- Smart Packaging

- Splicing Tape Market

Splicing Tape Market Size, Share, and Growth Forecast, 2026 - 2033

Splicing Tape Market by Product Type (Double-Sided Tape, Repulpable Tape, Others), Resin Type (Acrylic, Silicone, Others), Backing Material, Application, and Regional Analysis for 2026 - 2033

Splicing Tape Market Size and Trends Analysis

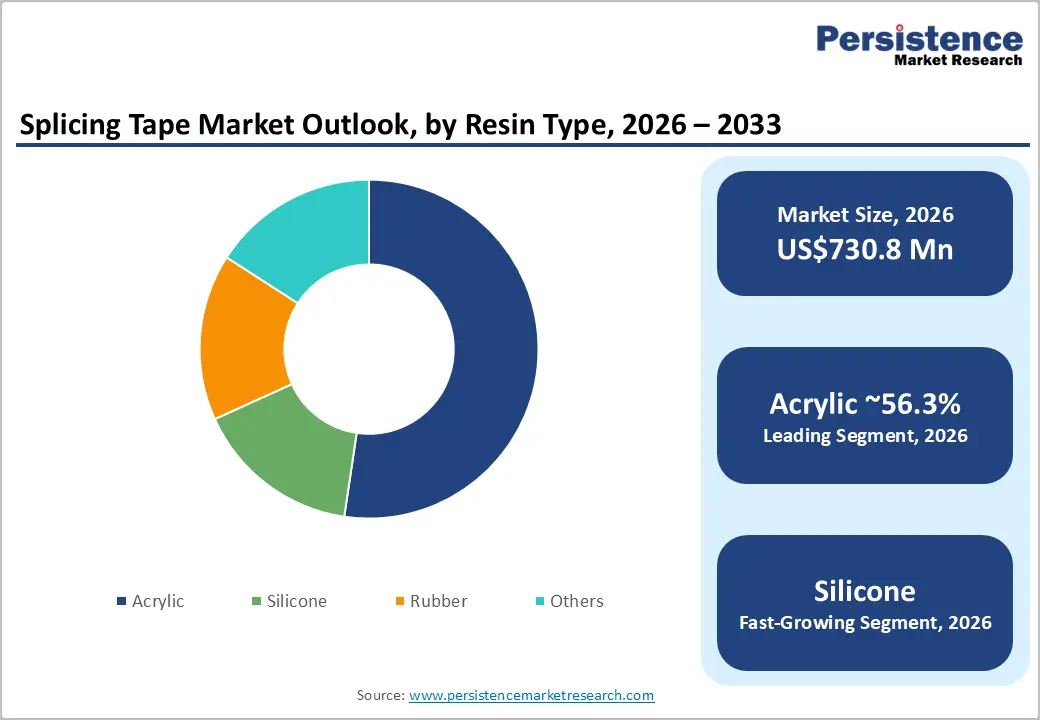

The global splicing tape market size is likely to be valued at US$730.8 million in 2026 and is expected to reach US$1,014.7 million by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by expanding automation across paper, printing, and packaging operations, along with rising demand for high-speed converting systems that require reliable, zero-stop splicing solutions.

Material innovation, particularly in repulpable and silicone-adhesive variants, is enabling higher productivity and lower waste rates. Asia-Pacific holds the largest share and is the fastest-growing regional market, driven by manufacturing expansion in China, India, Japan, and the ASEAN economies. The competitive landscape remains moderately concentrated, with global adhesive manufacturers and regional converters shaping product development and pricing dynamics.

Key Industry Highlights:

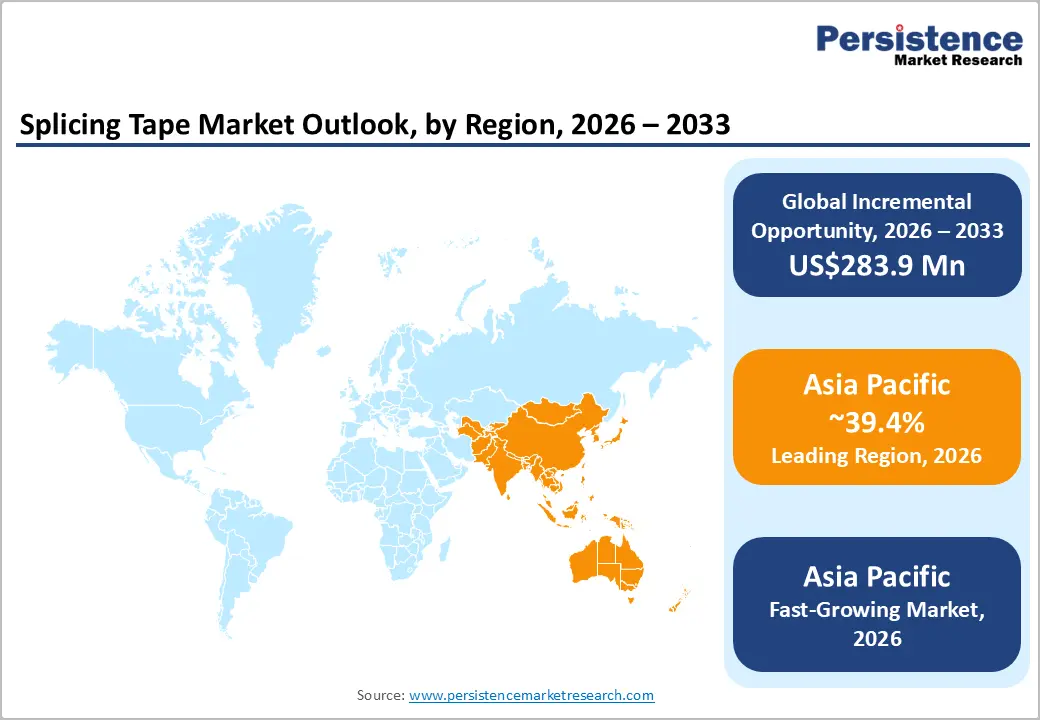

- Leading Region: Asia-Pacific is projected to account for over 39.4% of the market, supported by large-scale paper, packaging, and electronics manufacturing across China, Japan, India, and ASEAN.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, due to expanding converting capacity and e-commerce-driven packaging demand.

- Investment Plans: Manufacturers are investing in localized adhesive coating lines, repulpable product development, and silicone-based high-performance formulations, particularly in North America and the Asia Pacific, to strengthen supply resilience and technical support capabilities.

- Dominant Product Type: Double-sided splicing tape leads the product type segment with a 60.8% market share, driven by its widespread use in flying splices, roll changes, and automated converting systems.

- Leading Resin Type: Acrylic adhesives dominate the resin segment with an estimated 56.3% share, owing to their balanced adhesion strength, durability, cost efficiency, and compatibility with paper and packaging applications.

| Key Insights | Details |

|---|---|

| Splicing Tape Market Size (2026E) | US$730.8 Mn |

| Market Value Forecast (2033F) | US$1,014.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Industrial Automation and High-Speed Converting Expansion

The modernization of paper mills, corrugated plants, label converters, and flexible packaging facilities is accelerating demand for advanced splicing solutions. High-speed web-handling systems and flying-splice equipment require tapes capable of rapid adhesion, high tensile strength, and consistent performance at elevated speeds. As conversion lines increasingly exceed several hundred meters per minute, reducing downtime becomes a financial priority. Splicing tapes enables continuous production during roll changes, reducing waste and improving operational efficiency. This shift favors double-sided and performance-engineered splicing tapes, particularly those designed for automated splicing heads. Higher line speeds increase the technical requirements of tapes, supporting premium-grade adoption and higher average selling prices (ASPs). Even when volume growth is moderate, value expansion occurs through product-mix upgrades toward specialty grades.

Sustainability and Recyclability Requirements

Environmental regulations and brand-owner commitments to circular packaging are reshaping material selection across the paper and packaging industries. Since paper & printing applications account for a significant portion of splicing tape consumption, the need for recyclable and pulp-compatible materials directly influences purchasing decisions. Repulpable splicing tapes, which use water-soluble adhesives and tissue-based backings, are designed to disintegrate during pulping without contaminating recycled fiber streams. Mills increasingly require certification or documented recyclability testing before approving materials. As sustainability criteria become embedded into procurement frameworks, demand is shifting toward premium, environmentally compliant adhesive systems. This dynamic increases R&D investments and supports pricing power for manufacturers offering validated repulpable solutions.

Resin and Material Innovation Enabling New Applications

Advancements in adhesive chemistry and backing materials are expanding the technical scope of splicing tapes. Silicone adhesives, engineered nonwovens, and ultrathin PET backings enable reliable splicing on low-surface-energy substrates and on high-temperature production lines. These capabilities are particularly relevant in release liner manufacturing, specialty films, flexible electronics, and advanced packaging. As converters diversify substrate portfolios, splicing tapes must accommodate higher temperatures, aggressive coatings, and demanding unwind conditions. Silicone-based formulations provide enhanced thermal stability and release properties compared to conventional acrylic systems. This innovation broadens the addressable market beyond traditional paper operations, increasing penetration in specialty manufacturing and electronics sectors while supporting premium pricing.

