- Non-food Packaging

- Flatback Tape Market

Flatback Tape Market Size, Share, and Growth Forecast, 2026 - 2033

Flatback Tape Market by Product Type (Single-Sided, Double-Sided), Material Type (Paper-Based, Plastic-Based), Adhesive Type (Water-Based Adhesives, Synthetic/Rubber Adhesives), Application (Electronics, Packaging and Sealing, Others), and Regional Analysis 2026 - 2033

Flatback Tape Market Size and Trends Analysis

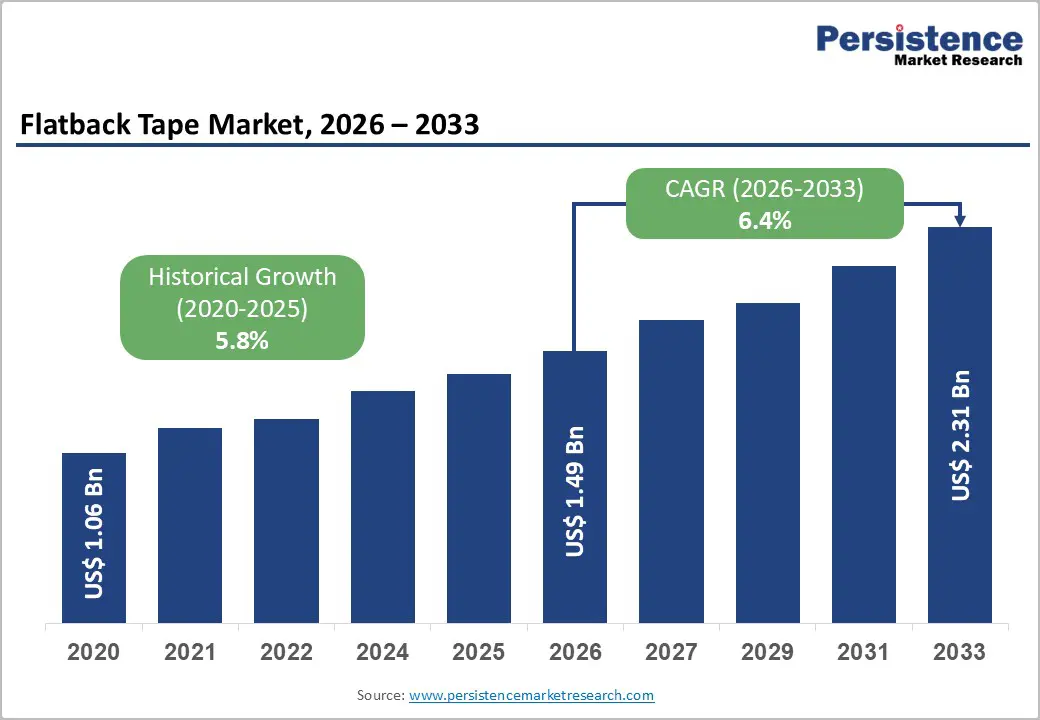

The global flatback tape market size is likely to be valued at US$1.49 billion in 2026 and is expected to reach US$2.31 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by a profound regulatory shift toward sustainable packaging solutions and an exponential rise in global e-commerce volumes.

Unprecedented advancements in eco-friendly water-based adhesives and curbside-recyclable paper backings are directly addressing corporate carbon-neutral mandates. Consequently, enterprise procurement is increasingly shifting from conventional plastic-based tapes toward heavy-duty, performance-grade flatback formats that seamlessly integrate with high-speed automated carton sealing machinery without compromising environmental compliance. Sustainability shifts favor paper-based variants, while adhesive innovations support high-performance uses.

