- Medical Devices

- Dental Imaging Equipment Market

Dental Imaging Equipment Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Dental Imaging Equipment Market by Drugs (Intraoral Dental Imaging Equipment, Extraoral Dental Imaging Equipment, Cone-Beam Computed Tomography (CBCT) Imaging), by Dimension, by End-user, and Regional Analysis from 2026 - 2033

Dental Imaging Equipment Market Share and Trends Analysis

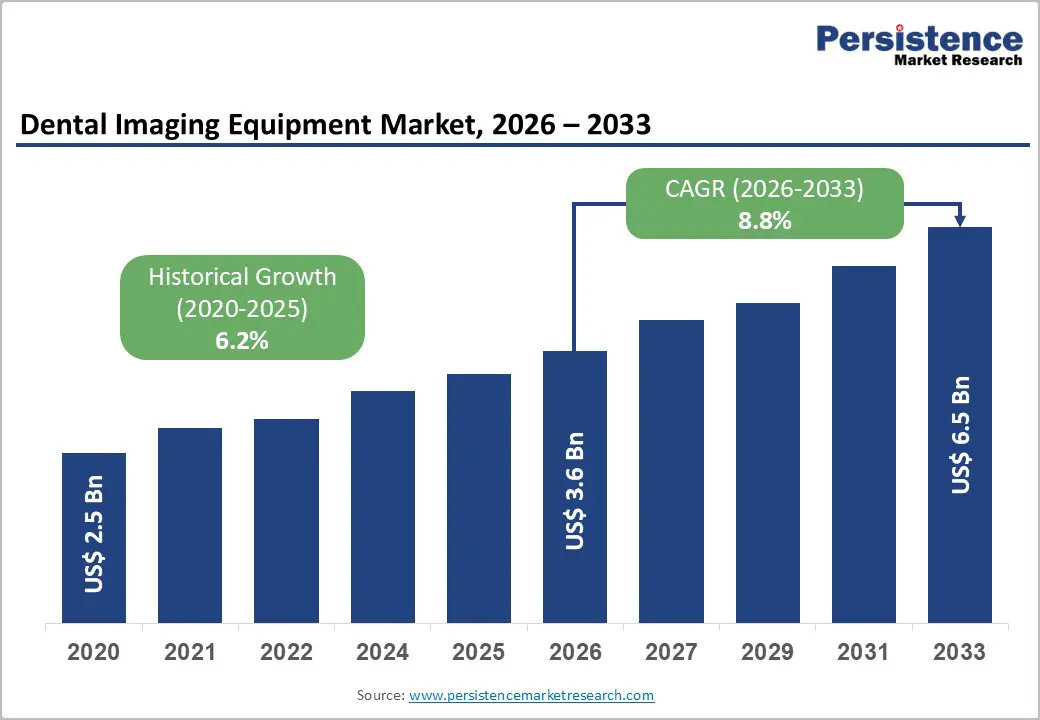

