- Automotive Components & Materials

- Pneumatic Tires Market

Pneumatic Tires Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Pneumatic Tires Market by Tire Type (Radial, Cross-Ply), Vehicle Type (Two-Wheelers, Passenger Vehicle, Commercial Vehicle, Aircrafts, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026 to 2033

Pneumatic Tires Market Trends & Analysis

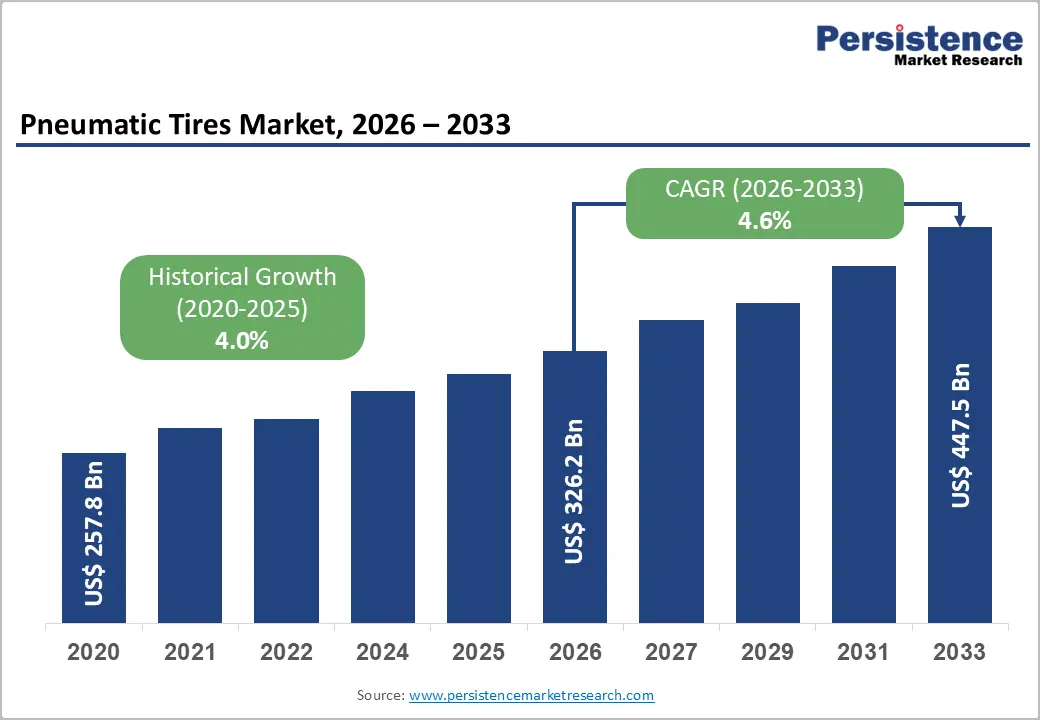

The global pneumatic tires market size is anticipated at US$ 326.2 billion in 2026 and is projected to reach US$ 447.5 billion growing at a CAGR of 4.6% between 2026 and 2033.

Rising global vehicle parc, expanding commercial fleet operations, and accelerating replacement cycles in emerging economies are the primary catalysts propelling pneumatic tire demand. The robust recovery in automotive production post-pandemic, combined with sustained freight and logistics activity, underpins consistent volume growth across both OEM and aftermarket channels.

Technological evolution toward fuel-efficient, low-rolling-resistance radial tires and the rapid electrification of passenger and commercial vehicle fleets are reinforcing premium tire adoption. Aviation sector expansion, particularly in Asia Pacific and the Middle East, is additionally broadening addressable demand, elevating the long-term structural outlook for the pneumatic tires industry.

Key Industry Highlights :

- Historical Momentum: The market expanded at a 4.0% historical CAGR (2020 - 2025) from US$ 257.80 Bn, reflecting resilient demand recovery post-pandemic across both OEM and aftermarket channels globally.