Key Industry Highlights:

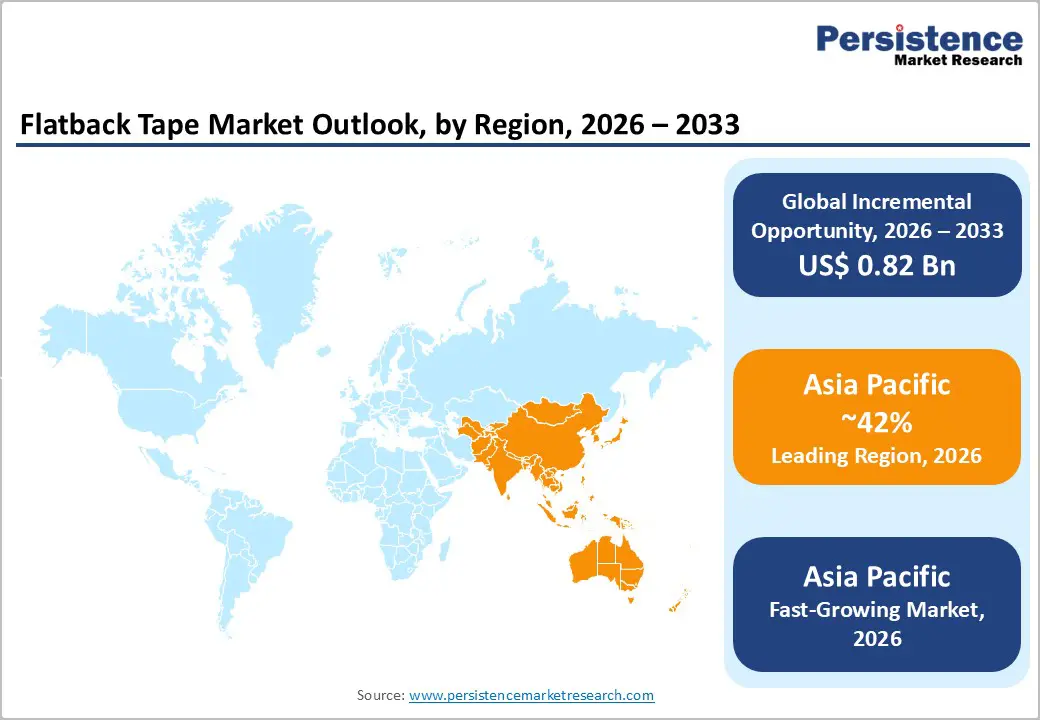

- Leading Region: Asia Pacific is projected to lead due to large-scale electronics manufacturing, automotive production intensity, and export-oriented packaging ecosystems, accounting for approximately 42% share in 2026, supported by rapid automation adoption and integrated raw material supply advantages.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to accelerating industrialization, supportive trade frameworks such as regional tariff alignment, and rising adoption across e-commerce, semiconductor, and electric vehicle sectors.

- Leading Material Type: Paper-based material type is expected to lead, accounting for approximately 63% share in 2026, through widespread industrial adoption, high packaging throughput compatibility, superior tear resistance, and expanding high-value recyclable applications.

