- Medical Devices

- Dental CAD/CAM Market

Dental CAD/CAM Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Dental CAD/CAM Market by Product (In-lab Systems and In-office Systems), by Component (Hardware and Software), by End User (Dental clinics, Hospitals, and Academic and Research Institutions), and Regional Analysis from 2026 to 2033

Dental CAD/CAM Market Share and Trends Analysis

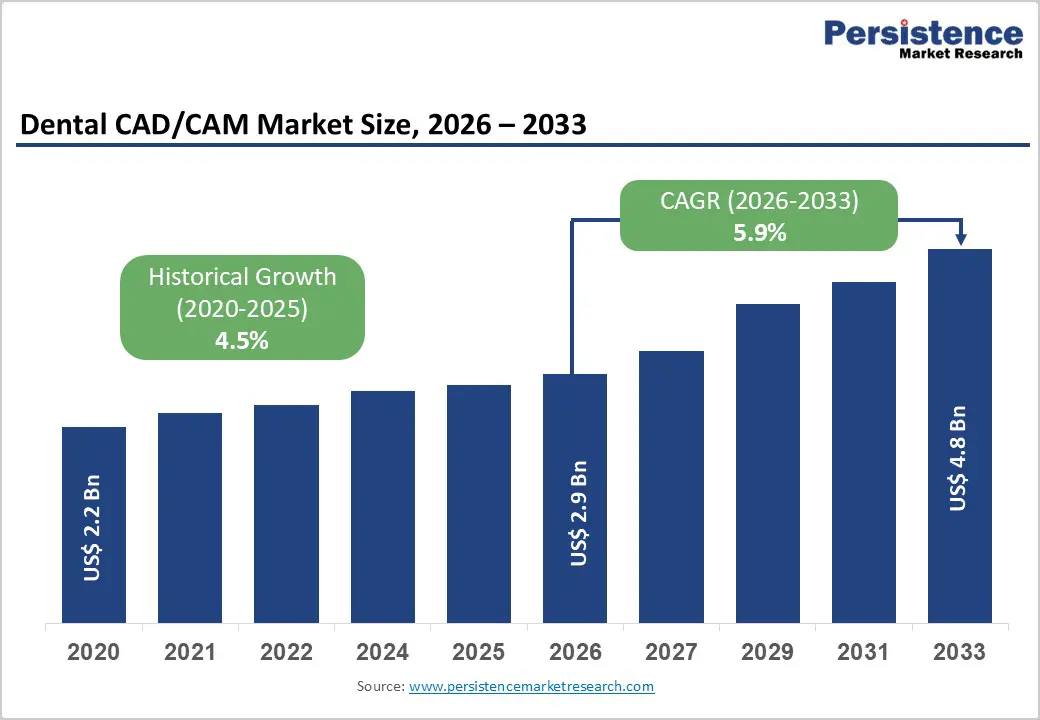

The global dental CAD/CAM market size is likely to be valued at US$ 2.9 billion in 2026 to US$ 4.8 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for dental CAD/CAM (computer-aided design/computer-aided manufacturing) solutions is rising rapidly, driven by increasing volumes of restorative and cosmetic dental procedures, growing adoption of digital dentistry workflows, and rising patient preference for precise, time-efficient treatments. Dental clinics and laboratories are increasingly utilizing CAD/CAM systems to support chairside restorations, implant-supported prosthetics, and high-volume laboratory fabrication. Rising investments in dental infrastructure, expansion of laboratory networks, and growth of organized dental service organizations are accelerating global adoption. Continuous advancements in intraoral scanning, multi-axis milling, dental 3D printing, and AI-enabled CAD software are significantly improving restoration accuracy, workflow efficiency, and turnaround times. Additionally, increasing clinician awareness, expanding training in digital dentistry, and growing clinical evidence supporting CAD/CAM-based restorations are further propelling global market growth.

