- Inks, Coatings, Adhesives & Sealants (ICAS)

- Masking Tape Market

Masking Tape Market Size, Share, and Growth Forecast, 2026 - 2033

Masking Tape Market by Backing Material (Paper, Plastic, Fiberglass, Foil, Others), Adhesive Type (Silicone-based Adhesive, Acrylic-based Adhesive, Rubber-based Adhesive), End-use (Automotive, Building & Construction, Others), and Regional Analysis for 2026 - 2033

Masking Tape Market Size and Trends Analysis

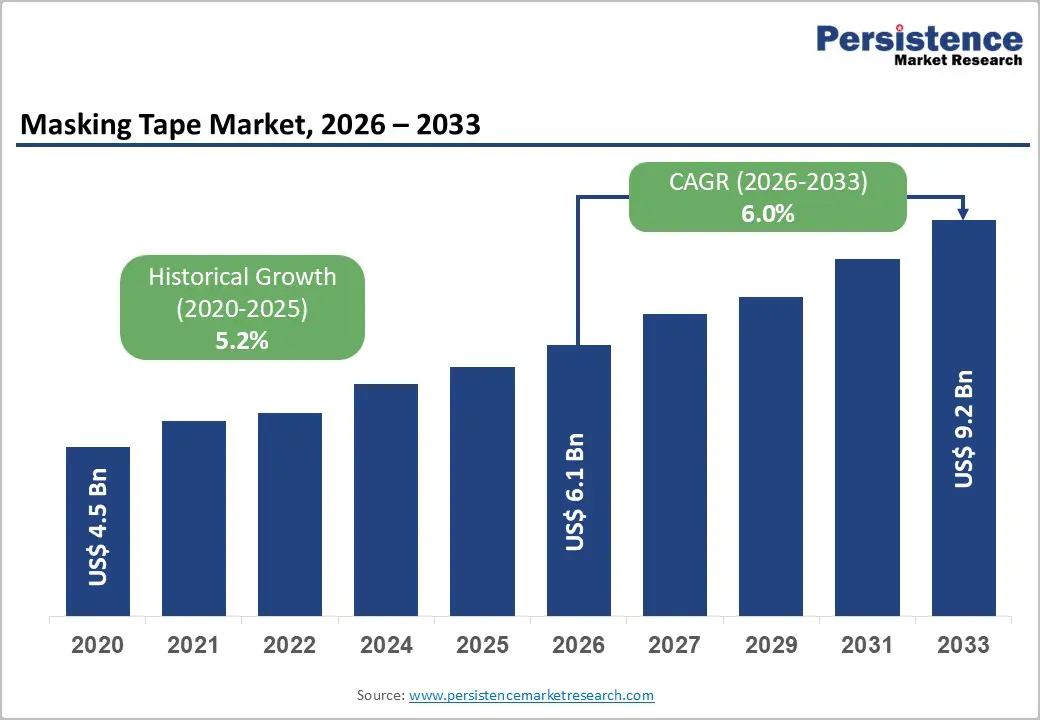

The global masking tape market size is likely to be valued at US$6.1 billion in 2026, and is expected to reach US$9.2 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by expanding automotive production, rapid infrastructure development, rising demand for precision painting and surface protection, increasing electronics manufacturing, and growing adoption in packaging and logistics applications.

Increasing recognition of masking tape as an essential, cost-effective solution for clean-edge masking, temporary bonding, and surface protection across industries remains a major driver of market growth in the masking tape market.

