- Automotive Components & Materials

- Tire Material Market

Tire Material Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Tire Material Market By Material Type (Elastomers, Reinforcing Fillers, Plasticizers, Chemicals), Vehicle Type (Passenger Cars, Buses, Trucks, LCV), Regional Analysis from 2025 to 2032

Tire Material Market Share and Trends Analysis

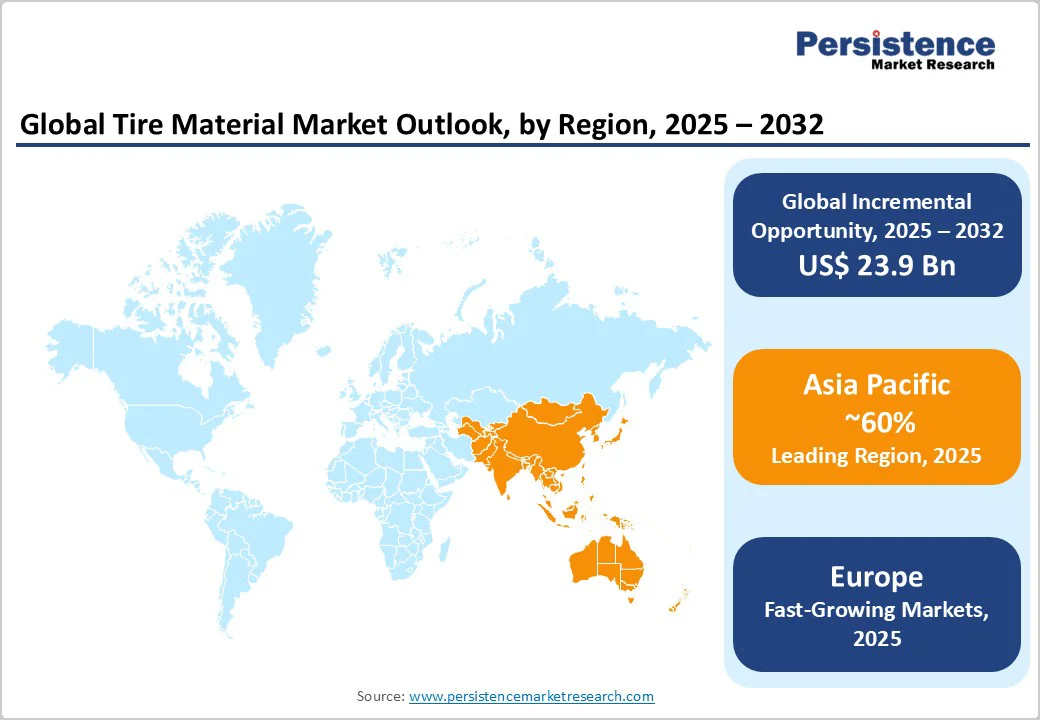

The global tire material market size was valued at US$85.0 Bn in 2025 and is projected to reach US$108.9 Bn by 2032, growing at a CAGR of 3.6% between 2025 and 2032.

The tire material industry is expanding due to rising global vehicle production and the shift toward sustainable, high-performance materials that enhance fuel efficiency and safety. Supporting this growth, worldwide motor vehicle production reached 85.4 million units in 2022, marking a 5.7% increase from the previous year, driven by urbanization and increasing disposable incomes in emerging economies.

Key Market Highlights:

- Regional Leader: Asia Pacific leads the tire material market, driven by manufacturing powerhouses such as China and India, where surging vehicle production supports dominant elastomer demand.

- Fastest Growing Region: Europe emerges as the fastest-growing region, fueled by EV adoption and infrastructure investments.

- Leading Segment: Elastomers are the dominant material type, accounting for 55% of the market share due to their critical role in traction and flexibility across tire applications.

- Fastest-Growing Segment: Reinforcing fillers are the fastest-growing segment, boosted by silica innovations for low-rolling resistance

- in sustainable tires.

- Growth Opportunities: Key opportunities lie in EV-specific materials, where low-noise, high-grip compounds can capture rising demand from NEV sales growth worldwide.

| Key Insights | Details |

|---|---|

| Tire Material Size (2025E) | US$85.0 Bn |

| Market Value Forecast (2032F) | US$ 08.9 Bn |

| Projected Growth CAGR (2025-2032) | 3.6% |

| Historical Market Growth (2019-2024) | 3.3% |

Market Dynamics

Drivers - Rising Global Vehicle Production

The surge in automotive manufacturing worldwide is a primary driver of the tire material market, as higher vehicle output directly boosts demand for essential components such as elastomers and reinforcing fillers. In 2023, commercial vehicle production in China alone grew by 22.1% year over year to 4.03 million units, reflecting a robust economic recovery and infrastructure development in Asia.

