- Medical Devices

- Tissue Level Implant Market

Tissue Level Implant Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Tissue Level Implant Market by Product Type (Titanium, Zirconia, Hybrid), Application (Dental Clinics, Hospitals, Ambulatory Surgical Centers (ASCs)), Modality (Fixed, Removable), and Regional Analysis for 2026-2033

Tissue Level Implant Market Share and Trends Analysis

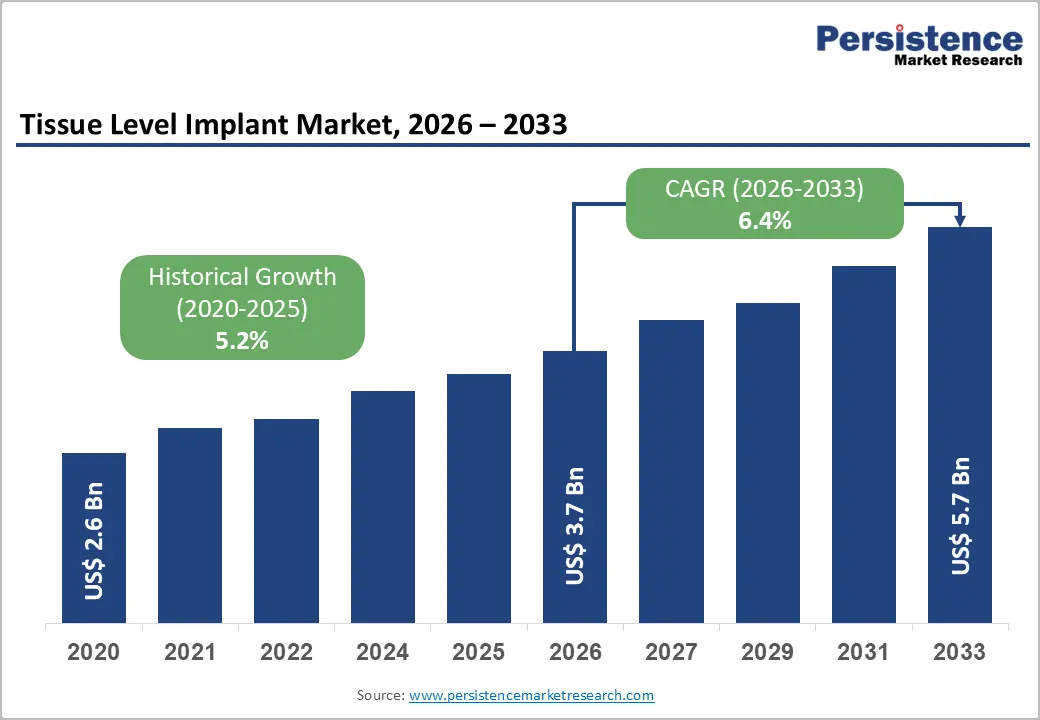

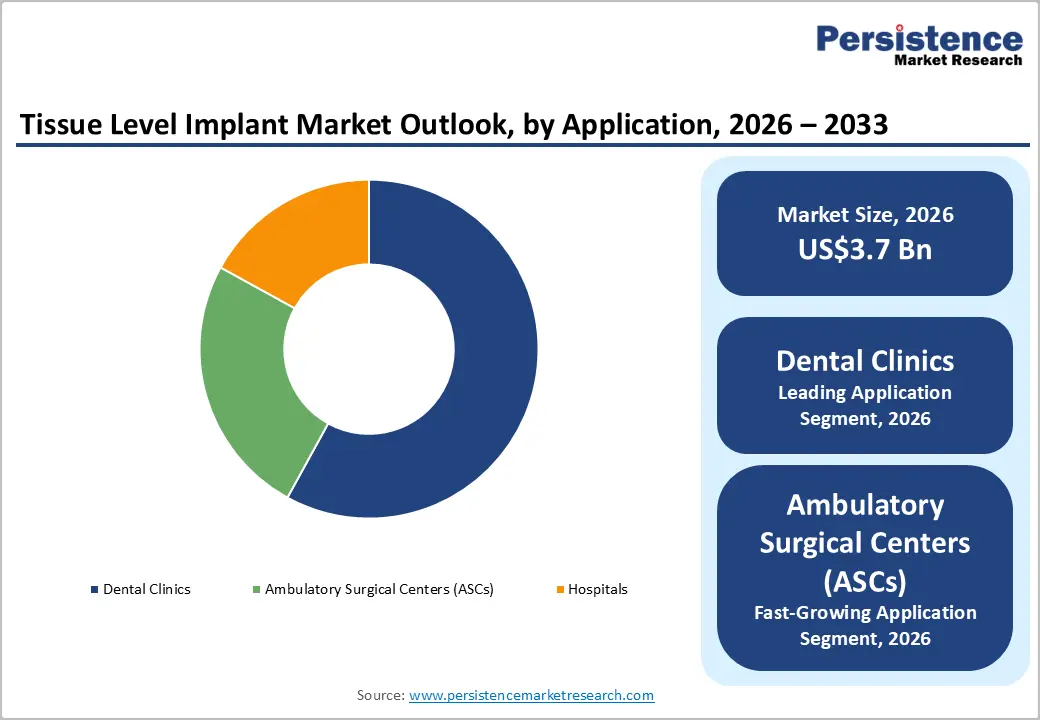

The global tissue level implant market size is likely to be valued at US$ 3.7 billion in 2026, and is projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026−2033. The market is experiencing sustained expansion, driven by the rising global incidence of edentulism, increasing geriatric populations, and widespread adoption of minimally invasive dental