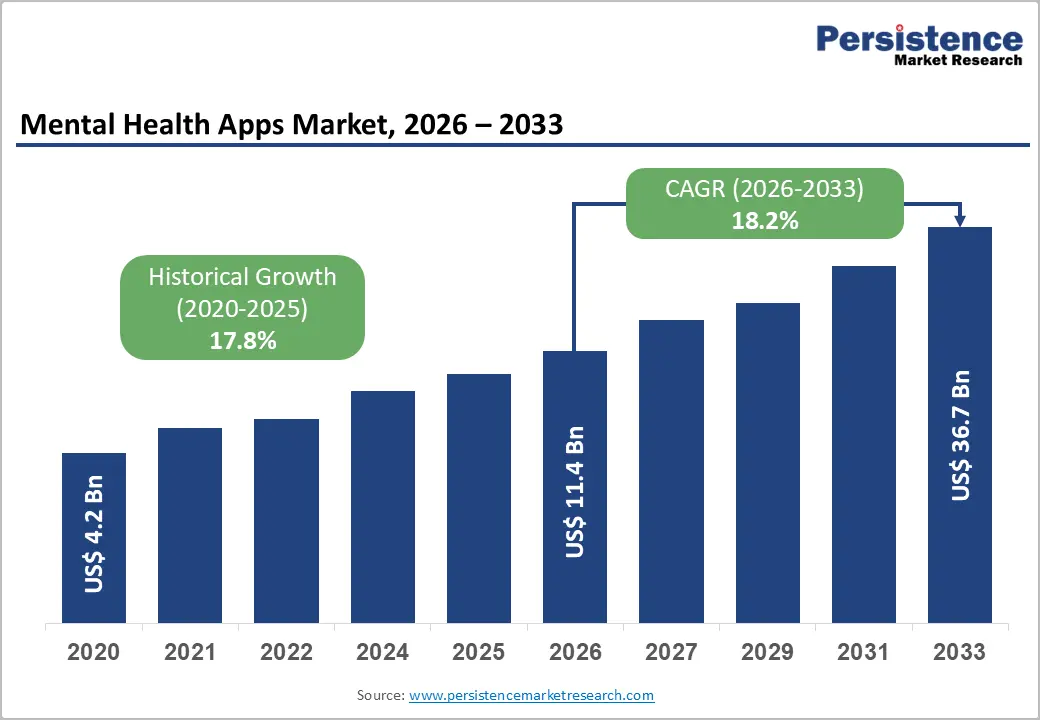

The global mental health apps market size is likely to be valued at US$11.4 billion in 2026 and is estimated to reach US$36.7 billion by 2033, growing at a CAGR of 18.2% during the forecast period 2026 - 2033, driven by rising mental health disorder prevalence, accelerating smartphone adoption, and a global shift toward digital-first healthcare delivery.

Millennials and Generation Z are driving the demand for self-directed, app-based mental wellness tools as workplace stress and burnout intensify. Regulatory frameworks such as the U.S. FDA's SaMD pathway and the EU Medical Device Regulation are expanding reimbursement eligibility for digital therapeutics.

Key Industry Highlights:

- Leading Platform: Android is anticipated to secure around 54% of the mental health apps market share in 2026, driven by dominant installed base concentration across emerging and mid-tier smartphone markets.

- Fastest-growing Platform: iOS is projected as the fastest-growing platform segment, supported by premium user concentration in high-income markets and Apple Health ecosystem integration advantages.

