- Industrial Machinery

- Tissue Paper Converting Machine Market

Tissue Paper Converting Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Tissue Paper Converting Machine Market by Machine Type (Toilet Roll Converting Lines, Kitchen Roll Converting Lines, Others), Operation Mode (Automatic, Semi-Automatic, Others), End-user, and Regional Analysis for 2026 - 2033

Tissue Paper Converting Machine Market Size and Trends Analysis

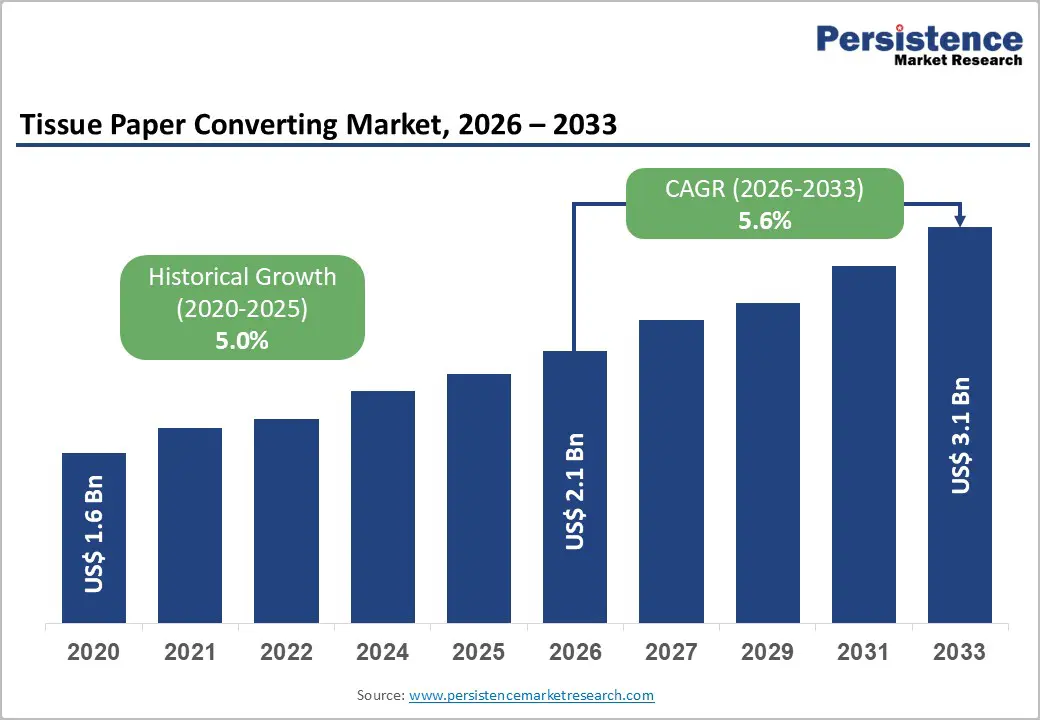

The global tissue paper converting machine market size is likely to be valued at US$2.1 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, driven by sustained demand for packaged household and away-from-home (AFH) tissue products, ongoing replacement cycles in mature economies, and accelerated capacity additions across the Asia Pacific region, the market continues to expand.

Advancements in automation, energy efficiency, and Industry 4.0-enabled retrofits are elevating average selling prices while enhancing aftermarket revenue potential. Although cost pressures from steel and electronic components during 2022-2024 temporarily compressed margins, they also catalyzed investment in higher-efficiency, higher-throughput converting lines that reduce lifecycle operating costs.

