- Biotechnology

- Gel and Blot Imaging Systems Market

Gel and Blot Imaging Systems Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Gel and Blot Imaging Systems Market by Product Type (Instruments, Software, Accessories), Application (Research Applications, Clinical Applications, Pharmaceutical Applications), End-use, and Regional Analysis for 2025 - 2032

Gel and Blot Imaging Systems Market Size and Trends Analysis

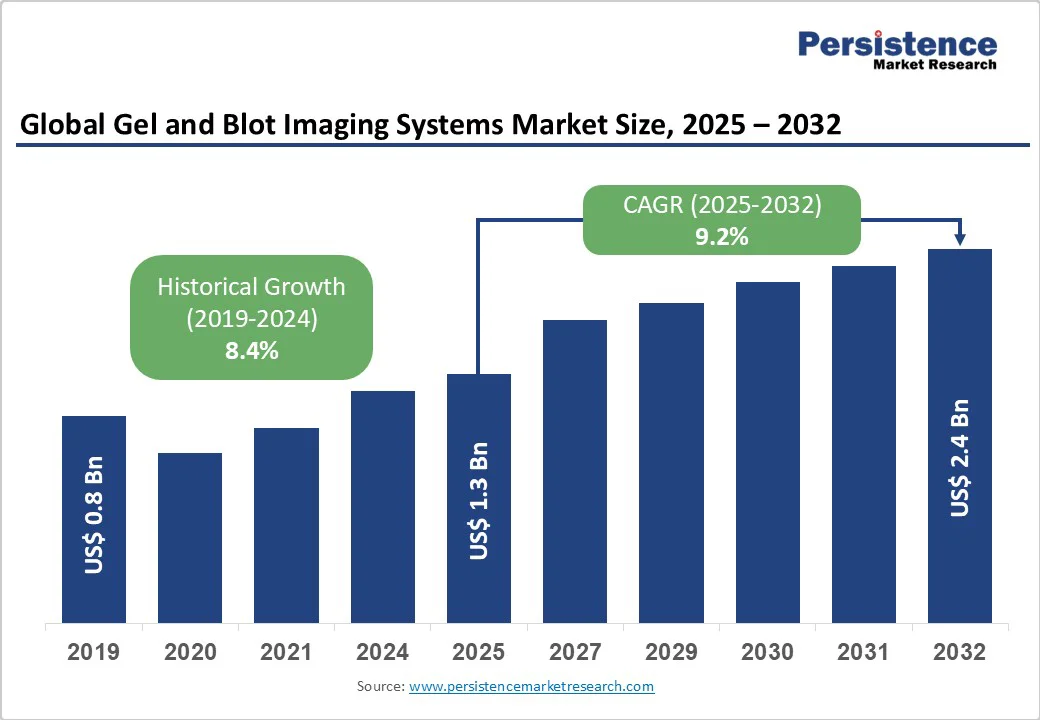

The global gel and blot imaging systems market size is likely to value US$1.3 Bn in 2025 and is expected to reach US$ 2.4 Bn by 2032, growing at a CAGR of 9.2% during the forecast period from 2025 to 2032, driven by the increasing demand for high-throughput, precise imaging technologies in life sciences, advancements in automated and digital imaging solutions, and the growing adoption of these systems across academic, clinical, and industrial settings.

Key Industry Highlights:

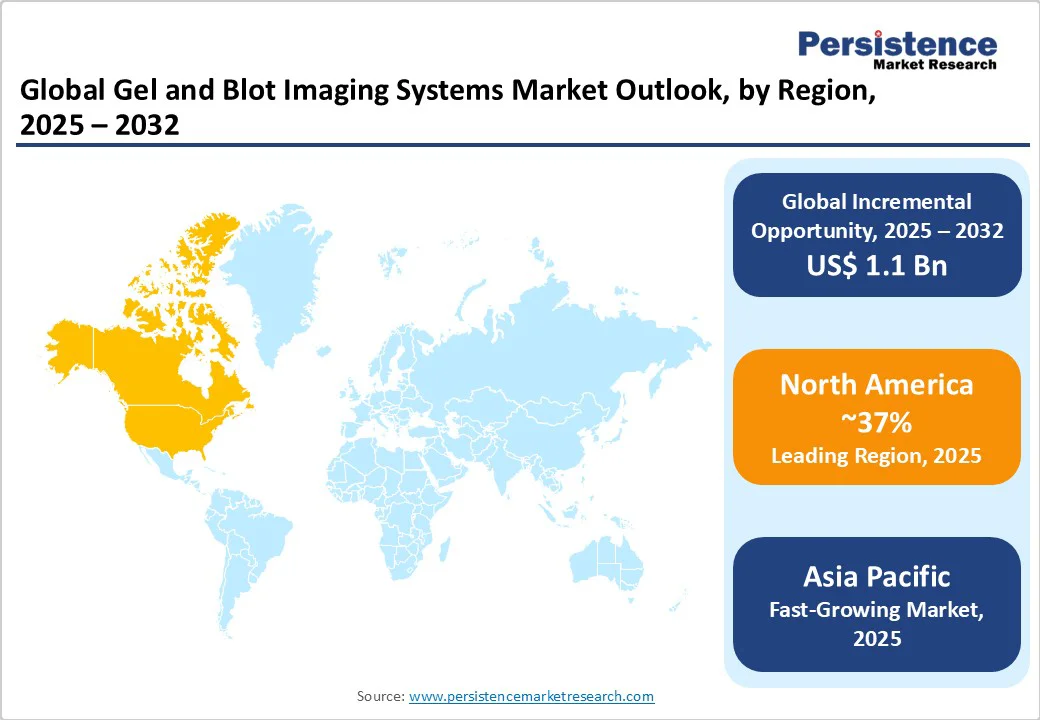

- Leading Region: North America is likely to register a 37% share in 2025, driven by robust research infrastructure in the U.S.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, fueled by biotechnology advancements in China and India.

- Dominant Product Type: Instruments account for a 52% share, driven by their critical role in imaging workflows.