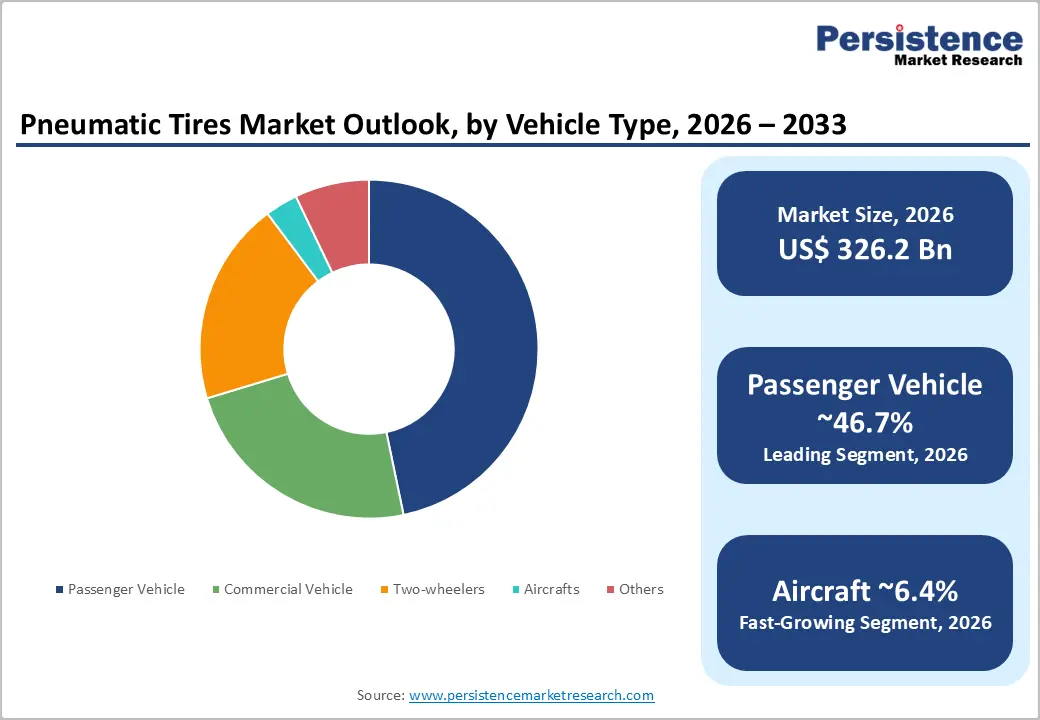

- Dominant Segment: Radial tires lead with 71.8% share and also grow fastest at 5% CAGR, while passenger vehicles command 46.7% of vehicle type revenue, underscoring segment-level market concentration.

- Aftermarket Leadership: The aftermarket sales channel holds 61.6% share and grows at 4.9% CAGR; aviation tires are the fastest-growing vehicle type at 6.4% CAGR amid global fleet expansion.