Key Industry Highlights

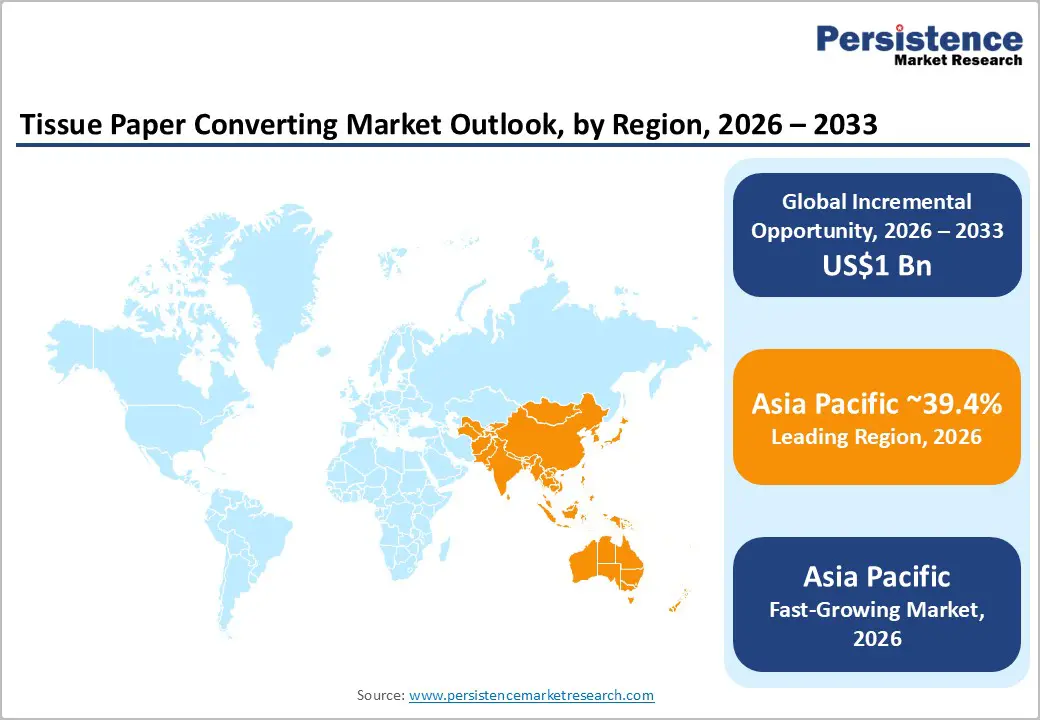

- Leading Region: Asia Pacific is projected to hold 39.4% market share, driven by rapid urbanization, expanding retail infrastructure, and high-volume tissue production in China, India, Japan, and Southeast Asia.

- Fastest-Growing Region: Asia Pacific is driven by emerging converters, adoption of modular automation, and strong demand for AFH and household tissue; regional CAGR outpaces North America and Europe.

- Investment Plans: Focused on automation upgrades, energy-efficient and digital-enabled machines, and regional manufacturing footprints; OEMs also emphasize retrofit services and modular platforms to capture recurring revenue.

- Dominant Machine Type: Toilet roll converting lines are anticipated to hold 44.6% of market share, supported by consistent replacement demand, standardized packaging formats, and high utilization in household tissue production.

