- Oil & Gas

- Surface Mining Market

Surface Mining Market Size, Share, and Growth Forecast, 2026 - 2033

Surface Mining Market by Commodity (Coal, Iron Ore, Copper & Base Metals, Precious Metals, Bauxite, Uranium & Battery Metals, Others), Propulsion (Diesel, Diesel-Electric/Hybrid, Battery-Electric, Trolley-Assist, Others), Application (Haulage, Loading & Excavation, Drilling & Blasting, Crushing & Screening, Conveying & Material Handling, Surface Support), and Regional Analysis for 2026 - 2033

Surface Mining Market Share and Trends Analysis

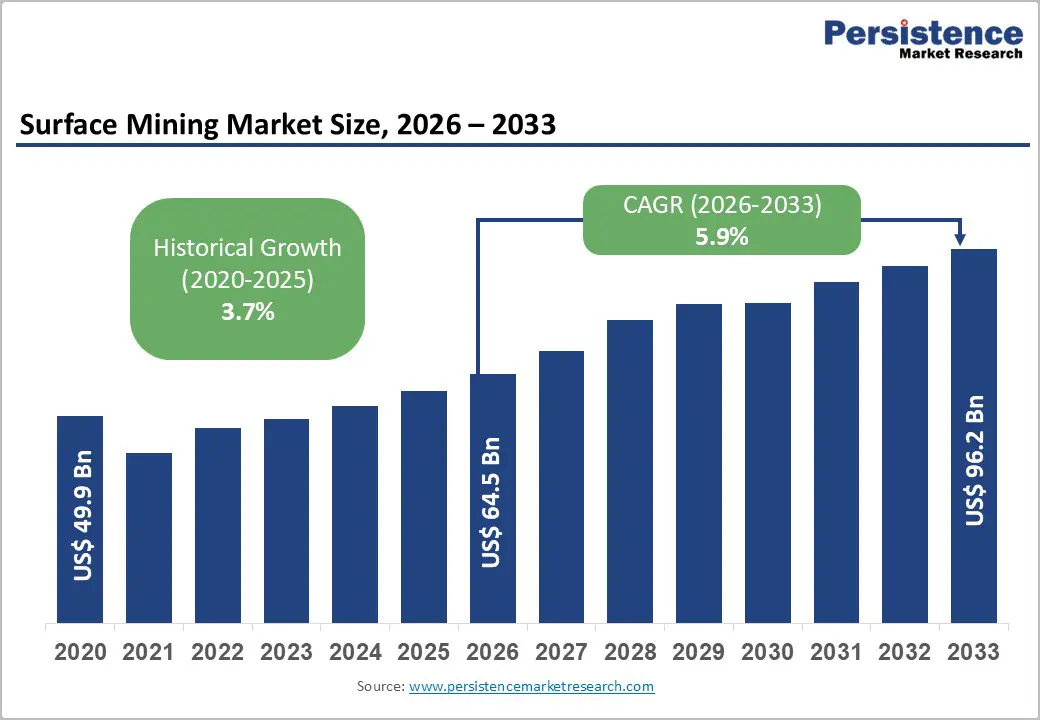

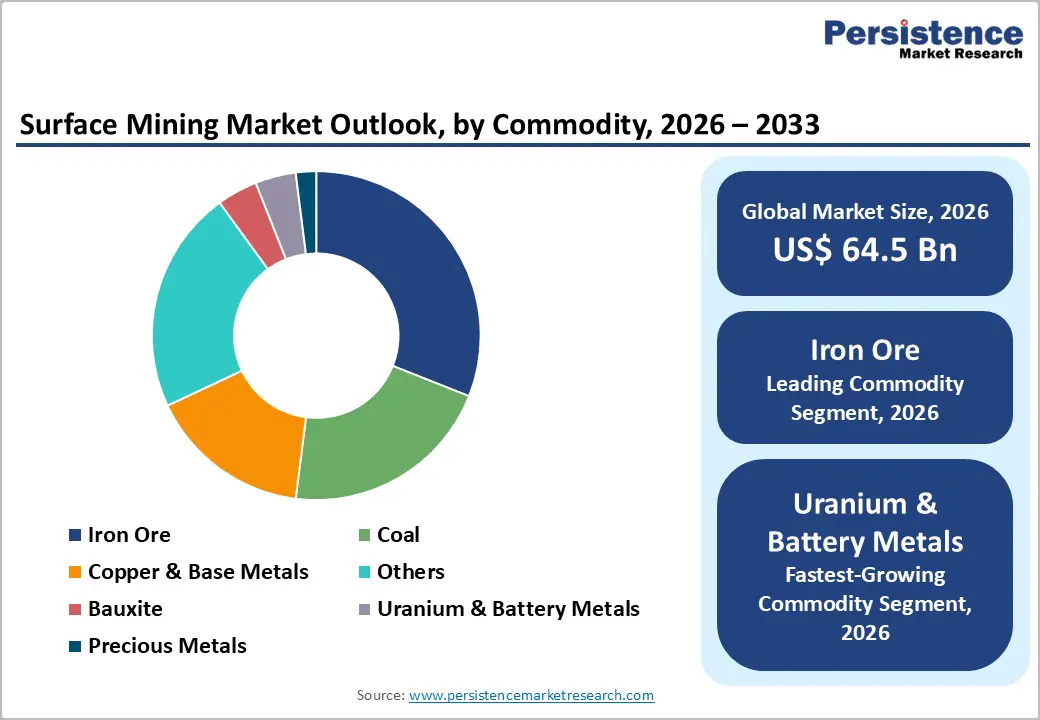

The global surface mining market size is likely to be valued at US$ 64.5 billion in 2026, and is estimated to reach US$ 96.2 billion by 2033, growing at a CAGR of 5.9% during the forecast period 2026 - 2033.

With mining companies increasing capital allocation to large open-pit operations and technology upgrades, the market is poised for steady expansion. Demand is strengthening across iron ore, copper, and construction aggregates as governments are continuing to fund infrastructure programs and energy transition initiatives. Mining operators are modernizing fleets to improve productivity and cost efficiency, and this shift is increasing average equipment values rather than simply raising unit volumes. As a result, revenue growth is increasingly reflecting technology intensity rather than extraction expansion alone. Capital expenditure among the top 40 global mining companies has been rising, as per industry reports, with automation and decarbonization investments accounting for a growing proportion of total equipment budgets.

Diesel-powered machinery maintains the majority of the installed base, yet battery-electric, diesel-electric, and trolley-assist systems are expanding at faster rates as companies pursue emission-reduction targets and fuel-cost optimization. Original equipment manufacturers (OEMs) are integrating digital fleet management, predictive maintenance platforms, and electrified haulage systems to strengthen recurring service revenues. Market performance is increasingly shaped by integrated service contracts, retrofit programs, and energy-efficient platforms, creating clear strategic advantages for suppliers that align their technology portfolios with regulatory and cost-transformation trends.

Key Industry Highlights

- Dominant Commodity: Iron ore is likely to dominate with approximately 29% of global market revenue in 2026, owing to massive steel demand in Asia Pacific and large-scale open-pit operations in Australia and Brazil.

- Fastest-Growing Commodity: Uranium and battery metals are expected to register a 2026 - 2033 CAGR of about 8.5%, driven by accelerating energy transition policies.

- Leading Propulsion: Diesel-powered equipment is estimated to hold roughly 68% revenue share in 2026, reflecting installed base inertia and established refueling infrastructure, while battery-electric equipment is projected to record the highest 2026-2033 CAGR.