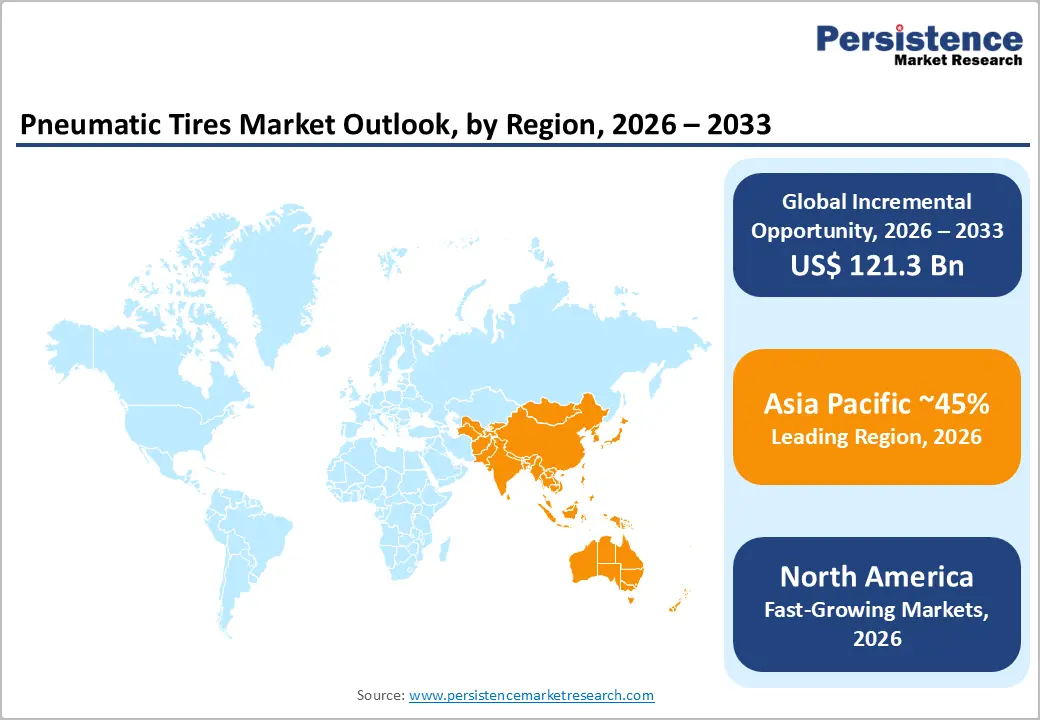

- Regional Leader: Asia Pacific dominates with ~45% global revenue share; China alone contributes ~US$ 70 Bn. North America grows at 3.9% CAGR with the U.S. market valued at US$ 58.7 Bn.

- Key Opportunity: EV-specific tires represent a US$ 10-15 Bn incremental opportunity through 2033; aviation tire demand in Asia Pacific and the Middle East presents a high-value niche for certified manufacturers.

- Strategic Activity: Bridgestone's US$ 1.3 Bn EV tire investment and Apollo's €150 Mn Hungary capacity expansion signal intensifying regional competition and EV-driven product premiumization as dominant industry themes.

Market Dynamics Analysis

Market Drivers

Rising Global Vehicle Production and Fleet Expansion

Global motor vehicle production surpassed 93 million units in 2023, according to the International Organization of Motor Vehicle Manufacturers (OICA), signaling a decisive post-pandemic rebound. Pneumatic tires are a mandatory fitment for every manufactured vehicle, creating a direct and proportional demand relationship. Emerging markets, particularly India, Indonesia, and Brazil, are registering accelerated vehicle ownership growth, expanding both OEM tire off-take and long-term replacement demand cycles significantly.

The International Energy Agency (IEA) projects the global vehicle fleet to exceed 2.0 billion units by 2035. Freight transportation, including road haulage, which represents over 75% of inland freight movement in the EU (Eurostat, 2023), maintains continuous commercial tire demand. Fleet electrification programs further drive tire upgrade requirements as EV-specific tires engineered for higher torque loads and reduced rolling resistance are increasingly specified in both OEM and fleet procurement programs.

Regulatory Push Toward Fuel Efficiency and Tire Labeling Standards

Stringent fuel economy and emissions regulations globally are compelling manufacturers to develop high-performance, low-rolling-resistance tires. The EU Tire Labeling Regulation (EU) 2020/740 mandates energy efficiency grading for all tires sold in European markets, incentivizing consumer and fleet purchases of premium-grade products. The U.S. EPA Corporate Average Fuel Economy (CAFE) Standards similarly require automakers to specify tires that contribute to overall vehicle efficiency targets, driving OEM procurement toward certified tire categories.

Japan's Top Runner Program and China's GB 18306 tire performance standards enforce comparable benchmarks, creating a globally synchronized regulatory tailwind for technologically advanced pneumatic tire segments. According to the European Tyre & Rubber Manufacturers' Association (ETRMA), labeling compliance has measurably shifted procurement preferences toward A- and B-rated fuel-efficiency tires, accelerating premium product penetration in regulated markets and elevating average selling prices across the industry.

Market Restraints

Volatility in Natural and Synthetic Rubber Supply Chains

Natural rubber, sourced predominantly from Thailand, Indonesia, and Malaysia, which collectively account for over 70% of global natural rubber supply (FAO, 2023), is subject to climatic variability, leaf blight epidemics, and geopolitical disruption, creating persistent feedstock instability. Synthetic rubber production is tied to petrochemical feedstock pricing, amplifying cost and supply unpredictability. These structural supply-side vulnerabilities constrain manufacturers' ability to maintain margin consistency and respond rapidly to demand surges across the global pneumatic tire market.