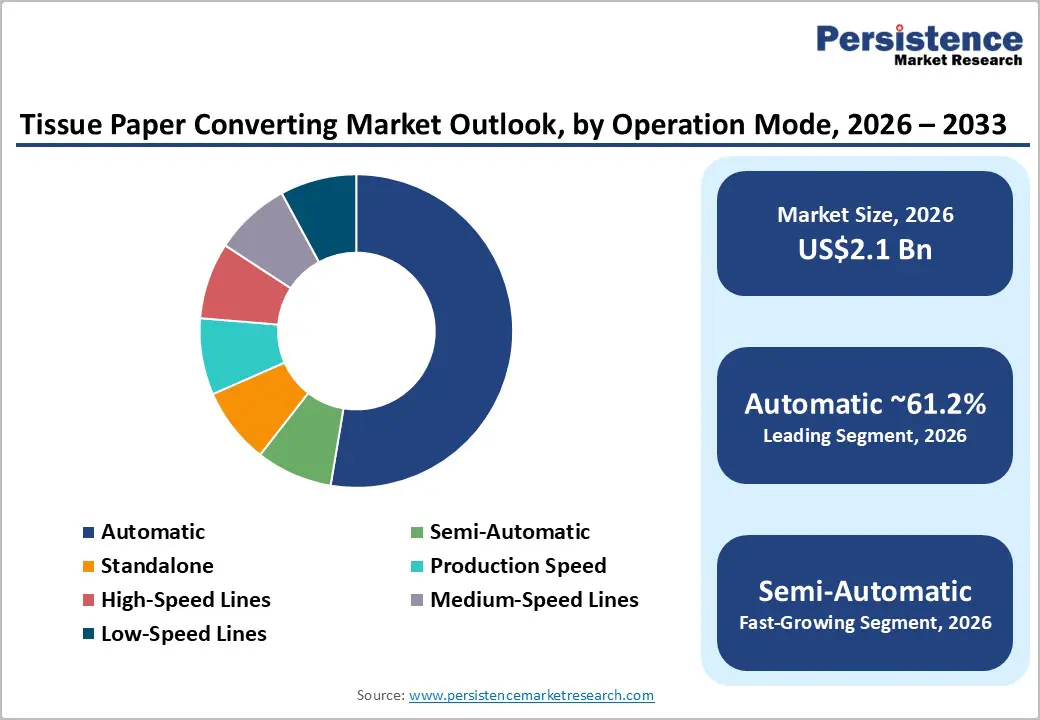

- Leading Operation Mode: Automatic systems are estimated to hold 61.2% market share, adoption driven by labor efficiency, throughput gains, reduced waste, and aftermarket revenue opportunities from digital services and preventive maintenance programs.

| Key Insights | Details |

|---|---|

| Tissue Paper Converting Machine Market Size (2026E) | US$2.1 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Per-Capita Tissue Consumption and Urbanization

Global tissue consumption continues to rise in line with urbanization, hygiene awareness, and improving retail penetration. While developed markets exhibit stable replacement demand, emerging economies are experiencing structural increases in per-capita tissue usage as disposable incomes rise and modern retail formats expand. For converting machine manufacturers, this trend directly translates into higher order volumes for new production lines and incremental capacity expansions.

Household tissue remains the dominant end-use category, sustaining demand for toilet roll and kitchen roll converting lines. Converters are increasingly upgrading machine specifications, including higher speeds and automated changeovers, to improve margins on premium and differentiated tissue formats. Equipment procurement typically occurs 6-18 months ahead of production ramp-ups, providing reasonable demand visibility for suppliers.

Automation and Digitalization across Tissue Converting Operations

Tissue converters are rapidly transitioning from semi-automatic and low-speed equipment to fully automatic, integrated converting and packaging systems. Automation reduces labor dependency, minimizes material waste, and shortens changeover times, which improves overall equipment effectiveness.

Technologies such as automated log change systems, in-line quality inspection, and plant-level performance dashboards significantly reduce downtime and stabilize output quality. These advancements raise the intrinsic value of converting machines and expand service-based revenue streams. Suppliers that integrate software, remote diagnostics, and predictive maintenance into their equipment offerings are increasingly capturing recurring revenue through service contracts, reflecting a broader shift toward data-driven operating models.

Sustainability and Energy-Efficiency Regulations

Stricter energy-efficiency standards and packaging waste regulations in Europe and parts of Asia are reshaping capital investment priorities. Tissue producers are replacing older machines with energy-efficient models and adopting converting systems compatible with recyclable or bio-based packaging materials.

Equipment with lower power consumption and reduced material waste is increasingly favored in procurement decisions and may qualify for financing or incentive support in certain jurisdictions. As a result, converters are choosing modernization and efficiency upgrades over low-cost replacements, increasing average order values and strengthening demand for technologically advanced converting solutions.

Barrier Analysis - High Capital Intensity and Extended Sales Cycles

High-performance tissue converting lines, particularly fully integrated automatic systems with high-speed rewinders and packaging units, require multi-million-dollar capital investments. These projects involve long procurement timelines, complex installation requirements, and extended commissioning periods.

Smaller and mid-sized converters often delay purchases or opt for used equipment, creating a bifurcated market between high-end new machinery and lower-cost alternatives. Capital intensity also increases exposure to interest-rate fluctuations and working-capital constraints. Even modest increases in borrowing costs can materially slow order intake for large, turnkey converting projects, particularly in price-sensitive regions.

Volatility in Components and Electronics Supply Chains

Modern converting machines rely heavily on specialized drives, servo motors, sensors, and advanced control systems. Supply chain disruptions and price volatility in steel, semiconductors, and electronic components have increased manufacturing lead times and project risk. OEMs face higher input costs and longer delivery schedules, while customers may postpone or renegotiate investments due to uncertainty.