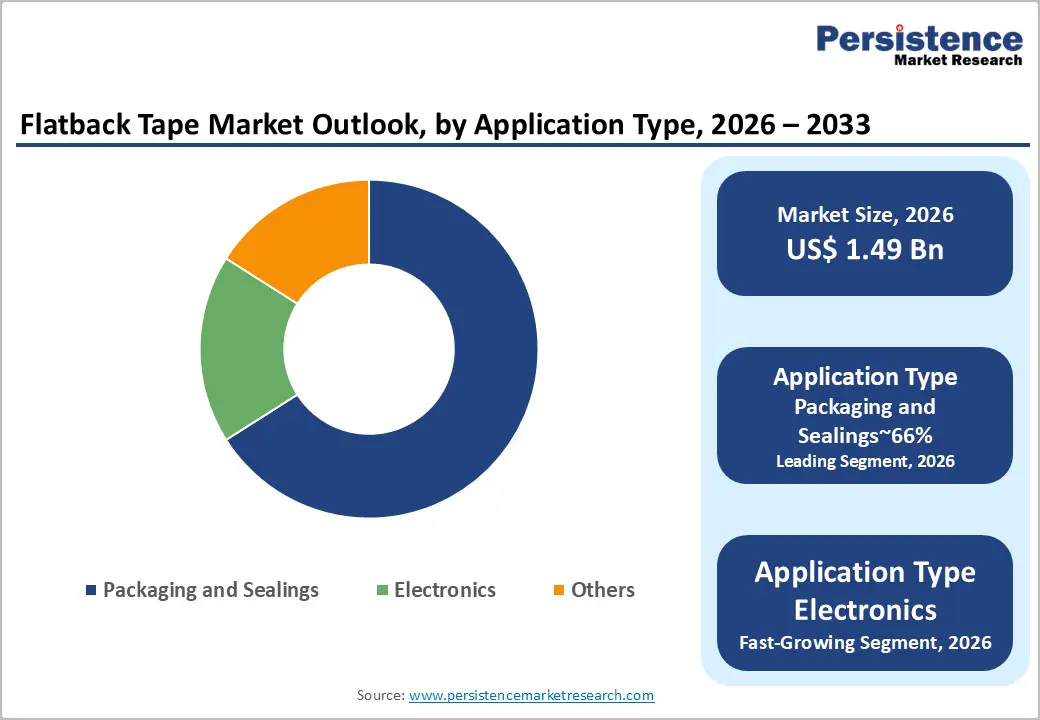

- Leading Application Segment: Packaging and sealing applications are projected to dominate for operational simplicity, cost-efficiency in carton closure, universal industrial adoption, and functional compatibility across logistics-intensive sectors, holding approximately 66% share in 2026.

| Key Insights | Details |

|---|---|

| Flatback Tape Market Size (2026E) | US$1.49 Bn |

| Market Value Forecast (2033F) | US$2.31 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Acceleration of E-Commerce Fulfillment and Automated Packaging Infrastructure

The rapid expansion of global e-commerce networks is intensifying demand for industrial-grade packaging materials. Parcel volumes are rising as digital marketplaces expand cross-border distribution capabilities. Third-party logistics operators are scaling high-throughput fulfillment centers to manage growing shipment complexity. Automated case sealing systems require tapes engineered for tensile integrity and consistent adhesion. Flatback tapes demonstrate strong compatibility with high-speed applicators and robotic packaging arms. Their cross-directional strength reduces breakage risks during continuous automated dispensing cycles. Reduced tape snapping lowers machine stoppages and improves packaging line productivity. Operational efficiency pressures are therefore accelerating procurement standardization toward performance-grade flatback variants.

Automation-led packaging environments are reshaping material specifications across logistics-intensive industries. Quick-stick adhesive systems support rapid carton closure under compressed cycle times. Water-based and synthetic adhesive formulations are optimized for corrugated substrates and temperature variability. Regulatory emphasis on secure transit packaging further elevates demand for durable sealing solutions. Higher throughput conditions increase tape consumption intensity across distribution hubs. Stable unwind properties minimize calibration disruptions within automated machinery. These functional attributes collectively strengthen flatback tape positioning within high-volume parcel ecosystems.

Expanding Electronics and Automotive Splicing Applications

Rising electronics manufacturing intensity is strengthening the demand for specialized splicing materials. Semiconductor output growth is increasing reliance on precision assembly processes. Flatback tapes engineered for elevated thermal resistance support circuit board mounting operations. High-temperature variants maintain adhesion integrity under sustained heat exposure conditions. Rubber-based adhesive systems provide rapid tack and dependable substrate bonding performance. These properties are critical during film processing and automated component placement cycles. Automotive electrification trends further expand requirements for stable insulation and masking solutions. Splicing reliability, therefore, becomes integral to uninterrupted electronics and mobility production workflows.

