- Automotive Components & Materials

- Retreaded Tire Market

Retreaded Tire Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

Retreaded Tire Market By Vehicle Type (Passenger Cars, Light Commercial Vehicle, Heavy Commercial Vehicle, and Off-road Vehicles), By Process Type (Pre Cure, and Mold Cure), By Sales Channel (OEM, and Independent Service Provider), and Regional Analysis for 2025 - 2032

Retreaded Tire Market Size and Trends Analysis

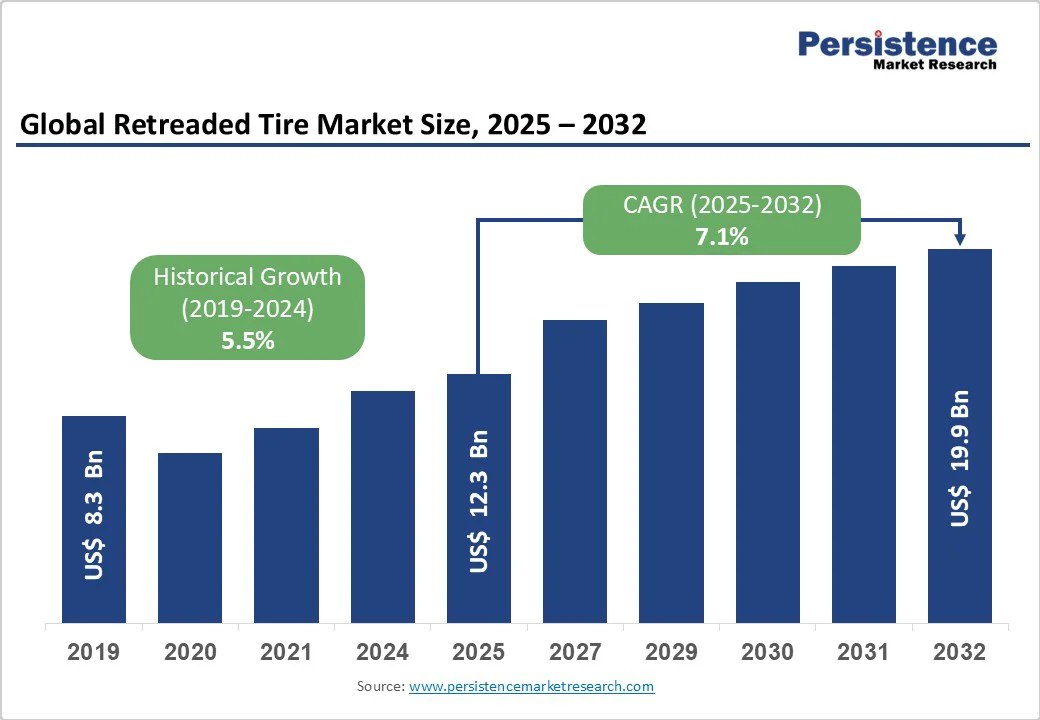

The global retreaded tire market size is expected to increase from US$12.3 billion in 2025 to US$19.9 billion by 2032, growing at a CAGR of 7.1% during the forecast period from 2025 to 2032.

The retreaded tire market has experienced rapid growth in recent years, driven by the high usage of retreaded tires in commercial fleets and increasing environmental regulations. For example, U.S. fleets haul over 72% of the nation’s freight by weight, and nearly half of that mileage runs on retreaded truck tires.

Key Industry Highlights:

- Dominant Region: North America dominates the market with 15 million tires retreaded annually and 268,000 associated jobs.

- Fast-growing Region: Asia Pacific emerges as the fastest-growing region, driven by industrialization, logistics expansion, and cost-saving initiatives.

- Leading Vehicle Type: Heavy trucks dominate retread demand globally, accounting for roughly 87% of total market consumption.

- Fast-growing Vehicle Type: Passenger vehicles are the fastest-growing segment, driven by environmental awareness and evolving retread technologies.

- Dominant Process: Pre-cure retreading remains dominant, controlling 96% of the global market share due to cost-effectiveness and flexibility.

- Fast-growing Process Type: Mold-cure retreading is the fastest-growing, targeting premium tire segments with improved performance and appearance.

- Leading Services: Independent service providers lead sales, holding 68% market share, while OEM channels expand at 7.2% CAGR.

| Key Insights | Details |

|---|---|

| Retreaded Tire Market Size (2025E) | US$12.3 Bn |

| Market Value Forecast (2032F) | US$19.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.5% |

Market Dynamics

Driver- Strengthening Performance and Sustainable Transportation Solutions Globally

The retreaded tire market is driven by economic, environmental, and technological factors that underscore its importance in sustainable transportation. Cost efficiency is a key driver, with retreaded tires costing 30-50% less than new ones, allowing fleets such as long-haul trucks, delivery services, and waste haulers to save billions annually.