surgical techniques. Tissue level implants, which emerge through the gingival tissue and provide a biologically stable transmucosal interface, are increasingly preferred by clinicians for their simplified prosthetic workflow and favorable long-term osseointegration outcomes.

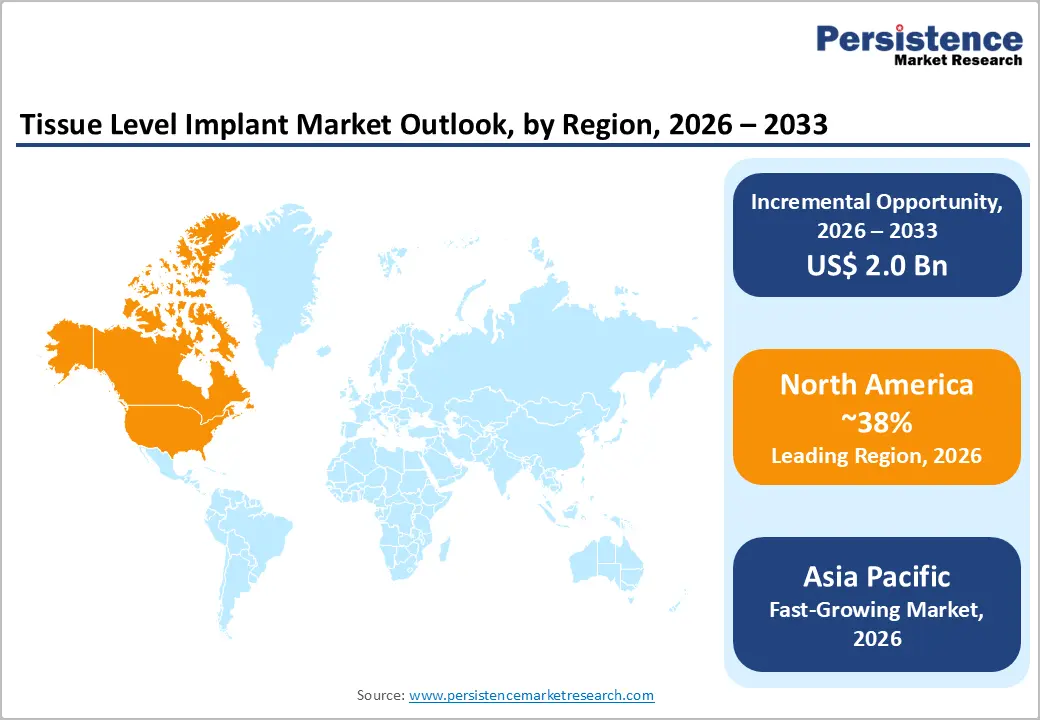

Key growth accelerants include heightened dental tourism in emerging economies, expanding insurance reimbursement coverage in developed markets, and rapid advancements in implant surface modification technologies. North America and Europe collectively account for the majority of global implant procedures, while Asia Pacific is emerging as the fastest growing regional market, fueled by improving healthcare infrastructure, rising disposable incomes, and a growing base of dental professionals trained in implantology.

