- Non-food Packaging

- Spacer Tapes Market

Spacer Tapes Market Size, Share, and Growth Forecast, 2026 - 2033

Spacer Tapes Market By Material (Polyethylene (PE) Foam, Acrylic Foam, Others), Adhesive Type (Acrylic-Based Adhesive, Silicone-Based Adhesive, Others), Thickness, End-user, and Regional Analysis for 2026 - 2033

Spacer Tapes Market Size and Trends Analysis

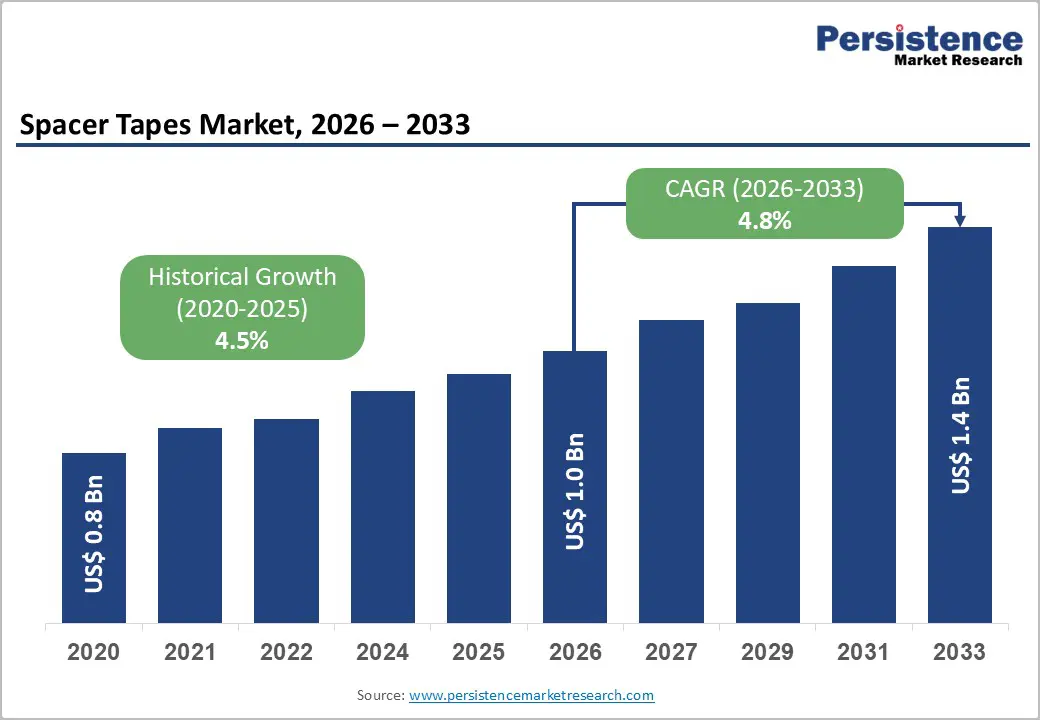

The global spacer tapes market size is likely to be valued at US$1.0 billion in 2026 and is expected to reach US$1.4 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by rising electric vehicle production, increased electronics miniaturization, growing requirements for vibration and noise mitigation, and broader adoption of specialty adhesive technologies, particularly acrylic foam systems.

Spacer tapes are foam-backed and adhesive-backed materials engineered to create controlled spacing, cushioning, and sealing between assembled components. Demand continues to expand across automotive, electronics, construction, aerospace, and packaging applications. The overall trajectory aligns with sustained expansion across the global adhesive and specialty tape industry.

