- Healthcare Services

- Medical Document Management Systems Market

Medical Document Management Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Medical Document Management Systems Market By Product Type (Solution, Service), Delivery Mode (On-premise, Cloud-based, Web-based), Application (Patient Medical Record Management), and Regional Analysis for 2025 - 2032

Medical Document Management Systems Market Size and Trends Analysis

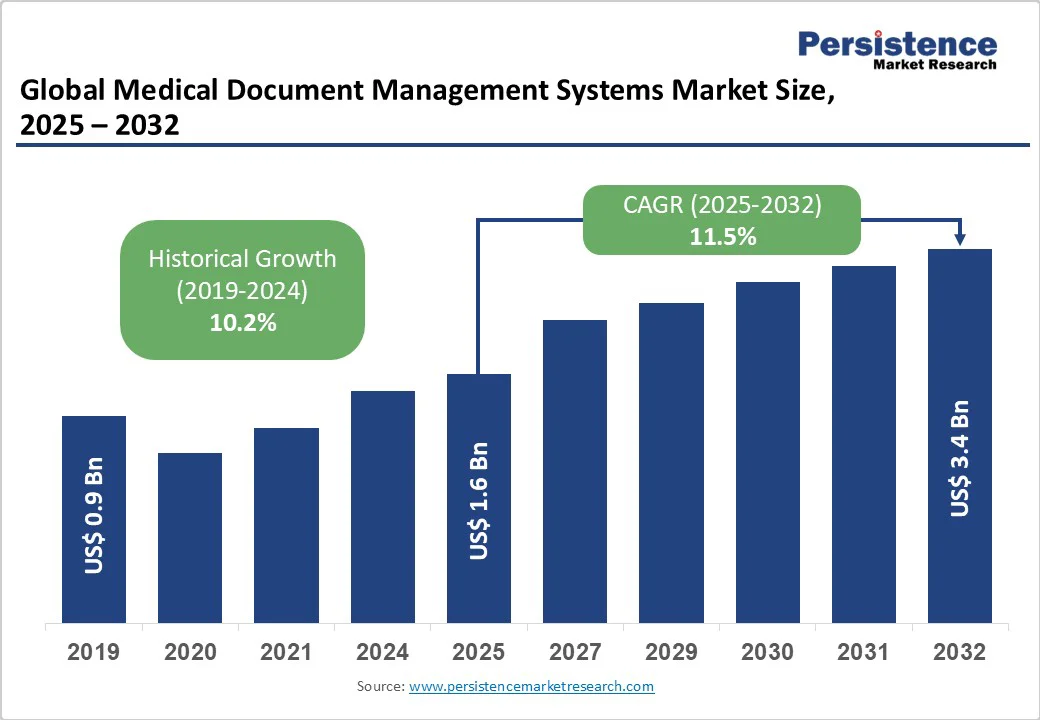

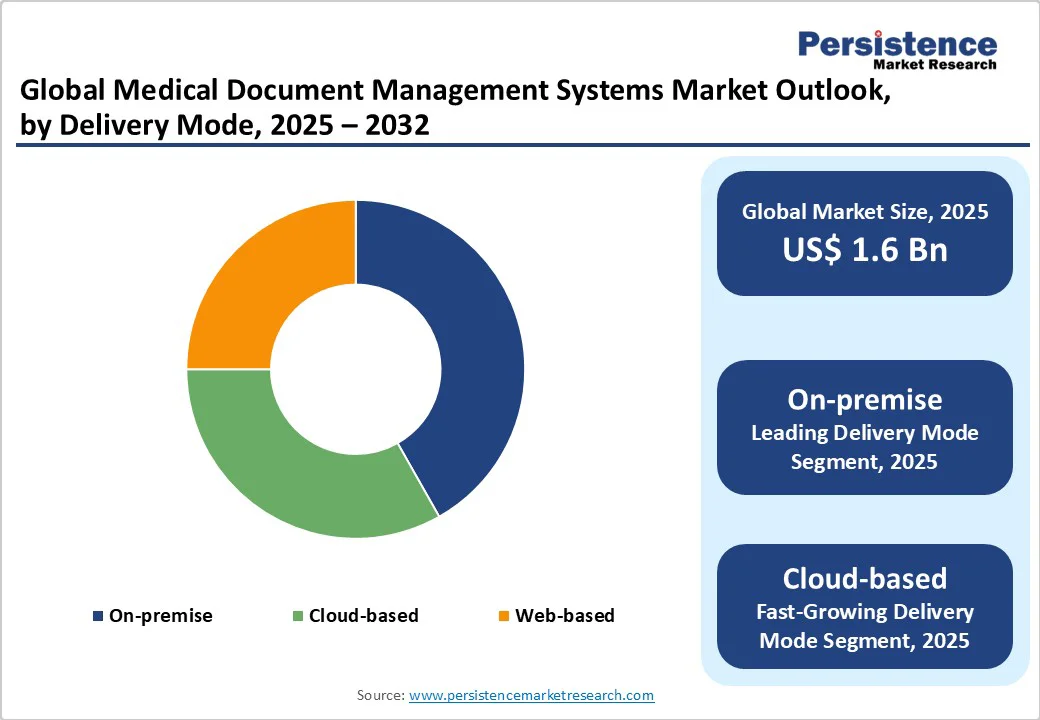

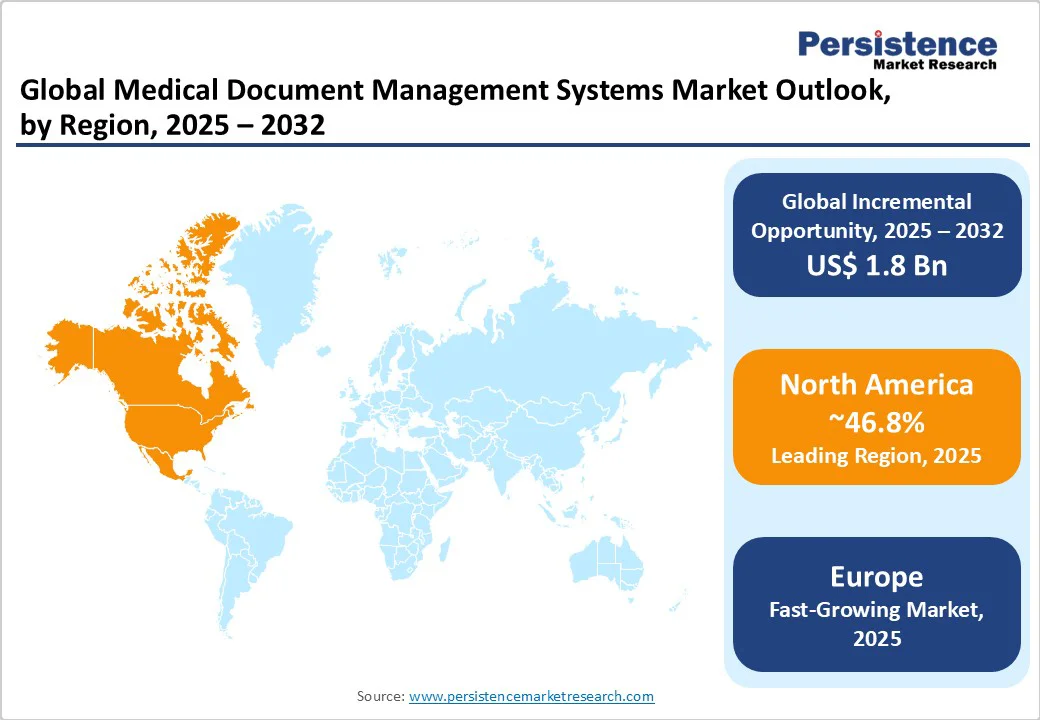

The global medical document management systems market size is likely to be valued at US$1.6 Billion in 2025 and is estimated to reach US$3.4 Billion in 2032, growing at a CAGR of 11.5% during the forecast period 2025 - 2032, driven by the healthcare sector’s push toward digitization, automation, and regulatory compliance.