Intensifying Competition from Solid and Foam-Filled Tire Alternatives

Non-pneumatic and solid tire technologies are increasingly competitive in specific applications, including warehouse logistics, urban micro-mobility, and low-speed commercial equipment. Companies investing in Michelin's UPTIS airless tire concept and similar innovations signal a structural displacement risk for pneumatic tires in select segments. As alternative tire technologies mature and production costs decline, their addressable application scope broadens, potentially constraining pneumatic tire volume growth in niche but cumulatively significant end-use segments over the forecast period.

Market Opportunities

EV-Specific Tire Segment: A High-Value Emerging Product Category

The global electric vehicle fleet is projected to reach 245 million units by 2030 (IEA, Global EV Outlook 2023), each requiring purpose-built pneumatic tires that address unique performance demands, including higher instantaneous torque, increased vehicle weight, and enhanced rolling resistance requirements. EV-specific tires carry a significant 15-25% price premium over conventional counterparts, creating a substantial revenue opportunity for tire manufacturers that invest in dedicated R&D and production lines for electric mobility applications.

Leading OEMs including Tesla, BMW, and Volkswagen are specifying EV-optimized tires as factory fitments, embedding suppliers into long-term platform programs. Bridgestone, Continental, and Michelin have each announced dedicated EV tire product lines, reflecting the strategic priority accorded to this high-growth vertical. The incremental revenue opportunity from EV-specific tires is estimated to represent a US$ 10-15 Bn addressable uplift within the broader pneumatic tire market through 2033.

Aviation Tire Market Expansion in Asia Pacific and the Middle East

Global air passenger traffic is forecast to double by 2040 (IATA, 2023 Air Transport Outlook), with fleet expansions concentrated in Asia Pacific, the Middle East, and Latin America. Commercial aircraft tires represent a high-value niche within the pneumatic tires market, with each aircraft requiring periodic replacement of landing gear tires. Airbus projects delivery of over 42,000 new aircraft through 2042, with Asia Pacific operators accounting for approximately 40% of demand.

Aviation tire contracts command significant per-unit value and are governed by stringent safety certification requirements that favor established suppliers with regulatory expertise. Tire manufacturers positioned in the MRO (Maintenance, Repair and Overhaul) and OEM aviation supply chains, including Michelin, Bridgestone, and Goodyear, stand to capture a disproportionate share of this expanding addressable segment as global fleet sizes and aircraft utilization rates increase through the forecast period.

Category-wise Analysis

Tire Type Insights

Radial tires are likely to command the dominant position in the tire type segment, holding a 71.8% market share in 2026. Their supremacy is underpinned by superior fuel efficiency, extended tread life, superior heat dissipation, and better load-bearing characteristics compared to cross-ply alternatives. Radial tire architecture, with cord layers running perpendicular to the direction of travel, reduces sidewall flexing and rolling resistance, attributes that align with tightening global fuel economy mandates.

OEM specifications across passenger vehicles, commercial trucks, and aviation platforms overwhelmingly favor radial constructions, making displacement by cross-ply tires structurally unlikely within the forecast horizon.

Radial tires are the fastest-growing segment, but the cross-ply tires continue to witness steady growth at a CAGR of 3.5%, supported by their continued usage in off-road vehicles, agricultural equipment, two-wheelers, and cost-sensitive commercial transportation applications.

Vehicle Type Insights

In 2026, passenger vehicles are likely to represent the leading vehicle type segment with a 46.7% share of the pneumatic tires market, reflecting the sheer scale of the global passenger car fleet. Passenger vehicles generate consistent replacement demand given tire wear cycles of 25,000-50,000 miles and a broad geographic distribution of vehicle ownership. Compared to commercial or two-wheeler segments, passenger vehicles offer a wider range of high-value SKUs, from all-season to performance tires.

The growing prevalence of SUVs and crossovers in the passenger vehicle mix has further elevated average tire size and unit value, sustaining the segment's revenue dominance without risk of near-term share displacement. Aircraft represent the fastest-growing vehicle type segment at a 6.4% CAGR, driven by fleet expansion, rising air travel, and accelerated aircraft deliveries across Asia Pacific and Middle Eastern airline operators.