Barrier Analysis - Raw Material Cost Volatility

Splicing tape production relies on pulp, acrylic polymers, silicone resins, rubber adhesives, and carrier films such as PET and tissue. Price fluctuations in petrochemical feedstocks and pulp markets can materially affect manufacturing costs. Periods of polymer inflation have historically led to gross margin compression for adhesive producers, particularly when raw material prices rise sharply over short timeframes. Smaller converters often lack pricing leverage to pass through cost increases immediately. This volatility constrains profitability and may slow the adoption of higher-cost specialty tapes unless converters clearly demonstrate total cost-of-ownership advantages through productivity gains.

Fragmented Distribution and Conversion Landscape

While global adhesive manufacturers dominate premium segments, numerous regional converters and distributors operate in localized markets. This fragmentation increases the complexity of procurement for multinational converters seeking standardized performance specifications. Moderate market concentration limits the effectiveness of universal pricing control, particularly for commodity-grade tapes. Engineering teams may encounter switching barriers when transitioning between suppliers, owing to equipment compatibility and process validation requirements. Cross-border procurement adds further complexity, especially where local testing standards differ.

Opportunity Analysis - Retrofit and Upgrade Programs in Mature Markets

Paper mills and packaging converters in North America and Europe are allocating capital to retrofit aging production lines with automated splicing systems. Adding flying-splice capability reduces downtime and improves yield efficiency. These upgrades require compatible high-performance splicing tapes engineered for automated application. Premium double-sided, repulpable, and silicone-based tapes benefit directly from modernization programs. Suppliers can enhance revenue capture by bundling technical training, splicing kits, and on-site validation services. This integrated offering strengthens customer retention and increases lifetime value beyond product-only sales.

Asia Pacific Manufacturing Expansion

Asia-Pacific’s manufacturing scale in paper, packaging, electronics, and release liner production positions it as the largest and fastest-growing splicing tape market. As regional production capacity expands, tape consumption increases proportionally. Localizing production or establishing converting centers within APAC improves supply reliability and reduces lead times. Partnerships with regional converters accelerate product certification and technical adoption. Given its share exceeding 39.4%, APAC is expected to account for the majority of absolute value growth through 2033.

Electronics and Specialty Film Applications

The rapid development of flexible electronics, specialty films, and advanced release liners creates demand for precision splicing tapes capable of operating under tight tolerances. Silicone adhesives and PET backings are particularly well-suited to these environments. As electronics manufacturing migrates toward thinner substrates and higher thermal loads, tape performance specifications become more stringent. Suppliers that invest in thin-film adhesive coating technologies and precision converting capabilities can capture higher-margin specialty opportunities.

Category-wise Analysis

Product Type Insights

Double-sided splicing tape is expected to account for approximately 60.8% of the market in 2026, maintaining its leadership due to broad applicability across flying splices, core starts, butt splices, and roll finishing on paper, packaging, tissue, and labeling lines. Double-coated constructions provide immediate tack, strong overlap bonding, and clean web transfer, which are essential for high-speed converting operations exceeding several hundred meters per minute. For instance, corrugated board manufacturers and flexible packaging converters rely on differential adhesive constructions (high-tack on one side, controlled-release on the other) to ensure seamless roll changes without machine stoppages.

The extensive installed base of automatic splicing heads from suppliers such as Pasaban, Valmet, and BW Papersystems further reinforces the continued preference for double-sided formats. Their predictable shear strength, tensile stability, and compatibility with both paper and film substrates sustain long-term demand across mature and emerging converting markets.

Repulpable splicing tapes represent the fastest-growing product category, driven by tightening sustainability regulations and mill-level recyclability requirements. These tapes typically incorporate tissue backings with water-dispersible or alkaline-soluble adhesives that disintegrate during the pulping process without contaminating recycled fiber streams. Major paper producers increasingly mandate certified repulpability standards before approving consumables used in production lines.

For example, tissue and specialty paper mills that conduct recyclability trials often validate dispersion performance using TAPPI or equivalent testing protocols. Adoption is strongest in Europe and North America, where circular economy targets are embedded in packaging directives. As brand owners intensify commitments toward recyclable packaging, converters are accelerating the shift from conventional film-based splicing tapes to certified repulpable alternatives, supporting above-average segment growth through the forecast period.