Key Industry Highlights

- Dominant Region: North America is expected to command about 38% market share in 2026, supported by strong healthcare infrastructure and high dental care utilization.

- Fastest-growing Region: The Asia Pacific market is set to be the fastest-growing during the 2026-2033 forecast period, due to strong growth in private dental clinic networks and government programs.

- Leading & Fastest-growing Product Type: Titanium implants are poised to lead by commanding approximately 58% of total market revenue, whereas zirconia implants are likely to be the fastest-growing segment over the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Dental clinics are expected to capture approximately 75% of market revenue share in 2026, with ambulatory surgical centers (ASCs) growing the fastest through 2033.

| Key Insights | Details |

|---|---|

|

Tissue Level Implant Market Size (2026E) |

US$3.7 Bn |

|

Market Value Forecast (2033F) |

US$5.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

DRO Analysis

Technological Advancements in Implant Surface Engineering

Continuous progress in implant biomaterials and surface engineering is strengthening product differentiation and supporting premium positioning across dental implant systems. Advanced surface treatments such as sandblasted large grit acid etched (SLA), hydrophilic SLActive, and nanostructured titanium are improving early-stage stability and accelerating biological integration. These innovations are enabling clinicians to achieve faster healing responses while maintaining predictable outcomes. Manufacturers are focusing on optimizing surface chemistry and microtopography to enhance bone-to-implant contact and long-term durability. Regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) are continuing to evaluate and approve advanced surface technologies, which is encouraging companies to introduce refined implant solutions and expand their product portfolios.

Digital dentistry is transforming how tissue level implant procedures are being planned and executed. Technologies such as computer aided design and computer aided manufacturing (CAD/CAM), intraoral scanners, and guided surgery software are improving precision and reducing procedural variability. These tools are allowing clinicians to customize prosthetic designs and align implant placement with patient-specific anatomical conditions. Integration between digital workflows and implant systems is also streamlining communication across laboratories and clinics. This shift is increasing treatment efficiency and making advanced implant procedures more accessible to a broader patient base, while supporting consistent clinical outcomes.

Rising Prevalence of Edentulism and Tooth Loss

Tooth loss is continuing to pose a major challenge for public health systems across both developed and emerging regions. The World Health Organization (WHO) estimates global average prevalence of complete tooth loss is almost 7% among people aged 20 years or older. For people aged 60 years or older, a much higher global prevalence of 23% has been estimated. Losing teeth can be psychologically traumatic, socially damaging and functionally limiting. Aging populations are experiencing higher rates of edentulism, which is increasing the demand for long-term restorative solutions. Patients are seeking treatments that are not only functional but also natural in appearance and comfortable in daily use.

This shift in expectations is encouraging dental professionals to adopt more advanced therapeutic approaches. Tissue level implants are addressing this clinical gap by providing stable and durable tooth replacement options. These systems are improving load distribution and supporting healthy soft tissue integration, which is enhancing long-term outcomes. Institutions such as the U.S. Centers for Disease Control and Prevention (CDC) are continuing to highlight the broader health implications of tooth loss, which is reinforcing the importance of effective intervention. Dental practitioners are increasingly recommending implant-based solutions due to their reliability and improved patient satisfaction.

Stringent Regulatory Approval Frameworks

Regulatory diversity across key markets is creating a complex environment for dental implant manufacturers. Companies are navigating different approval frameworks that demand region-specific documentation, testing protocols, and compliance strategies. In the United States, the FDA classifies tissue level implants under moderate risk categories and is requiring premarket notification through the 510(k) pathway. In Europe, the European Union (EU) Medical Device Regulation (MDR 2017/745) enforces stricter clinical validation and post market surveillance requirements. These evolving standards are pushing manufacturers to strengthen clinical data generation and maintain detailed technical files. Regulatory authorities are also increasing scrutiny on product safety, biocompatibility, and long-term performance, which is raising the level of evidence needed before commercialization.