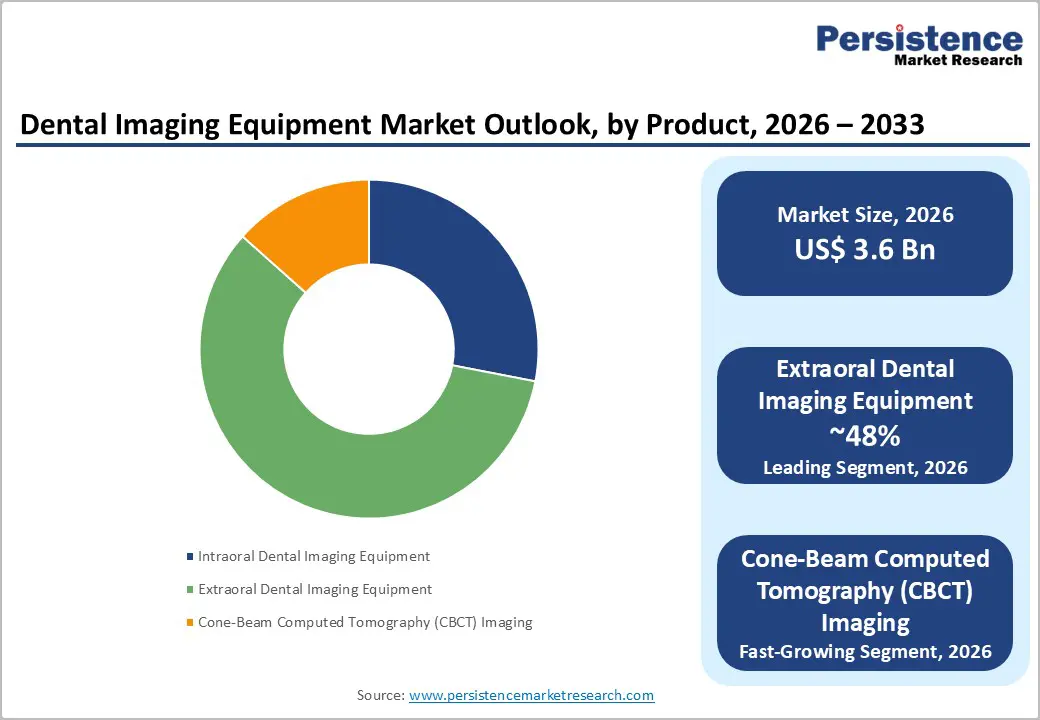

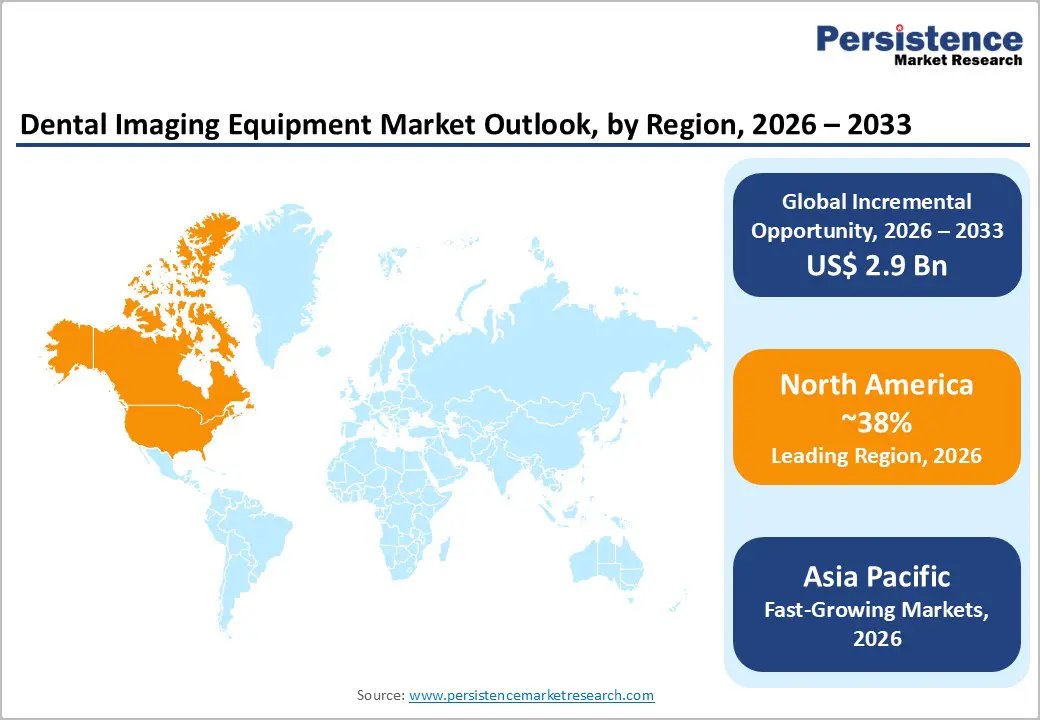

The global dental imaging equipment market size is likely to be valued at US$3.6 billion in 2026 to US$6.5 billion by 2033 growing at a CAGR of 7.5% during the forecast period from 2026 to 2033. Driven by rising dental disorders and increasing demand for early and accurate diagnosis, rapid technological advancements in digital dentistry drives growth.