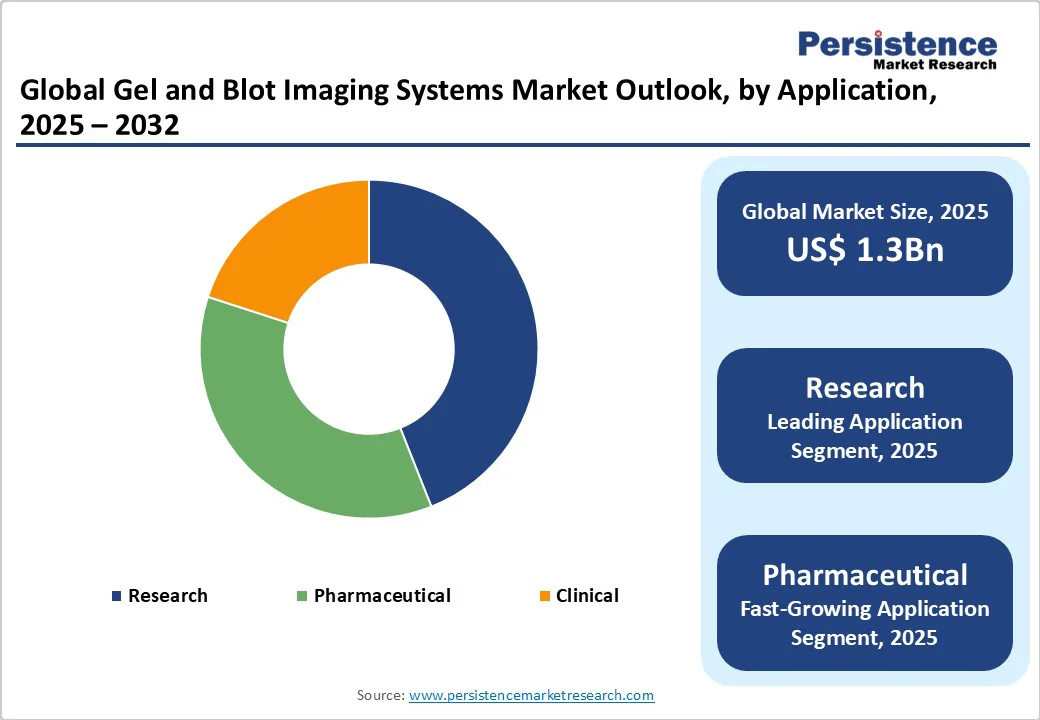

- Leading Application: Research applications poised for a 44% share in 2025, supported by extensive use in genomic and proteomic studies.

| Key Insights | Details |

|---|---|

| Gel and Blot Imaging Systems Market Size (2025E) | US$ 1.3 Bn |

| Market Value Forecast (2032F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.4% |

Market Dynamics

Driver- Growing Demand for High-Throughput Research Tools

The increasing demand for high-throughput research tools is a primary driver of the gel and blot imaging systems market. The rise in genomic and proteomic research, particularly in areas such as gene expression analysis, protein characterization, and biomarker discovery, has created a strong need for advanced imaging systems that can deliver precise, reproducible results. Gel and blot imaging systems, such as those offered by Bio-Rad Laboratories and Thermo Fisher Scientific, enable researchers to visualize and quantify DNA, RNA, and protein samples with high sensitivity and accuracy.

For instance, the ChemiDoc Go Imaging System from Bio-Rad is a compact benchtop device designed for high-sensitivity imaging of Western blots and nucleic acid gels. It leverages advanced CMOS digital imaging technology to deliver precise and reproducible results, making it suitable for high-throughput research environments.

The growing adoption of automated imaging systems, which reduce manual intervention and enhance throughput, has accelerated their use in high-volume research settings. For instance, the iBright CL1000 and FL1000 Imaging Systems from Thermo Fisher offer automated imaging and analysis for chemiluminescent and fluorescent western blots, as well as colorimetric protein and nucleic acid gels. These systems streamline workflows by automating image capture and analysis, thereby reducing manual intervention and increasing throughput in high-volume research settings.

Restraint- High Initial Costs and Maintenance Expenses

High initial costs and ongoing maintenance expenses act as significant restraints on the gel and blot imaging systems market, particularly affecting smaller laboratories and academic institutions. Advanced systems such as the Bio-Rad ChemiDoc Go and Thermo Fisher iBright Imaging Systems provide high sensitivity and automation but require a substantial upfront investment, making them less accessible for budget-limited facilities.

Beyond purchase, regular maintenance is essential to ensure optimal performance, with preventive maintenance adding to the overall financial burden. For instance, many universities and small research labs continue using traditional gel documentation methods instead of upgrading to automated imaging systems due to these high costs, which can slow down workflow efficiency and limit the adoption of high-throughput research techniques.

This is particularly evident in low- and middle-income countries, where the high cost of gel documentation systems remains a significant barrier, especially for laboratories in public universities and government-funded research labs.

Opportunity- Advancements in AI-Integrated Imaging Technologies

Advancements in AI-integrated imaging technologies present a significant opportunity for the gel and blot imaging systems market, enhancing efficiency and accuracy in molecular biology research. AI algorithms can automate image analysis, reduce human error, and increase throughput, which is particularly beneficial in high-volume research environments.

For instance, Thermo Fisher’s iBright Analysis Software uses AI-driven algorithms to automatically detect and quantify bands in Western blots, improving accuracy and saving researchers significant time.