Key Industry Highlights

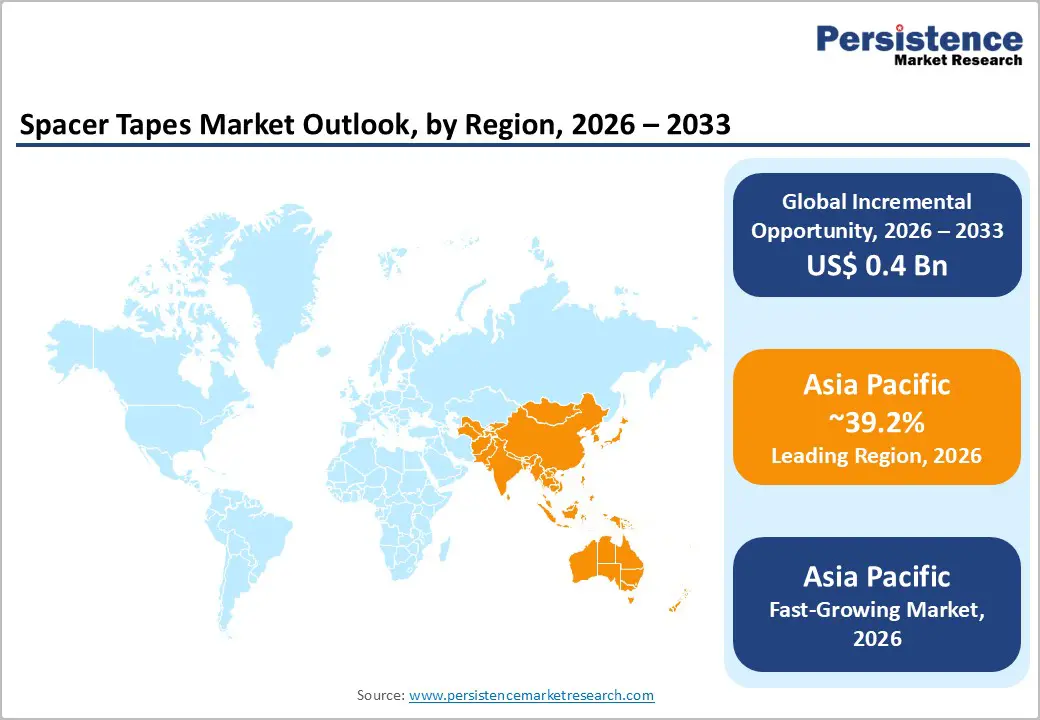

- Leading Region: Asia Pacific is projected to lead the market, accounting for an estimated 39.2% share, supported by concentrated electronics manufacturing, large-scale electric vehicle production, and expanding construction activity across China, Japan, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is also likely to be the fastest-growing regional market, driven by rapid expansion in EV battery assembly, electronics manufacturing services, and localized converting capacity.

- Investment Plans: Industry investments are focused on regional converting and slitting capacity expansion, particularly in Southeast Asia, India, and near North American OEM hubs, alongside increased spending on application engineering, certification testing, and engineered acrylic foam systems to support high-value automotive and electronics applications.