Key Industry Highlights

- New Features: Wisedocs recently launched two new features designed to improve the processing of complex medical records and claims documentation. These tools, namely WiseChat Q&A and Custom Reports, aim to improve efficiency for insurance carriers, legal professionals, and healthcare providers.

- Leading Region: North America, with about 46.8% share in 2025, backed by high healthcare IT adoption and a well-established hospital infrastructure.

- Fastest-growing Region: Europe, spurred by government investments in digital health infrastructure and interoperability projects.

- Leading Product Type: Service holds nearly 56.4% share in 2025, as healthcare providers rely on third-party services for system integration and maintenance.

- Dominant Delivery Mode: On-premise, approximately 41.8% of the medical document management systems market share in 2025, due to greater control over sensitive patient data and regulatory compliance.

- Key Application: Admission and registration recorded about 44.6% share in 2025, as these processes generate large volumes of patient data.

| Key Insights | Details |

|---|---|

| Medical Document Management Systems Market Size (2025E) | US$1.6 Bn |

| Market Value Forecast (2032F) | US$3.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 11.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Shift toward Cost-efficient Digital Workflows

Healthcare institutions are now adopting Medical Document Management Systems (MDMS) to cut the high costs of paper handling, printing, and physical storage. These platforms automate document organization, approvals, and retrieval, thereby reducing administrative workloads and operational inefficiencies.

Hospitals that have moved to digital document management report saving thousands of staff hours annually by eliminating manual filing and reducing the requirement for off-site storage. For instance, the Mayo Clinic’s adoption of a paperless documentation model led to a 25% reduction in administrative expenses and quick patient record retrieval, showcasing the financial advantage of digital workflows.

Improved Clinical Outcomes through Real-time Data Access

The ability to instantly retrieve accurate and updated patient information allows doctors to make quick and informed medical decisions. Integrated MDMS platforms ensure that lab reports, imaging results, and clinical notes are accessible across departments, supporting better coordination in patient care.

A 2024 study by the Journal of Medical Systems found that hospitals using real-time digital document access reduced diagnostic delays by 18%. This smooth access to updated data not only improves treatment accuracy but also minimizes medical errors and refines care efficiency.

Barrier Analysis- Surging Concerns over Data Privacy and Cybersecurity

The rising digitization of healthcare records has made medical document systems a prime target for cyberattacks. Hospitals and clinics often face ransomware and phishing threats that can expose sensitive patient data. In 2025, the U.S. Department of Health and Human Services reported over 540 healthcare data breaches in a single year, affecting more than 112 million individuals.

Even with encryption and multi-factor authentication, weak legacy systems and human errors still make data vulnerable. These risks discourage small-scale healthcare facilities from fully adopting digital document solutions, fearing regulatory penalties and reputational damage from potential data leaks.

High Upfront Investment and Integration Costs

Deploying a medical document management system involves significant initial expenses for software licensing, IT infrastructure, and employee training. Small-scale hospitals and clinics often struggle with these costs, especially when integrating new platforms with outdated hospital information systems.

The requirement for customization and regulatory compliance further increases project complexity and delays return on investment. For instance, NHS hospitals in the U.K. reported multi-million-pound overruns during EHR and DMS integration projects due to compatibility issues and extended staff training periods, emphasizing the financial strain of digital transformation in healthcare.

Opportunity Analysis - Rising Adoption by Insurance Providers

Insurance companies are increasingly integrating medical document management systems to streamline claims processing and reduce administrative errors. These platforms enable insurers to securely store and access patient data, verify medical histories, and automate claims validation, significantly improving turnaround time.