AI can facilitate the detection of subtle protein or nucleic acid signals that might be missed by manual analysis. AI-driven systems also adapt to various imaging modalities, such as chemiluminescence, fluorescence, and colorimetric imaging, providing versatility in experimental setups.

The integration of AI allows for real-time data analysis and interpretation, accelerating research workflows and supporting the growing demand for personalized medicine. As the global gel and blot imaging system market expands, AI-enabled technologies are expected to drive adoption by offering enhanced capabilities, efficiency, and reliability in high-throughput research settings.

Category-wise Analysis

Product Type Insights

Instruments dominate the gel and blot imaging systems Market, accounting for approximately 52% share. Their dominance is attributed to their critical role as the core component of imaging workflows, offering high-resolution imaging for gels, blots, and other biomolecular analyses.

Systems such as GE Healthcare’s Amersham Imager series and Bio-Rad’s ChemiDoc systems are widely adopted due to their versatility, supporting both chemiluminescence and fluorescence detection. The demand for modular and scalable instruments, which can be customized for various research needs, further drives their adoption across academic and industrial settings.

Software is the fastest-growing segment, driven by the increasing need for advanced image analysis and data management tools. AI-integrated software solutions, such as those offered by LI-COR Biosciences and Thermo Fisher Scientific, enhance automation and data accuracy, making them essential for high-throughput research and clinical applications.

Application Insights

Research applications lead, holding a 44% share in 2025. This segment’s dominance is driven by the widespread use of gel and blot imaging systems in academic and research institutes for genomic and proteomic studies. The increasing focus on fundamental research, such as gene expression and protein-protein interactions, drives demand for high-performance imaging systems. For instance, Scientific Digital Imaging’s systems are extensively used in research laboratories for their high sensitivity and ease of use.

Pharmaceutical applications are the fastest-growing segment, propelled by the rising demand for imaging systems in drug discovery and development. The global pharmaceutical R&D expenditure is driving the adoption of imaging systems for high-throughput screening and biomarker validation. The segment is expected to grow, supported by the growing emphasis on precision medicine and biologics development.

End-use Insights

Academic and research institutes are poised for a 43% revenue share in 2025. This segment benefits from strong research funding and the widespread use of imaging systems in molecular biology and life sciences research. Companies such as Bio-Rad Laboratories and Thermo Fisher Scientific provide tailored solutions for academic users, offering cost-effective and scalable systems.

Pharmaceutical and biotechnology companies are the fastest-growing end-use segment, driven by the increasing adoption of imaging systems in drug development and quality control. The rise in biologics and biosimilars development, coupled with the need for high-throughput screening, is accelerating the adoption of advanced imaging systems in this sector. The segment is expected to grow, reflecting the growing importance of imaging in pharmaceutical innovation.

Regional Insights

North America Gel and Blot Imaging Systems Market Trends

North America is projected to hold a 37% share in the global gel and blot imaging systems market by 2025, driven by robust research infrastructure in the U.S., substantial funding in academic and clinical research, and a high demand for advanced imaging technologies in molecular biology and diagnostics. The presence of leading manufacturers such as Bio-Rad Laboratories, Thermo Fisher Scientific, and GE Healthcare strengthens the region’s market position.

Technological advancements, including AI integration and automation in gel imaging systems, further enhance competitiveness. Additionally, supportive regulatory frameworks and continuous investment in life sciences research contribute to North America’s dominance. This 37% share highlights the region’s leadership in innovation, R&D capabilities, and adoption of cutting-edge imaging solutions, positioning it as a critical hub for the global gel and blot imaging systems market.

Europe Gel and Blot Imaging Systems Market Trends

Europe has emerged as a major player in the gel and blot imaging systems market, underpinned by well-established research frameworks and extensive collaborative initiatives across the region. Key countries, including Germany, the UK, and France, are driving market growth through substantial investments in life sciences research and the development of cutting-edge technologies.