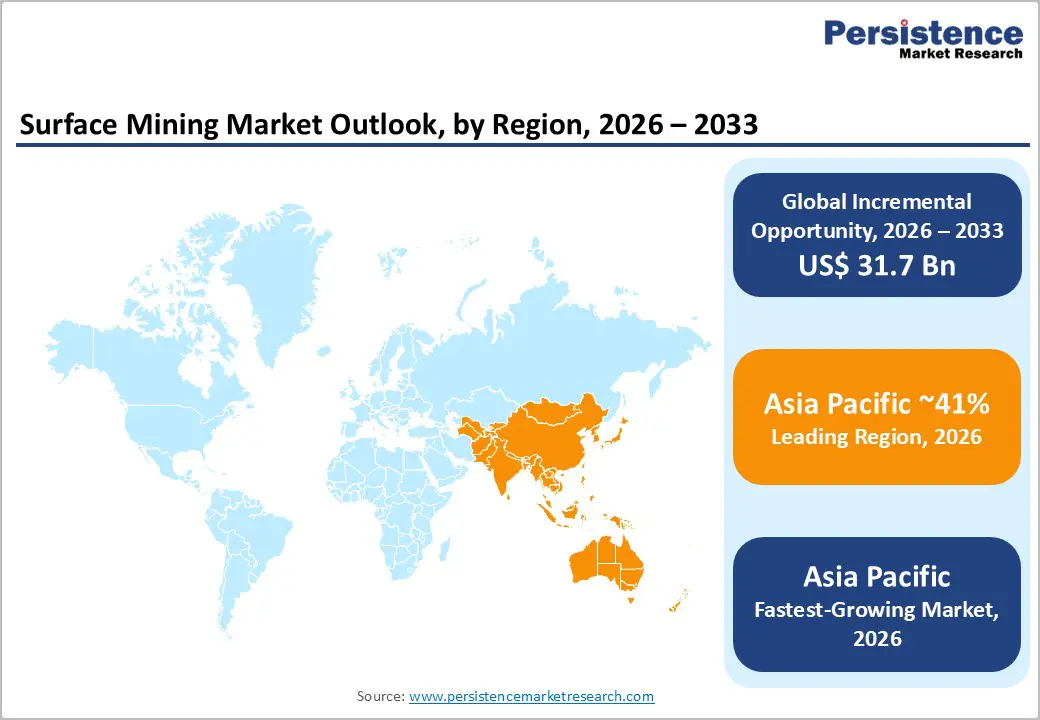

- Dominant Region: Asia-Pacific is positioned to dominate the market, with an estimated 41% share in 2026, supported by iron ore exports from Australia and by coal and mineral output from China and India.

- Fastest-Growing Market: Asia Pacific is forecast to be the fastest-growing market at around 6.7% through 2033, underpinned by infrastructure-led mineral demand.

- Competitive Trend: A strategic emphasis on electrification, autonomous haulage systems, and digital fleet management, with leading OEMs strengthening aftermarket service portfolios, is shaping the market's competitive landscape.

- August 2025: Sandvik Mining launched a new AutoMine Surface Drilling Training Simulator to accelerate operator competence and improve the efficiency and safety of automated surface drilling operations.

| Key Insights | Details |

|---|---|

| Surface Mining Market Size (2026E) | US$ 64.5 Bn |

| Market Value Forecast (2033F) | US$ 96.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors - Growth, Barriers, Opportunity Analysis

Electrification of Ultra-Class Haul Fleets to Restructure Capital Allocation in Surface Mining

Mining operators are accelerating the transition toward diesel-electric, trolley-assist, and battery-electric haulage platforms as carbon pricing systems and Scope 1 emission reduction targets are tightening across major jurisdictions. The International Energy Agency (IEA) estimates that mining is responsible for 4-7% of global energy-related industrial emissions, which is placing measurable pressure on operators to decarbonize extraction activities. At the same time, more than 70% of the top 40 mining companies are committing to net-zero targets by 2050, according to the International Council on Mining and Metals (ICMM). Ultra-class haul trucks are consuming nearly 3,000 to 4,000 liters of diesel per unit per day, and fuel expenses are accounting for 20-30% of total operating expenditure in open-pit operations, as outlined in recent industry reports. Electrified haulage systems are therefore reducing exposure to oil price volatility while improving cost predictability. Operators are prioritizing capital allocation toward lower-emission fleets to manage regulatory compliance and long-term margin stability.