Key Industry Highlights:

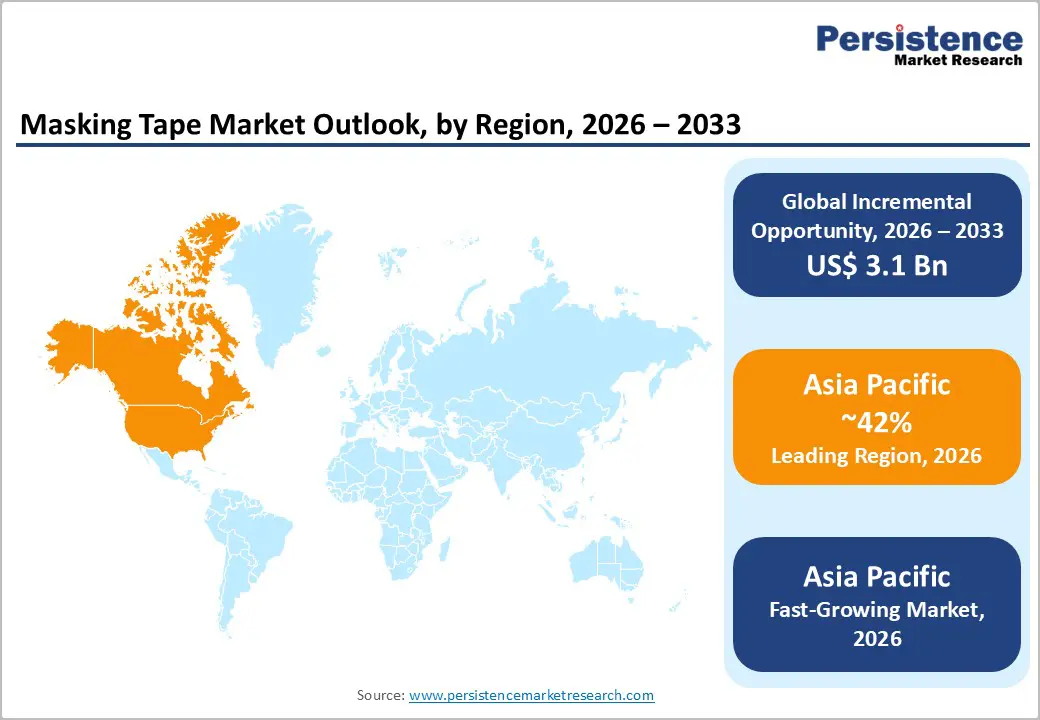

- Leading Region: Asia Pacific, anticipated to account for a 42% market share in 2026, driven by massive manufacturing output, construction boom, and automotive expansion in China and India.

- Fastest-growing Region: Asia Pacific, fueled by industrialization, urbanization, and rising FDI in automotive and electronics sectors.

