- Advanced Materials

- Surface Protection Service Market

Surface Protection Service Market Size, Share, and Growth Forecast, 2026 - 2033

Surface Protection Service Market by Service Type (Corrosion Protection Services, Mechanical Protection Services, Electroplating Services, Thermal Spray Services), Application (Pipelines, Hydraulic Shafts & Cylinders, Process & Vessel Equipment, Tanks, Pumps & Compressors), Industry (Oil & Gas, Manufacturing, Mining, Power & Energy, Aerospace & Defense) and Regional Analysis for 2026 - 2033

Surface Protection Service Market Size and Trends Analysis

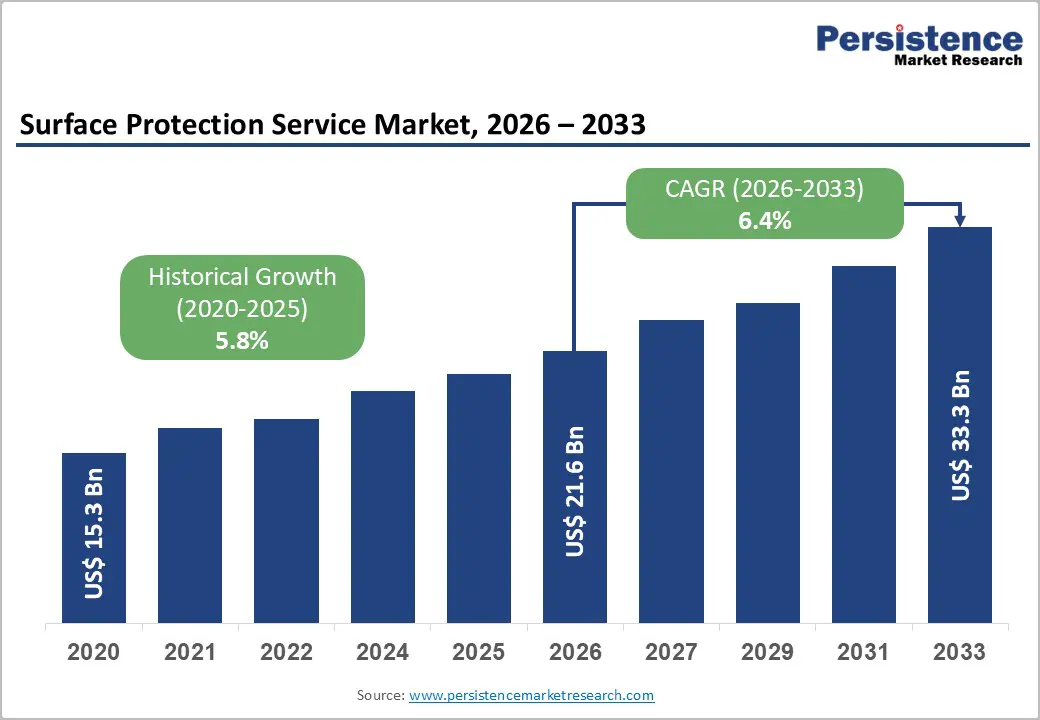

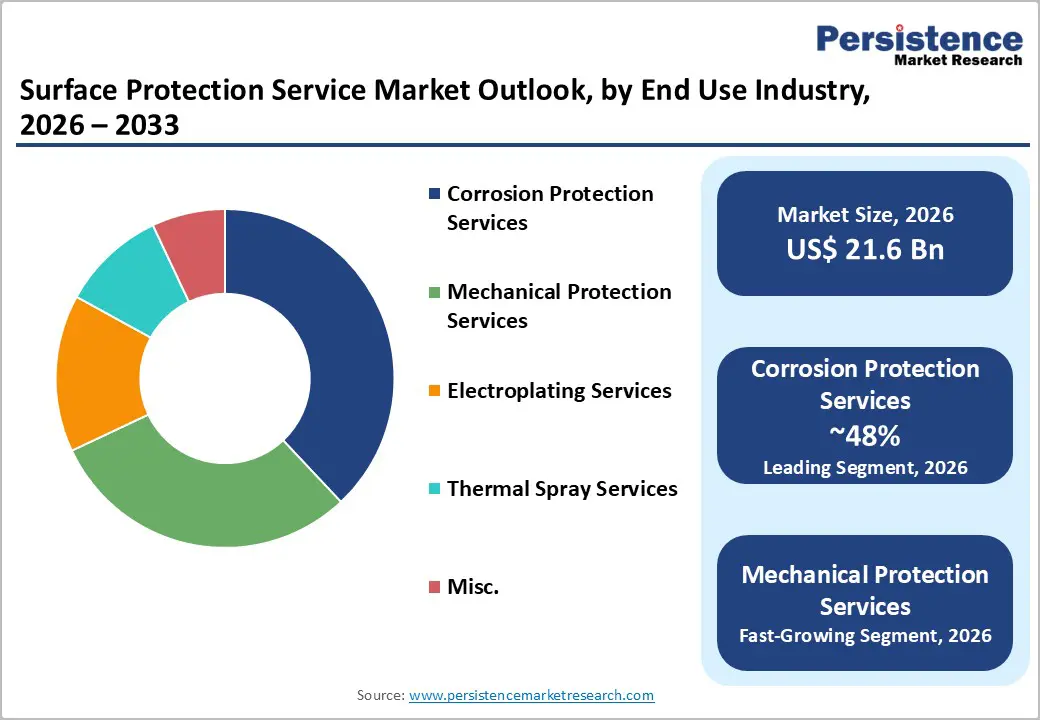

The global surface protection service market size is likely to be valued at US$ 21.6 billion in 2026 and is projected to reach US$ 33.3 billion by 2033, growing at a CAGR of 6.4 percent between 2026 and 2033. The market demonstrated steady historical expansion from US$15.3 billion in 2020 at a historical CAGR of 5.8 percent.

This consistent growth trajectory is driven by infrastructure maintenance requirements for ageing industrial assets, regulatory mandates for corrosion prevention and environmental protection, and technological advancements in coating application methodologies that improve service efficiency and durability.

Key Industry Highlights:

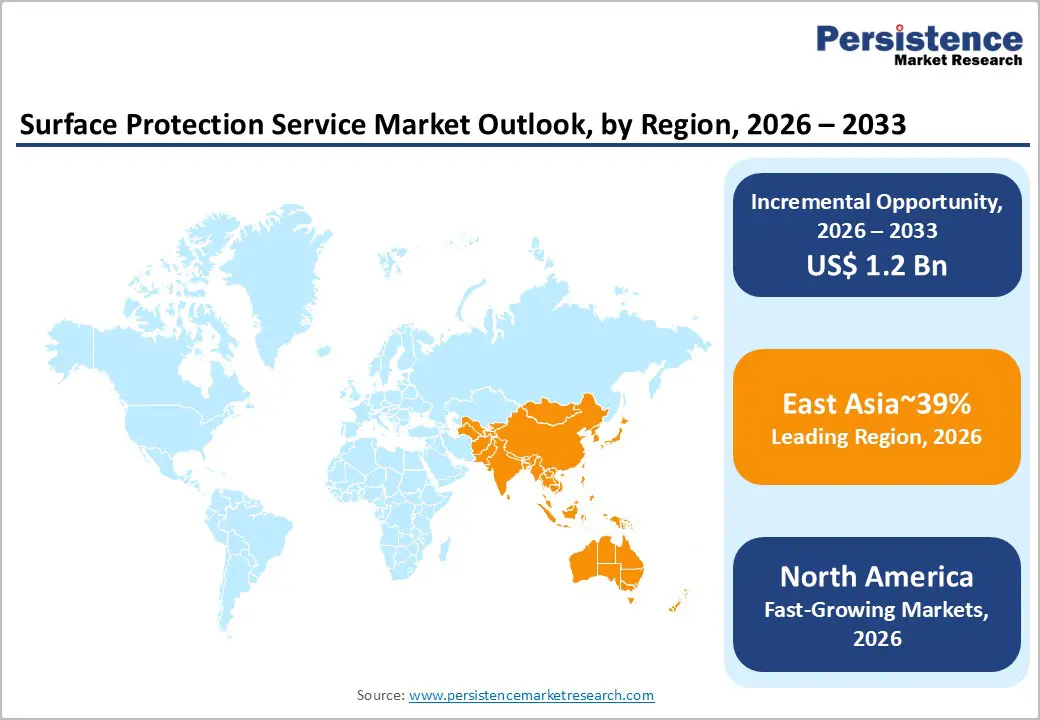

- East Asia Market Scenario: East Asia holds a significant 39% share of the global Surface Protection Service Market, driven by China's leadership in manufacturing expansion, renewable energy deployment, and infrastructure development.

- Dominant Industry: The oil and gas sector remains the largest end-use industry, commanding approximately 40% of the market share, with growing demand for corrosion protection services in upstream, midstream, and downstream operations.

- Dominant Industry: The power and energy sector is the fastest-growing segment, fueled by renewable energy infrastructure deployment, particularly solar PV and offshore wind, alongside growing demand for grid-scale battery storage coatings.

- Growth Indicators: Corrosion protection services account for 48% of the market, with demand driven by the need for protective coatings in harsh environments such as oil, gas, and renewable energy infrastructure.

- Novel Opportunities: The convergence of surface protection services with advanced inspection technologies and IoT-enabled monitoring creates opportunities for integrated, outcome-based service models, driving recurring revenue streams.

- Marine & Offshore Renewable Energy Focus: The expansion of offshore wind and floating solar installations presents a niche market for marine protection services, requiring specialized coatings for saltwater immersion and long-term durability in harsh conditions.

- Aerospace & Defense Demand Surge: The aerospace and defense sector, particularly in Europe, is experiencing significant growth, creating demand for specialized protective coatings for military and commercial aircraft, contributing to market expansion.

| Key Insights | Details |

|---|---|

|

Surface Protection Service Market Size (2026E) |

US$ 21.6 Bn |

|

Market Value Forecast (2033F) |

US$ 33.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Dynamics

Drivers - Infrastructure Asset Lifecycle Extension and Maintenance Imperatives

Asset lifecycle management strategies and preventive maintenance protocols constitute primary demand drivers for the surface protection service market as industrial operators prioritise equipment longevity and operational reliability. According to the International Energy Agency, global oil production capacity is set to expand substantially through 2030, led by non OPEC plus producers including the United States, Brazil, Guyana, Canada, and Argentina contributing 4.6 million barrels per day of net capacity increase, requiring extensive corrosion protection and mechanical integrity services for upstream production facilities, midstream pipeline infrastructure, and downstream refining operations.

The refining sector faces structural pressure as global capacity rises moderately by 3.3 million barrels per day through 2030, with capacity growth concentrated in Asia, particularly China and India, necessitating protective coatings for new installations and maintenance of existing assets. In the aerospace and defence sector, the European industry achieved a turnover of €325.7 billion in 2024, representing 10.1 percent year-over-year growth, with employment expanding by 6.9 percent to nearly 1.103 million employees, supporting demand for specialised protective coatings, ensuring aircraft component durability and corrosion resistance across civil and military applications.

Renewable Energy Infrastructure Deployment and Protection Requirements

The systematic expansion of renewable energy generation capacity creates substantial new demand channels for surface protection services addressing harsh environmental exposure conditions across wind, solar, and energy storage installations. According to the International Energy Agency Tracking Clean Energy Progress report, more than 560 GW of renewable capacity was added in 2023, with annual investment approaching US Dollar 2 trillion, nearly double that of fossil fuel supply investment.

Solar photovoltaic generation saw a remarkable 26 percent growth in annual electricity generation in 2022, while global renewable energy and nuclear sectors accounted for 80 percent of electricity generation growth in 2024, with new renewable capacity additions reaching a record 700 GW, where 80 percent was solar PV. Wind turbine protective coating requirements are substantial, with Hempel protective coatings serving approximately 50 percent of global wind turbines, ensuring longevity in harsh environmental conditions through durable corrosion-resistant formulations, with the company strengthening collaboration with industry players to improve efficiency and reduce environmental impact.