Governments are reinforcing this transition by implementing carbon border adjustment mechanisms such as the European Union Carbon Border Adjustment Mechanism (EU CBAM), which is incentivizing low-emission mineral supply chains. Australia and Canada are providing tax incentives and infrastructure support for mining electrification projects, thereby lowering upfront investment barriers. Original equipment manufacturers are introducing 240-300 metric-ton battery-electric haul truck platforms and expanding trolley-assist deployments in copper-producing regions, such as Chile. These technology shifts are increasing average selling prices per unit and are raising lifecycle service revenue potential. Electrification is not reflecting a short-term commodity cycle response; it is restructuring capital planning and procurement frameworks. Fleet modernization programs are expected to materially increase equipment value density, strengthen aftermarket service integration, and improve revenue visibility for suppliers aligned with decarbonization mandates.

Permitting Delays and ESG Compliance to Extend Project Development Cycles

Surface mining projects are experiencing extended environmental and social approval cycles across major producing regions. The World Bank is estimating that large-scale mining developments are requiring between seven and ten years from initial discovery to commercial production within member countries of the Organisation for Economic Co-operation and Development (OECD). In the United States, federal permitting under the National Environmental Policy Act (NEPA) is frequently exceeding five years, particularly for projects involving federal land or water access. European operators are complying with stricter water abstraction and discharge standards under the European Union Water Framework Directive, which is lengthening approval procedures. In Latin America, community consultations and social-licensing negotiations are delaying expansions of copper and lithium capacity. These regulatory and stakeholder requirements are increasing pre-production risk and are extending capital payback horizons.

Capital intensity continues to remain elevated across open-pit developments. For instance, ultra-class haul trucks cost between US$ 3 million and US$ 5 million per unit, while electrification infrastructure such as substations and charging systems is adding approximately 15-20% to upfront capital expenditure. Higher benchmark interest rates since 2022 are increasing the weighted average cost of capital for mining companies, thereby tightening investment thresholds. Supply chain bottlenecks are persisting in high-voltage power electronics, specialized steel components, and advanced control systems, which is extending original equipment manufacturer delivery timelines. These constraints are limiting near-term production growth, particularly among junior and mid-tier operators with restricted financing access. Regulatory tightening is likely to further stiffen entry barriers, reinforcing industry consolidation while reducing short-term expansion flexibility.

Critical Minerals Expansion in Emerging Economies to Create Huge Fleet Modernization Demand

The IEA projects that the demand for lithium, nickel, cobalt, and copper may increase between two and four times by 2030 under stated energy transition policies. Emerging economies such as Indonesia, Chile, and the Democratic Republic of Congo are expanding surface mining capacity to meet this anticipated supply gap. Indonesia is enforcing downstream mineral processing mandates that are accelerating new open-pit nickel developments, while Chile is sustaining copper output above 5 million metric tons annually according to the United States Geological Survey (USGS). These production levels are requiring continuous fleet renewal and productivity optimization. Battery mineral extraction is typically operating with lower strip ratios compared to bulk commodities, yet operators are requiring high-precision drilling and selective ore recovery to maintain grade quality. As a result, mining companies are deploying automation-ready drill rigs and electric excavators to improve recovery rates and reduce dilution.

Fiscal regimes in emerging markets are increasingly supporting mineral investment through tax incentives and infrastructure co-investment programs. The African Development Bank (AfDB) highlights that mining capital inflows across the continent are rising as governments are prioritizing resource monetization. The commercial opportunity is extending beyond greenfield fleet procurement and is increasingly encompassing retrofit programs for electrification and autonomy. Operators are converting legacy diesel haul trucks to trolley-assist configurations to lower fuel consumption and emissions intensity, thereby generating incremental service and upgrade revenues for original equipment manufacturers. Suppliers that are integrating electrified haulage systems and autonomous drilling technologies can strengthen their competitive positioning as fleet modernization accelerates across resource-rich developing economies.