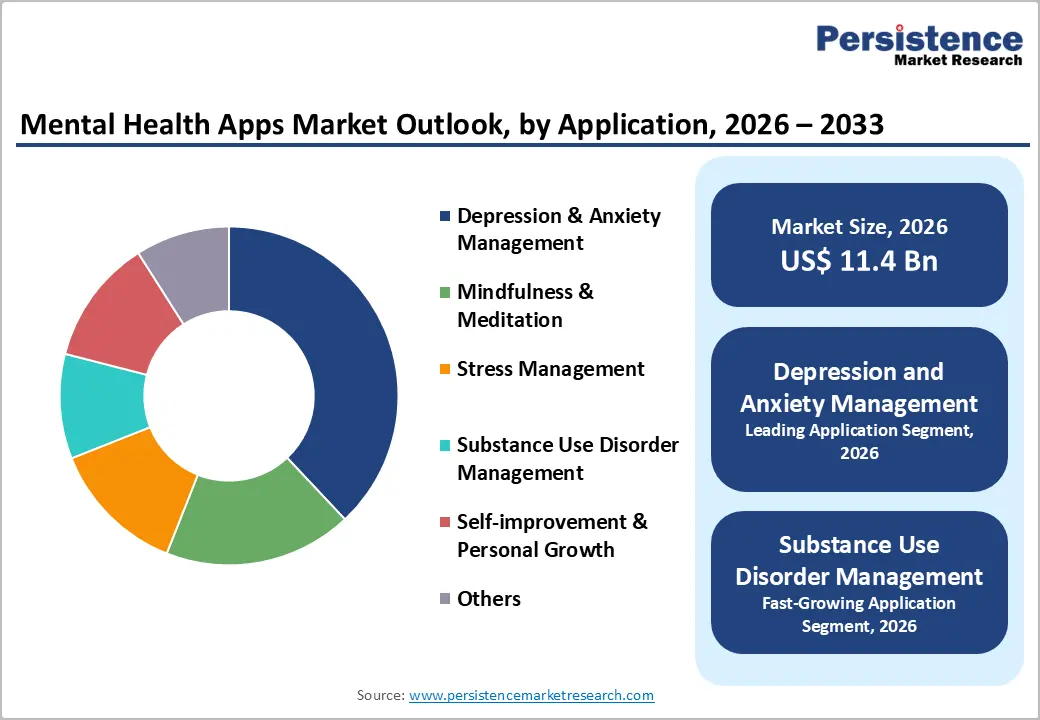

- Leading Application: Depression and anxiety management is estimated to hold roughly 38% of market share in 2026, due to the highest global clinical prevalence and the widest availability of digitally deliverable evidence-based treatment modalities.

- Fastest-growing Application: Substance use disorder management is forecast to record the fastest growth, driven by U.S. opioid crisis response funding and rising payer acceptance of app-based relapse prevention protocols.

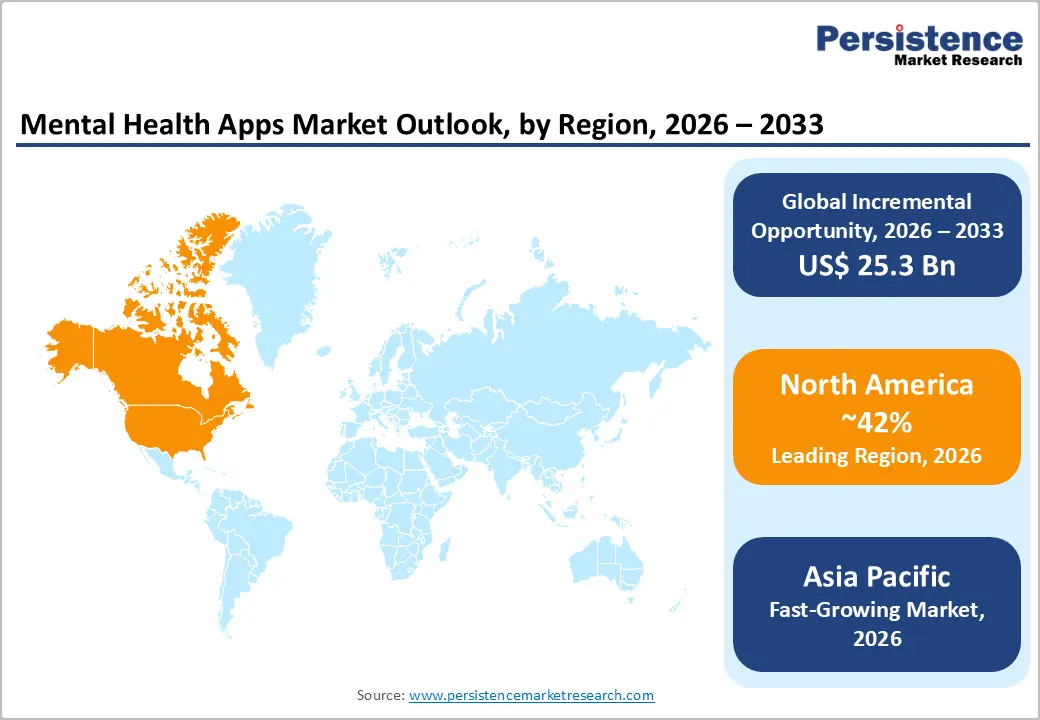

- Regional Leadership: North America is expected to capture approximately 42% of the mental health apps market share in 2026, while Europe is forecast to record the fastest growth due to government-mandated digital health reimbursement framework expansion.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players including Calm, Headspace Health, BetterHelp, Talkspace, and Wysa leveraging clinical validation, enterprise health plan partnerships, and AI personalization to maintain competitive positioning.

DRO Analysis

Driver - Surging Global Burden of Mental Health Disorders

The World Health Organization (WHO) estimates that one in seven people globally lives with a mental disorder. Depression and anxiety account for the highest case volumes. Lost productivity from mental illness costs the global economy over US$1 trillion annually, compelling governments and employers to fund scalable digital intervention tools.