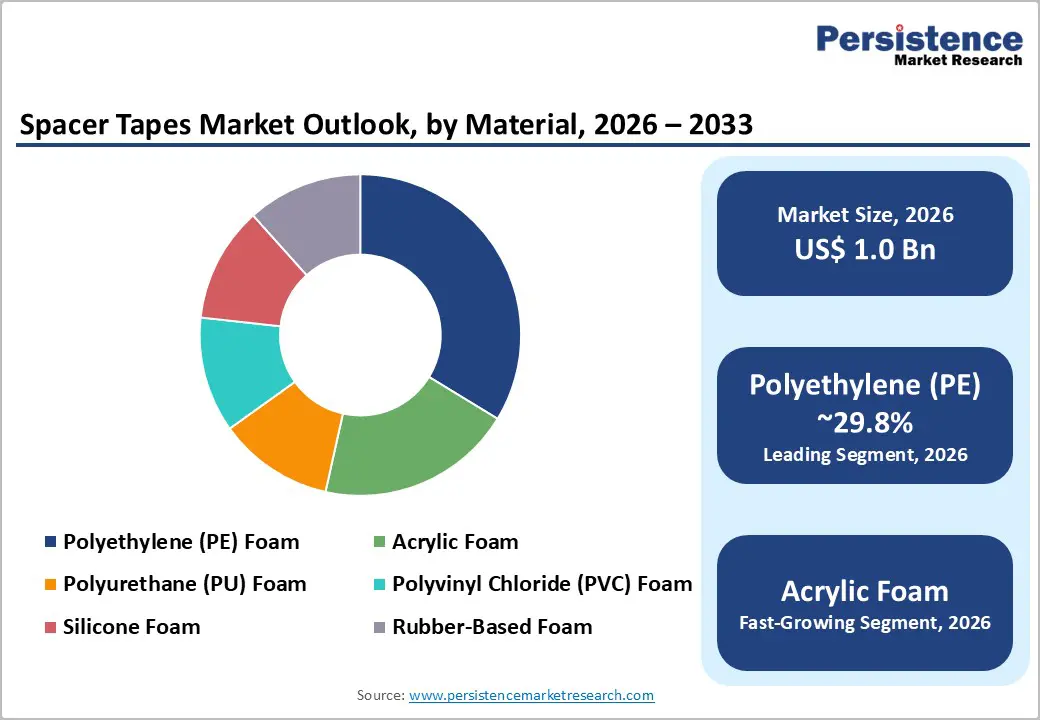

- Dominant Material: Polyethylene (PE) foam is expected to remain the dominant material category, holding an anticipated 29.8% market share, due to its cost-efficiency, moisture resistance, and suitability for high-volume automotive, HVAC, and construction sealing applications.

- Leading Adhesive Type: Acrylic-based adhesives are likely to be the leading adhesive type, accounting for an anticipated 43.5% of market share, favored for their balanced performance in durability, weather resistance, and long-term adhesion across automotive, construction, and industrial end-use sectors.

| Key Insights | Details |

|---|---|

| Spacer Tapes Market Size (2026E) | US$1.0 Bn |

| Market Value Forecast (2033F) | US$1.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Electrification and Automotive Lightweighting Increase Spacer Tape Demand

The global shift toward vehicle electrification is reshaping component design and assembly processes. Electric vehicle platforms increasingly reduce the use of mechanical fasteners in favor of bonded joints, elevating the importance of vibration isolation, sealing, and thermal spacing functions provided by spacer tapes. Electric vehicles incorporate higher electronics content, battery systems, and thermal management assemblies, all of which require precise spacing and insulation solutions.

Global electric vehicle production reached approximately 17.3 million units in 2024, with China accounting for nearly 70% of total output. Continued growth in EV penetration through the 2025-2030 period is expected to increase spacer tape usage in under-hood components, battery pack insulation, interior trim bonding, and noise-dampening applications. This structural shift supports sustained volume growth and favors premium spacer tapes using specialty adhesive systems.

Miniaturization and Higher-Density Electronics Drive Thin, High-Performance Spacer Tapes

Electronics manufacturing trends continue to emphasize smaller form factors, higher component density, and greater functional integration. Consumer electronics, telecommunications equipment, and industrial electronics increasingly require thin, high-adhesion spacer tapes capable of maintaining consistent spacing while delivering mechanical decoupling, thermal insulation, and electromagnetic interference control.

Asia Pacific remains the global center of electronics manufacturing, creating concentrated demand for spacer tapes with thicknesses of one millimeter or less. Foam carriers and advanced adhesives are being specified for applications where tight tolerances, long-term adhesion, and dimensional stability are critical. This shift supports rising unit volumes and higher average selling prices for engineered spacer tape products, reinforcing growth across the specialty tape segment.

Barrier Analysis - Raw-Material Price Volatility and Feedstock Constraints

Spacer tapes rely on polymer-based foam carriers such as polyethylene, polyurethane, PVC, silicone, and rubber, combined with acrylic, silicone, or rubber adhesives. Volatility in petrochemical feedstocks creates cost uncertainty and margin pressure for manufacturers. Regions with limited access to local polymer production face longer lead times and higher logistics costs, increasing overall landed costs. Industry data indicates that during periods of sharp feedstock price increases, manufacturers are typically able to pass through only 60 to 80% of cost increases. Competitive pricing pressures often prevent full cost recovery, leading to margin compression and slower procurement decisions among OEM customers.