Category-Wise Analysis

Commodity Insights

Iron ore is expected to lead in 2026 with an estimated 31% of the surface mining market revenue share. This dominance is continuing as steel consumption in Asia Pacific is supporting sustained extraction volumes. China, India, and Southeast Asian economies are investing in transportation networks, urban housing, and industrial corridors, which is reinforcing bulk commodity demand. The USGS reports that global iron ore production above 2.6 billion metric tons annually, reflecting stable output levels. Iron ore operations are typically large-scale and are requiring high-capacity haul trucks, electric rope shovels, and extensive material handling systems. Australia and Brazil are maintaining strong export performance, and replacement cycles in these mature mining hubs are sustaining capital expenditure. The sheer size of open-pit iron ore mines is ensuring that fleet intensity remains high, which is preserving this segment’s revenue leadership.

Uranium and battery metals are slated to emerge as the fastest-growing commodities between 2026 and 2033, showcasing a CAGR of approximately 8.5%. Energy transition frameworks are increasing long-term demand visibility for copper, nickel, lithium, and cobalt. The IEA confirms that critical mineral demand growth is exceeding the broader mining sector average under stated policy pathways. Surface extraction for battery-related minerals is expanding across Indonesia, Chile, and several African jurisdictions as governments are strengthening supply chain resilience strategies. New projects are prioritizing electrified fleets and digital mine management systems from the outset, which is increasing technology penetration rates. Long-term offtake agreements and policy-backed investment programs are reducing demand uncertainty, thereby improving capital allocation confidence. This segment is foreseen to enlarge its share through 2033, as decarbonization policies and electrification targets continue to influence mineral procurement strategies.

Propulsion Insights

Diesel-powered equipment is poised to dominate by holding approximately 68% of the surface mining market share in 2026. This dominance is reflecting the scale of the existing installed base and the operational familiarity that mining companies are maintaining with internal combustion platforms. Fleet replacement cycles are progressing gradually because large open-pit operations are prioritizing asset utilization over rapid turnover. Original equipment manufacturer disclosures are confirming that diesel configurations are still representing the majority of equipment deliveries by value. Remote mining regions are lacking grid connectivity and high-capacity charging infrastructure, which is reinforcing reliance on conventional fuel systems. In several jurisdictions, logistics networks are already structured around diesel distribution, which is reducing short-term transition urgency. Operators are therefore continuing to allocate capital toward proven diesel systems while evaluating long-term decarbonization pathways.

Battery-electric equipment is anticipated to become the fastest-growing propulsion between 2026 and 2033. Manufacturers are scaling pilot deployments of battery-electric haul trucks and excavators in countries such as Australia and Canada, where mining electrification programs are advancing. The IEA and the ICMM are influencing adoption through modelled climate and emission reduction scenarios, nudging the adoption of battery-powered mining machinery and equipment. Governments are offering fiscal incentives, tax credits, and infrastructure grants that are lowering initial investment barriers for electrified fleets. Although upfront acquisition costs remain elevated, operators are offsetting these expenditures through lower fuel consumption, reduced maintenance complexity, and improved energy efficiency over the equipment lifecycle. As cost curves improve and regulations bolster adaptability, electrified mining equipment will continue to gain traction during the 2026-2033 forecast period.

Application Insights

Haulage is predicted to be the leading application for surface mining equipment in 2026, likely to capture an estimated revenue share of 34%. Haul trucks are commanding the largest capital allocation since unit prices are significantly higher than most other surface mining assets. Ultra-class platforms deployed in iron ore and copper operations are requiring substantial upfront investment, and these fleets are forming the backbone of material movement in large open-pit sites. Mining companies are allocating capital toward replacement and capacity expansion programs to maintain throughput targets. Electrification initiatives are further increasing average selling prices per unit, as diesel-electric and battery-electric configurations are incorporating advanced power systems and digital monitoring tools. This trend is raising revenue intensity per vehicle rather than simply expanding fleet size, resulting haulage operations continuing to anchor overall market performance through value concentration and technology integration.