With the rising number of digital health records and telemedicine claims, insurers are relying on MDMS to improve transparency and prevent fraudulent activities. For example, leading U.S. insurers have begun integrating AI-enabled document management tools to extract data from complex medical forms, cutting claims processing time by up to 30%.

Developments in Automated Data Conversion

The surging use of unique Optical Character Recognition (OCR) and Intelligent Document Processing (IDP) technologies is transforming the efficiency of medical data handling. These tools allow healthcare facilities to scan, digitize, and convert paper-based medical files into searchable digital formats in bulk.

Recent developments include AI-backed OCR systems capable of reading handwritten notes and structured forms with over 95% accuracy. Hospitals in Europe and Japan are extensively deploying such solutions to digitize decades of legacy patient records, accelerating the shift toward fully paperless healthcare environments.

Category-wise Analysis

Product Type Insights

The service segment is predicted to lead with nearly 56.4% of the share in 2025, as healthcare providers rely heavily on third-party vendors for system integration, maintenance, and staff training. Several hospitals lack in-house IT expertise to manage complex document systems, making outsourced support essential for smooth deployment and regulatory compliance. Service providers also provide customization, software upgrades, and cybersecurity monitoring, ensuring data security under evolving healthcare laws such as HIPAA and GDPR.

Software-based solutions remain central to this market as they automate data storage, retrieval, and indexing processes, replacing traditional manual workflows. Hospitals increasingly adopt integrated software platforms that connect Electronic Health Records (EHRs), laboratory systems, and billing modules for smooth data exchange. Vendors are now developing AI-based solutions that identify errors in medical records or automate coding for insurance claims.

Delivery Mode Insights

The on-premise segment will likely dominate with approximately 41.8% of share in 2025, as it delivers high control over sensitive patient data and superior customization options. Various organizations prefer hosting data within their own secure servers to comply with regional data protection laws such as GDPR in Europe or HIPAA in the U.S. These systems also allow smooth integration with existing hospital IT infrastructure without dependency on external networks.

Cloud-based medical document management is gaining traction due to its extensibility, low upfront cost, and remote accessibility. These systems allow healthcare professionals to access patient records from any location, supporting telemedicine and multi-site coordination. Cloud vendors also deliver built-in disaster recovery and automatic updates, reducing IT maintenance efforts.

Application Insights

A share of 44.6% is expected to be captured by the admission and registration application segment in 2025. Admission and registration processes generate large volumes of patient data that need to be accurately captured, verified, and stored. Document management systems simplify this by digitizing patient forms, ID proofs, and consent papers, enabling quick onboarding and reducing manual errors. Automated data capture tools ensure immediate record creation, which speeds up subsequent care delivery.

Managing billing and insurance documentation is another key application area for MDMS. Automated systems streamline the collection and verification of invoices, claims, and reimbursement papers, minimizing delays and billing disputes. These solutions also help detect discrepancies between clinical records and billing data, ensuring compliance with insurance regulations. For instance, U.S. healthcare providers using AI-based billing document systems have seen claim rejection rates fall by nearly 25%.

Regional Insights

North America Medical Document Management Systems Market Trends

North America is predicted to account for approximately 46.8% of the share in 2025, owing to increasing adoption of digital health technologies and the requirement for efficient management of medical records. In addition, stringent regulatory requirements such as the Health Insurance Portability and Accountability Act (HIPAA), which mandates secure handling of patient information, fuel demand. The increasing volume of healthcare data necessitating efficient storage and retrieval systems is another key driver.

The integration of AI into MDMS is transforming healthcare operations. Abridge, a healthcare start-up, raised US$250 Million to improve its AI-backed medical documentation capabilities, aiming to automate the creation of clinical notes and records from medical conversations.

Consolidation in the healthcare technology sector is also influencing the regional market. In 2025, Clearlake Capital acquired a majority stake in Modernizing Medicine (ModMed), a company providing EHR systems to over 160,000 specialty physicians and surgeons in the U.S.