Sales Channel Insights

The aftermarket channel leads with a 61.6% share of the pneumatic tires market, driven by the mathematical inevitability of tire replacement requirements across the global vehicle parc of over 1.4 billion vehicles (OICA, 2023). Consumer behavior strongly favors established aftermarket brands and retailer networks for replacement purchases, aided by the growth of e-commerce tire platforms and mobile fitting services.

The aftermarket channel's structural resilience, insulated from OEM production cycle fluctuations, provides a stable and growing revenue base. Independent tire dealers, automotive workshops, and franchise service networks amplify distribution reach beyond what OEM channels alone can offer.

Aftermarket is also the fastest growing channel at a 4.9% CAGR, propelled by fleet management digitalization, subscription-based tire service models, and rising vehicle ownership in developing markets.

Regional Market Insights

North America Pneumatic Tires Market

North America is projected to witness a steady CAGR of 3.9%, supported by ongoing fleet modernization efforts and a well-established automotive ecosystem. Strong EV adoption incentives, a large installed vehicle base, and a mature aftermarket network continue to drive demand across the region. Additionally, rising commercial vehicle production and the growing adoption of EV-specific tire solutions are creating new opportunities in both OEM and replacement tire segments, reinforcing North America's long-term market growth.

U.S. Pneumatic Tires Market

The United States pneumatic tires market is projected to reach nearly US$58.7 billion in 2026, supported by strong passenger vehicle replacement demand, an extensive commercial trucking industry, and a highly developed aftermarket distribution network that includes national retail chains and digital sales platforms. Growing adoption of smart tire technologies, connected tire monitoring systems, and sustainable rubber compounds is transforming product innovation across both OEM and aftermarket channels.

Rising vehicle parc volumes, increasing freight transportation activity, and continuous advancements in tire performance, durability, and fuel efficiency further reinforce the country’s position as the largest tire market in North America.

Canada contributes additional regional demand through its sizeable vehicle fleet and recurring winter tire replacement cycles. Regulatory alignment with U.S. fuel-efficiency and tire-performance standards supports harmonized product adoption across North American OEM platforms, while Canada’s harsh climatic conditions continue to drive strong seasonal tire demand and sustain a well-established network of distributors, retailers, and automotive service centers.

Europe Pneumatic Tires Market

Europe accounts for approximately 23% of the global pneumatic tires market in 2026, supported by its strong automotive manufacturing base and stringent regulatory framework. The region benefits from a high concentration of premium vehicle OEMs, extensive vehicle ownership levels, and rigorous EU tire-labeling standards that emphasize safety, efficiency, and performance. Furthermore, Europe’s sustainability agenda is accelerating the adoption of low-rolling-resistance tires, encouraging manufacturers to invest in advanced materials and eco-friendly compounds to meet evolving environmental requirements and consumer expectations.

Germany Pneumatic Tires Market

The Germany pneumatic tires market is projected to reach nearly US$18.4 billion in 2026, supported by its position as Europe’s largest automotive manufacturing hub and the home base of major vehicle producers such as Volkswagen AG, BMW Group, and Mercedes-Benz Group AG. Strong OEM tire fitment demand, combined with a high-value replacement market, continues to drive revenue growth across the country. Accelerating electric vehicle adoption is also increasing demand for specialized EV-optimized tires designed for lower rolling resistance, higher torque handling, and enhanced durability, while the aftermarket segment remains the dominant revenue contributor within the market.

The U.K., France, and Spain represent important secondary markets, with France benefiting from the strong domestic manufacturing presence of Michelin and Spain strengthening its position through automotive assembly expansion and export-oriented tire production. Meanwhile, Italy adds further strength to Europe’s premium tire sector through the global presence of Pirelli & C. S.p.A. and its long-standing expertise in high-performance and motorsport-oriented tire technologies.

Asia Pacific Pneumatic Tires Market

Asia Pacific leads the global pneumatic tires market, accounting for approximately 45% of total revenue. The region’s dominance is fueled by China's vast vehicle production capacity, India's rapidly expanding automotive industry, and rising vehicle ownership across Southeast Asia. Beyond strong domestic demand, Asia Pacific is increasingly establishing itself as a global tire manufacturing and export hub, with producers across China, India, and ASEAN countries expanding capacity to serve growing demand from both regional and international markets.

