- Power Generation, Transmission, & Distribution

- U.S. Thermal Power Market

U.S. Thermal Power Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Thermal Power Market by Fuel Type (Natural Gas, Coal, Oil), End-user (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

U.S. Thermal Power Market Size and Trends Analysis

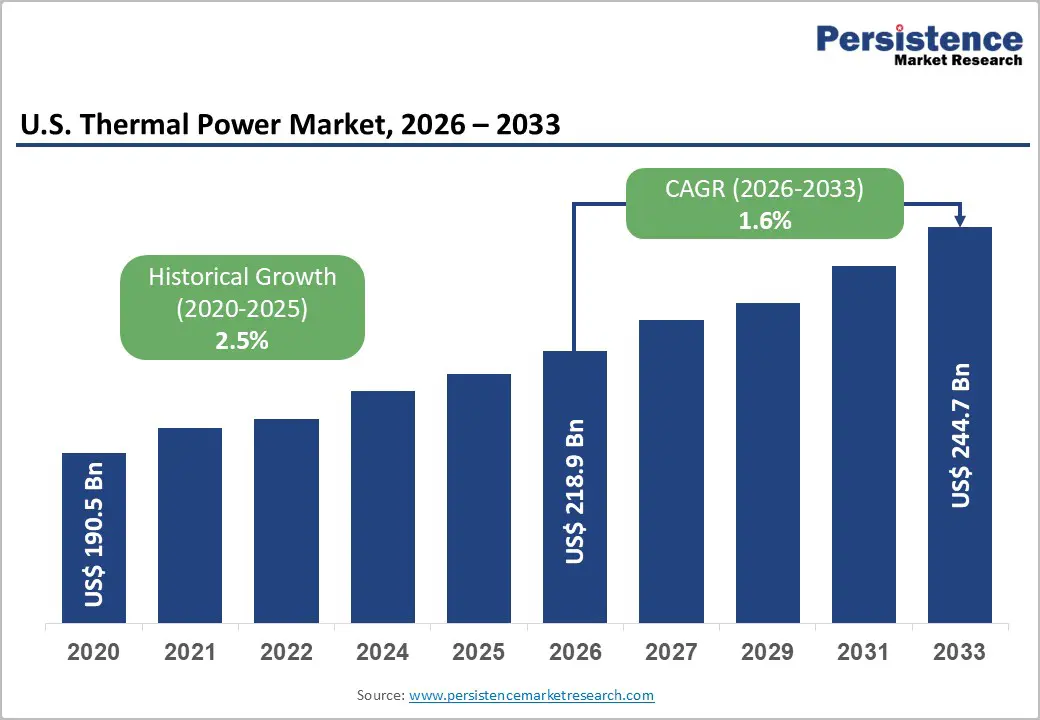

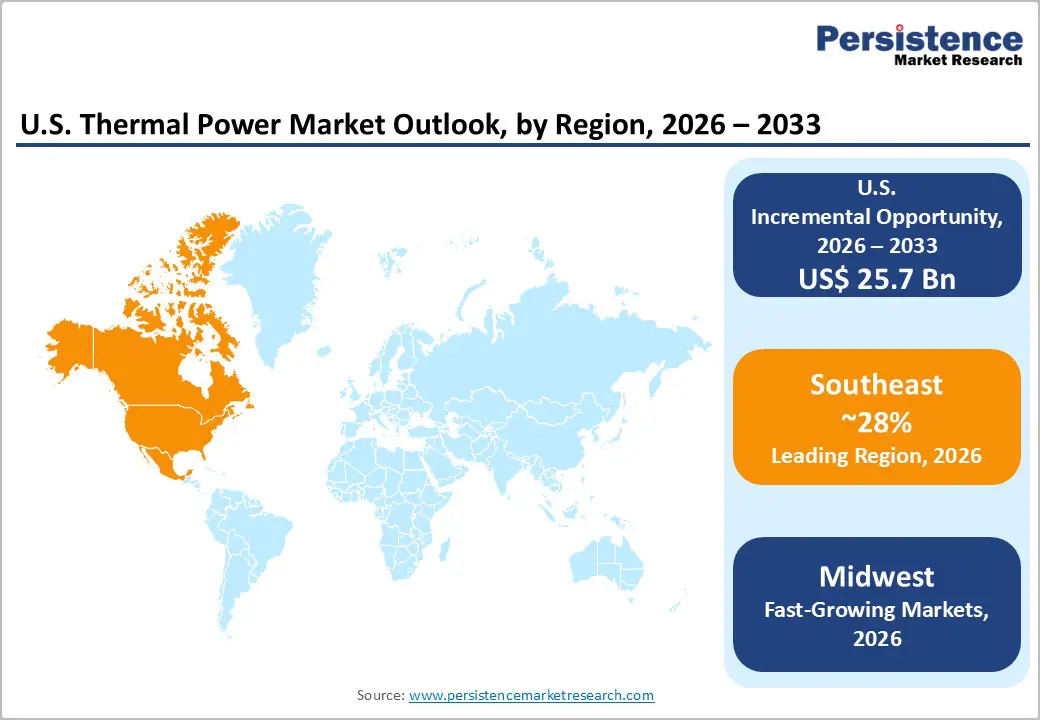

The U.S. thermal power market size was valued at US$ 218.9 Bn in 2026 and is projected to reach US$ 244.7 Bn by 2033, growing at a CAGR of 1.6% between 2026 and 2033. The market registered a historical CAGR of 2.5% between 2020 and 2026, expanding from US$ 190.5 Bn in 2020, demonstrating consistent long-term demand for dispatchable baseload power across the national grid. Primary demand momentum is anchored by record natural gas consumption averaging 