Key Industry Highlights

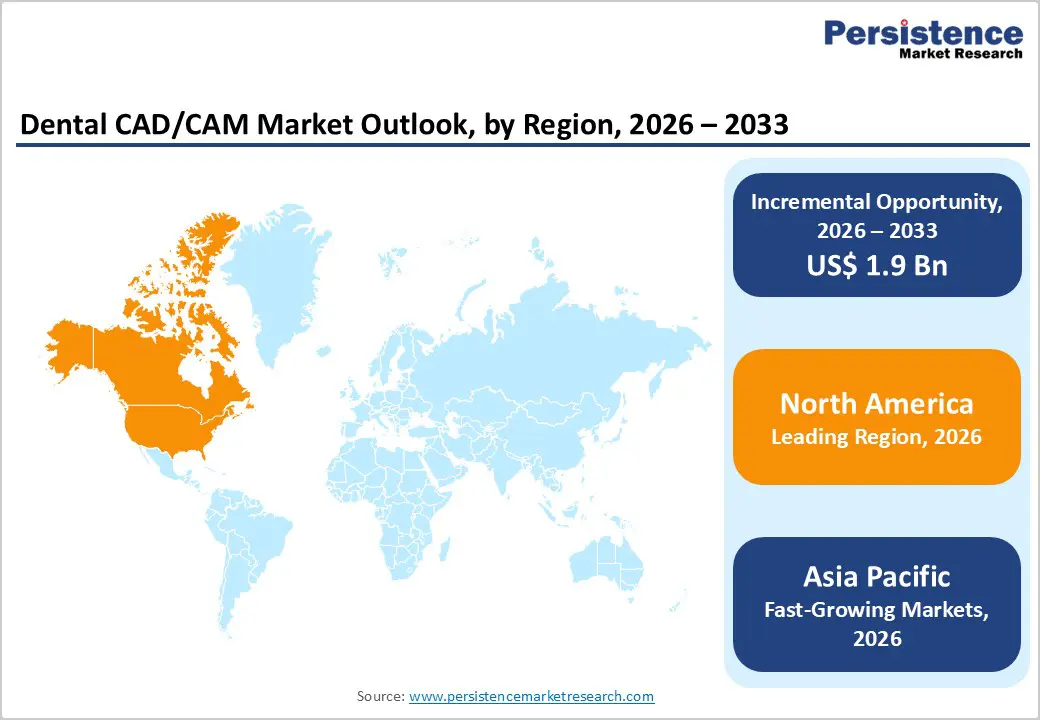

- Leading Region: North America holds the largest share at 47.8%, supported by advanced dental care infrastructure, high adoption of digital dentistry workflows, strong healthcare expenditure, and early access to FDA-approved dental CAD/CAM technologies.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large patient base, rapid modernization of dental clinics and laboratories, increasing medical tourism, and growing investments in digital dental infrastructure.

- Leading Product Segment: In-lab systems dominate the market due to their extensive use in high-volume prosthetic fabrication, multi-unit restorations, and implant workflows, offering high precision and long-term clinical reliability.

- Fastest-Growing Product Segment: In-office systems are growing rapidly as demand for same-day restorations, improved patient experience, and declining equipment costs support broader chairside adoption.