Product development timelines are becoming longer as companies are aligning innovation with regulatory expectations. Research and development teams are investing more resources in clinical trials, risk assessments, and quality assurance processes. Smaller manufacturers are facing greater pressure due to limited financial and operational capacity, which is slowing their ability to introduce new designs. Larger firms are adapting by building dedicated regulatory teams and forming strategic partnerships to manage compliance efficiently. This environment is influencing innovation cycles and encouraging a more structured approach to product development, while ensuring that patient safety and product reliability are consistently maintained.

Risk of Implant Failure and Post-Operative Complications

Implant failure is remaining an important clinical and business concern despite overall improvements in technology and surgical protocols. Certain patient groups are presenting higher risk due to underlying conditions such as uncontrolled diabetes, smoking habits, and insufficient bone support. These factors are affecting healing capacity and are reducing the likelihood of successful osseointegration. Clinicians are therefore placing greater emphasis on patient screening, risk assessment, and personalized treatment planning before proceeding with implantation. Research bodies such as the European Federation of Periodontology (EFP) are continuing to study long term outcomes and complications, which is guiding clinical decision making. This growing awareness is encouraging the adoption of preventive strategies and improved surgical techniques.

Peri implantitis is emerging as a critical complication that is impacting implant longevity and patient satisfaction. This inflammatory condition is damaging the surrounding tissues and is increasing the risk of implant instability or loss. Dental professionals are focusing on early diagnosis, maintenance protocols, and patient education to control disease progression. Manufacturers are developing surface modifications and antimicrobial coatings to reduce bacterial accumulation. Financial implications associated with corrective procedures are also influencing treatment decisions and referral patterns. These challenges are shaping a more cautious and evidence driven approach, while the industry is continuing to strengthen reliability and long-term performance standards.

Digital Dentistry Integration and Guided Implant Surgery

The integration of tissue level implant systems with digital dentistry platforms is creating a strong commercial pathway for manufacturers and service providers. Companies are developing connected ecosystems that combine implant hardware with software driven planning and execution tools. Technologies such as CAD/CAM, guided surgery kits, and digital impression systems are enabling seamless coordination across clinical and laboratory workflows. This integration is improving precision and reducing manual errors during implant placement and restoration. Firms that are investing in proprietary digital interfaces are strengthening brand differentiation and building long term customer loyalty.

Advanced digital tools are transforming how clinicians are planning and performing implant procedures. Real time bone mapping and artificial intelligence assisted planning systems are enhancing diagnostic accuracy and supporting data driven decisions. 3D-printed surgical guides are allowing precise implant positioning and are minimizing intraoperative deviations. These innovations are reducing chair time and improving procedural consistency for dental professionals. Group practices and institutional providers are adopting these solutions to standardize treatment protocols and increase operational efficiency. This shift is expanding access to advanced care while supporting scalable growth for implant manufacturers and dental service organizations.

Increasing Adoption of Digital Dentistry and Advanced Manufacturing Techniques

Digital technologies are reshaping how dental implants are being designed and manufactured across modern clinical settings. Tools such as CAD/CAM, 3D printing, and advanced digital imaging systems are enabling highly accurate implant modeling and production. These solutions are allowing clinicians and technicians to create patient specific designs that closely match anatomical requirements. Improved visualization and planning capabilities are reducing uncertainty during procedures and are enhancing treatment predictability. Laboratories are also streamlining production workflows by using automated systems that ensure consistency and reduce turnaround time. This transformation is strengthening collaboration between dental clinics and fabrication centers, which is supporting more reliable and efficient care delivery.

Clinical adoption of tissue level implants is increasing as digital workflows are simplifying complex procedures and improving overall outcomes. Practitioners are using integrated platforms to plan, simulate, and execute implant placement with greater confidence. Customized prosthetic components are fitting more precisely, which is improving comfort and long-term stability for patients. Manufacturers are focusing on digital integration and advanced production methods to differentiate their offerings and meet evolving clinical expectations. Continuous investment in innovation is positioning these companies to respond effectively to changing market demands while expanding their competitive advantage.