90.3 billion cubic feet per day (Bcf/d) in 2024, the highest annual volume ever recorded by the U.S. Energy Information Administration, combined with accelerating electricity load from AI-driven data centres, industrial capacity additions, and extreme seasonal weather events.

The U.S. electric power sector consumed 32.11 quads of primary energy in 2023, functioning as the country's single largest primary energy-consuming segment. Thermal generation retains its structural position as the primary mechanism for meeting peak grid demand that intermittent renewable sources cannot fully serve.

Key Industry Highlights:

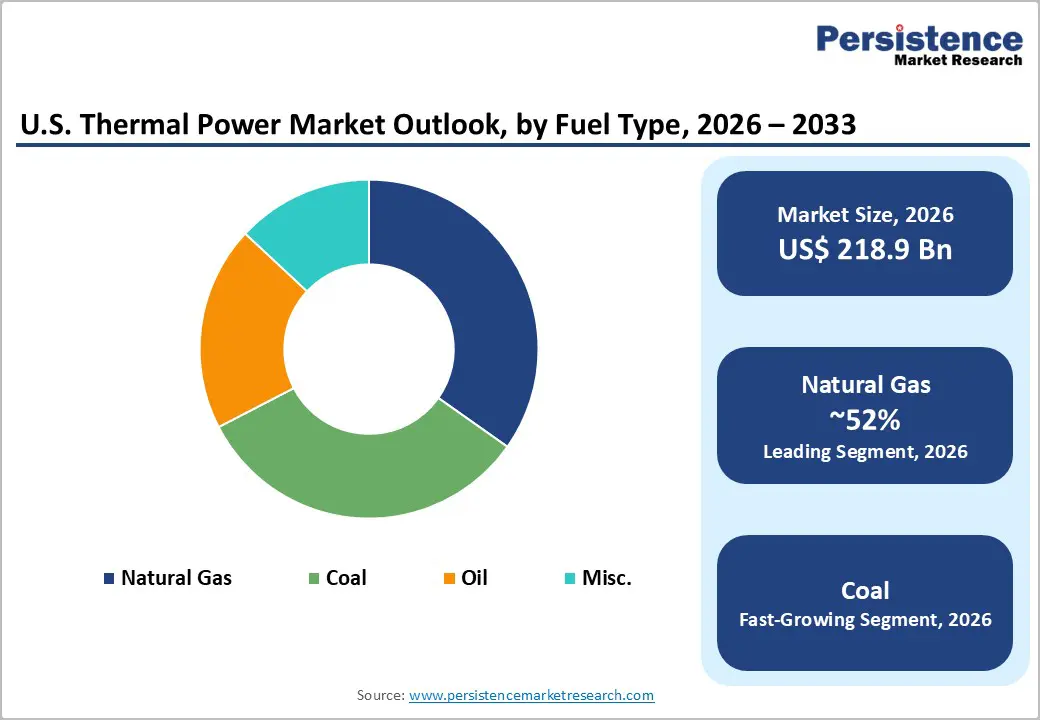

- Leading Fuel Type: Natural gas dominates with 52% market share in 2025, driven by abundant domestic reserves, cleaner combustion, and widespread infrastructure investment across all major U.S. regions.