Grid-scale battery storage is projected to expand nearly 35-fold between 2022 and 2030, reaching nearly 970 GW globally, with 170 GW expected to be added in 2030 alone, requiring specialised protective coatings for battery enclosures, thermal management systems, and corrosion protection addressing electrical insulation requirements.

China announced plans to install over 30 GW of energy storage by 2025, while the United States Inflation Reduction Act provides investment tax credits for standalone storage, boosting grid scale storage competitiveness, and India and Australia have set ambitious national targets for battery energy storage deployment. Global investment in battery energy storage exceeded US Dollar 20 billion in 2022, with grid-scale projects accounting for over 65 percent of total spending, expected to exceed US Dollar 35 billion in 2023, driven by expanding project pipelines and government targets. For the Surface Protection Service Market, renewable energy infrastructure expansion represents a high growth demand channel requiring specialised protective solutions addressing ultraviolet radiation exposure, thermal cycling, moisture ingress prevention, and electrochemical corrosion, creating differentiated service opportunities distinct from traditional oil and gas applications.

Restraint - High Capital Investment Requirements and Service Cost Sensitivities

Surface protection service deployment requires substantial upfront capital investments in specialised equipment, certified workforce training, and quality assurance systems, creating barriers for market entry and limiting service provider expansion, particularly in cost-sensitive industrial segments.

Advanced application technologies, including electrostatic spraying, thermal spray systems, and automated coating equipment, demand significant capital outlays ranging from hundreds of thousands to millions of dollars per installation, while workforce certification requirements for specialised techniques, including passive fire protection, aerospace coatings, and nuclear facility applications, necessitate extensive training investments and ongoing competency maintenance programs. Industrial customers facing margin pressures, particularly in mature oil and gas fields, legacy manufacturing facilities, and budget-constrained public infrastructure projects, often prioritise lowest initial cost solutions over lifecycle value optimisation, forcing service providers to compete primarily on price rather than technical differentiation.

According to International Energy Agency projections, global spare oil production capacity could reach unprecedented levels around 8 million barrels per day above projected demand by 2030, creating potential downward pressure on commodity prices and constraining capital expenditure budgets for upstream and midstream infrastructure maintenance, including protective coating services. These cost pressures compound in emerging economies where capital availability constraints and underdeveloped service infrastructure limit adoption of advanced protection solutions despite substantial infrastructure development activity.

Opportunity - Integrated Coating and Inspection Service Delivery Models

The convergence of surface protection services with advanced inspection technologies, including ultrasonic testing, infrared thermography, and drone-based visual assessment, creates differentiated service offerings addressing comprehensive asset integrity management requirements. Industrial operators increasingly demand integrated solutions combining protective coating application with baseline condition assessment, ongoing monitoring, and predictive maintenance analytics, enabling proactive intervention before catastrophic failures occur and optimising maintenance budget allocation across asset portfolios.

Digital technologies, including IoT sensors embedded within coating systems, artificial intelligence-powered defect detection algorithms, and blockchain-based coating history documentation, enable service providers to deliver outcome-based contracts guaranteeing performance thresholds rather than traditional activity-based pricing models. For the surface protection service market, integrated delivery models create opportunities for recurring revenue streams through monitoring subscriptions, premium pricing for comprehensive solutions, and strategic partnerships with asset owners seeking single source accountability for surface protection and integrity management, particularly relevant in aerospace applications where AkzoNobel's €50 million Waukegan facility expansion enhances customization and faster turnaround for maintenance and repair operations supporting commercial and military aircraft fleets.

Category-wise Analysis

Service Type Insights

Corrosion protection services are dominant and are projected to account for 48% of the market in 2026, reflecting the fundamental need to prevent corrosion across industrial infrastructure exposed to moisture, chemicals, saltwater, and atmospheric contaminants, which systematically degrade metal substrates and structural integrity. This segment encompasses comprehensive solutions, including surface preparation through abrasive blasting, chemical conversion coatings, multi-layer protective paint systems, cathodic protection installation, and specialised formulations addressing specific corrosive environments, including sour gas service, marine immersion, and chemical process applications. Hempel's protective coatings serve approximately 50 percent of global wind turbines with durable corrosion-resistant formulations, ensuring longevity in harsh environmental conditions, while the company's ongoing industry collaboration focuses on improving efficiency and reducing environmental impact.