Regulatory and Performance Certification Complexity in Critical Sectors

Automotive, aerospace, and regulated construction applications require compliance with strict fire, smoke, toxicity, and outgassing standards, along with OEM-specific qualification processes. Certification testing, including thermal cycling, salt spray exposure, and volatile organic compound analysis, extends development timelines and raises technical entry barriers. Development and certification processes can add between six and eighteen months to product commercialization and increase project costs by an estimated 2 to 6%. These requirements limit rapid market entry for smaller converters and reinforce competitive advantages for established suppliers with in-house testing capabilities and regulatory expertise.

Opportunity Analysis - Value Migration to Engineered Acrylic Foam Spacer Systems

Acrylic-based foam spacer tapes are increasingly adopted for structural bonding and environmental sealing in automotive and construction applications. Transitioning from commodity foam products to engineered acrylic foam systems enables suppliers to offer differentiated performance through tailored density profiles, surface treatments, and multilayer adhesive constructions.

Capturing even a modest incremental share of the broader specialty foam tape ecosystem could generate significant incremental revenue over the medium term. As demand shifts toward high-performance bonding solutions, suppliers that invest in application engineering and product customization are positioned to benefit from margin expansion and longer-term OEM partnerships.

Regional Manufacturing Partnerships in ASEAN and India

Nearshoring strategies and industrial policy incentives are accelerating electronics and automotive manufacturing investment across Southeast Asia and India. These regions present strong opportunities for localized spacer tape converting, slitting, and finishing operations. Establishing regional manufacturing partnerships enables suppliers to reduce transportation costs, improve responsiveness to just-in-time production schedules, and comply with local sourcing requirements.

Given Asia Pacific’s dominant role in electronics manufacturing, capturing even a small share of regional assembly spend represents a meaningful growth opportunity, particularly for thin, high-performance spacer tape products tailored to local OEM specifications.

Category-wise Analysis

Material Insights

Polyethylene foam is anticipated to account for 29.8% market share in 2026, supported by its cost efficiency, moisture resistance, and favorable compression recovery characteristics. PE foam is extensively used in automotive interior components, HVAC gasketing, appliance sealing, and construction joint applications. Its balanced combination of flexibility, dimensional stability, and lightweight properties makes it suitable for high-volume production programs that require consistent mechanical performance over long service cycles. Major converters maintain extensive PE foam inventories and highly optimized converting lines to support large-scale OEM contracts, particularly in the automotive and building materials sectors. Applications such as body-side sealing, instrument panel cushioning, trim attachment, and door-gap spacing continue to rely on PE foam due to its predictable behavior under compression, ease of die-cutting, and compatibility with a wide range of pressure-sensitive adhesives.

Acrylic foam is expected to be the fastest-growing material category within the market, driven by its superior adhesion strength, long-term durability, and ability to replace mechanical fasteners in structural bonding applications. Adoption is accelerating across electric vehicles, battery pack assemblies, architectural glazing systems, and façade installations, where resistance to temperature fluctuations, UV exposure, and environmental aging is critical. Acrylic foam commands higher pricing per unit length compared with conventional foam materials, enabling suppliers to capture greater value per application. Increasing penetration in electronics housings, automotive lightweighting initiatives, and glass bonding solutions continues to support growth rates that significantly exceed those of commodity foam-based spacer tapes.