This expansion extends to passenger vehicles, where global sales are projected to increase due to urbanization, with emerging markets such as India and Southeast Asia contributing significantly to tire replacements and original equipment demand. Consequently, tire materials must meet enhanced durability standards, supporting a cycle of innovation and sustained market growth without compromising performance.

Growing Demand for Fuel-Efficient and Sustainable Tires

Consumer and regulatory emphasis on reducing carbon emissions is propelling the adoption of advanced tire materials that improve fuel economy and environmental impact. For instance, integrating silica-silane systems into tires can reduce rolling resistance by up to 35% compared to traditional carbon black fillers, enabling fuel savings of up to 8% in passenger vehicles.

This aligns with global trends in the Pneumatic Tire Market, where eco-friendly formulations are increasingly prioritized to comply with emission standards, such as those set by the European Union. As electric vehicle adoption rises, with NEV sales in China soaring 40% to 9.75 million units in the first 10 months of 2024, specialized materials for low-noise and high-grip tires are essential, fostering long-term market expansion.

Restraints - Volatile Raw Material Prices

Fluctuations in key raw material costs, particularly natural rubber and synthetic polymers, pose significant challenges to tire material manufacturers, eroding profit margins and disrupting supply chains. Natural rubber prices have shown volatility, driven by weather disruptions in major producers such as Thailand and Indonesia, resulting in a 10-15% price swing in recent years, according to the International Rubber Study Group.

This instability affects the cost of elastomers, which constitute the bulk of tire compounds, making it difficult for companies to maintain consistent pricing for end-products. Ultimately, such economic pressures hinder investment in R&D and limit market accessibility in price-sensitive regions.

Stringent Environmental Regulations

Increasingly rigorous global regulations on chemical usage and waste management are raising compliance costs for tire material production, potentially slowing industry growth.

In the European Union, the updated tire labeling regulation, effective from May 2021, mandates detailed disclosures on rolling resistance, wet grip, and noise, compelling manufacturers to reformulate materials to meet Classes A or B ratings, which can increase production expenses by 5-10%.

Similar rules in the U.S. under the Environmental Protection Agency focus on reducing volatile organic compounds from plasticizers and adhesives, adding layers of testing and certification burdens. These constraints not only delay product launches but also challenge smaller players in adapting to sustainable alternatives.

Opportunities - Advancements in Electric Vehicle-Specific Materials

The rapid proliferation of electric vehicles (EVs) presents a major opportunity for tire material innovators, as these vehicles require specialized compounds for higher torque, reduced noise, and extended range. With global EV sales expected to rise, tire designs incorporating low-rolling-resistance fillers like silica can improve efficiency by 15-20%, addressing the unique demands of battery weight and instant acceleration.

Recent developments, such as Michelin's expansion in China to produce EV-compatible tires with an annual capacity increasing to 17 million units by 2026, highlight this potential, supported by NEV production growth in key markets. Companies focusing on bio-based elastomers could capture a significant share of this segment, driven by policies such as the EU's Green Deal, which promotes zero-emission mobility.

Expansion in Sustainable and Recycled Materials

The growing emphasis on circular economy principles opens avenues for recycled and bio-based tire materials, reducing dependence on virgin resources and appealing to eco-conscious consumers. The global push for tire recycling, which generates $4.8 billion annually in the U.S. and supports 45,000 jobs, underscores the viability of reclaimed rubber and carbon black recovery.

Innovations such as Evonik's Si 363® silane enable "green tires" with up to 80% less hydrocarbon materials, aligning with regulations on extended producer responsibility in Europe and Asia. As the Retreaded Tire Market gains traction for cost-effective sustainability, manufacturers investing in chemical recycling technologies could see demand surge by 20-30% in emerging applications.

Category-wise Insights

Material Type Analysis

Elastomers dominate the material type segment in the tire market, accounting for approximately 55% of the market share due to their essential role in providing flexibility, traction, and durability in tire construction. Natural and synthetic rubbers, such as styrene-butadiene rubber, form the backbone of treads and sidewalls, enabling high elasticity while withstanding road stresses, as evidenced by their widespread use in over 80% of global tire production.

The International Rubber Study Group reports that elastomer consumption in tires exceeded 12 million tons in recent years, driven by the need for weather-resistant compounds in passenger vehicles. This leadership is further justified by advancements in bio-elastomers, which enhance recyclability without compromising performance, making them indispensable for modern tire designs.

Vehicle Type Analysis

Passenger cars lead the vehicle type category, accounting for about 50% of the tire material market share, driven by high replacement demand and the popularity of personal mobility worldwide. With global passenger vehicle production surpassing 70 million units annually, materials like reinforcing fillers are optimized for everyday commuting, offering low rolling resistance for fuel savings.

Data from the U.S. Tire Manufacturers Association indicates that passenger tire shipments reached 267.1 million units in 2024, a trend supported by rising urban populations and consumer preference for all-season tires. This dominance is reinforced by innovations in the Automotive Tire Market, where lightweight textiles reduce vehicle weight by 5-10%, improving efficiency in sedans and SUVs.