The U.S. Substance Abuse and Mental Health Services Administration reported in 2025 that 59.3 million American adults experienced mental illness in 2022. This demand-supply gap is accelerating the adoption of app-based cognitive behavioral therapy and mood tracking tools. Digital platforms directly address the chronic shortage of licensed practitioners, converting a structural supply constraint into sustained market demand.

Restraint - Data Privacy Risks and Cybersecurity Vulnerabilities

Mental health applications manage highly sensitive behavioral and emotional data, creating elevated cybersecurity exposure for platform operators. Weak encryption frameworks, fragmented compliance standards, and inconsistent user consent mechanisms are increasing operational risks. Security breaches can reduce consumer trust, resulting in higher compliance spending and increasing pressure on operating margins for small and mid-sized developers.

Cross-border data transfer limitations and regional privacy regulations are complicating global scalability strategies for app providers. Frequent software upgrades and security auditing requirements are increasing infrastructure expenditure. Healthcare organizations are also delaying integration agreements with smaller application developers due to concerns regarding long-term data governance stability.

Opportunity - Integration of Generative Artificial Intelligence and Predictive Machine Learning Models

The deployment of large language models and real-world biometric analysis provides an opportunity to deliver real-time, responsive therapeutic interventions. Traditional applications rely on rigid, pre-programmed decision trees that fail to adapt to complex human emotional changes. Integrating advanced natural language understanding enables software platforms to conduct sophisticated, contextual text and voice conversations, mimicking clinical therapeutic interactions.

Predictive machine learning models can process passive smartphone telemetry, including sleep patterns, typing speed, and vocal inflection modifications, to detect early signs of clinical regression. This proactive diagnostic capability allows the application to initiate immediate, tailored behavioral exercises before an individual experiences an acute crisis. By transitioning software functionality from passive tracking to autonomous, predictive intervention, developers can unlock highly scalable enterprise contract opportunities with corporate health sponsors.

Category-wise Analysis

Platform Insights

Android is anticipated to secure around 54% of the mental health apps market share in 2026, reflecting its dominant installed base across price-sensitive emerging markets. Wysa has prioritized Android-first deployment to reach high-volume users across South and Southeast Asia. Superior data volumes from this scale accelerate AI model training and drive compounding personalization benefits that reinforce long-term platform retention.

iOS is expected to be the fastest-growing segment, propelled by its concentration of high-income, insurance-covered users across North America and Western Europe. Calm leads App Store revenue, illustrating the monetization premium of the iOS demographic. HealthKit interoperability enables deeper biometric-informed personalization than competing platforms, strengthening the value proposition for premium-tier subscribers.

Application Insights

Depression and anxiety management applications are poised to dominate with a forecast market share of over 38% in 2026, powered by the highest global prevalence of these conditions and the proven digital deliverability of cognitive behavioral therapy. BetterHelp's structured Cognitive Behavioral Therapy (CBT) integration demonstrates the clinical credibility that secures institutional endorsement. Advanced validation in this category is broadening payer reimbursement eligibility and expanding the addressable market beyond self-pay users.

Substance use disorder management is estimated to be the fastest-growing segment, fueled by opioid crisis funding under the U.S. SUPPORT Act and rising acceptance of app-based relapse prevention. Workit Health combines FDA-authorized digital therapeutics with telehealth prescribing to reduce patient drop-off. Measurable cost savings relative to inpatient rehospitalization are compelling payers to accelerate platform adoption across health system networks.

Subscription Model Insights

Paid subscription is likely to be the leading segment with a projected 61% of the mental health apps market share in 2026 due to growing employer and insurer willingness to fund clinically developed platforms with demonstrated outcomes. Headspace Health's health plan contracts confirm that institutional payer acceptance is expanding.

Free apps are anticipated to be the fastest-growing segment, fueled by surging user base expansion in emerging markets where zero-cost access drives initial adoption. Wysa's freemium model in India converts a portion of its free base into paid coaching tiers. Large free user cohorts generate proprietary behavioral datasets that improve AI performance and enable future monetization through licensing and institutional data partnerships.

Regional Insights

North America Mental Health Apps Market Trends

North America is expected to lead with an estimated 42% of the mental health apps market share in 2026, supported by mature digital healthcare infrastructure, extensive corporate wellness spending, and favorable regulatory frameworks. High consumer awareness regarding psychological well-being, accelerating app adoption across diverse demographic groups, drives the regional market.

U.S. Mental Health Apps Market Insights

The U.S. market growth stems from the widespread implementation of automated digital therapeutics reimbursement frameworks and extensive employee benefit programs. Projected deployment of artificial intelligence-driven triaging tools across corporate healthcare plans aims to reduce employer insurance liabilities. Commercial entities, including Teladoc Health, Inc. and Talkspace, are continuously expanding their domestic software capabilities to capture institutional contracts.