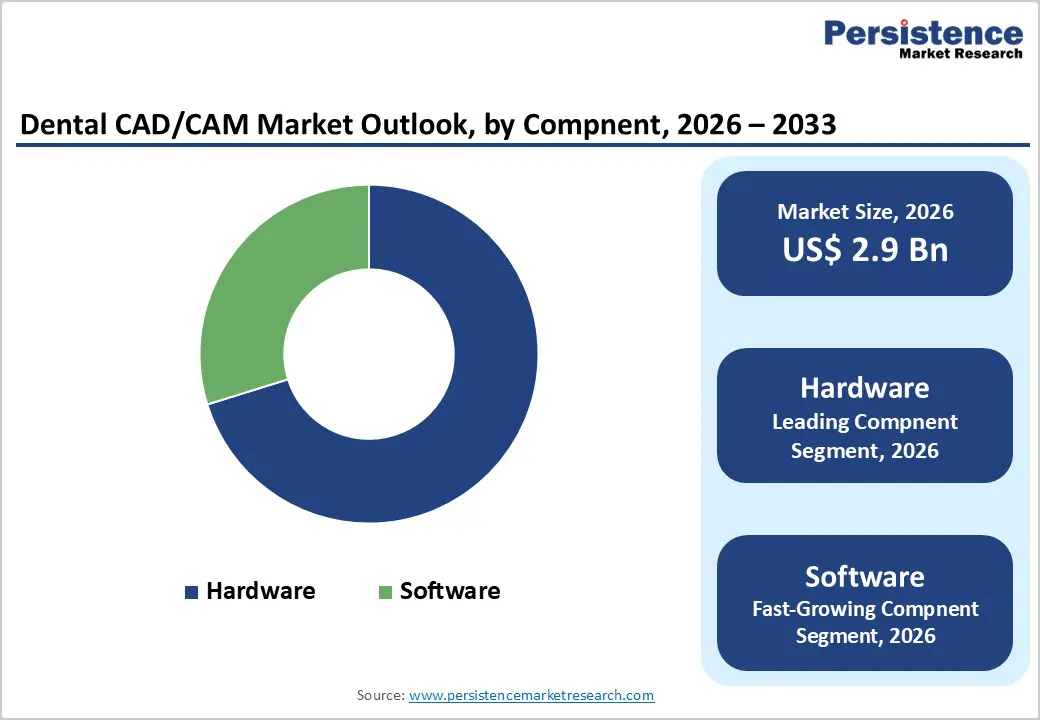

- Leading Component Segment: Hardware remains the top application, driven by high capital investment in milling machines, scanners, and 3D printers, as well as their essential role in daily restorative workflows.

- Fastest-Growing Component Segment: Software is scaling quickly as demand increases for AI-assisted design, cloud-based collaboration, and workflow integration across clinics and laboratories.

| Key Insights | Details |

|---|---|

| Dental CAD/CAM Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Driver - Rising Demand for Aesthetic Dentistry Supported by Rapid Technological Advancements

The global dental CAD/CAM market is experiencing strong growth driven by rising demand for aesthetic and restorative dentistry and ongoing technological advancements in digital manufacturing platforms. Aging populations worldwide are increasingly affected by tooth loss, wear, and restorative needs, driving sustained demand for crowns, bridges, implants, and full-arch rehabilitations. At the same time, growing cosmetic awareness among younger and middle-aged populations is accelerating demand for veneers, aesthetic crowns, and minimally invasive restorative procedures. Patients are increasingly prioritizing precision, natural aesthetics, and reduced chair time, which is encouraging dental professionals to adopt CAD/CAM-enabled workflows.

The advancements in intraoral scanning, multi-axis milling machines, and dental 3D printing technologies are significantly enhancing restoration accuracy, material versatility, and clinical outcomes. High-resolution scanners enable precise digital impressions, while improved milling systems and additive manufacturing technologies support a wider range of materials, including zirconia, lithium disilicate, hybrid ceramics, and advanced resins. Integration of AI-driven design tools and workflow automation further improves consistency, reduces remakes, and shortens turnaround times. Together, these demand-side and technology-driven factors are reinforcing the adoption of dental CAD/CAM systems across clinics and laboratories, supporting sustained market expansion globally.

Restraints - High Cost Barriers and Limited Accessibility Constraining Market Adoption

Despite strong growth potential, the global dental CAD/CAM market faces notable restraints, including cost and accessibility. High initial capital investment required for CAD/CAM hardware, such as intraoral scanners, milling machines, and dental 3D printers, along with associated software licenses, remains a significant barrier for small and independent dental clinics. For many practitioners, especially solo practices, the upfront expenditure can be difficult to justify without guaranteed patient volumes or immediate return on investment. In addition, ongoing costs related to system maintenance, software upgrades, annual licensing fees, and consumables such as milling burs, blocks, and printing resins further increase the total cost of ownership over time.

Moreover, these financial challenges are compounded in price-sensitive and rural markets, where lower treatment volumes, limited reimbursement, and constrained patient spending reduce the feasibility of adopting advanced digital dentistry solutions. Inadequate infrastructure, including unreliable power supply, limited technical support, and a lack of trained personnel, further restricts adoption in underserved regions. As a result, many clinics in emerging economies and rural areas continue to rely on conventional manual workflows or outsource digital fabrication to centralized laboratories. Together, high capital requirements and structural limitations slow market penetration and create uneven adoption patterns across regions, particularly outside major urban and developed healthcare markets.