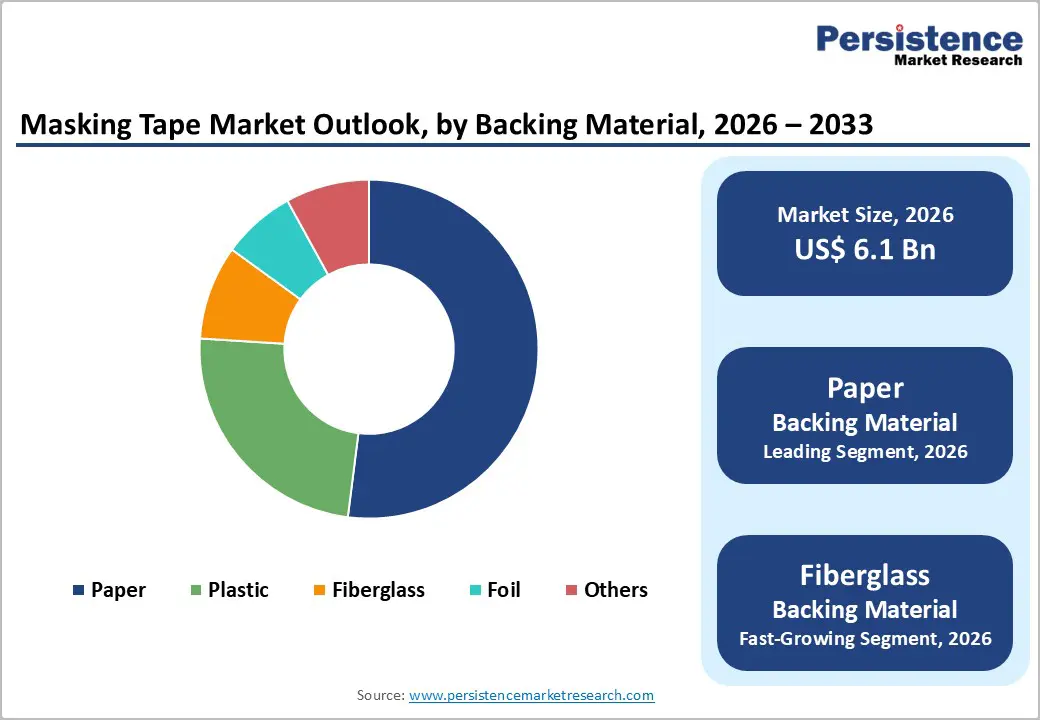

- Dominant Backing Material: Paper, to hold approximately 55% of the market share, due to its affordability, ease of use, and widespread availability.

- Leading End-use: Automotive, contributing nearly 28% of the market revenue, supported by high-volume vehicle assembly and refinishing needs.

| Key Insights | Details |

|---|---|

| Masking Tape Market Size (2026E) | US$6.1 Bn |

| Market Value Forecast (2033F) | US$9.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automotive & Construction Expansion in the Indian Auto Industry

Rapid expansion in automobile manufacturing significantly increases the demand for masking tapes. According to the Society of Indian Automobile Manufacturers, India produced more than 28 million vehicles in FY 2023-24, positioning the country among the world’s leading automotive producers and contributing notably to overall manufacturing output. Automotive assembly lines rely heavily on masking tape for paint masking, surface protection, and temporary component holding during fabrication, resulting in significant, consistent material consumption. High production volumes therefore lead to repeated use of specialized tapes across body shop operations and finishing processes, supporting stable industrial demand.

Expansion in the construction sector further drives demand for masking tape. The Indian construction industry’s gross value added (GVA) grew by around 9.4% in FY 2024-25, reflecting significant activity in infrastructure, housing, and commercial projects, where masking tape is used extensively for surface protection, precision painting, insulation masking, and joint sealing. This construction growth, backed by elevated capital expenditure and broad sectoral investment, ensures ongoing requirements for industrial tapes across preparatory and finishing works in building and infrastructure projects.

Rise of DIY/Home Improvement Trend

Homeowners taking on their own projects significantly increases demand for products like masking tape, particularly in surface protection and painting tasks. According to the U.S. Census Bureau’s American Housing Survey, 49 million homeowners made home improvements, and of 135 million total projects, 53 million were completed by homeowners themselves (“DIY”), not professionals. DIY projects often involve painting, surface refinishing, sealing, and small structural adjustments, where masking tape is a standard consumable. This direct engagement in home improvement means homeowners will buy more tools and materials to complete tasks independently, rather than subcontracting, expanding the overall market for basic supplies like masking tape used to protect surfaces and create clean finishes.

With a large share of improvements done personally, there is an ongoing need for consumable products that support these activities efficiently and affordably. Masking tape’s role in DIY projects extends across tasks such as wall painting, trim work, and temporary fixture holding, all common in homeowner-driven upgrades. The American Housing Survey data on DIY projects underscores a persistent consumer behavior trend: homeowners are actively maintaining and enhancing their properties themselves.

Barrier Analysis - Product Performance Limitations

Certain operational characteristics of masking tape limit its adoption in certain applications. Standard masking tapes can leave adhesive residue on surfaces after removal, reducing their suitability for high-precision tasks such as automotive finishing or electronics assembly. Paint bleed-through during use can compromise work quality, leading to increased waste and rework. These performance shortcomings restrict industrial buyers who require flawless finishes and reliability in demanding manufacturing environments. Users often need to select higher-end or specialized tapes, which increases costs and reduces the appeal of conventional masking tapes for budget-sensitive projects.