Adhesive Type Insights

Acrylic-based adhesives are anticipated to dominate, accounting for approximately 43.5% of market share in 2026. These adhesive systems provide strong shear and peel strength, excellent weathering resistance, and stable adhesion performance across a wide operating temperature range. As a result, they are widely specified for automotive exterior trim attachment, glazing systems, signage mounting, and construction sealing applications where long-term reliability is essential. OEMs consistently favor acrylic-based adhesive systems for long-life assemblies that require resistance to moisture, UV radiation, and thermal cycling. Manufacturers continue to refine acrylic formulations, liner technologies, and surface treatments to enhance adhesion to low-surface-energy substrates such as plastics and coated metals, while also reducing the risk of delamination and in-service failure.

Silicone-based adhesives represent the fastest-growing adhesive segment, particularly in applications demanding high-temperature stability, chemical resistance, and low outgassing performance. Growth is driven by increasing usage in aerospace interiors, electric vehicle battery enclosures, power electronics, and advanced industrial equipment, where conventional adhesive systems may fail under extreme operating conditions. Although silicone adhesive systems carry higher raw material and processing costs, their performance advantages enable entry into premium, highly regulated applications. This segment benefits from higher average selling prices, longer qualification cycles, and improved margins for suppliers capable of meeting stringent aerospace, electronics, and automotive safety standards.

Regional Insights

North America Spacer Tapes Market Trends - OEM-Driven Demand in Automotive, Aerospace, and EV Manufacturing

North America accounts for a significant share of global spacer tape demand, underpinned by the region’s strong automotive, aerospace, industrial equipment, and advanced electronics manufacturing base. The U.S. leads regional consumption, with demand concentrated among OEMs and tier-one suppliers that require certified, application-specific materials for long production cycles. Automotive OEMs such as General Motors, Ford, and Tesla continue to specify high-performance spacer tapes for exterior trim bonding, battery module spacing, and noise, vibration, and harshness management, reinforcing stable baseline demand.

Growth across North America is driven by vehicle electrification, rising aerospace maintenance, repair, and overhaul activity, and increasing automation in industrial and medical equipment manufacturing. For example, expanding EV battery production capacity across Michigan, Texas, and Tennessee has increased the use of acrylic foam spacer tapes for thermal management and structural bonding applications. In aerospace, suppliers aligned with Boeing and major MRO providers increasingly require silicone- and acrylic-based systems that meet flammability and low-outgassing standards.

Regulatory requirements related to flammability, volatile organic compound emissions, and material traceability extend qualification timelines but favor suppliers with established testing, documentation, and certification infrastructure. Investment trends focus on expanding converting capacity near OEM manufacturing hubs and strengthening partnerships with adhesive formulators. Companies such as 3M and Avery Dennison have continued to invest in application engineering support and localized converting operations, enabling faster OEM approvals and reinforcing supplier lock-in within regulated end-use segments.

Europe Spacer Tapes Market Trends - Sustainability-Led Adoption Across Automotive, Construction, and Energy

Europe’s spacer tape market is diversified across automotive manufacturing, construction, renewable energy, and industrial equipment, with demand shaped by both mature OEM ecosystems and evolving regulatory priorities. Germany leads regional demand through its automotive and machinery sectors, supported by OEMs such as Volkswagen, BMW, and Mercedes-Benz, which increasingly rely on spacer tapes for lightweight assembly, trim attachment, and acoustic insulation. The U.K., France, and Spain contribute through construction activity, retrofit projects, and renewable energy installations, particularly in façade systems and glazing applications.

European OEMs place strong emphasis on sustainability, recyclability, and low-emission materials, directly influencing spacer tape material selection and adhesive formulation. Regulatory frameworks such as REACH and evolving fire performance standards drive demand for compliant foam carriers, low-VOC adhesives, and traceable supply chains. These requirements increase qualification costs but also raise entry barriers, benefiting established suppliers with proven compliance records. Ongoing investment across the region focuses on sustainable foam technologies, recyclable liners, and expanded testing capabilities. Several European converters and material suppliers have expanded laboratory and validation facilities to support OEM sustainability targets and lifecycle assessment requirements. Brands supplying the construction and mobility sectors increasingly position spacer tapes as alternatives to mechanical fasteners, aligning with Europe’s broader push toward material efficiency, reduced assembly complexity, and lower lifecycle emissions.