- Fast-growing Fuel Type: Coal is the fastest-growing fuel segment in the short term, supported by elevated natural gas prices, above-trend electricity demand, and constrained CCGT availability despite long-term retirements.

- Residential End-user Dominance: The residential segment holds 38% of market share, reflecting steady household demand for space heating, water heating, and cooling across the U.S.

- Industrial Segment Rapid Growth: Industrial demand is the fastest-growing end-use category, fueled by AI-enabled data centres, steel production, and large-scale manufacturing requiring continuous baseload thermal power.

- Extreme Weather Drives Peak Demand: Polar vortex events and summer heatwaves significantly spike thermal power consumption, validating continued investment in dispatchable generation assets.

- Fuel Security & Midstream Integration Opportunity: Vertical integration across the natural gas supply chain strengthens cost competitiveness and operational resilience, particularly amid LNG export expansion and regional price volatility.

- Combined-Cycle Expansion for AI & Industrial Loads: New combined-cycle natural gas projects targeting high-load industrial and AI data center demand offer a compelling long-term growth vector for thermal power developers.

| Key Insights | Details |

|---|---|

| U.S. Thermal Power Market Size (2026E) | US$ 218.9 Bn |

| Market Value Forecast (2033F) | US$ 244.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 1.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.5% |

Market Dynamics

Drivers - Natural Gas Achieves Record Consumption as the Structural Backbone of U.S. Power Generation

Natural gas has evolved from a supplementary fuel to the indispensable backbone of U.S. electricity supply, underpinned by two decades of shale-driven domestic production growth and progressive fuel switching from coal. Its flexibility, price competitiveness, and high combustion efficiency have made it the preferred dispatch fuel for the U.S. Thermal Power Market across both seasonal peaks and baseload requirements.

In 2024, U.S. natural gas consumption reached a historic high of 90.3 Bcf/d, with the electric power sector alone accounting for 41% of total national gas use, rising 4% (1.6 Bcf/d) year-over-year, as historically low prices improved its dispatch economics relative to coal. Natural gas achieved a record 43% share of total U.S. electricity generation in 2024. By 2025, the annual average price recovered to $3.52/MMBtu, a 56% year-over-year increase signalling supply-demand normalisation as LNG export capacity added an estimated 3 Bcf/d of structural demand. Since 2017, U.S. natural gas production has consistently exceeded domestic consumption, and in 2023, domestic output reached approximately 39 quads (38% of total primary energy production), reinforcing long-term energy security and fuel supply reliability for thermal power operators.

Extreme Weather Cycles Drive Sustained Peak Electricity Demand Across Thermal Generation Assets

Weather conditions function as the single largest short-term driver of electricity generation demand in the United States, directly determining dispatch volumes and fuel burn rates across the U.S. Thermal Power Market. Polar vortex events in winter and prolonged heat waves during summer consistently expose the limitations of intermittent generation, reinforcing the irreplaceable dispatch role of thermal power assets in grid balancing.

January 2024 natural gas consumption surged 12% year-over-year due to severe winter heating demand, while July 2024 consumption rose 3% on the back of elevated summer cooling loads. The summer of 2024 ranked as the fourth warmest on record across the Lower 48 states, pushing electric power sector gas consumption to record highs in July and August. U.S. electricity generation was up 6.3% in the first four months of 2025 compared to the same period in 2024, reflecting a sustained upward trajectory in total grid demand. Toward year-end 2025, a polar vortex event in late November–early December temporarily pushed natural gas spot prices above $5.00/MMBtu, with Algonquin Citygate averaging $16.37/MMBtu in January 2025 and $14.00/MMBtu in February 2025, the highest monthly averages since 2022. These recurring demand spikes systematically validate continued investment in dispatchable thermal capacity.