Transition toward electric vehicle architectures amplifies demand for recyclable and compliant materials. Manufacturers are aligning adhesive systems with evolving environmental and waste management mandates. Regulatory scrutiny encourages integration of recyclable substrates within industrial consumables portfolios. Thermal durability and mechanical stability reduce rework rates in battery module assembly. Industrial procurement teams prioritize materials, ensuring minimal downtime during high-speed production. Adhesive chemistry innovation is increasingly tied to sustainability certification pathways. Supply resilience in the semiconductor and mobility sectors reinforces consistent tape utilization patterns. These structural shifts collectively enhance the industrial relevance of advanced flatback splicing tapes.

Barrier Analysis – Competitive Pressure from Low-Cost Plastic Tape Alternatives

Standard flatback tapes encounter sustained competitive intensity from conventional plastic-based sealing solutions. Biaxially oriented polypropylene and polyvinyl chloride tapes maintain entrenched positions in legacy packaging systems. Their established conversion infrastructure supports a consistent supply across fragmented distribution networks. Lower production costs enable aggressive pricing strategies in highly price-sensitive regions. Procurement teams frequently prioritize immediate budget containment over environmental transition objectives. This purchasing behavior limits substitution momentum despite rising sustainability narratives. Plastic tapes also benefit from strong moisture resistance and long shelf stability. These attributes collectively constrain flatback tape penetration within cost-driven emerging markets.

Premium-grade flatback tapes typically command higher pricing due to paper substrates and adhesive formulations. Elevated input and coating costs restrict margin flexibility for competitive discounting. Developing economies often lack regulatory enforcement mechanisms supporting sustainable material migration. Infrastructure for recyclable packaging segregation remains uneven across industrial corridors. Buyers with short planning horizons delay adoption of higher-value paper-based alternatives. Established supplier relationships further reinforce inertia within conventional tape procurement cycles. This competitive asymmetry slows structural demand reallocation toward fiber-based sealing formats. Consequently, substitution dynamics remain gradual despite broader environmental policy discourse.

Volatility in Upstream Raw Material Pricing

Profitability within the flatback tape market remains exposed to raw material price instability. Production depends heavily on natural kraft paper and synthetic rubber derivatives. Acrylic polymer inputs further intensify exposure to petrochemical cost fluctuations. Global pulp market volatility transmits directly into substrate procurement expenses. Geopolitical disruptions and logistics bottlenecks amplify supply unpredictability across sourcing corridors. Adhesive resin price swings create uneven cost absorption across converter operations. Sudden input escalation compresses gross margins within contract-bound industrial supply agreements. These structural pressures complicate pricing stability across packaging and electronics end-use sectors.

Mid-sized manufacturers face limited bargaining leverage in long-term procurement negotiations. Absence of hedging flexibility heightens vulnerability to cyclical commodity swings. Cost pass-through mechanisms often lag procurement price escalation timelines. Downstream customers resist abrupt price revisions amid competitive packaging markets. Margin compression constrains reinvestment capacity in process automation and coating technologies. Working capital cycles elongate as inventory valuation fluctuates unpredictably. Regulatory sustainability transitions may further alter fiber and polymer sourcing economics. Persistent input volatility, therefore, restricts predictable profitability across the flatback tape production ecosystem.

Opportunity Analysis – Digital Supply Chain Integration and Traceable Packaging Systems

Integration of blockchain-enabled tracking mechanisms is expanding the functional scope within industrial tapes. Traceability requirements are intensifying across food, pharmaceutical, and high-value retail logistics. Digitally authenticated tapes can embed batch-level verification within packaging workflows. This capability supports anti-counterfeit compliance and improves audit transparency across distribution channels. Rapid expansion of e-grocery platforms increases reliance on moisture-resistant sealing materials. Temperature variability during last-mile delivery heightens performance expectations for adhesive durability. Smart labeling convergence enables interaction between physical sealing and digital monitoring systems.