Asia Pacific Spacer Tapes Market Trends - High-Volume Electronics and EV Production Driving Rapid Growth

Asia Pacific holds the largest share of the market, estimated at approximately 39.2%, and represents the fastest-growing regional market. Demand is driven by the region’s concentration of electronics manufacturing, large-scale automotive production, and expanding construction activity. The presence of vertically integrated supply chains and high-volume manufacturing environments continues to support widespread adoption of spacer tapes across multiple end-use industries.

China remains the largest single manufacturing hub, particularly for electric vehicles, consumer electronics, and battery systems. OEMs and suppliers supporting brands such as BYD, CATL, and leading smartphone manufacturers increasingly use acrylic foam and silicone-based spacer tapes for structural bonding, thermal isolation, and component spacing. Japan contributes demand for high-specification industrial, automotive, and electronics applications, where precision tolerances and long-term reliability are critical, reinforcing demand for premium adhesive systems.

India and ASEAN countries are experiencing rapid growth, supported by policy initiatives promoting electric mobility and electronics manufacturing localization. Programs encouraging domestic production have accelerated investment in converting facilities and application engineering centers across India, Vietnam, Thailand, and Indonesia. Local content rules and import policies encourage regional production, while global suppliers increasingly partner with regional converters to shorten lead times and improve OEM responsiveness. These developments strengthen Asia Pacific’s position as both the largest consumption base and the primary growth engine for the spacer tapes market.

Competitive Landscape

The global spacer tapes market is moderately concentrated at the global level. Large multinational adhesive and tape manufacturers dominate high-value engineered and certified products, supported by integrated research, formulation, and converting capabilities. A broad base of regional converters supplies commodity and custom spacer tapes for cost-sensitive and short-lead applications.

Recent strategic activity across the market includes expansion of engineered acrylic foam production capacity to address automotive and electronics bonding demand, regional converting investments in Southeast Asia to support nearshoring strategies, and partnerships focused on certified high-temperature silicone spacer tapes for aerospace and battery systems.

Leading companies emphasize product differentiation through advanced adhesive systems, vertical integration of adhesive formulation and converting, and regional capacity deployment aligned with OEM production footprints. Emerging strategies include co-development with OEMs, long-term supply agreements, and sustainability-focused product positioning.

Key Industry Developments

- In March 2025, Avery Dennison introduced pressure-sensitive adhesive tape solutions for electric vehicle battery cell wrapping applications, enhancing electrical insulation performance within EV battery packs.

Companies Covered in Spacer Tapes Market

- 3M

- Tesa SE

- Nitto Denko Corporation

- Avery Dennison

- Henkel AG & Co. KGaA

- Shin-Etsu Chemical Co., Ltd.

- Intertape Polymer Group

- Berry Global

- Scapa Group

- Dow

- Sika AG

- Saint-Gobain

- Adhesives Research

- Lintec Corporation

- Lohmann GmbH & Co. KG

- Orafol Group

- Mitsubishi Chemical Group

- Parker Hannifin

Frequently Asked Questions

The global spacer tapes market size is likely to be valued at US$1.0 billion in 2026.

By 2033, thespacer tapes market is expected to reach US$1.4 billion.

Key trends include increased adoption of acrylic foam spacer tapes, rising demand for thin-profile tapes in compact electronics, substitution of mechanical fasteners with adhesive solutions in electric vehicles, and regionalization of converting capacity in Asia Pacific and North America to support just-in-time manufacturing.

By material, polyethylene (PE) foam is the leading segment, accounting for an anticipated 29.8% market share, driven by its cost efficiency and wide use in automotive interiors, HVAC, and construction sealing applications.

The spacer tapes market is projected to grow at a CAGR of 4.8% between 2026 and 2033.

Major players include 3M, Tesa SE, Nitto Denko Corporation, Avery Dennison, and Henkel AG & Co. KGaA.