Widespread adoption of digital X-ray systems, cone-beam computed tomography (CBCT), and intraoral scanners is improving diagnostic precision while reducing radiation exposure. Growing awareness of preventive oral healthcare, expansion of dental clinics, and increasing cosmetic dentistry procedures further support market expansion. Additionally, integration of artificial intelligence and cloud-based imaging platforms is enhancing workflow efficiency and clinical decision-making, positioning dental imaging equipment as a critical component of modern dental care delivery systems.

Key Industry Highlights:

- Increasing prevalence of dental caries, periodontal diseases, and oral infections worldwide is driving demand for advanced imaging systems to support early diagnosis and effective treatment planning.

- Dental practices are rapidly transitioning from analog to digital imaging technologies due to superior image quality, faster processing, reduced radiation exposure, and improved data storage capabilities.

- Advancements in low-dose imaging technologies and stricter regulatory standards are encouraging the adoption of safer dental imaging systems among practitioners and healthcare providers.

- Leading Product: Extraoral dental imaging equipment accounts for the highest market share because it supports a wider range of high-value applications, including orthodontics, implant planning, maxillofacial surgery, and full-jaw assessment.

- Leading Region: North America leads the dental imaging equipment market due to its well-established dental care infrastructure, high penetration of digital and CBCT imaging technologies, and strong presence of leading manufacturers.

| Key Insights | Details |

|---|---|

|

Dental Imaging Equipment Market Size (2026E) |

US$3.6 Bn |

|

Market Value Forecast (2033F) |

US$6.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.2% |

Market Dynamics

Driver - Growing Focus on Cosmetic Dentistry Fuels Demand for Imaging Equipment

The growing focus on cosmetic dentistry is significantly driving the demand for advanced imaging equipment. Cosmetic procedures such as teeth whitening, veneers, and orthodontic treatments are becoming increasingly popular as more people seek to enhance their smiles. This trend has led to a surge in the need for precise and high-quality dental imaging solutions.

The integration of advanced technologies like intraoral cameras and digital radiography has revolutionized cosmetic dentistry. These tools provide detailed images that aid in accurate diagnosis and treatment planning, ensuring optimal results for patients. The ability to visualize the end result before starting treatment has also increased patient satisfaction and confidence in cosmetic procedures.

Enhanced imaging capabilities allow for comprehensive assessments of dental and facial structures, facilitating accurate diagnosis and treatment planning. With high-resolution imaging, practitioners can visualize the intricate details of patients’ oral anatomy, leading to better treatment outcomes and minimized complications.

A notable manufacturer in this field is Dentsply Sirona, a leading provider of dental imaging solutions. Their products, such as the Orthophos SL 3D, offer high-resolution images and advanced features that cater to the needs of cosmetic dentistry, enhancing both diagnostic accuracy and treatment outcomes.

Restraints - Radiation Exposure Concerns Among Patients

Radiation exposure remains a significant concern in the dental imaging equipment market, despite continuous technological advancements aimed at reducing dose levels. Many patients remain apprehensive about the cumulative effects of repeated exposure to X-rays, particularly when imaging is required multiple times for diagnosis, treatment planning, and follow-up. This concern is more pronounced among vulnerable groups such as children, pregnant women, and elderly patients, where long-term health risks are perceived to be higher. In pediatric and preventive dentistry, parents often question the necessity of imaging, leading dentists to limit usage or seek alternative diagnostic approaches.

Although modern digital radiography and cone-beam computed tomography (CBCT) systems offer substantially lower radiation doses compared to conventional imaging, awareness of these improvements remains limited among patients. Media coverage, online health information, and increasing public sensitivity toward radiation safety further amplify fears, even when exposure levels fall within clinically acceptable limits. Additionally, stricter radiation protection guidelines and the “as low as reasonably achievable” (ALARA) principle encourage clinicians to minimize imaging frequency, indirectly reducing equipment utilization. These factors collectively slow adoption rates, particularly for high-dose imaging modalities, and restrain market growth by influencing both patient acceptance and clinical decision-making in routine dental care.