Policy frameworks promoting domestic manufacturing strengthen localized tape production capabilities. Incentive schemes encourage investment in advanced coating, slitting, and adhesive compounding facilities. Domestic capacity expansion reduces import dependence for specialty performance variants. Moisture-resistant and digitally trackable formats align with evolving food safety regulations. Integrated data visibility enhances inventory governance and recall management efficiency. Procurement contracts increasingly incorporate compliance-linked digital authentication requirements. Traceable packaging components, therefore, become embedded within broader digital supply infrastructures. This convergence of policy support and logistics digitization expands strategic opportunity for technologically enhanced flatback tapes.

Commercialization of Fully Curbside Recyclable Flatback Tape Innovations

Advancements in adhesive chemistry are enabling the development of fully curbside recyclable flatback tapes. Novel formulations allow tapes to remain attached during hydrapulping without contaminating fiber streams. This compatibility aligns sealing materials with circular packaging recovery frameworks. Retailers are intensifying scrutiny of secondary plastic components within shipping cartons. Zero-residue performance reduces manual tape removal requirements during recycling operations. Regulatory pressure on plastic reduction strengthens demand for fiber-compatible sealing systems. FDA-compliant adhesive systems expand applicability across food and regulated packaging categories. These technological shifts position recyclable flatback tapes as a differentiated, sustainability-driven growth avenue.

Commercial-scale adoption could reshape procurement standards across multinational retail networks. Large distributors increasingly embed recyclability criteria within supplier qualification processes. Patented repulpable technologies offer defensible intellectual property advantages in competitive tenders. Integration with existing carton substrates simplifies transition without altering packaging formats. Recycling facility acceptance enhances brand credibility within extended producer responsibility regimes. Higher specification products may command premium pricing supported by compliance alignment. Margin structures could improve through value-based contracting rather than volume discounting. This innovation trajectory strengthens long-term strategic positioning within sustainable packaging ecosystems.

Category–wise Analysis

Material Type Insights

The paper-based segment is expected to lead, accounting for approximately 63% share in 2026, supported by entrenched recyclability advantages and broad industrial qualification across packaging and splicing workflows. Kraft-backed constructions deliver high tensile integrity, controlled unwind, and hand-tearability suited for automated case sealers and robotic dispensers. Utility-grade variants sustain high-volume carton sealing, while printable surfaces enable branded and tamper-evident applications. Sustainability-driven procurement shifts away from plastic films, further reinforcing substrate preference in e-commerce logistics. Leading suppliers such as 3M Company, Shurtape Technologies, tesa SE, and Intertape Polymer Group anchor enterprise adoption through performance flatback portfolios and recyclable kraft innovations.

The paper-based segment is also expected to be the fastest-growing segment, propelled by accelerating circular economy mandates and migration toward plastic-free sealing formats across retail and industrial channels. Advancements in pressure-sensitive adhesive chemistries enable performance parity with filmic tapes under demanding thermal and humidity conditions. Integration of bio-based polymers and water-based coatings improves environmental compliance while maintaining bond strength. Smart tape developments incorporating IoT-enabled traceability and digital print customization expand functional scope beyond basic sealing. Companies, including 3M Company, Avery Dennison, Shurtape Technologies, and Intertape Polymer Group, are introducing recyclable and renewable-content platforms to capture early-cycle demand.

Application Insights

The packaging and sealing segment is expected to lead, accounting for approximately 66% share in 2026, anchored by its universal role in carton closure across global freight and direct-to-consumer distribution models. High tensile strength, fiber-tear tamper evidence, and writable paper surfaces reinforce its suitability for corrugated substrates. Machine-length rolls engineered for controlled unwind support robotic case sealers and high-throughput fulfillment centers. Temperature stability across cold-chain and tropical warehousing conditions sustains performance reliability versus filmic alternatives. Intertape Polymer Group, 3M Company, Nitto Denko, and Vibac Group maintain strong positioning through medium-to-heavy duty packaging portfolios and printable flatback platforms.