Europe Medical Document Management Systems Market Trends

In Europe, medical document management is being influenced by superior regulation and cross-border data initiatives, surging concerns around interoperability, and the shift from document-centric systems to data-centric records. One of the prominent changes is the European Health Data Space (EHDS), which became a regulation in early 2025.

It mandates standards and governance for sharing electronic health data across the EU, both for direct care and secondary uses. That means document management systems need to support far stricter rules on consent, data access, metadata, and cross-organization sharing.

There is also investment at the EU level for digital health infrastructure under programs such as EU4Health. It supports interoperability, data exchange pilots, and strengthening national health-IT systems. Another characteristic is that multiple Europe-based health-IT vendors are now providing mobile-optimized or regional-compliance versions of document systems. For example, Dedalus, System C, and ChipSoft have been spotlighted as leading vendors in mobile-EHR or digital document workflows in various countries across Europe.

Asia Pacific Medical Document Management Systems Market Trends

In Asia Pacific, medical document management systems are evolving at a fast pace, backed by government digitization mandates, rising telehealth and AI adoption, and infrastructure upgrades. India, Indonesia, and China are implementing national programs to shift from paper-based to digital health records.

India’s Ayushman Bharat Digital Mission is encouraging hospitals to build EHRs, while Indonesia has made it mandatory for healthcare facilities to adopt electronic medical records by the end of 2023. These regulations are creating a steady demand for digital documentation platforms across public and private hospitals.

Asia Pacific is also seeing steady adoption of cloud-based and AI-based systems that automate document processing and storage. Hospitals are extensively using AI tools to extract and organize medical data, reducing administrative work for staff. In developed markets such as Japan, Australia, and Singapore, integrated MDMS platforms are already being used to connect patient data across healthcare networks. In contrast, developing countries are still in the early stages, focusing on building digital infrastructure and improving interoperability.

Competitive Landscape

The global medical document management systems market consists of key players such as DocuWare, Connecteam, and Box for Healthcare. DocuWare delivers a cloud-based platform with workflow automation and HIPAA-compliant document storage, making it suitable for healthcare facilities.

Connecteam provides secure, cloud-based storage with self-service tools, enabling healthcare workers to create, upload, and access documents. Box for Healthcare is a cloud-based content management system with HIPAA-compliant storage and sharing capabilities, facilitating secure collaboration and easy access to files from any device.

Key Industry Developments

- In October 2025, Becton, Dickinson and Company launched the BD Incada Connected Care Platform. It is a new, extensible, AI-enabled, cloud-based platform that unifies BD device data into an intelligent ecosystem for the first time.

- In October 2025, Regions Bank introduced improved Treasury Management services designed to help healthcare clients automate, streamline, and effectively manage the entire payments process. Regions Healthcare Receivables Services are now powered by MediStreams.

Companies Covered in Medical Document Management Systems Market

- Epic Systems Corporation

- 3M Company

- Henry Schein Medical Systems

- docSTAR

- Treeno

- Cerner Corporation

- GE Healthcare

- Hyland Software Inc.

- athenahealth, Inc.

- Agaram Technologies Pvt Ltd.

- FUJIFILM Holdings Corporation

- Allscripts Healthcare Solutions Inc.

- McKesson Corporation

- Laserfiche

- ThoughtTrace, Inc.

Frequently Asked Questions

The medical document management systems market is projected to reach US$1.6 Billion in 2025.

The launch of cloud-based solutions enabling remote access and collaboration with insurance providers presents key opportunities for market growth.

The medical document management systems market is poised to witness a CAGR of 11.5% from 2025 to 2032.

The launch of cloud-based solutions for remote access and collaboration with insurance providers is a key market opportunity.

Epic Systems Corporation, 3M Company, and Henry Schein Medical Systems are a few key market players.