These dynamics compress near-term revenues and complicate production planning. Effective mitigation requires diversified supplier bases, higher component inventories, and balanced contractual structures that allocate risk between suppliers and buyers.

Opportunity Analysis - Retrofit and Modernization Services

A large global installed base of legacy converting machines presents a significant opportunity for retrofit and modernization solutions. Typical upgrades include energy-efficient drives, PLC and control system replacements, automatic loading and unloading modules, in-line quality monitoring, and modular packaging add-ons. Retrofit projects generally offer higher margins and shorter sales cycles than new machine installations.

If approximately 20-30% of the installed base undergoes modernization within a three- to five-year period, retrofit revenues could represent 15-25% of the annual new-machine market value. Suppliers that bundle engineering services, spare parts, and digital subscriptions can convert episodic capital spending into stable, recurring revenue streams.

Expansion in the Asia Pacific and AFH Segments

Asia Pacific represents both the largest and fastest-growing regional market, accounting for approximately 39.4% of global demand. Growth is driven by China, India, Japan, and Southeast Asia, where household tissue consumption and AFH demand from hospitality, healthcare, and institutional facilities are expanding rapidly.

Suppliers that adopt localized manufacturing, regional service networks, and flexible financing models are well positioned to capture share in cost-sensitive markets. Incremental gains of even 1-2% in annual equipment penetration can deliver meaningful revenue growth given the region’s scale. Localizing spare parts and service operations further reduces the total cost of ownership for converters and accelerates adoption.

Category-wise Analysis

Machine Type Insights

Toilet roll converting lines are expected to account for approximately 44.6% of total market revenue, serving as the structural backbone of the global tissue paper converting machine market. Their dominance is underpinned by high-volume, non-discretionary demand, standardized product dimensions, and strong replacement cycles among established tissue converters. Large consumer goods companies and private-label manufacturers rely heavily on high-speed rewinders, embossers, and automated case packers optimized for common roll diameters and multi-pack retail formats.

In mature markets such as the U.S., Germany, and Japan, converters increasingly prioritize equipment uptime exceeding 95%, waste reduction below 3%, and rapid changeovers to manage SKU proliferation driven by promotional activity and retailer differentiation. Leading OEMs such as PCMC, Fabio Perini, and Baosuo have introduced next-generation toilet roll lines featuring predictive maintenance, servo-driven modules, and integrated quality inspection. These upgrades sustain premium average selling prices (ASPs) while also expanding high-margin aftermarket revenues from spare parts, consumables, and long-term service agreements.

Kitchen roll converting lines represent the fastest-growing machine category, supported by structural premiumization trends across both household and away-from-home (AFH) segments. Unlike standard toilet tissue, kitchen rolls increasingly feature higher ply counts, larger sheet sizes, textured embossing, and enhanced absorbency, enabling brand owners to command higher per-roll pricing. This pricing uplift incentivizes converters to invest in specialized converting lines capable of handling larger log diameters, heavier basis weights, and complex embossing patterns.

Growth is particularly strong in Western Europe and the Asia Pacific, where kitchen towels are gaining traction in food service, healthcare, and light industrial cleaning applications. In response, equipment suppliers are launching flexible hybrid platforms that allow rapid switching between toilet and kitchen roll formats, improving asset utilization. For example, several mid-sized converters in Italy and Southeast Asia have adopted dual-purpose lines to reduce capital intensity while addressing shifting demand profiles, strengthening the long-term growth outlook for this segment.

Operation Mode Insights

Automatic converting systems are anticipated to maintain a dominant 61.2% market share, reflecting their clear advantages in labor productivity, throughput consistency, and material efficiency. These systems integrate end-to-end processes, including automatic reel handling, high-speed splicing, embossing, log sawing, in-line inspection, and fully automated packaging, significantly reducing manual intervention.

Converters operating in high-cost labor markets such as North America and Western Europe increasingly view full automation as a risk-mitigation strategy against workforce shortages and rising wage pressures. Automatic systems also enable tighter quality tolerances, supporting premium brand positioning and regulatory compliance related to hygiene and product uniformity. From a supplier perspective, this segment delivers recurring revenue streams through digital performance monitoring, predictive maintenance software, and OEM-certified spare parts programs. Leading manufacturers such as Valmet, ANDRITZ, and Korber Tissue continue to enhance automation platforms with data analytics and remote diagnostics, reinforcing customer lock-in and long-term service contracts.