Regional Insights

North America Tire Material Trends

North America, particularly the U.S., maintains leadership in the tire material market through advanced innovation and stringent safety standards. The region's tire shipments are projected to hit 340.4 million units in 2025, up 0.9% from 2024, driven by robust automotive output and a focus on high-performance materials.

Regulatory frameworks from the National Highway Traffic Safety Administration emphasize durability testing, promoting silica-based fillers for better wet grip, as seen in recent EV tire developments by major OEMs.

The innovation ecosystem here thrives on R&D investments, with companies advancing nanotechnology for sustainable reinforcements, aligning with EPA guidelines on emissions reduction.

Europe Tire Material Trends

Harmonized regulations and a push for sustainability, with key markets like Germany, the U.K., France, and Spain leading adoption shape Europe's tire material dynamics. The EU Tire Labeling Regulation (EU) 2020/740 requires performance ratings on fuel efficiency and noise, spurring the use of low-emission elastomers that cut CO2 by up to 15 TWh annually.

Germany's automotive sector, which produces over 4 million vehicles annually, favors advanced silanes for premium tires, enhancing wet braking by 20%.

Performance analysis shows strong growth in radial construction, supported by cross-border collaborations under the EU Green Deal that are fostering the integration of recycled materials across France and Spain.

Asia Pacific Tire Material Trends

Asia Pacific is experiencing explosive growth in tire materials, led by China, Japan, India, and ASEAN countries, driven by manufacturing hubs and rising vehicle ownership. China's tire production capacity expansions, like Continental's Hefei plant reaching 18 million units by 2027, capitalize on NEV demand, with investments nearing $1 billion. India's market surges with 10% annual vehicle growth, driving demand for cost-effective fillers amid infrastructure booms.

Manufacturing advantages include low-cost labor and raw material proximity, enabling 40% of global output, as per the China Association of Automobile Manufacturers, with a focus on eco-innovations for the Industrial Tires Market.

Competitive Landscape

The global tire material market is partially fragmented, with major players holding around 40-50% share through strategic expansions and R&D, while smaller firms compete in niche sustainable segments.

Companies pursue mergers and joint ventures in bio-materials and invest in nanotechnology for lightweight reinforcements, differentiating via eco-certifications. Emerging models emphasize circular supply chains, with leaders focusing on EV-specific portfolios to capture growth in high-margin areas.

Key Market Developments

- June 2024: Continental inaugurated phase four expansion at its Hefei tire plant in China, boosting annual capacity to 18 million passenger and light truck tires by 2027 with nearly $1 billion investment.

- February, 2024: Bridgestone invested CNY 562 million over three years to enhance high-end passenger tire production in China, targeting EV market growth and premium segments.

- November, 2024: Michelin converted its Shenyang truck tire factory to passenger vehicle production, aiming for over 17 million units annually to meet NEV demands.

Top Companies in Tire Material

- ExxonMobil Corporation (Houston, United States): A leader in synthetic elastomers, ExxonMobil innovates in low-permeability compounds like Exxpro for durable inner liners, reducing raw material use by 80% and supporting fuel-efficient tires globally.

- Evonik Industries AG (Essen, Germany): Evonik excels in silica and silane technologies, with Si 363® enabling green tires that cut fuel consumption by 8%, strengthening its position in sustainable material solutions.

- Sinopec (Beijing, China): As a key petrochemical supplier, Sinopec dominates Asian markets with cost-effective chemicals and reinforcements, leveraging domestic production to supply over 20% of regional tire needs.

Companies Covered in Tire Material Market

- Bekaert

- Birla Carbon

- Cabot Corporation

- Evonik Industries AG

- ExxonMobil Corporation

- JSR Corporation

- Kuraray Co., Ltd.

- LANXESS

- PetroChina Company Limited

- Solvay SA

- Orion

- Sinopec

- Umicore

- Michelin

- Bridgestone

- Continental

Frequently Asked Questions

The global tire material market is expected to reach US$ 108.9 Bn by 2032, growing from US$ 85.0 Bn in 2025 at a CAGR of 3.6%, driven by vehicle production and sustainability trends.

Rising global vehicle production and the need for fuel-efficient tires are key drivers, with motor vehicle output hitting 85.4 million units in 2022 and silica systems reducing fuel use by 8%.

Elastomers lead with 55% market share, providing essential flexibility and traction, as used in over 80% of tire production worldwide.

Asia Pacific dominates, powered by China's expansions and India's growth, accounting for 40%+ of global output through manufacturing advantages.

Advancements in EV-specific materials offer significant potential, improving efficiency by 15-20% amid soaring NEV sales like China's 9.75 million units in 2024.

Leading players include ExxonMobil Corporation, Evonik Industries AG, and Sinopec, focusing on innovative elastomers and sustainable solutions for global dominance.