Electronics is expected to be the fastest-growing segment, driven by escalating requirements for high-temperature splicing, precision masking, and residue-free debonding within semiconductor and electric vehicle manufacturing lines. Miniaturization of circuit architectures increases demand for dimensionally stable, clean-cut paper backings compatible with automated assembly. Advanced acrylic and synthetic rubber systems withstand solder reflow cycles without outgassing or adhesive transfer. Nitto Denko, 3M, tesa SE, and Avery Dennison Performance Tapes are expanding thermal management and battery insulation portfolios to capture this demand. Automation intensity and cleanroom qualification pathways position electronics as a high-margin acceleration vector.

Regional Insights

Asia Pacific Flatback Tape Market Trends

Asia Pacific is projected to stand as the leading and fastest-growing region, commanding a 42% global share in 2026. The region functions as the world’s primary manufacturing base, supported by large-scale electronics assembly, automotive production, and export-oriented packaging ecosystems. China anchors high-volume output, while Japan reinforces premium quality manufacturing, and India accelerates industrial capacity expansion under production-linked incentives. Trade facilitation through the Regional Comprehensive Economic Partnership lowers intra-regional tariff barriers, strengthening adhesive material supply chains. Rapid automation across packaging and semiconductor facilities increases demand for machine-grade and high-temperature masking tapes.

China remains the structural demand center due to EV battery scaling and advanced electronics exports, generating sustained consumption of flame-retardant and ultra-thin splicing variants. India’s enforcement of single-use plastic restrictions further shifts retail packaging toward recyclable kraft flatback tapes. Regional leaders such as Nitto Denko Corporation, Sekisui Chemical, Avery Dennison, and 3M continue expanding localized coating lines and automation-ready jumbo rolls to support high-velocity fulfillment networks. Investment flows into Southeast Asia under the “China Plus One” strategy are redistributing production footprints while preserving Asia Pacific’s structural dominance in global flatback tape manufacturing and consumption.

North America Flatback Tape Market Trends

North America is expected to remain a mature and structurally stable market, supported by advanced manufacturing infrastructure and strict environmental compliance alignment across packaging and industrial tape ecosystems. Demand is projected to remain anchored in replacement cycles, automation upgrades, and sustainability-driven product reformulation rather than greenfield capacity expansion. The region’s sophisticated e-commerce and third-party logistics architecture is positioned to sustain high utilization of machine-grade flatback tapes compatible with robotic dispensers and high-speed sorting systems. Regulatory oversight from the EPA and evolving TSCA evaluations are expected to reinforce the transition toward water-based, low-VOC adhesive chemistries, reshaping formulation standards.

The U.S. is expected to anchor regional momentum, shaping procurement standards through its scale in aerospace, electronics reshoring, and direct-to-consumer logistics networks. Domestic investment in precision coating lines and high-tensile specialty formats is projected to elevate performance benchmarks for industrial masking and composite bonding applications. Federal climate disclosure frameworks are anticipated to intensify demand for verified low-carbon and bio-based tape substrates, influencing supplier qualification processes. USMCA content rules are likely to reinforce regional sourcing strategies across automotive supply chains, favoring North American producers. As labor costs remain elevated, automation-compatible flatback systems are positioned to sustain steady lifecycle-driven demand.

Europe Flatback Tape Market Trends

Europe represents a highly regulated market shaped by unified sustainability mandates and innovation in paper-based adhesive technologies. The region operates under binding climate alignment frameworks such as the European Green Deal, which structurally prioritizes recyclable, plastic-free, and low-emission adhesive technologies. Regulatory harmonization under the European Commission accelerates the adoption of paper-based flatback tapes across industrial and retail supply chains. Stringent implementation of the EU Packaging and Packaging Waste Regulation materially restricts composite packaging formats, reinforcing substitution toward mono-material paper systems. High energy costs and carbon accountability standards further incentivize solvent-free, UV-curing, and bio-polymer adhesive production processes.