Drilling and blasting applications are slated to grow the fastest from 2026 to 2033, as mining operators are actively deploying automation and precision drilling technologies to improve ore recovery rates and reduce dilution. Surface extraction for battery minerals such as lithium and nickel is requiring selective targeting of high-grade deposits, which is increasing demand for advanced drill rigs with real-time data capability. Autonomous drill platforms are enhancing workforce safety by limiting exposure to hazardous zones while also improving operational consistency. These systems are reducing cycle time variability and are supporting predictive maintenance through digital integration. Automated drilling technologies are anticipated to deepen their presence and amplify their reach across both mature and emerging mining regions, enhancing productivity gains and increasing technology-driven revenue share.

Regional Insights

North America Surface Mining Market Trends

North America is expected to account for an estimated 22% of the surface mining market share in 2026 and is projected to expand at a moderate CAGR through 2033. The United States and Canada are increasing investment in copper and lithium production under the Inflation Reduction Act (IRA), which is prioritizing domestic critical mineral supply chains. Federal infrastructure programs are sustaining demand for construction aggregates, particularly for transportation corridors, grid upgrades, and public works projects. Mining companies are aligning capital expenditure plans with mineral security objectives, and this alignment is strengthening medium-term equipment demand visibility. Although permitting complexity under the NEPA is extending project timelines, fiscal incentives and strategic mineral designations are encouraging resource development. This policy framework is supporting steady fleet modernization rather than rapid expansion.

OEMs are also maintaining a strong operational footprint across North America, supported by established distribution networks and service centers. Electrification pilots are progressing in copper and lithium operations, particularly in Canada, where mining companies are integrating battery-electric haul trucks and digital fleet management systems. Government-backed funding programs are reducing the financial burden of early-stage electrification infrastructure. Operators are prioritizing productivity optimization and emission reduction simultaneously, which is increasing demand for advanced equipment platforms. The regional market is also gaining significantly through high-value mineral production, exhibiting stable growth driven by infrastructure demand, technology adoption, and supply chain reshoring strategies.

Europe Surface Mining Market Trends

Europe is forecast to represent approximately 15% of the surface mining market value in 2026. Overall extraction volumes in the region are notably lower than those in Asia Pacific and North America, yet operators are modernizing assets at a faster technological pace. The EU CBAM and tightening emissions standards under the European Green Deal are accelerating the shift toward low-carbon mining operations. Companies are prioritizing electrified haulage systems, digital monitoring platforms, and energy-efficient processing equipment to comply with regulatory requirements. Although new project approvals are progressing cautiously due to environmental scrutiny, existing operations are upgrading fleets to reduce carbon intensity. This modernization trajectory is supporting steady equipment demand despite moderate volume growth.

Nordic countries are playing a central role in battery metal extraction within the region. Sweden and Finland are expanding nickel, cobalt, and rare earth projects to strengthen strategic mineral independence. Governments are supporting exploration and processing investments through sustainability-linked financing mechanisms. Market expansion is occurring at a cautious. However, technology penetration is high relative to global averages. Mining companies are adopting autonomous drilling systems and hybrid power solutions earlier in the asset lifecycle. During the 2026-2033 forecast period, Europe will have consolidated its position as a technologically advanced mining jurisdiction where regulatory compliance, electrification, and digital integration are shaping capital allocation decisions more strongly than output growth alone.

Asia Pacific Surface Mining Market Trends

Asia Pacific is anticipated to command approximately 41% of the surface mining market value in 2026, and is projected to expand at a CAGR of about 6.7% through 2033. Australia, China, and India dominate production volumes across iron ore, coal, and industrial minerals. Strong infrastructure investment in transportation networks, urban development, and energy systems is sustaining demand for construction aggregates and bulk commodities. Australia is maintaining its position as a leading iron ore exporter, supplying large-scale open-pit operations that are requiring high-capacity haulage and material handling systems. China and India are supporting domestic mineral extraction to meet industrial growth requirements. These factors are reinforcing steady capital deployment across surface mining fleets in the region.