Resin Type Insights

Acrylic adhesives are expected to account for 56.3% of the market in 2026, reflecting their balanced performance characteristics, cost efficiency, and processing flexibility. Acrylic systems are available in solvent-based, water-based, and hot-melt variants, enabling manufacturers to tailor tack level, shear resistance, and temperature tolerance to specific converting conditions. In paper and corrugated applications, acrylic adhesives provide reliable bonding under moderate heat and humidity, making them suitable for high-speed flying splices and core-start applications.

Their compatibility with double-sided constructions and consistent aging performance ensures stable adhesion during storage and operation. Leading adhesive manufacturers continue refining low-VOC and water-based acrylic technologies to meet environmental compliance requirements while maintaining bonding reliability.

Silicone adhesives are the fastest-growing resin segment, driven by rising demand in release liner production, specialty films, and electronics web handling. Silicone-based systems offer superior thermal stability, chemical resistance, and adhesion to low-surface-energy substrates such as fluoropolymers and treated films. For example, release liner manufacturers for label stock and medical applications often require silicone-compatible splicing tapes that maintain bond strength at elevated curing temperatures.

In electronics and battery film manufacturing, where substrates are thin and sensitive, silicone adhesives provide clean removability and consistent performance without residue transfer. Their premium positioning enables higher margins, particularly in Asia-Pacific and advanced European converting operations, where specialty film production is expanding.

Regional Insights

North America Splicing Tape Market Trends - Automation-Driven Demand, EPR-Led Repulpability Shift, and Electronics-Grade Silicone Expansion

North America represents a technologically advanced and innovation-driven splicing tape market, supported by mature paper converting, flexible packaging, and specialty film industries. The U.S. accounts for the majority of regional demand, reflecting its large installed base of corrugated board plants, tissue mills, and high-speed labeling operations. According to the American Forest & Paper Association (AF&PA), the U.S. paper and paperboard industry ships more than 80 million tons annually, providing a stable consumption base for splicing consumables.

Investments in modernization, including automated flying splice systems and zero-defect roll-change technologies, continue to sustain steady demand for double-sided and specialty adhesive tapes. Recent corporate developments illustrate the region’s momentum in innovation. In 2024, 3M expanded its investment in advanced manufacturing capabilities in the U.S., including adhesive technologies supporting industrial and electronics applications, reinforcing domestic supply resilience.

Similarly, Avery Dennison strengthened its pressure-sensitive materials operations in North America to support labeling and packaging growth, which indirectly drives demand for high-performance splicing tapes used in release liner and label stock production. In the specialty adhesives segment, Intertape Polymer Group (IPG) has expanded its sustainable product lines, including water-based and recyclable tape solutions aligned with circular-economy goals.

Demand growth is further supported by sustainability mandates at both the federal and state levels. Extended Producer Responsibility (EPR) legislation adopted in states such as California and Colorado is increasing scrutiny on packaging recyclability, encouraging converters to adopt repulpable splicing tapes. North America’s expanding electronics manufacturing ecosystem, boosted by semiconductor and battery investments under the U.S. CHIPS and Science Act, creates demand for silicone-based splicing tapes capable of performing under high-temperature and precision conditions. Strategically, suppliers operating in North America must balance premium silicone offerings for electronics and specialty film converters with certified repulpable alternatives for paper mills seeking compliance with sustainability benchmarks.

Europe Splicing Tape Market Trends - EU Circular Economy Compliance, Precision Converting Systems, and Sustainable Adhesive Innovation

Europe maintains a structurally strong demand for splicing tapes across paper & printing, corrugated packaging, and release liner production. Germany is the regional technology leader, supported by advanced converting machinery manufacturers such as BST Group, Kampf, and Pasaban, which drive adoption of automated splicing systems that require precise adhesive performance. The country’s highly developed packaging ecosystem and export-oriented manufacturing base contribute significantly to overall European consumption.

Regulatory harmonization under the European Union’s Packaging and Packaging Waste Directive (PPWD) and circular economy action plan has accelerated the adoption of recyclable and repulpable splicing solutions. Certification requirements aligned with CEPI (Confederation of European Paper Industries) guidelines and mill-level recyclability testing standards increasingly influence purchasing decisions.

Recent developments reflect this transition. In 2024, tesa SE expanded its sustainable adhesive portfolio, introducing solvent-free and more recyclable bonding solutions targeted at paper and packaging applications, strengthening its position in Germany and neighboring markets. Similarly, Lohmann GmbH & Co. KG continued advancing high-performance bonding technologies for industrial and electronics applications, supporting Europe’s growing specialty film and battery manufacturing sectors.