Environmental conditions also impact tape performance and limit market growth. Extreme temperatures, high humidity, or prolonged exposure to sunlight can cause tapes to lose adhesion or degrade prematurely. Weak adhesion on textured or uneven surfaces further constrains their effectiveness.

Intense Competition from Low-Cost Alternatives

The availability of low-cost alternatives to masking tape limits growth opportunities for established manufacturers. Budget-friendly tapes, often imported or produced by smaller regional players, attract price-sensitive buyers in construction, painting, and home improvement sectors. These products provide basic functionality at lower prices, reducing demand for premium or specialty masking tapes. Companies face pressure on profit margins and pricing strategies as end users prioritize cost over advanced performance features, which constrains revenue growth for higher-quality offerings.

Market fragmentation further intensifies competitive pressures. Numerous small-scale producers enter local markets with minimal marketing costs and competitive pricing, making it challenging for established brands to maintain market share. Differences in product quality create a perception among some buyers that all masking tapes are interchangeable, undermining brand loyalty.

Opportunity Analysis - High-Performance & Specialty Tapes

High-performance and specialty masking tapes present a significant opportunity for market expansion by aligning with the growth of technologically advanced manufacturing sectors. Industries such as electronics and semiconductor production increasingly require tapes with precise adhesion, heat resistance, and electrical insulation for component assembly and protection. India’s electronics production has grown rapidly from INR 1.9 lakh crore in 2014-15 to INR 11.3 lakh crore in 2024-25, reflecting a sixfold increase in output as domestic manufacturing scales up under supportive policies. This shift toward sophisticated devices such as smartphones, chips, and high-density printed circuit boards drives demand for specialty tapes capable of meeting strict performance criteria in automated and delicate assembly processes.

Growth in high-precision manufacturing opens demand beyond basic masking applications. Sectors such as automotive electronics, aerospace components, and advanced materials fabrication increasingly adopt specialty adhesives for bonding, insulation, and protection under demanding conditions where standard tapes fall short. As industrial production and exports rise, evidenced by targeted government initiatives to grow electronics manufacturing into a US$300 billion industry by FY26, advanced masking tape products that offer superior thermal stability, residue-free removal, and enhanced durability can capture higher-value applications and premium pricing.

Development of Eco-friendly & Sustainable Products

Traditional masking tape often uses petroleum-based adhesives and non-recyclable backing, which contribute to environmental pollution and waste. Manufacturers focusing on biodegradable, recyclable, and low-VOC (volatile organic compounds) tapes can cater to environmentally conscious consumers and industries seeking to reduce their ecological footprint. Sustainable masking tapes are increasingly preferred in sectors such as automotive, construction, and home improvement, where environmental standards and corporate social responsibility initiatives are becoming integral to operational decisions.

The adoption of eco-friendly masking tape also aligns with the global push for circular-economy practices. Businesses can enhance their brand reputation and meet regulatory requirements while offering functional products that perform comparably to conventional tapes. Innovations in bio-based adhesives, recycled paper backings, and solvent-free coatings enable masking tapes to retain adhesion, withstand heat, and provide residue-free removal, meeting both environmental and performance criteria.

Category-wise Analysis

Backing Insights

The paper backing material is anticipated to dominate, accounting for 55% market share in 2026, driven by its versatility, cost-effectiveness, and ease of use. Paper-backed tapes offer strong adhesion while remaining easy to tear by hand, making them suitable for both industrial and consumer applications such as painting, surface protection, and packaging. Their ability to provide clean removal without leaving residue enhances their appeal across sectors such as automotive, construction, and DIY projects. Tesa-Masking-Tape-Excellent - Painter's tape with a thin paper backing, ideal for clean paint masking in construction and renovation projects. Paper backing allows these tapes to balance strength with ease of handling, supporting widespread use across automotive, construction, and household painting tasks.