Funding programs such as the European Research Council and Horizon Europe play a crucial role in supporting innovative projects, thereby fueling demand for advanced imaging systems across both academic and clinical settings.

Prominent companies such as GE Healthcare and Scientific Digital Imaging contribute significantly by providing state-of-the-art gel and blot imaging solutions that cater to a range of applications, from molecular biology research to clinical diagnostics.

Germany’s emphasis on biotechnology and the UK’s focus on genomics research, including large-scale genomic initiatives, further accelerate the adoption of these imaging systems. Additionally, Europe’s increasing attention to sustainable, automated, and efficient research tools aligns with the growing need for precision diagnostics. Together, these factors ensure a steady expansion of the gel and blot imaging systems market in Europe, positioning the region as a hub for innovation and technological advancement.

Asia Pacific Gel and Blot Imaging Systems Market Trends

Asia Pacific is the fastest-growing market for gel and blot imaging systems, driven by rapid advancements in biotechnology and life sciences research across the region. Countries such as China and India are at the forefront, investing heavily in research infrastructure, academic institutions, and clinical laboratories to support innovations in molecular biology, proteomics, and genomics.

The rising number of biotech startups, expansion of pharmaceutical R&D centers, and increasing government initiatives to promote scientific research are significantly boosting the demand for advanced imaging systems.

Growing awareness of precision diagnostics, coupled with the adoption of automated and high-throughput technologies, is accelerating the deployment of gel and blot imaging systems in both research and clinical applications. The region’s large pool of skilled scientists, coupled with cost-effective manufacturing and scalable solutions, further strengthens market growth.

As a result, the Asia Pacific is poised to continue leading global growth in this sector, offering lucrative opportunities for manufacturers, technology providers, and research institutions seeking to capitalize on the expanding biotechnology landscape.

Competitive Landscape

The global gel and blot imaging systems market is moderately consolidated, dominated by established players such as Bio-Rad Laboratories, Thermo Fisher Scientific, GE Healthcare, and Azure Biosystems, alongside smaller, fragmented regional manufacturers.

In North America and Europe, leading companies leverage advanced R&D capabilities, extensive product portfolios, and collaborations with academic and clinical research institutions to develop high-performance gel and blot imaging solutions. In the Asia Pacific, rapid biotechnology growth in countries such as China and India, along with expanding research infrastructure, attracts both international and local players.

Companies focus on innovative imaging technologies, including chemiluminescent, fluorescent, and multiplex systems, while strategic partnerships, acquisitions, and training initiatives enhance market penetration. Competition is driven by technological advancements, product innovation, automation, and regional expansion strategies, with a growing emphasis on sustainable and AI-integrated imaging solutions.

Key Developments

- In July 2024, Bio-Rad Laboratories launched the ChemiDoc Go imaging system, a benchtop imager utilizing advanced CMOS digital imaging to capture high-sensitivity images of Western blots and gels. This system enhances lab workflows with its compact design and versatility.

- In May 2025, GE Healthcare announced plans to advance enterprise imaging with innovative workflow efficiency solutions, aiming to enhance imaging capabilities across various applications.

Companies Covered in Gel and Blot Imaging Systems Market

- Bio-Rad Laboratories

- Bio-Techne

- LI-COR Biosciences

- GE Healthcare

- Scientific Digital Imaging

- Azure Biosystems

- Cleaver Scientific

- Thermo Fisher Scientific

- TBG Biotechnology

- Others

Frequently Asked Questions

The global gel and blot imaging systems market is projected to reach US$ 1.3 billion in 2025.

The increasing demand for high-throughput research tools is a key driver.

The gel and blot imaging systems market is expected to witness a CAGR of 9.2% from 2025 to 2032.

Advancements in AI-integrated imaging technologies are a key opportunity.

Bio-Rad Laboratories, Bio-Techne, LI-COR Biosciences, GE Healthcare, and Thermo Fisher Scientific are key players.