Opportunity - Emerging Market Expansion and Digital Innovation Creating New Growth Opportunities

The global dental CAD/CAM market presents significant growth opportunities driven by rapid adoption in emerging economies and accelerating digital innovation. Regions such as Asia Pacific and Latin America are witnessing increased uptake of CAD/CAM technologies due to expanding dental care infrastructure, rising disposable incomes, and growing awareness of advanced restorative and cosmetic dental treatments. The proliferation of private dental chains, medical tourism, and investments in modern dental laboratories is enabling wider access to digital dentistry solutions across urban and semi-urban centers. As equipment costs gradually decline and local manufacturing increases, adoption among mid-sized clinics and laboratories is expected to rise substantially.

Furthermore, the growing integration of AI-driven and cloud-based CAD platforms is transforming dental workflows by enabling design automation, remote case collaboration, and centralized planning across multiple locations. These platforms support efficient case sharing between clinics and laboratories, reduce turnaround times, and improve consistency in restoration design. Additionally, increasing use of dental 3D printing for applications such as dental models, surgical guides, and provisional restorations is expanding the functional scope of CAD/CAM systems. Additive manufacturing offers cost-efficient production, faster prototyping, and material flexibility, making it particularly attractive for emerging markets. Together, geographic expansion and digital innovation are creating strong long-term growth opportunities for the dental CAD/CAM market.

Category-wise Analysis

By Product, In-lab Systems Dominate Globally Owing to Proven Accuracy and High-Volume Prosthetic Fabrication

The in-lab systems segment is projected to dominate the global dental CAD/CAM market in 2026, accounting for 45.7% of revenue. This dominance is driven by the critical role of dental laboratories in fabricating crowns, bridges, implant restorations, and full-arch prosthetics with high precision and consistency. In-lab CAD/CAM systems support multi-unit restorations, advanced material processing such as zirconia and metal frameworks, and high-throughput production workflows. Their widespread adoption across independent and centralized dental laboratories, combined with proven accuracy, material versatility, and compatibility with industrial milling and printing platforms, continues to reinforce their leading position globally.

By Component, Hardware Dominates Globally Owing to Capital-Intensive Equipment and High Utilization Rates

The hardware segment is projected to dominate the global dental CAD/CAM market in 2026, accounting for 70.2% of revenue. This is attributed to the high capital costs and the essential role of core equipment, such as milling machines, intraoral scanners, laboratory scanners, and dental 3D printers. Dental laboratories and clinics rely heavily on these systems for routine restorative, implant, and prosthetic workflows. Continuous equipment upgrades, growing adoption of multi-axis milling machines, and expanding use of 3D printing for models and surgical guides contribute to sustained demand. High utilization rates and long replacement cycles further support the hardware segment’s strong market position.

By End User, Dental Clinics Dominate Globally Due to High Procedure Volumes and Chairside Adoption

The dental clinics segment is projected to dominate the global dental CAD/CAM market in 2026, capturing a 44.6% revenue share. Dental clinics are the primary point of care for restorative and cosmetic dental procedures, and the increasing adoption of chairside CAD/CAM systems enables same-day crowns and restorations. High patient throughput, growing preference for minimally invasive and time-efficient treatments, and expanding dental service organizations (DSOs) support strong demand from clinics. Improved affordability of intraoral scanners and compact milling units further accelerates adoption, reinforcing dental clinics as the leading end-user segment globally.

Regional Insights

North America Dental CAD/CAM Market Trends

North America is expected to maintain global dominance in the dental CAD/CAM market, with a market share of 46.5%, supported by advanced dental care infrastructure, high adoption of digital dentistry, and a strong presence of leading CAD/CAM manufacturers. The U.S. leads the region due to widespread use of chairside systems, high penetration of dental laboratories equipped with advanced milling technologies, and strong investment in cosmetic and implant dentistry. Routine use of digital impressions, rapid turnaround expectations, and continued product approvals support sustained adoption.

The region also benefits from favorable reimbursement dynamics for dental procedures, high clinician acceptance of digital workflows, and growing integration of cloud-based CAD platforms. Investments in practice modernization, automation of laboratory operations, and expansion of group dental practices further reinforce North America’s long-term leadership in the global dental CAD/CAM market.