The fiberglass-backed segment is expected to be the fastest-growing, due to its superior strength, durability, and heat resistance. Unlike traditional paper-backed tapes, fiberglass tapes can withstand extreme temperatures and harsh environmental conditions, making them ideal for industrial applications such as automotive manufacturing, electrical insulation, aerospace, and high-temperature painting processes. Their reinforced structure prevents tearing, stretching, or deformation during use, ensuring consistent performance in demanding tasks. 3M™ Scotch® 361 Glass Cloth Tape, engineered with a woven fiberglass backing and silicone adhesive, withstands elevated temperatures and is used in automotive, aerospace, and industrial sealing applications, underscoring real industrial demand for fiberglass variants.

Adhesive Insights

Rubber-based adhesives are expected to dominate, accounting for over 52% of revenue in 2026, driven by their strong initial tack, excellent adhesion to a variety of surfaces, and cost-effectiveness. These tapes provide reliable bonding on metals, plastics, painted surfaces, and wood, making them suitable for industrial, automotive, construction, and DIY applications. The rubber adhesive ensures clean removal without leaving significant residue when used within recommended timeframes, enhancing user convenience and minimizing rework. 3M 201+ Masking Tape, 60 Yd, a widely used rubber-based adhesive masking tape from 3M with strong initial tack and clean removal, ideal for general paint masking and surface protection in automotive and construction applications.

Silicone-based adhesives are likely to be the fastest-growing, owing to their superior performance in demanding environments. Silicone adhesives maintain strong bonding even at extremely high or low temperatures, making them suitable for industrial applications such as electronics manufacturing, aerospace components, and powder-coating processes. These tapes provide excellent resistance to chemicals, moisture, and oxidation while maintaining flexibility and stability over long periods. 3M™ Polyimide Tape 8997, which uses a silicone pressure-sensitive adhesive designed for high-temperature industrial processes. This tape is widely used in electronics manufacturing, powder-coating lines, electroplating, and aerospace component masking, where materials must tolerate extreme heat and harsh chemicals. The silicone adhesive enables the tape to withstand temperatures up to about 260°C (500 °F) while maintaining strong adhesion and removing cleanly without residue after high-temperature curing cycles.

Regional Insights

North America Masking Tape Market Trends

North America's growth is driven by strong industrial activity, particularly in the automotive, construction, and aerospace sectors. In the region, masking tapes are widely used for surface protection, precision painting, and coating processes, where they help create clean paint lines and protect sensitive components during finishing operations. The United States dominates regional demand because of its large manufacturing base and extensive vehicle production and maintenance industry. Automotive repair centers and OEM manufacturers often use high-performance masking tape to protect parts during painting and refinishing.

Rising construction and renovation activity across the United States and Canada is driving increased use of masking tape for interior and exterior painting applications. The region also shows a growing shift toward specialty and high-temperature masking tapes that can withstand industrial paint-bake cycles and chemical exposure while still allowing residue-free removal. This trend reflects the increasing demand for efficiency and quality in industrial coating operations. According to the U.S. Department of Energy, modern vehicle production involves multiple painting and coating stages, during which protective masking materials are applied to shield components from paint overspray during manufacturing and refinishing processes.

Europe Masking Tape Market Trends

Europe's growth is influenced by strong manufacturing activity, strict environmental regulations, and increasing demand for high-precision painting and coating applications. Industries such as automotive manufacturing, construction, and industrial equipment production are major consumers of masking tapes in Europe. These tapes are widely used during painting and coating operations to protect surfaces, create sharp paint lines, and prevent overspray. European manufacturers emphasize high-quality finishing and surface protection, which drives the use of specialized masking tapes that maintain adhesion during heat curing and chemical exposure in industrial paint processes.