According to the U.S. Tire Manufacturers Association (USTMA), over 15 million tires are retreaded each year in the U.S., supporting approximately 51,000 jobs within a broader tire ecosystem of around 268,000 jobs.

Environmental advantages further fuel demand. Each retread saves approximately 15 gallons of oil and 90 pounds of raw material, resulting in a 24% reduction and CO2 emissions and diverting 1.4 billion pounds of waste from landfills annually. These benefits align with global circular economy goals, EPA sustainability initiatives, and EU waste directives.

Technological advancements amplify growth, with innovations like Bridgestone’s Bandag Buffer 8550E improving quality and consistency. Enhanced products, such as the Bandag BDR-AS3, with 18% longer wear life, meet the rising needs of the e-commerce and logistics sectors, projected to expand by 4-5% annually.

Market Restraining Factors

Consumer Misconceptions, Limited Infrastructure, and Cost Volatility Restrain Market Expansion Globally

Despite its benefits, the retreaded tire market faces notable restraints that limit adoption. Persistent myths about safety and quality remain a major challenge. Many consumers believe retreads lack structural integrity since new tread is applied over used casings.

However, USTMA data confirms that properly maintained casings are durable, and retreads undergo rigorous inspections to ensure safety comparable to new tires. Skepticism is especially high in the passenger car segment, where new tires dominate 80% of replacements (DOT).

Limited retreading facilities further constrain growth. U.S. plants have declined from 3,000 in 1982 to 500 today (USTMA), restricting access in rural and developing areas while increasing logistics costs. Raw material price fluctuations, exacerbated by global supply disruptions, raise production costs by 10-15% (RMA), reducing competitiveness against low-cost imports.

Regulatory restrictions in regions like the EU, variable casing quality, which limits mileage to 70-80% of that of new tires, and myths about heat buildup also hinder expansion. Addressing these challenges through consumer education and infrastructure investments is crucial to unlocking the market’s full potential.

Key Market Opportunities

Sustainable Growth Opportunities Driven by Circular Economy, Innovation, and Expanding Global Fleet Demand

The Retreaded tire market presents significant opportunities for players to enhance growth, sustainability, and profitability. The global shift toward a circular economy positions retreads as an eco-friendly choice. According to the U.S. Tire Manufacturers Association (USTMA), retreads save 215 million gallons of oil annually in North America and cut CO2 emissions by 24%, aligning with the UN Sustainable Development Goals.

Expanding applications in aviation and off-road sectors, where 70% of aircraft tires are retreated (FAA), offer additional revenue streams. Technological advancements, including AI-driven inspections and robotic curing, boost efficiency by 20-30%, as demonstrated by Bridgestone’s 2023 Buffer 8550E. These improvements deliver premium-quality retreads that rival new tires, dispelling myths about safety and performance while strengthening customer trust.

Emerging markets, such as Asia and Latin America, offer untapped growth opportunities. The Asian Development Bank projects a 6% CAGR in commercial fleets, with cost-sensitive operators saving up to 40% by adopting retreads. Government incentives in India and proposed North American tax credits (15-20% production boost) further drive adoption.

Retreaded Tire Market Insights and Trends

Process Insights

Pre-Cure Leads Global Retreading While Mold-Cure Rapidly Expands in Premium Tire Segments

In retreading, Pre-Cure (or envelope cure) is the dominant process. It commands about 96% of the global market share as of 2024. Pre-cure retreading involves affixing a pre-formed tread strip to a prepared casing and curing them together. It is favored for its lower setup costs and flexibility to match various tire sizes, making it attractive to independent retreaders worldwide.

Mold-Cure retreading (where tread rubber is applied as a raw compound and cured under a mold) accounts for the remaining share. Mold-cure processes yield retreads with performance and appearance comparable to new tires, but require higher capital expenditures. As a result, mold-cure has been gaining momentum in premium segments.

Leading tire companies have been expanding their mold-cure retread operations; for instance, major manufacturers are increasing mold-cure capacity to serve fleets that demand “like-new” quality. In summary, pre-cure remains the leading process, valued for cost-effectiveness, while mold-cure is the fastest-growing niche, driven by quality and appearance requirements.

Process Type Insights

Heavy Trucks Dominate Retread Demand While Passenger Vehicles Emerge as The Fastest-Growing Opportunity

The commercial vehicles segment (including heavy-duty trucks, buses, and LCVs) overwhelmingly leads the retread market. Reports indicate commercial vehicles account for roughly 87% of global retread demand in 2024. This dominance is driven by the cost-sensitive nature of trucking and fleet operations: large trucks and buses are designed for multiple retreads, and operators use retreads routinely to cut costs.