Germany anchors regional industrial demand due to its advanced automotive and aerospace manufacturing base, where precision masking and high-thermal flatback tapes are operationally critical. Compliance shifts under European Chemicals Agency PFAS proposals are accelerating reformulation toward fluorine-free release systems across most European portfolios. Mandatory FSC and PEFC alignment under the EU Deforestation Regulation reinforces certified fiber sourcing as a procurement prerequisite. Leading manufacturers, including Tesa SE, Lohmann GmbH & Co. KG, Scapa Group, and Monta Klebebandwerk, continue expanding bio-based adhesive research and certified sustainable production capacity to maintain competitive positioning within Europe’s compliance-driven ecosystem.

Competitive Landscape

The global flatback tape market reflects a moderately consolidated competitive structure, where scale advantages and vertical integration remain decisive strategic levers. The top three suppliers, including 3M, Intertape Polymer Group, and Berry Global, collectively account for roughly one-fifth of global revenue, while the broader Tier 1 cohort captures close to two-fifths of market share. Consolidation at the upper tier is reinforced by economies of scale in kraft paper sourcing, in-house adhesive formulation, and high-speed coating infrastructure, which buffer margin volatility amid raw material cost fluctuations.

Beyond the leading group, the market remains structurally fragmented, with Tier 3 converters representing a meaningful niche-focused segment emphasizing eco-certified and application-specific variants. Industry dynamics increasingly center on sustainability validation, selective acquisitions of specialty adhesive formulators, and automation-compatible product portfolios, indicating a forward trajectory defined by regulatory alignment, technical differentiation, and supply chain resilience rather than pure volume expansion.

Key Industry Developments:

- In February 2026, Intertape Polymer Group (IPG) launched an upgraded IPG Hub digital platform with advanced tape monitoring features. Allows real-time tracking of tape usage and efficiency, significantly reducing downtime in automated packaging operations.

- In April 2025, 3M Company released a comprehensive 2026 Technical Update for the 2526 Textile Flatback Tape. Enhanced moisture resistance and holding power for synthetic fibers, optimizing high-speed textile manufacturing lines.

Companies Covered in Flatback Tape Market

- 3M Company

- Intertape Polymer Group

- Berry Global Inc.

- tesa SE

- Nitto Denko Corporation

- Shurtape Technologies LLC

- Sekisui Chemical Co., Ltd.

- Scapa Group plc

- Saint-Gobain

- Avery Dennison Corporation

- Vibac Group

- Atlas Tapes S.A.

- Ahlstrom

- PPM Industries S.p.A.

- Pro Tapes & Specialties

- Shanghai Yongguan Adhesive Products Corp.

Frequently Asked Questions

The global flatback tape market is projected to be valued at US$1.49 billion in 2026 and is expected to reach US$2.31 billion by 2033, supported by expanding e-commerce logistics, automation-led packaging infrastructure, and increasing substitution of plastic tapes with recyclable paper-based alternatives.

The rapid expansion of automated fulfillment centers and robotic case sealing systems is accelerating demand for high-tensile, machine-grade flatback tapes. These tapes offer controlled unwind, strong cross-directional strength, and stable adhesion under high-speed dispensing conditions, reducing downtime and improving operational efficiency in large-scale logistics networks.

The global flatback tape market is forecast to grow at a CAGR of 6.4% from 2026 to 2033, reflecting steady demand from packaging, electronics splicing, and sustainability-driven procurement transitions.

Asia Pacific is the leading regional market, accounting for approximately 42% share in 2026, driven by large-scale electronics manufacturing, expanding automotive production, strong export-oriented packaging activity, and rising domestic e-commerce consumption across China, Japan, and India.

The market is moderately consolidated, with key players including 3M Company, Intertape Polymer Group, Berry Global Inc., tesa SE, Nitto Denko Corporation, Shurtape Technologies LLC, Sekisui Chemical Co., Ltd., Scapa Group plc, Saint-Gobain, Avery Dennison Corporation, Vibac Group, Atlas Tapes S.A., Ahlstrom, PPM Industries S.p.A., Pro Tapes & Specialties, and Shanghai Yongguan Adhesive Products Corp.