Category-wise Analysis

Product Type Insights

Titanium implants are anticipated to command approximately 58% of the tissue level implant market revenue share in 2026, owing to their proven clinical reliability and long-term performance. These implants are offering excellent biocompatibility and are supporting strong osseointegration, which is making them a preferred choice among dental professionals. Their mechanical strength is allowing consistent performance under varying load conditions, which is improving treatment predictability. Widespread clinical acceptance and extensive research backing are reinforcing their market leadership. Manufacturers are continuing to enhance surface treatments and design features to improve outcomes. Established supply chains and familiarity among clinicians are further strengthening their position, ensuring sustained demand across diverse patient groups.

Zirconia implants are likely to be the fastest-growing segment during the 2026-2033 forecast period. Increasing demand for metal-free and aesthetically superior solutions. These implants are providing a tooth-like appearance, which is making them suitable for patients seeking natural-looking restorations. Their favourable tissue response is supporting improved soft tissue integration and reducing visible discoloration near the gum line. Growing awareness around material sensitivity and holistic dental care is encouraging adoption among specific patient segments. Manufacturers are investing in material innovation and design optimization to enhance durability and expand clinical indications, which is accelerating growth and strengthening their presence in modern implantology.

Application Insights

Dental clinics are likely to dominate in 2026, capturing an estimated 75% of the tissue level implant market share in 2026. These settings are offering specialized expertise, focused treatment environments, and access to advanced dental technologies, which are improving procedural efficiency. Most implant placements are being performed in clinics due to their cost effectiveness and shorter patient turnaround time. Practitioners are increasingly adopting digital tools such as intraoral scanners and guided surgery systems to enhance precision. Strong patient trust, ease of scheduling, and personalized care approaches are further strengthening the dominance of dental clinics in routine and advanced implant treatments.

Ambulatory surgical centers are expected to be the fastest-growing segment over the 2026-2033 forecast period, as they are providing streamlined and outpatient-based surgical care. These facilities are enabling efficient implant procedures with reduced hospital dependency and shorter recovery timelines. Patients are preferring these centers due to convenience, controlled costs, and quicker discharge processes. Surgeons are utilizing advanced surgical infrastructure and standardized protocols to ensure consistent outcomes. Increasing collaboration between dental specialists and surgical teams is expanding the scope of procedures performed in these centers, which is accelerating their adoption and positioning them as an important growth avenue in implant dentistry.

Regional Insights

North America Tissue Level Implant Market Trends

North America is set to command a significant portion of the tissue level implant market share at approximately 38% in 2026, due to strong healthcare infrastructure and high dental care utilization. The United States is driving regional performance through well-established reimbursement systems and widespread access to advanced dental treatments. Organizations such as the American Dental Association (ADA) and its Health Policy Institute are continuously highlighting trends in dental spending and treatment adoption. Dental service organizations (DSOs) are expanding multi-location networks and are standardizing implant procedures to improve efficiency and procurement strategies. Clinics are increasingly adopting advanced implant systems to meet rising patient expectations for durability and aesthetics, which is strengthening overall market demand.

The United States Census Bureau is projecting sustained growth in the aging population, which is increasing the need for restorative dental solutions. Younger patient groups are also seeking cosmetic enhancements, which is encouraging early adoption of implant procedures. Regulatory support from the FDA is enabling faster evaluation of new implant technologies, which is helping manufacturers introduce improved products. Leading companies such as Straumann, Nobel Biocare, and Dentsply Sirona are continuing to strengthen their presence through innovation and strategic partnerships. Canada is also progressing with broader oral health coverage through the Canadian Dental Care Plan, which will be improving accessibility and supporting regional growth.

Europe Tissue Level Implant Market Trends

Europe is holding a strong position in the global tissue level implant market, supported by advanced healthcare systems and a well-established dental ecosystem. Germany is leading regional demand due to structured reimbursement under statutory health insurance and a highly trained clinical workforce. The United Kingdom is gradually shifting toward privately funded treatments as access limitations within the National Health Service (NHS) are influencing patient choices. Countries such as France and Spain are experiencing increased procedure volumes due to rising awareness and the expansion of dental tourism. Professional associations and regulatory bodies are continuing to promote quality standards, which is strengthening clinical outcomes and supporting consistent adoption across diverse patient groups.