Semi-automatic and standalone converting machines are experiencing accelerated adoption in emerging and cost-sensitive markets, particularly across the Asia Pacific, Latin America, and parts of Eastern Europe. These systems appeal to regional brands, private-label producers, and new market entrants that prioritize lower upfront capital expenditure, operational simplicity, and faster installation timelines.

Semi-automatic machines typically combine manual reel loading with automated rewinding and cutting, offering a balanced trade-off between cost and productivity. Modular system architecture is a key growth enabler, allowing converters to incrementally add automation modules such as auto-packers or vision inspection as volumes scale. Equipment suppliers that offer local assembly, operator training, and flexible financing or leasing models gain a competitive edge in this segment. For example, several Indian and ASEAN-based converters have adopted semi-automatic lines as an entry platform before transitioning to fully automatic systems, positioning this segment as a strategic feeder pipeline for future automation upgrades.

Regional Insights

North America Tissue Paper Converting Machine Market Trends - Automation-Driven Replacement Demand and Brownfield Modernization

North America remains a high-value, technology-intensive market for tissue paper converting machines, supported by a large installed base of equipment and consistently high adoption of automation. Market demand is driven primarily by replacement cycles, brownfield modernization projects, and selective greenfield investments, particularly in private-label and premium household tissue categories.

The U.S. dominates regional capital expenditure, reflecting high per-capita tissue consumption, consolidated retail structures led by Walmart, Costco, and Kroger, and sustained demand from away-from-home (AFH) channels such as healthcare and hospitality. Major tissue producers, including Kimberly-Clark, Procter & Gamble, Georgia-Pacific, and Clearwater Paper, continue to upgrade their converting lines to improve energy efficiency, reduce downtime, and support the rapid SKU changes retailers demand. Recent investments have focused on fully automatic lines with advanced packaging, vision inspection, and digital performance monitoring, enabling consistent quality while mitigating labor shortages. In parallel, private-label growth has driven mid-scale converters to invest in flexible, high-speed systems capable of short production runs.

The regulatory environment plays a material role in shaping investment decisions. OSHA workplace safety standards, stricter state-level emissions controls, and extended producer responsibility (EPR) initiatives related to packaging recyclability are accelerating the retirement of older, less efficient machines. As a result, converters increasingly favor energy-efficient motors, electric drives, and low-waste embossing technologies, improving the total cost of ownership despite higher upfront costs. Financing partnerships, vendor-backed leasing programs, and performance-based service contracts offered by suppliers such as Valmet, Korber Tissue, and PCMC are gaining traction, reducing capital intensity and supporting steady modernization across the region.

Europe Tissue Paper Converting Machine Market Trends - Sustainability-Regulated Upgrades Led by High-Spec Engineering

Europe represents a technologically mature and regulation-driven market, where investment decisions are closely aligned with sustainability compliance and lifecycle efficiency. The region is characterized by strong replacement demand, high engineering standards, and early adoption of digital and energy-saving converting technologies. Germany leads in advanced automation uptake, supported by a robust manufacturing base and strong demand from premium tissue producers, while Italy remains a global hub for tissue converting machinery design and export, hosting leading OEMs such as Fabio Perini, Gambini, Futura, and A.Celli.

Key consumer markets, including France, Spain, and the United Kingdom, continue to invest in line upgrades to meet evolving packaging waste regulations and retailer sustainability mandates. The implementation of the EU Packaging and Packaging Waste Regulation (PPWR) and tightening energy-efficiency benchmarks under the EU Green Deal are pushing converters toward low-energy, recyclable-ready, and digitally optimized converting lines. While these systems carry higher initial costs, they deliver superior lifecycle economics through lower energy consumption, reduced material waste, and enhanced compliance certainty.

Recent years have seen increased supplier consolidation and strategic integration of digital services, reshaping competitive dynamics. European OEMs are embedding remote diagnostics, predictive maintenance, and energy monitoring as standard offerings, strengthening long-term customer relationships and aftermarket revenue streams. For example, several Western European tissue producers have partnered with Italian equipment suppliers to retrofit legacy lines with servo drives and smart control systems rather than pursue full greenfield builds. This trend supports capital discipline while reinforcing Europe’s role as a benchmark market for high-specification tissue converting technology.