Canada Mental Health Apps Market Insights

Canada is likely to see steady market expansion due to public health initiatives focusing on digital mental health integration across provincial healthcare delivery frameworks. Forecast public funding allocations aim to increase remote counseling accessibility for rural populations via validated mobile applications. Canadian mental health organizations are actively collaborating with private software developers to establish standardized clinical benchmarks for mobile interventions.

Europe Mental Health Apps Market Trends

Europe exhibits robust market growth driven by centralized government initiatives to validate and integrate digital health applications into national health insurance registers. European consumers demand high levels of data security, forcing developers to construct applications with strict adherence to regional privacy mandates. Strategic alignment between local clinical research institutions and mobile software developers accelerates the commercialization of certified digital therapeutics.

Germany Mental Health Apps Market Insights

Germany is projected to record substantial growth due to the established Digital Healthcare Act framework, which allows physicians to prescribe certified digital health applications directly to patients. This systemic reimbursable structure eliminates financial barriers for users, guaranteeing predictable revenue streams for approved software developers. German market entrants are likely to focus heavily on securing clinical validation to fulfill the rigorous requirements of the national digital health register.

U.K. Mental Health Apps Market Insights

The U.K. market evolution is expected to be influenced by the ongoing digital transformation strategies executed within the National Health Service. The government response to community mental health reviews in 2026 emphasized the creation of a digital front door through the NHS App, facilitating direct consumer access to National Institute for Health and Care Excellence-approved digital therapeutics. This integration is forecast to drive massive user enrollment and long-term application engagement across the country.

Asia Pacific Mental Health Apps Market Trends

Asia Pacific is forecast to be the fastest-growing market for mental health apps, stimulated by rising smartphone ubiquity, expanding urban populations, and a structural reduction in societal stigmas surrounding mental health care. The vast population base across developing nations creates a massive addressable market for scalable, low-cost digital wellness solutions.

China Mental Health Apps Market Insights

China is expected to register rapid software adoption driven by massive mobile consumer populations and increasing levels of urban work-related stress. The projected integration of mental health screening modules into large-scale, multi-functional domestic mobile applications will allow developers to access hundreds of millions of users instantly. Local tech enterprises are forecast to expand investments in natural language processing to deliver culturally tailored emotional support tools.

India Mental Health Apps Market Insights

The market in India is likely to witness exponential growth due to the critical shortage of traditional psychiatric professionals and the expanding digital literacy among youth cohorts. A favorable government focus on expanding tele-mental health networks provides a strong foundation for mobile application deployment across tier-2 and tier-3 urban centers. Domestic startups are expected to introduce multi-lingual, voice-activated mindfulness applications to address diverse linguistic populations effectively.

Competitive Landscape

The global mental health apps market is moderately fragmented, with well-capitalized incumbents and clinical AI ventures competing across consumer, enterprise, and health system channels. Calm, Headspace Health, BetterHelp, Talkspace, and Wysa have established differentiated positioning through clinical validation, employer contracts, and proprietary AI development, forming a tiered competitive structure.

Consolidation pressure is intensifying as leading platforms acquire clinical validation assets, localization capabilities, and condition-specific tools. Mid-tier platforms compete through specialized condition depth in areas such as substance use disorder and eating disorder recovery. Early-stage entrants differentiate primarily on AI novelty and user experience design quality.

Key Industry Developments:

- In October 2025, the Ministry of Health and Family Welfare launched enhanced Tele-MANAS app features, including multilingual access, chatbot integration, and emergency mental health support modules, reinforcing the expansion of digital behavioral healthcare accessibility across India.

- In October 2025, Australian startup GM5 launched its beta mental health app in Hyderabad with emotional wellness and early intervention features, reinforcing digital mental healthcare accessibility across emerging urban populations.

Companies Covered in Mental Health Apps Market

- Calm

- Headspace Health

- BetterHelp

- Talkspace

- Wysa

- Woebot Health

- Happify Health

- SilverCloud Health

- Spring Health

- Lyra Health

- Ginger

- MindDoc

- Sanvello Health

- Noom

- Pear Therapeutics

Frequently Asked Questions

The mental health apps market is projected to reach US$11.4 billion in 2026.

Rising prevalence of anxiety, depression, and workplace stress, alongside expanding smartphone adoption and telehealth integration, is driving growth in the mental health apps market.

The mental health apps market is poised to witness a CAGR of 18.2% from 2026 to 2033.

Integration of artificial intelligence, expansion of employer wellness programs, and growing insurance coverage for digital therapy platforms are creating key growth opportunities in the mental health apps market.

Some of the key market players include Calm, Headspace Health, BetterHelp, Talkspace, and Wysa.