Regulatory transformation under the MDR is reshaping the competitive environment for implant manufacturers. Companies are investing heavily in compliance processes, clinical validation, and documentation to meet stricter approval requirements. Smaller firms are facing operational challenges, which is leading to product rationalization and market exits. Larger organizations are strengthening their position by leveraging resources to maintain compliance and expand certified product portfolios. Innovation hubs in countries such as Germany, Switzerland, and Sweden are continuing to advance research and development, which is supporting technological progress and long-term regional growth.

Asia Pacific Tissue Level Implant Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for tissue level implants between 2026 and 2033. China is leading regional demand through strong growth in private dental clinic networks and government programs such as Healthy China 2030, which are promoting oral health adoption. A growing middle class is seeking advanced dental solutions, which is increasing demand for implant procedures. Japan is maintaining a stable market with high clinical standards and premium treatment positioning. Countries such as India, Thailand, Vietnam, Indonesia, and South Korea are experiencing strong momentum as access to dental care is improving and awareness of aesthetic treatments is increasing.

Regional manufacturing capabilities are strengthening market accessibility and competitive positioning. Companies based in South Korea and China are producing cost effective implant systems, which are expanding treatment availability across price sensitive populations. Dental tourism is attracting international patients to destinations such as Thailand and Vietnam, where quality care is being offered at competitive pricing. Global manufacturers are forming joint ventures and partnerships to establish local production and distribution networks. Regulatory alignment through the ASEAN Medical Device Directive (AMDD) is simplifying approval processes across multiple countries. This evolving landscape is encouraging innovation, increasing market penetration, and supporting sustained regional growth.

Competitive Landscape

The global tissue level implant market structure is moderately consolidated, dominated by leading players such as Straumann Group, Nobel Biocare, Dentsply Sirona, Zimmer Biomet, and Osstem Implant. These players collectively capture 35-40% of the market share. Competition in the tissue level implant market is intensifying as companies are actively pursuing growth through innovation and strategic expansion. Established players are strengthening their global presence, while emerging firms are entering with differentiated offerings and cost competitive solutions.

Organizations are also forming partnerships and distribution alliances to expand market reach and improve accessibility. Continuous investment in research and development is driving the introduction of advanced implant designs and enhanced surface technologies. Manufacturers are also refining existing products to align with evolving clinical expectations and patient preferences, which is supporting a highly dynamic and innovation driven competitive environment.

Key Industry Developments

- In March 2026, Berlin based biotech Cellbricks Therapeutics raised € 10 million to advance its 3D bioprinted tissue implants toward clinical use. The funding will accelerate pre clinical validation of biofabricated tissue implants for severe soft tissue defects and wound repair, with the long term aim of enabling 3D printed living organs.

- In November 2025, Indonesia’s National Research and Innovation Agency (BRIN) developed a new generation of bone implants using magnesium based materials designed to be biodegradable and osteopromotive. The implants aim to support bone healing while gradually breaking down in the body, reducing the need for secondary removal surgeries.

- In June 2025, Tufts researchers developed a “smart” dental implant designed to mimic real tooth function by restoring sensory feedback during chewing and speech. The implant uses a biodegradable coating loaded with stem cells and a nerve promoting protein that gradually dissolves, encouraging new nerve rich soft tissue to form around it.

Companies Covered in Tissue Level Implant Market

- Straumann Group

- Nobel Biocare

- Dentsply Sirona

- Zimmer Biomet Dental

- Osstem Implant Co., Ltd.

- Dentium Co., Ltd.

- BioHorizons

- Bredent Medical GmbH

- CAMLOG Biotechnologies

- Alpha-Bio Tec

- MIS Implants Technologies

- TBR Group

- SHINHUNG Co., Ltd.

- Neodent

Frequently Asked Questions

The global tissue level implant market is projected to reach US$ 3.7 billion in 2026.

The market is driven by an aging population and rising prevalence of tooth loss and chronic diseases around the globe.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Major opportunities lie in expanding 3D‑printed and personalized implants and developing bioactive/biodegradable tissue‑level solutions.

Straumann Group, Nobel Biocare, Dentsply Sirona, Zimmer Biomet, and Osstem Implant are some of the key players in the market.