The heavy truck segment is the largest contributor, with demand boosted by long-haul carriers and logistics companies. Passenger cars are a smaller segment of the retread market, but they represent the fastest-growing opportunity. Environmentally conscious drivers and policymakers in regions such as Europe are advocating for the use of passenger car retreads to reduce waste. Manufacturers are developing new retread processes to meet car safety standards.

Advances in materials and tread design are making car retreads increasingly viable; for example, some fleets of taxis or corporate cars in niche markets now utilize retreaded tires. Light Commercial Vehicles (LCVs) (vans and pickups) occupy a middle ground: they are less frequent than trucks, but retreads are still used, especially in cost-focused fleets.

Off-road vehicles (construction, mining, agricultural equipment) use retreads selectively; their heavy loads and harsh conditions require robust retreads, but the market share is smaller due to specialized tire needs. Overall, heavy trucks remain the leading segment, while passenger vehicles (and emerging urban delivery fleets) show the fastest growth as technology and awareness improve

Sales Channel Type Insights

Independent Providers Dominate Retread Sales While OEM Expansions Accelerate Growth Through Partnerships and Certifications

Sales channels in the Retreaded tire market include OEMs and independent service providers, with independents leading with a 68% share, according to Market.us, due to their extensive networks and competitive pricing for fleets. USTMA notes that these small businesses produce nearly 100% of the domestic retreads, serving 15 million U.S. tires annually and supporting 51,000 jobs. Their flexibility in customization drives HCV dominance, offering 40% savings over OEMs.

OEM channels are the fastest-growing at a 7.2% CAGR, from a 32% share, as manufacturers like Bridgestone integrate retreading into their supply chains. OEM expansions, such as 2023 plant investments, enhance quality assurance, appealing to military and government users. DOT data shows OEM retreads improving fleet efficiency by 30% in energy use. Independents lead in accessibility, while OEMs grow through partnerships and certifications, bolstering market trust.

Regional Insights and Trends

North America Leads with Sustainable Retreading, Advanced Fleets, and Expanding Transportation Efficiency

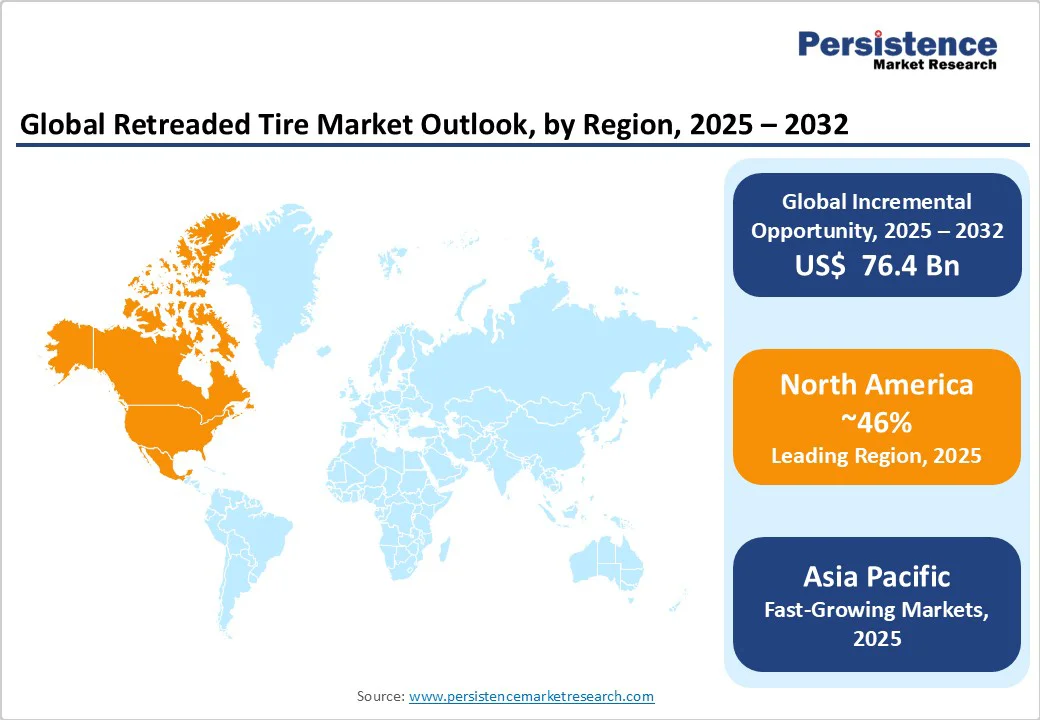

North America remains the dominant region in the retreaded tire market with a 46% revenue share in 2024, supported by advanced transportation infrastructure, extensive commercial fleets, and a strong focus on sustainability.