Geopolitical Energy Supply Risk Reinforces the Strategic Value of Domestic Thermal Infrastructure

Heightened geopolitical tensions, particularly the escalating conflict involving the United States, Israel, and Iran, have placed renewed emphasis on the strategic importance of domestically controlled thermal power generation capacity. Supply disruptions affecting global energy transit routes directly translate into domestic fuel price volatility, amplifying the economic and energy security arguments for maintaining and optimising existing U.S. Thermal Power Market infrastructure.

The Strait of Hormuz, through which approximately one-fifth to one-quarter of global oil and a significant share of LNG exports transit, represents a critical global energy chokepoint that rising conflict risk has made increasingly uncertain. U.S. crude oil production reached an all-time monthly record of 13.4 million barrels per day (b/d) in August 2024, with annual production forecast to reach 13.5 million b/d in 2025, partially insulating domestic fuel supply chains from external shocks.

Global oil price benchmarks remain tightly correlated with domestic wholesale energy prices. Historically, energy supply disruptions tied to geopolitical events have contributed to inflationary pressure and economic slowdowns in the United States. This risk environment reinforces the case for domestic thermal power capacity as a fuel-flexible, grid-stable hedge against international supply volatility, particularly for high-load industrial consumers and grid operators prioritising reliability-of-supply over cost minimisation.

Restraint - Structural Coal Plant Retirements Reduce Long-Term Thermal Generation Capacity

Coal-fired generating capacity across the United States is in irreversible structural decline, constrained by environmental compliance obligations, carbon emissions regulation, and the sustained price competitiveness of natural gas.

The U.S. EIA projects coal generating capacity to fall from 177.1 GW in Q4 2023 to approximately 162 GW by the end of 2025, as plant retirements accelerate significantly. Total coal stocks in the electric power sector declined from 116.4 MMst to 105.4 MMst during Q3 2025 alone, reflecting tighter fuel balances even as generation temporarily rebounded. The irreversible contraction in coal capacity represents a meaningful long-term constraint on the fuel diversity of the U.S. thermal power fleet, limiting grid operators' ability to deploy coal as a swing generation resource during high-demand periods.

Pipeline Infrastructure Constraints and Regional Bottlenecks Limit Generation Dispatch Efficiency

Persistent transmission and pipeline infrastructure limitations constitute a structural barrier to optimising the economic performance of U.S. thermal generation assets. Regional supply constraints, particularly in the Northeast, have repeatedly caused price spikes at key trading hubs, undermining cost predictability for thermal operators.

The U.S. combined-cycle gas turbine (CCGT) fleet declined by nearly 2,000 MW since 2023, with no new capacity additions in the preceding 16 months, creating additional dispatch headroom for coal during periods of constrained gas infrastructure availability. Algonquin Citygate and Transco Zone 6 NY spot prices surged to multi-year highs in early 2025 due to cold weather events compounded by pipeline bottlenecks, highlighting how infrastructure deficiencies translate directly into market risk for thermal power generation economics.

Opportunity - Combined-Cycle Natural Gas Capacity Development to Serve AI-Driven Data Centre and Industrial Power Demand

The rapid deployment of AI computing infrastructure and hyperscale data centres across the United States is generating a structurally new category of large, continuous electricity demand, one that requires the reliability, dispatchability, and capacity scale that only thermal power generation can readily provide. This trend represents a compelling long-term growth vector for the U.S. Thermal Power Market, linking digital infrastructure investment directly to new thermal power plant development.

In December 2025, NextEra Energy Resources, LLC and Basin Electric Power Cooperative signed a Memorandum of Understanding to jointly explore the River Run Energy Center, a proposed ~1,450 MW combined-cycle natural gas-fired power plant in North Dakota, submitted to the Southwest Power Pool for expedited resource adequacy evaluation under Basin Electric's Large Load Commercial Program explicitly designed to serve data center and high-load industrial demand. As AI infrastructure and manufacturing facility deployments intensify across multiple U.S. regions, thermal power developers with access to capital, fuel supply, and transmission interconnection rights are positioned to capture long-term contracted generation revenue from this high-reliability demand segment within the U.S. Thermal Power Market.