Opportunity - Advanced Technologies and Emphasis on Regenerative Medicine

3D printing integration for treatment planning represents a high-value opportunity within the dental imaging equipment market, driven by the growing need for precision, personalization, and efficiency in dental procedures. The seamless workflow from cone-beam computed tomography (CBCT) imaging to 3D printing enables dentists to convert high-resolution anatomical data into accurate physical models, surgical guides, and custom prosthetics. This integration significantly enhances treatment planning for dental implants, orthodontics, maxillofacial surgery, and restorative dentistry by allowing clinicians to visualize patient-specific anatomy in advance.

3D-printed surgical guides improve implant placement accuracy, reduce chair time, and minimize procedural risks, while orthodontic models support customized aligners and braces with predictable outcomes. Additionally, prosthetic components such as crowns, bridges, and dentures can be precisely designed using CBCT-based imaging data, improving fit and patient comfort. The adoption of digital workflows also reduces manual errors, accelerates turnaround times, and enhances communication between dentists, laboratories, and patients. As dental clinics increasingly invest in chairside CAD/CAM systems and in-house 3D printers, demand for imaging equipment compatible with advanced digital manufacturing workflows is rising. This convergence of CBCT imaging and 3D printing is reshaping modern dentistry by enabling more accurate, efficient, and patient-centric care delivery.

Category-wise Analysis

By Product, Extraoral Dental Imaging Equipment Segment is leading in the Market

Extraoral dental imaging equipment holds the highest market share due to its versatility, high clinical value, and broader application compared with intraoral and CBCT-only systems. Extraoral devices, which include panoramic and cephalometric X-rays along with integrated 3D CBCT systems, are widely used for comprehensive diagnostics, treatment planning, and surgical procedures in dentistry. Their ability to capture full-arch, jaw, and craniofacial images makes them indispensable for implantology, orthodontics, oral surgery, and complex restorative treatments.

Although intraoral imaging systems are more commonly used in routine check-ups, they have limited scope, primarily focusing on single-tooth or small-area imaging, and generate lower revenue per unit. CBCT imaging alone is highly specialized, offering three-dimensional visualization, but its adoption is comparatively limited due to high costs and training requirements. In contrast, extraoral systems serve multiple clinical needs within one platform, combining panoramic, cephalometric, and sometimes CBCT imaging, which increases their utility and overall market revenue.

Additionally, the rise of multi-specialty dental clinics and hospitals has further strengthened demand for extraoral imaging equipment, solidifying its position as the leading segment in the dental imaging market.

By End-user, Independent Dental Clinics Segment Leads the Market

Independent dental clinics account for the highest share in the dental imaging equipment market due to their central role in delivering routine, preventive, and cosmetic dental care. Unlike hospitals or ambulatory surgical centers, which primarily handle specialized or surgical cases, independent clinics perform a high volume of daily dental procedures, including check-ups, restorations, orthodontics, and aesthetic treatments. These clinics increasingly rely on advanced intraoral and extraoral imaging systems to ensure accurate diagnosis, treatment planning, and patient education.

The growing awareness of oral health, rising disposable incomes, and increasing demand for cosmetic dentistry have driven more patients to seek services at private dental clinics, further boosting equipment adoption.

Additionally, independent clinics are more flexible in investing in digital imaging technologies, such as digital X-rays, CBCT, and intraoral scanners, to enhance efficiency and improve patient outcomes. While hospitals and forensic laboratories use imaging systems, their frequency of routine dental imaging is limited compared with private practices. Consequently, independent dental clinics dominate equipment usage and revenue contribution, making them the leading end-user segment in the global dental imaging market.