Industry Insights

Oil and gas is likely to account for 40% of the market in 2026, establishing its position as the dominant end-use industry for surface protection services due to its extensive infrastructure footprint, harsh operating environments, and stringent integrity management requirements across upstream production, midstream transportation, and downstream refining operations. This sector demands comprehensive protection solutions addressing hydrogen sulfide corrosion, CO2 corrosion, chloride stress cracking, and mechanical erosion across wellheads, pipelines, storage tanks, pressure vessels, and process equipment operating in desert heat, arctic cold, offshore marine environments, and corrosive process streams.

According to the International Energy Agency, global oil production capacity is set to expand substantially through 2030, led by the United States, Brazil, Guyana, Canada, and Argentina, contributing 4.6 million barrels per day net capacity increase, while global refining capacity rises moderately by 3.3 million barrels per day with growth concentrated in Asia, particularly China and India. Non-crude products, particularly natural gas liquids and condensates, will account for 45 percent of new capacity, reflecting strategic pivots requiring specialised protective coatings for NGL processing facilities and associated infrastructure.

Power and Energy represent the fastest growing end-use industry segment, driven by renewable energy infrastructure deployment, grid modernisation initiatives, and battery energy storage system expansion, creating new protection service requirements beyond traditional thermal power generation applications. According to the International Energy Agency, global electricity consumption surged by nearly 1,100 terawatt hours in 2024, marking the largest increase outside post-recession rebound years, with renewable energy and nuclear sectors accounting for 80 percent of electricity generation growth, and new renewable capacity additions reaching a record 700 GW, where 80 percent was solar PV.

Grid-scale battery storage is projected to expand nearly 35-fold between 2022 and 2030, reaching nearly 970 GW globally, with China planning over 30 GW of energy storage by 2025 and the United States Inflation Reduction Act providing investment tax credits, boosting grid-scale storage competitiveness. Jotun launched specialised powder coating systems in June 2025 for the battery market, addressing electrical insulation, thermal management, fire protection, and corrosion protection, improving battery life, safety, and manufacturing efficiency through collaboration with manufacturers, especially in China.

Regional Insights and Trends

East Asia Surface Protection Service Market Trends

East Asia commands approximately 39% of the global surface protection service market, with China serving as the dominant force in manufacturing capacity expansion, renewable energy deployment, and infrastructure development, driving concentrated demand for comprehensive protective coating services. China's energy demand growth continued in 2024, recording the largest absolute increase in energy consumption globally, with emerging and developing economies contributing over 80 percent of global demand growth.

According to the International Energy Agency (IEA), China accounted for 60 percent of new renewable capacity in 2023, with solar PV generation projected to exceed the total electricity demand of the United States by the early 2030s, creating substantial surface protection requirements for solar mounting structures, inverter enclosures, and associated electrical infrastructure. China announced plans to install over 30 GW of energy storage by 2025, with global battery energy storage investment exceeding US Dollar 20 billion in 2022 and expected to exceed US Dollar 35 billion in 2023, driven by expanding project pipelines and government targets.

The region's manufacturing concentration, renewable energy leadership, infrastructure development velocity, and government policy support position East Asia as the largest and highest growth market for surface protection services through 2033, with China's dominance creating substantial opportunities for both international service providers and domestic competitors developing specialized technical capabilities.

North America Surface Protection Service Market Trends

North America accounts for approximately 26% of the global surface protection service market, driven by mature industrial infrastructure requiring ongoing maintenance, aerospace and defence sector concentration, and renewable energy capacity additions, particularly utility-scale solar and offshore wind deployments. The region benefits from established regulatory frameworks mandating pipeline integrity management, industrial facility maintenance standards, and environmental protection requirements that systematically drive surface protection service demand across oil and gas midstream infrastructure, chemical processing facilities, and manufacturing operations.