Natural Gas Supply Chain Integration Enhances Fuel Security and Cost Competitiveness for Thermal Operators

Vertical integration across the natural gas value chain, encompassing upstream supply, midstream storage, and fuel delivery logistics, represents a high-impact commercial opportunity for thermal power generators seeking to insulate their operations from regional price volatility and tightening LNG export-driven supply dynamics. Control over midstream infrastructure directly strengthens the operational and financial resilience of gas-fired generation assets within the U.S. Thermal Power Market.

In December 2025, NextEra Energy Resources, LLC announced the acquisition of Symmetry Energy Solutions from Energy Capital Partners, expanding gas supply, storage, and asset management capabilities across 34 U.S. states. This transaction reflects a broader industry trend toward fuel supply security as LNG export demand expanded by an estimated 3 Bcf/d in 2025 following new export terminal capacity additions, tightening domestic supply-demand balances.

U.S. natural gas production has exceeded domestic consumption every year since 2017, reaching approximately 39 quads in 2023, but mid-continent supply access and storage positioning remain critical determinants of dispatch cost for individual thermal operators. Integrated midstream ownership reduces basis risk and operational vulnerability to weather-related supply disruptions.

Grid Modernisation and High-Voltage Transmission Investment to Unlock Thermal Generation Asset Value

Expanding high-voltage bulk transmission infrastructure presents a strategic opportunity to extend the commercial dispatch range and economic efficiency of large-scale thermal power plants, directly improving the return profile of existing generation assets within the U.S. Thermal Power Market. Projects that materially increase power-transfer capacity between generation-rich and demand-constrained regions are essential to realising the full economic value of installed thermal capacity.

In February 2026, the PJM Interconnection Board of Directors approved the development of an approximately 220-mile, 765-kV transmission line across West Virginia, Pennsylvania, and the Mid-Atlantic region, jointly developed by NextEra Energy Transmission, LLC and Exelon Corporation. The 765-kV architecture can transmit 2–3 times more power than comparable 500-kV systems while reducing transmission losses by up to 50% directly improving dispatch economics and revenue certainty for large-scale fossil-fuel power plants connected to the corridor. Addressing transmission bottlenecks through capital investment, such as this PJM-recommended project, strengthens long-term grid reliability and enables sustained operation of thermal generation facilities amid the Northeast's structurally constrained energy infrastructure.

Category-wise Analysis

Fuel Type Insights

Natural gas holds 52% of the U.S. Thermal Power Market’s fuel type share, commanding the majority position due to its superior economics, cleaner combustion profile relative to coal, and the structural advantages conferred by abundant domestic shale reserves. It’s dominance is reinforced by sustained investment in gas-fired generation infrastructure across all U.S. power market regions over the past two decades.

In 2024, natural gas achieved a record 43% share of total U.S. electricity generation, with electric power sector consumption rising 4% year-over-year to 41% of national gas demand. U.S. natural gas production has consistently exceeded domestic consumption since 2017, with output reaching approximately 39 quads in 2023, reinforcing long-term fuel supply security for thermal power operators. The 2025 Henry Hub price recovery to $3.52/MMBtu reflects normalisation from historically weak 2024 pricing, while regional hubs such as Algonquin Citygate saw January 2025 averages reach $16.37/MMBtu, underscoring natural gas's price-sensitive but structurally indispensable role in U.S. thermal power fuel economics.

Coal represents the fastest-growing fuel type segment within the U.S. Thermal Power Market on a short-term basis, experiencing a cyclical generation resurgence driven by elevated natural gas prices, above-trend electricity load growth, and constrained CCGT fleet availability, even as its longer-term structural trajectory remains shaped by capacity retirements and regulatory pressure.

End-user Insights

The residential segment holds 38% of the U.S. Thermal Power Market’s end-use share, reflecting the broad and consistent reliance of U.S. households on natural gas and electricity for space heating, water heating, and cooling. The segment's dominance stems from the sheer scale and geographic dispersion of residential energy demand, which creates stable, recurring fuel consumption patterns across all seasons.