According to the U.S. Tire Manufacturers Association, retreading is the nation’s largest remanufacturing sector, employing over 51,000 workers and supporting more than 268,000 jobs within the $28.4 billion U.S. tire industry. While major brands like Bridgestone, Continental, Goodyear, and Michelin license franchise agreements, nearly all retreading is performed domestically by small, independent businesses that employ 10-60 workers.

The region retreads approximately 15 million tires annually, with U.S. truck and bus fleets retreading each tire two to three times on average. Nearly 90% of fleets with more than 100 trucks rely on retreads for cost savings, operational reliability, and environmental benefits.

Retreads account for 44% of all commercial truck tires across the U.S. and Canada, underscoring their pivotal role in logistics and national security. In 2022, trucks accounted for 72% of U.S. freight by weight, with nearly half of the freight transported on retreaded tires. Growing fleet electrification, stricter ESG goals, and advanced technologies will sustain North America’s leadership through 2025-2032.

Asia Pacific Emerges as the Fastest-Growing Hub for Retreated Tire Through 2032

Asia Pacific is projected to remain the fastest-growing region in the Retreaded tire market, driven by rapid industrialization, urbanization, and expanding logistics networks. In 2024, the region held a commanding 60% market share, with China and India leading the growth.

China’s commercial vehicle fleet surpasses 30 million units (CAAM), relying on retreaded tires to reduce operational costs by up to 40%, supported by a 7% annual growth rate in logistics. Regional industry bodies, echoing USTMA findings, report 20-25% emission reductions, aligning with China’s 2060 carbon neutrality target. India’s adoption is accelerating through government sustainability incentives and the expansion of heavy commercial vehicle fleets.

SIAM notes a 15% rise in retread usage among e-commerce fleets, showcasing the cost-efficiency and eco-friendly benefits of retreads. Japan and South Korea contribute advanced technologies, particularly pre-cure processes, to enhance tread life and performance. According to the Asian Development Bank, Asia Pacific’s automotive production is set to grow at a 5-6% CAGR, reinforcing retread demand as manufacturers and fleets embrace circular economy practices through 2032.

Competitive Landscape

The global retreaded tire industry is fiercely competitive, with leading players focusing on innovation, strategic partnerships, and geographic expansion to reinforce their market positions.

Companies invest heavily in advanced retreading technologies to enhance tire performance, durability, and safety, while meeting stringent regulatory standards and addressing consumer concerns about quality. Collaborations with fleet operators, logistics providers, and service networks enhance market reach and build customer loyalty.

Mergers and acquisitions are common, enabling firms to consolidate expertise, diversify product portfolios, and optimize supply chains for efficiency. Sustainability and cost-effectiveness drive strategies, with manufacturers adopting automation, AI-based inspections, and strong R&D to deliver high-quality, eco-friendly retreads.

According to USTMA, these efforts support over 268,000 U.S. tire industry jobs through domestic manufacturing. Top companies leverage technology and sustainable practices to capitalize on the rising global demand and maintain a competitive edge.

Key Industry Developments:

- In 2025, Bridgestone increased capacity by 20% for pre-cure retreads, enhancing U.S. supply for commercial fleets. Bridgestone Invests $60 Million to Expand Abilene Bandag Retread Tire Plant.

- In 2023, Michelin introduced the X One Line Energy D2 Pre-Mold, targeting the long-haul market across the U.S. with a focus on optimizing fuel efficiency. Simultaneously, the X One XDS2 Pre-Mold was launched to deliver enhanced traction and durability, specifically engineered to handle the harshest Canadian winter conditions.

- In 2021, The Goodyear Tire & Rubber Company (NASDAQ: GT) introduced its RT-3B bead-to-bead retread. Designed for loaders and graders, the new retread delivers versatile performance across a range of diverse underfoot conditions, enhancing Goodyear’s existing portfolio of premium off-the-road (OTR) retread tires.

Companies Covered in Retreaded Tire Market

- Bridgestone Corporation

- The Goodyear Tire & Rubber Company

- JK Tyres

- Michelin

- Continental AG

- MRF

- Yokohama Rubber Company

- Carloni Tires

- Nokian Tyres.

- Others

Frequently Asked Questions

The Retreaded tire market is estimated to be valued at US$ 12.3 Bn in 2025.

Key growth drivers strengthening Retreaded tire market performance and sustainable transportation solutions globally.

In 2025, the North America region dominates with a 46% revenue share in the global market.

Among the processes, pre-cure leads the retreaded tire market beyond 60% of the market revenue share in 2025, surpassing other processes.

Bridgestone Corporation, The Goodyear Tire & Rubber Company, JK Tyres, Michelin, Continental AG, and MRF are among the prominent companies operating in the Retreaded tire market.