AkzoNobel announced a €50 million investment in December 2025 to upgrade its Waukegan, Illinois, aerospace coatings facility, expanding production capacity, automation, and warehousing to strengthen North American supply, enhancing output of high-performance primers, basecoats, clearcoats, and pre-treatment coatings used for aircraft surface protection while improving customisation and faster turnaround for maintenance and repair operations.

Europe Surface Protection Service Market Share and Insights

Europe accounts for approximately 16% of the global market driven by stringent environmental regulations, renewable energy transition initiatives, aerospace and defence sector expansion, and industrial facility modernisation across established manufacturing economies. The European aerospace and defence industry achieved a turnover of €325.7 billion in 2024, representing 10.1 percent year over year growth with employment expanding by 6.9 percent to nearly 1.103 million employees, supporting demand for specialised protective coatings, ensuring aircraft component durability and corrosion resistance.

Competitive Landscape

The global surface protection service market is characterized by a blend of consolidation and fragmentation. Major multinational players like PPG Industries, Hempel, Jotun, AkzoNobel, Sherwin-Williams, and Nippon Paint dominate the market, leveraging their global presence, diverse service portfolios, and long-term relationships with industries such as oil & gas, mining, and power generation. These companies focus on corrosion, thermal spray, and electroplating services, securing large institutional contracts, particularly in offshore and industrial segments.

The market remains fragmented at regional levels, with smaller, specialized firms such as Pristine Surface Coating LLP and KAEFER SE capturing significant business through tailored, cost-effective offerings. These regional players often partner with larger firms for large-scale projects, adding competition within the market. Innovation in advanced coatings, sustainability, and hybrid protection systems drives competition, while geographic coverage and service quality continue to be key competitive factors.

Key Industry Developments

- In July 2025 - PPG announced the completion of its 100th dry docking using electrostatic coating applications for marine hulls, marking a significant milestone in the surface protection service market. The technique, used on the MV Colossus, applies premium antifouling and fouling release coatings, offering improved efficiency and reduced waste. PPG's innovation in electrostatic spraying has led to enhanced distribution, smoother finishes, and environmental benefits, such as reduced fuel consumption and greenhouse gas emissions, strengthening its commitment to sustainability in the marine sector.

- In March 2025 - Hempel A/S launched its latest epoxy Passive Fire Protection (PFP) solution, Hempafire Extreme 550, designed to provide up to four hours of fire resistance for cellulosic fires. This innovative product sets a new benchmark in fire safety, delivering exceptional durability, efficiency, and sustainability, with up to 40% reduction in application effort and CO2 emissions. It is fully compliant with global standards and is particularly suitable for commercial and industrial projects, ensuring long-term performance while reducing costs and environmental impact.

Companies Covered in Surface Protection Service Market

- PPG Industries

- Hempel

- Jotun

- AkzoNobel

- Sherwin-Williams

- Nippon Paint Holdings

- Pristine Surface Coating LLP

- Ecoplast

- KAEFER SE & Co.KG

- BarodA Surface Protection Services

Frequently Asked Questions

The global surface protection service market is projected to be valued at US$ 21.6 Bn in 2026.

The Corrosion Protection Services segment is expected to account for approximately 48% of the Global Surface Protection Service Market by product type in 2026.

The market is expected to witness a CAGR of 6.4% from 2026 to 2033.

The growth of the Surface Protection Service Market is driven by infrastructure asset lifecycle management, maintenance imperatives, and the increasing demand for protective coatings in sectors like oil & gas, aerospace, defense, and renewable energy infrastructure.

Key market opportunities in the Surface Protection Service Market include integrated coating and inspection service delivery models, offering advanced monitoring and predictive maintenance solutions, and specialized protection for marine and offshore renewable energy infrastructure, including offshore wind and floating solar installations.

Key players in the Surface Protection Service Market include PPG Industries, Hempel, Jotun, AkzoNobel, Sherwin-Williams, and Nippon Paint.