Asia Pacific Tissue Paper Converting Machine Market Trends -Capacity Expansion and Rapid Automation across High-Growth Markets

Asia Pacific is projected to account for approximately 39.4% of global market share and represents the fastest-growing regional market, driven by rapid capacity additions, rising hygiene awareness, and expanding retail infrastructure. China remains the largest equipment buyer, supported by large-scale domestic tissue producers and export-oriented manufacturers investing in high-speed, fully automatic converting lines. Leading Chinese tissue groups continue to scale operations to serve both domestic consumption and regional export markets, sustaining strong demand for advanced converting equipment.

India and Southeast Asia are emerging as key growth engines, fueled by urbanization, population growth, modern retail expansion, and government-led sanitation initiatives. Indian tissue producers, many of which are transitioning from semi-organized to organized manufacturing, increasingly adopt semi-automatic and modular converting systems as entry platforms before upgrading to full automation. ASEAN markets such as Vietnam, Indonesia, and Thailand are seeing new investments in mid-speed and high-speed lines to support growing household and AFH demand.

Japan occupies a distinct position within the region, emphasizing high-precision engineering, reliability, and product consistency rather than volume expansion. Japanese converters prioritize advanced quality control, compact line layouts, and long service life, influencing supplier design requirements. Across the Asia Pacific, local manufacturing incentives, subsidized financing, and partnerships between international OEMs and regional service providers are accelerating adoption and shortening payback periods. Investments in electric drives, energy-efficient embossing, and waste-minimization technologies are becoming more common, reinforcing the region’s role as both a volume driver and a rapidly maturing technology market.

Competitive Landscape

The global tissue paper converting machine market exhibits moderate concentration. A limited group of global OEMs dominates high-end, fully automatic systems, while numerous regional and domestic suppliers serve the low- to mid-tier segments. Market share is weighted toward integrated line providers due to higher average selling prices and recurring service revenues. This tiered structure results in distinct competitive dynamics based on project size, technology requirements, and geographic focus.

Recent strategic activity has focused on vertical integration, digital capability expansion, and regional manufacturing investments. Leading suppliers have strengthened end-to-end offerings spanning tissue production, converting, packaging, and digital performance optimization. Investments in regional facilities have reduced delivery times and improved customer support, while advancements in low-emission and electric tissue technologies align supplier portfolios with sustainability mandates.

Key competitive strategies include vertical integration, modular product platforms, and service-centric business models. Market leaders differentiate through global service coverage, localized manufacturing, flexible financing options, and recurring revenue from digital performance solutions and retrofit programs.

Key Industry Developments

- In June 2025, Valmet announced the supply of an IntelliTissue 1600 machine to Fabryka Papieru i Tektury Beskidy in Poland to support low-energy, high-efficiency tissue production, with the line slated to start in 2026.

- In March 2025, Toscotec and Gambini announced a strategic partnership to co-develop integrated high-speed tissue converting lines to improve delivery times and energy efficiency for tissue manufacturers in Europe, the Middle East, and Africa.

Companies Covered in Tissue Paper Converting Machine Market

- Valmet

- PCMC

- Futura

- Toscotec

- A.Celli

- Gambini

- Körber

- Baosuo

- Andritz

- OMET Tissue

- Fabio Perini

- CMPC Technologies

- Papelera del Plata Engineering

- Hobema

- KDF Maschinenbau

- Jori Machinery

- Mitsubishi Heavy Industries

- Kawanoe Zoki

Frequently Asked Questions

The market size is valued at US$2.1 billion in 2026.

By 2033, the tissue paper converting machine market is expected to reach US$3.1 billion.

Key trends include rising automation and digitalization, increased demand for energy-efficient and sustainable converting lines, growth in retrofit and modernization services, and strong equipment demand from Asia Pacific capacity expansions.

Toilet roll converting lines are the leading segment, accounting for approximately 44.6% of total market share, supported by consistent household tissue demand and high replacement rates.

The market is projected to grow at a CAGR of 5.6% between 2026 and 2033.

Major players with strong product portfolios and global presence include Valmet, PCMC, Futura, Toscotec, and A.Celli.