Europe Dental CAD/CAM Market Trends

Europe demonstrates steady and mature adoption of dental CAD/CAM technologies, supported by well-established dental laboratory networks, standardized clinical practices, and strong regulatory oversight across key markets such as Germany, the U.K., France, Italy, Switzerland, and the Nordic countries. High demand for precision restorations, aesthetic dentistry, and implant-supported prosthetics drives consistent utilization of CAD/CAM systems. The region shows strong penetration of laboratory milling machines and increasing adoption of intraoral scanners in clinics.

Europe’s emphasis on quality assurance, clinician training, and digital workflow integration supports continued technology upgrades. Growing focus on cost efficiency, workflow optimization, and cross-border dental laboratory services further contributes to stable market expansion across the region.

Asia Pacific Dental CAD/CAM Market Trends

Asia Pacific is projected to be the fastest-growing region in the dental CAD/CAM market, with a CAGR of 8.0%, driven by expanding dental care infrastructure, rising awareness of oral health, and increasing adoption of digital dentistry solutions. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing rapid uptake of CAD/CAM systems across dental clinics and laboratories. Availability of cost-effective scanners, milling machines, and locally manufactured CAD/CAM solutions is improving accessibility, particularly in urban and mid-sized practices.

Government support for healthcare modernization, the growth of private dental chains, and rising medical tourism are accelerating market adoption. Increasing demand for aesthetic dentistry, implant treatments, and same-day restorations continues to support strong growth momentum, positioning the Asia Pacific as a key expansion region for global dental CAD/CAM manufacturers.

Competitive Landscape

The global dental CAD/CAM market is moderately to highly competitive, with prominent players such as 3Shape A/S, Align Technology, Inc., Amann Girrbach AG, DATRON AG, and Dental Wings Inc. These companies leverage comprehensive digital dentistry portfolios, advanced CAD software, high-precision milling and scanning systems, and well-established global distribution networks to strengthen their presence across dental clinics, laboratories, and hospital-based dental departments.

Manufacturers are increasingly focused on enhancing chairside and laboratory CAD/CAM workflows through AI-enabled design software, cloud-based platforms, and integration of 3D printing technologies. Strategic priorities include continuous product innovation, expansion into emerging markets, partnerships with dental service organizations and laboratories, and regulatory compliance to support broader adoption of digital dentistry solutions and sustain market growth.

Key Industry Developments:

- In December 2025, Align Technology, Inc. announced a series of new product innovations for iTero™ Digital Solutions, enhancing its intraoral scanners and integrated software ecosystem to deliver advanced, multi-modal oral health assessments and improve chairside experiences supporting Invisalign treatment conversion.

- In August 2025, Align Technology, Inc. announced the commercial availability in Thailand of the Invisalign System with mandibular advancement featuring integrated occlusal blocks, designed to address Class II skeletal and dental correction by advancing the mandible while aligning teeth, improving treatment predictability and efficiency.

- In March 2025, Alliedstar launched the Sensa intraoral scanner at IDS 2025, marking its first major product release since being acquired by Straumann and introducing a new brand, naming strategy, and upgraded scanner design.

Companies Covered in Dental CAD/CAM Market

- 3Shape A/S

- Align Technology, Inc.

- Amann Girrbach AG

- DATRON AG

- Dental Wings Inc.

- Dentsply Sirona

- Envista

- Hexagon AB

- imes-icore GmbH

- Ivoclar Vivadent

- Jensen Dental

- Planmeca Oy

- Roland DGA Corporation

- Institut Straumann AG

- Others

Frequently Asked Questions

The global dental CAD/CAM market is projected to be valued at US$ 2.9 Bn in 2026.

Rising demand for aesthetic and restorative dentistry, increasing adoption of digital workflows in clinics and laboratories, growing geriatric population, and efficiency gains from chairside and lab-based CAD/CAM systems are driving the global dental CAD/CAM market.

The global dental CAD/CAM market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Expansion of chairside CAD/CAM in emerging markets, rapid adoption of dental 3D printing and cloud-based software, integration of AI-driven design tools, and growing dental chains and hospital-based dentistry present key opportunities in the global dental CAD/CAM market.

3Shape A/S, Align Technology, Inc., Amann Girrbach AG, DATRON AG, Dental Wings Inc., are some of the key players in the dental CAD/CAM market.