Natural gas has long served as the primary heating fuel for U.S. homes, and its seasonal demand sensitivity is well-documented: January 2024 residential and commercial sector consumption surged 12% year-over-year due to severe winter heating demand. A polar vortex event in late November–early December 2025 pushed prices above $5.00/MMBtu, with Algonquin Citygate averaging $16.37/MMBtu in January 2025, reflecting the magnitude of residential heating-driven demand spikes. These recurring seasonal patterns reinforce the residential segment's role as the largest and most consistent demand category within the U.S. Thermal Power Market.

The industrial segment is the fastest-growing end-use category in the U.S. Thermal Power Market, propelled by manufacturing activity, chemical processing, and the emergence of high-load industrial consumers, including AI-enabled data centres, steel production facilities, and large-scale processing plants. Industrial demand is characterised by its continuous baseload nature, making it uniquely dependent on dispatchable thermal generation rather than intermittent renewables.

Competitive Landscape

The U.S. Thermal Power Market exhibits a consolidated and oligopolistic structure, with a limited number of large utilities controlling a substantial share of generation capacity, particularly in natural gas and residual coal-based power plants. The market is dominated by vertically integrated players with strong regulated utility operations, long-term power purchase agreements, and diversified fuel portfolios, creating high entry barriers for new participants. Major companies such as Duke Energy Corporation, Southern Company, American Electric Power Company, Inc., Dominion Energy, Inc., and NextEra Energy, Inc. hold significant thermal generation assets across multiple states.

These companies benefit from economies of scale, strong transmission networks, and regulatory relationships that stabilise revenues while allowing gradual fleet modernisation and fuel transition strategies. Competitive dynamics are shaped by fuel price volatility, environmental compliance costs, and capacity market mechanisms rather than aggressive price competition. Although independent power producers operate in certain deregulated markets, their influence remains regionally concentrated compared to these dominant utilities.

Key Industry Developments:

- In Feb 2026 - NextEra Energy, Inc. announced the pricing of $2.0 billion in equity units, with potential proceeds rising to approximately $2.27 billion including over-allotments, to strengthen its capital base for energy and power project investments. The funds raised through NextEra Energy Capital Holdings, Inc., will support project financing and debt repayment, reinforcing balance sheet flexibility. This capital infusion is strategically relevant to the U.S. thermal power market as it enhances the company’s ability to invest in power generation assets, operational upgrades, and infrastructure modernisation. The structured equity-linked financing, maturing between 2031 and 2034, signals long-term capital commitment toward power sector expansion and asset optimisation.

- In Feb 2026 - NextEra Energy Transmission, LLC and Exelon Corporation welcomed the approval by the PJM Interconnection Board of Directors for a proposed ~220-mile, 765-kV transmission line aimed at strengthening grid reliability across West Virginia, Pennsylvania, and the Mid-Atlantic region. The project is strategically significant for the U.S. thermal power market as it enhances high-voltage transmission capacity, enabling improved dispatch of large-scale fossil-fuel power plants and supporting integration of new generation assets. By addressing rising electricity demand and regional supply constraints, the investment reinforces grid stability and facilitates continued operation and connectivity of thermal generation facilities.

Companies Covered in U.S. Thermal Power Market

- NextEra Energy, Inc.

- Dominion Energy, Inc.

- Duke Energy Corporation

- Southern Company

- American Electric Power Company Inc

- Exelon Corporation

- Xcel Energy Inc

- Public Service Enterprise Group Inc.

Frequently Asked Questions

The U.S. Thermal Power Market is projected to be valued at US$ 218.9 Bn in 2026.

The Natural Gas segment is expected to account for approximately 52% of the U.S. Thermal Power Market by Fuel Type in 2026.

The market is expected to witness a CAGR of 1.6% from 2026 to 2033.

The U.S. Thermal Power Market growth is driven by record natural gas consumption as the backbone of electricity generation, extreme weather-driven peak demand, and the strategic value of domestic thermal infrastructure amid geopolitical energy supply risks.

Key market opportunities in the U.S. Thermal Power Market include combined-cycle natural gas capacity for AI and industrial demand, vertical integration of natural gas supply for cost and fuel security, and grid modernization with high-voltage transmission to enhance dispatch efficiency and asset value.

Key players in the Thermal Power Market include Duke Energy Corporation, Southern Company, American Electric Power Company, Inc., Dominion Energy, Inc., and NextEra Energy, Inc.