China Pneumatic Tires Market

China pneumatic tires market is projected to reach nearly US$70 billion in 2026, supported by its position as the world’s largest automotive manufacturing and vehicle consumption market. Strong OEM tire fitment demand, a massive replacement tire ecosystem, and continuous growth in passenger and commercial vehicle ownership continue to drive market expansion. China also remains a major global tire export hub, benefiting from extensive production capacity, competitive manufacturing costs, and a well-developed supply chain.

Increasing adoption of premium tires, EV-specific tire technologies, and smart tire solutions is further strengthening the country’s leadership in both domestic and international tire markets.

India, with an estimated market value of around US$26 billion, is experiencing strong growth driven by government support for automotive manufacturing, its position as the world’s largest two-wheeler market, and rising passenger and commercial vehicle sales. Japan contributes through its advanced OEM tire ecosystem and high-precision tire engineering capabilities, while India’s expanding highway infrastructure and increasing radial tire penetration in commercial vehicles continue to provide long-term structural support for market growth across the region.

Competitive Landscape

The global pneumatic tires market is moderately consolidated, with the top five manufacturers, Bridgestone, Michelin, Goodyear, Continental, and Sumitomo, collectively commanding an estimated 55-60% of global revenue. Key differentiators include proprietary compound technologies, global manufacturing footprint, OEM platform designations, and certified product portfolios for regulated markets. Emerging business models encompass tire-as-a-service (TaaS) for fleet operators and digital retailing through owned and partner e-commerce platforms.

Dominant strategic themes include EV-specific tire innovation, capacity expansion in Asia Pacific and Eastern Europe, sustainability-led R&D in bio-based rubber compounds, and digitalization of supply chain and consumer touchpoints. Market leaders are prioritizing ADAS-compatible and intelligent tire technologies embedded with sensors for real-time pressure and wear monitoring, establishing technology-driven competitive moats aligned with the connected vehicle ecosystem.

Strategic Developments

- In February 2024, Bridgestone Corporation invested nearly £5 million into its Bulldog Bandag retread facility in the U.K. to expand hot-cure commercial tire retreading capacity and strengthen sustainable fleet tire solutions across the European commercial vehicle market.

- In September 2024, Bridgestone Corporation launched the Potenza Sport A tire incorporating 55% ISCC PLUS-certified recycled and renewable materials, marking the company’s first mass-produced sustainable premium tire developed specifically for EV readiness and enhanced environmental performance.

- In February 2024, Pirelli & C. S.p.A. expanded its collaboration with Porsche by developing custom P Zero tires for the electric Macan SUV, focusing on optimized rolling resistance, sport handling characteristics, and high-performance EV compatibility for premium automotive applications.

Companies Covered in Pneumatic Tires Market

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Sumitomo Rubber Industries

- Pirelli & C. S.p.A.

- Yokohama Rubber Co.

- Hankook Tire & Technology

- Cooper Tire & Rubber

- Toyo Tire Corporation

- Nokian Tyres

- Apollo Tyres Ltd.

- MRF Limited

- Zhongce Rubber Group

- Giti Tire

Frequently Asked Questions

The global pneumatic tires market is valued at US$ 326.2 Bn in 2026, projected to reach US$ 447.5 Bn by 2033, supported by a global vehicle parc exceeding 1.4 billion units and steady replacement demand.

Growth is driven by rising global vehicle production surpassing 93 million units annually (OICA), mandatory tire labeling compliance, accelerating EV adoption, and expanding commercial fleet operations across emerging economies.

The market is projected to grow at a CAGR of 4.6% from 2026 to 2033, building on a 4.0% historical CAGR (2020-2025), driven by EV platform proliferation, aviation expansion, and aftermarket channel digitalization.

Key opportunities include EV-specific tire development, representing a US$ 10-15 Bn incremental market by 2033, and aviation tire expansion across Asia Pacific where Airbus projects over 42,000 new aircraft deliveries through 2042.

Leading players include Bridgestone, Michelin, Goodyear, Continental, Sumitomo Rubber, Pirelli, Yokohama, Hankook, Apollo Tyres, and MRF, competing on technology, geographic scale, OEM designations, and EV-specific product portfolios.