The European Commission’s Industrial Emissions Directive (IED) regulates emissions from industrial coating operations and requires manufacturers to reduce volatile organic compound (VOC) emissions during painting processes. To comply with these requirements, automotive plants in countries such as Germany and France have adopted advanced painting and coating technologies that rely on protective masking materials during multi-stage paint applications.

Asia Pacific Masking Tape Market Trends

Asia Pacific is projected to dominate and fastest growing, capturing the 42% share in 2026, propelled by increasing industrial production, large-scale infrastructure projects, and strong growth in automotive and electronics manufacturing across countries such as China, Japan, South Korea, and India. Masking tapes are widely used in industrial painting, surface protection, automotive refinishing, and construction finishing applications. Rapid urbanization and infrastructure development in the region have increased demand for paints and coatings, which in turn has driven increased consumption of masking tape used to protect surfaces and create clean paint lines during coating processes.

The growth of electronics manufacturing and precision engineering industries in countries such as Japan and South Korea has increased the demand for high-temperature and specialty masking tapes used in sensitive assembly processes. Rising vehicle production and expanding automotive repair services also contribute to market expansion, as masking tapes are essential during multi-stage vehicle painting and coating operations.

Competitive Landscape

The global masking tape market is characterized by strong competition between multinational corporations and numerous regional manufacturers. Large companies focus on continuous product innovation, developing advanced masking tapes that offer better temperature resistance, clean removal, and improved adhesion for demanding industrial applications such as automotive painting, electronics assembly, and aerospace coating. At the same time, manufacturers are investing in sustainable and eco-friendly adhesive formulations, including low-VOC and recyclable materials, to meet evolving environmental standards and customer preferences.

Strategy involves optimizing supply chains and production efficiency to manage costs in a price-sensitive market where bulk industrial buyers seek reliable yet affordable solutions. Regional manufacturers often compete by offering cost-effective products tailored to local industries such as construction, packaging, and automotive refinishing. Companies are also expanding manufacturing and distribution networks in fast-growing Asia Pacific markets, where rapid industrialization and infrastructure development drive demand.

Key Industry Developments

- In January 2025, Mitsui Chemicals ICT Materia, Inc. developed a new surface protective tape using a water-based acrylic adhesive in September 2024 for fiber laser cutting applications. The company stated that it would begin mass production in April 2025 as part of its Mitsui Masking Tape™ product lineup.

- In February 2024, Rogers Corporation announced the availability of DeWAL® Plasma X™ tape, the thinnest single-ply masking tape in its DeWAL® thermal spray masking tape product family. The company designed the tape using a silicone rubber and glass cloth laminate construction combined with an aggressive high-temperature silicone adhesive to enhance performance in demanding industrial environments.

Companies Covered in Masking Tape Market

- 3M

- Nitto Denko Corporation

- tesa SE

- Intertape Polymer Group Inc.

- PPM Industries SpA

- Shurtape Technologies, LLC

- PPI Adhesive Products

- Saint-Gobain

- Avery Dennison Corporation

- Sicad Group

- Berry Global Inc.

- Cintas Adhesivas Ubis SA

- Scapa Group Ltd

- Advance Tapes International

Frequently Asked Questions

The global masking tape market is projected to reach US$6.1 billion in 2026, reflecting steady demand from automotive painting, construction, and electronics manufacturing sectors.

Key drivers include surging automotive production, global infrastructure and construction activity, booming electronics, EV manufacturing, and the rising need for precision surface protection and packaging solutions.

The masking tape market is poised to witness a CAGR of 6.0% from 2026 to 2033.

Opportunities lie in high-temperature silicone and fiberglass tapes for EV batteries and aerospace, sustainable/recyclable paper-based variants for green construction, and expansion in Asia Pacific logistics and electronics sectors.

Leading players include 3M, Nitto Denko Corporation, tesa SE, Intertape Polymer Group, Shurtape Technologies, Avery Dennison, Saint-Gobain, and Berry Global.