Regional Insights

North America Dental Imaging Equipment Trends

North America stands out as the leading region in the dental imaging equipment market, driven by advanced healthcare infrastructure, high adoption of cutting-edge technologies, and robust dental service networks. With approximately 38–40% of the global market share, North America’s dominance is anchored by the United States, where strong reimbursement frameworks, widespread insurance coverage, and high dental care expenditure encourage frequent upgrades to digital imaging systems such as CBCT, intraoral scanners, and AI-enhanced radiography solutions. U.S. dental practices and large dental service organizations have rapidly transitioned from analog to digital imaging to improve diagnostic accuracy, streamline workflows, and enhance treatment planning, particularly for implants, orthodontics, and preventive care.

High patient awareness of oral health and cosmetic dental trends further intensifies demand for advanced imaging equipment. Additionally, the presence of major industry players and continuous innovation in imaging platforms reinforces the region’s leadership position. Canada also contributes to expanding coverage and public oral health initiatives that promote adoption. These combined factors ensure North America and especially the U.S. remain at the forefront of dental imaging market growth and technological adoption.

Asia Pacific Dental Imaging Equipment Market Trends

Asia Pacific is emerging as a high-growth region in the dental imaging equipment market, driven by rapid urbanization, rising disposable incomes, and increasing awareness of oral health. Countries such as China, India, Japan, and South Korea are witnessing significant expansion of private dental clinics and multi-specialty dental hospitals, fueling demand for advanced imaging solutions like digital X-rays, CBCT, and intraoral scanners. Growing emphasis on preventive and cosmetic dentistry, coupled with rising dental tourism in nations like Thailand and India, further boosts equipment adoption. Government initiatives to improve oral healthcare infrastructure, coupled with expanding insurance coverage in select countries, support market growth.

Additionally, technological advancements such as AI-enabled imaging software and portable, cost-effective devices are facilitating adoption among small and mid-sized clinics. With increasing investment in modern dental technologies and growing patient demand for precise diagnostics and treatment planning, Asia Pacific is poised to become the fastest-growing market for dental imaging equipment in the coming years.

Competitive Landscape

The dental imaging equipment market is highly competitive, characterized by several global and regional players vying for technological leadership and market share. Key companies focus on innovation, introducing advanced digital imaging systems such as CBCT, AI-powered software, and portable intraoral devices to differentiate offerings. Strategic partnerships, mergers, and acquisitions are common to expand product portfolios and geographic reach. Competitive pricing, strong distribution networks, and after-sales services further influence buyer decisions.

Key Industry Developments:

- In October 2025, Planmeca partnered with The Aspen Group to deliver advanced imaging solutions to Aspen Dental clinics across the United States. This collaboration aimed to enhance clinical outcomes and elevate the patient experience nationwide.

- In March 2025, Align Technology, Inc. announced the addition of restorative capabilities to its next-generation iTero Lumina™ intraoral scanner (without iTero Near Infra-Red Imaging [NIRI] technology) and the new iTero Lumina™ Pro dental imaging system (with iTero NIRI technology). These enhancements enabled efficient restorative and multidisciplinary ortho-restorative workflows and supported the diagnosis of interproximal caries above the gingiva, helping general practice dentists achieve higher practice efficiency and growth while delivering exceptional clinical outcomes.

Companies Covered in Dental Imaging Equipment Market

- Envista Holdings Corporation

- Dentsply Sirona

- Danaher Corporation

- Planmeca Oy

- VATECH Co., Ltd.

- Carestream Dental, LLC

- Acteon Group

- Owandy Radiology

- DÜRR DENTAL SE

- Midmark Corporation

- 3Shape

- J. Morita Corporation

- Others

Frequently Asked Questions

The global dental imaging equipment market is projected to be valued at US$3.6 Bn in 2026.

Increasing cases of dental caries, periodontal diseases, and oral health issues drive demand for accurate diagnostics.

The global market is poised to witness a CAGR of 8.8% between 2026 and 2033.

Growing demand for mobile and small-footprint imaging systems in rural and small clinics.