France and Spain contribute substantial corrugated output, supported by rising e-commerce penetration and food packaging demand, while the U.K. remains a key hub for labeling and pharmaceutical packaging. Investment trends across Europe increasingly focus on material circularity and automation efficiency. Collaborative R&D initiatives between adhesive manufacturers and paper mills aim to improve dispersion performance and minimize fiber contamination during recycling. Suppliers with documented environmental credentials and lifecycle data are positioned to capture growth as sustainability compliance becomes a procurement prerequisite rather than a differentiator.

Asia Pacific Splicing Tape Market Trends - Manufacturing Scale Leadership, High-Speed Converting Growth, and Electronics-Focused Adhesive Advancements

Asia Pacific is projected to lead the market with over 39.4% share in 2026, and represents the fastest-growing regional market. The region’s dominance stems from its concentration of paper, packaging, electronics, and film manufacturing capacity across China, Japan, India, and ASEAN economies. China serves as the principal manufacturing hub, accounting for a substantial portion of global paperboard and corrugated production, which directly drives consumption of double-sided and repulpable splicing tapes in high-speed converting lines. Recent industrial investments reinforce this trajectory.

Chinese packaging producers continue to expand corrugated capacity to support domestic e-commerce growth, with investments from companies such as Nine Dragons Paper and Lee & Man Paper Manufacturing, both of which have invested in modern, high-speed paper machines that require advanced splicing technologies. Japan maintains leadership in specialty adhesive innovation, with companies such as Nitto Denko Corporation and LINTEC Corporation developing high-performance silicone and acrylic adhesive systems tailored for electronics and optical film applications.

India and Southeast Asia are experiencing robust growth in corrugated packaging, driven by FMCG expansion and organized retail development. Investments in new containerboard facilities and converting plants increase the installed base of automatic splicing equipment, reinforcing long-term consumable demand. ASEAN countries, including Vietnam and Thailand, are attracting electronics and display panel manufacturing investments, which are expanding demand for high-temperature silicone-based splicing solutions.

Local production capacity and technical support centers represent critical success factors in Asia Pacific. Multinational suppliers are expanding their coating facilities and distribution networks to reduce lead times and meet regional customization requirements. Companies with strong converter partnerships and localized engineering support are positioned to capture the majority of incremental demand growth as the Asia Pacific consolidates its leadership in global manufacturing output.

Competitive Landscape

The global splicing tape market is moderately concentrated. Global adhesive manufacturers such as 3M, tesa SE, Nitto Denko, Avery Dennison, Lintec, and Scapa/SWM hold strong positions in premium and specialty segments. Regional converters compete in commodity-grade categories. Specialty combinations such as silicone adhesives with PET backings command stronger pricing power, while paper/tissue acrylic constructions remain price-sensitive. Leading companies emphasize product differentiation, sustainability validation, regional production expansion in Asia Pacific, and technical co-development with converters. Premium innovation supports margins, while cost leadership remains important in high-volume commodity segments.

Key Industry Developments:

- In February 2025, tesa SE launched the tesa® 61127 release liner splicing tape, a single-sided splicing tape with a silicone adhesive and anti-adhesive PET backing designed for efficient splicing of siliconized papers, films, and low-surface-energy materials to improve process continuity and reduce rework and waste in release liner applications.

Companies Covered in Splicing Tape Market

- 3M Company

- tesa SE

- Nitto Denko Corporation

- Avery Dennison Corporation

- LINTEC Corporation

- Intertape Polymer Group Inc.

- Scapa Group Ltd.

- Shurtape Technologies, LLC

- Lohmann GmbH & Co. KG

- Berry Global Inc.

- Saint-Gobain Performance Plastics

- Adhesive Applications, Inc.

- CCT Tapes

- DeWAL Industries (Rogers Corporation)

- Sekisui Chemical Co., Ltd.

- Lintec of America, Inc.

- Advanced Tape Solutions

- Parafix Tapes & Conversions Ltd.

Frequently Asked Questions

The global splicing tape market size is projected to be valued at US$730.8 million in 2026.

The splicing tape market is expected to reach US$1,014.7 million by 2033.

Key trends include increasing automation in high-speed converting lines, rising adoption of repulpable and recyclable adhesive solutions, growing demand for silicone-based tapes in release-liner and electronics applications, and regional manufacturing expansion in Asia Pacific. Suppliers are also investing in localized converting facilities and technical service support to enhance supply chain resilience.

Double-sided splicing tape is the leading product type, accounting for 60.8% market share, driven by its versatility in flying splices, roll changes, and automated converting systems.

The splicing tape market is anticipated to grow at a CAGR of 4.8% between 2026 and 2033.

Major players include 3M Company, tesa SE, Nitto Denko Corporation, Avery Dennison Corporation, and LINTEC Corporation.