Indonesia is emerging as a strategic nickel production hub, supported by downstream processing mandates and battery supply chain investments. This shift is accelerating open-pit developments and increasing demand for modernized excavation and drilling equipment. Fleet renewal programs are progressing as operators are integrating automation, digital monitoring platforms, and electrified haulage systems to improve productivity and reduce emissions intensity. Regional governments are also encouraging mineral self-sufficiency and export competitiveness through targeted industrial policies, further bolstering the role of Asia Pacific as the primary growth engine of this market.

Competitive Landscape

The global surface mining equipment market structure features moderate consolidation, with a limited group of multinational manufacturers, such as Caterpillar, Komatsu, Epiroc, and Sandvik, controlling a substantial portion of total revenue. Industry concentration is reflecting high capital intensity, advanced engineering requirements, and global distribution scale advantages. Barriers to entry are remaining elevated due to the need for extensive manufacturing capacity, established dealer networks, and long-term service infrastructure. Competition is occurring primarily among large original equipment manufacturers with diversified product portfolios spanning haulage, loading, drilling, and material handling systems. Regional players and specialized manufacturers are participating in niche categories, particularly in aggregates and mid-size equipment segments, yet large integrated suppliers are continuing to dominate ultra-class and high-value applications.

The competitive environment is shifting toward technology differentiation rather than volume-based rivalry. Manufacturers are integrating digital fleet management platforms, automation systems, and electrification solutions into core equipment offerings to strengthen value propositions. Lifecycle service integration is becoming central to strategy, as aftermarket activities such as spare parts supply, maintenance contracts, and performance monitoring are generating recurring revenue streams and improving customer retention. Buyers are prioritizing suppliers capable of delivering end-to-end solutions that combine hardware, software, and service support under unified contracts.

Key Industry Developments

- In December 2025, Epiroc collaborated with Cal-Nevada Precision Blasting to supply surface drilling equipment for mining operations in the U.S., aiming to enhance drilling productivity and support efficient fragmentation outcomes. The partnership will combine Epiroc’s drilling platforms with localized service support to strengthen equipment availability and optimize drilling performance for surface mining contractors and operators.

- In October 2025, BEML signed a MoU with Italy’s Tesmec to introduce advanced surface miner equipment for mining applications in India, marking a strategic collaboration to modernize open-cast extraction techniques. The partnership will bring machinery that cuts and crushes rock and soil without drilling or blasting, enhancing operational efficiency.

- In September 2025, Cummins and Komatsu partnered to accelerate hybrid and low-carbon powertrain solutions for haul trucks in mining, aiming to reduce greenhouse gas emissions and improve fuel efficiency. The collaboration will combine Cummins’ hybrid powertrain systems with Komatsu’s mining equipment platforms to support the industry’s decarbonization goals.

Companies Covered in Surface Mining Market

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Epiroc AB

- Hitachi Construction Machinery Co., Ltd.

- Liebherr-International AG

- Volvo Construction Equipment AB

- SANY Heavy Industry Co., Ltd.

- XCMG Group

- Metso Corporation

- ThyssenKrupp AG

- Doosan Infracore Co., Ltd.

- Astec Industries, Inc.

- Terex Corporation

Frequently Asked Questions

The global surface mining market is projected to reach US$ 64.5 billion in 2026.

Increasing capital allocation toward large open-pit operations, consistently high global demand for iron ore, copper, and construction aggregates, and electrification of fleets by mining companies are driving the market.

The market is poised to witness a CAGR of 5.9% from 2026 to 2033.

Growing adoption of digital fleet management solutions, predictive maintenance platforms, and electrified haulage systems by OEMs, and implementation of retrofit programs are key market opportunities.

Caterpillar Inc., Komatsu Ltd., Sandvik AB, and Epiroc AB are some of the key players in the market.