- Food Ingredients & Additives

- Soy Protein Concentrate Market

Soy Protein Concentrate Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Soy Protein Concentrate Market by Form (Dry/Powder, Liquid), by Nature (Organic, Conventional), by End Use (Food Products, Beverages, Dietary Supplements, Nutraceuticals, Animal Feed, Cosmetics & Personal Care, Pharmaceuticals, Others), and Regional Analysis, 2026 - 2033

Soy Protein Concentrate Market Share and Trends Analysis

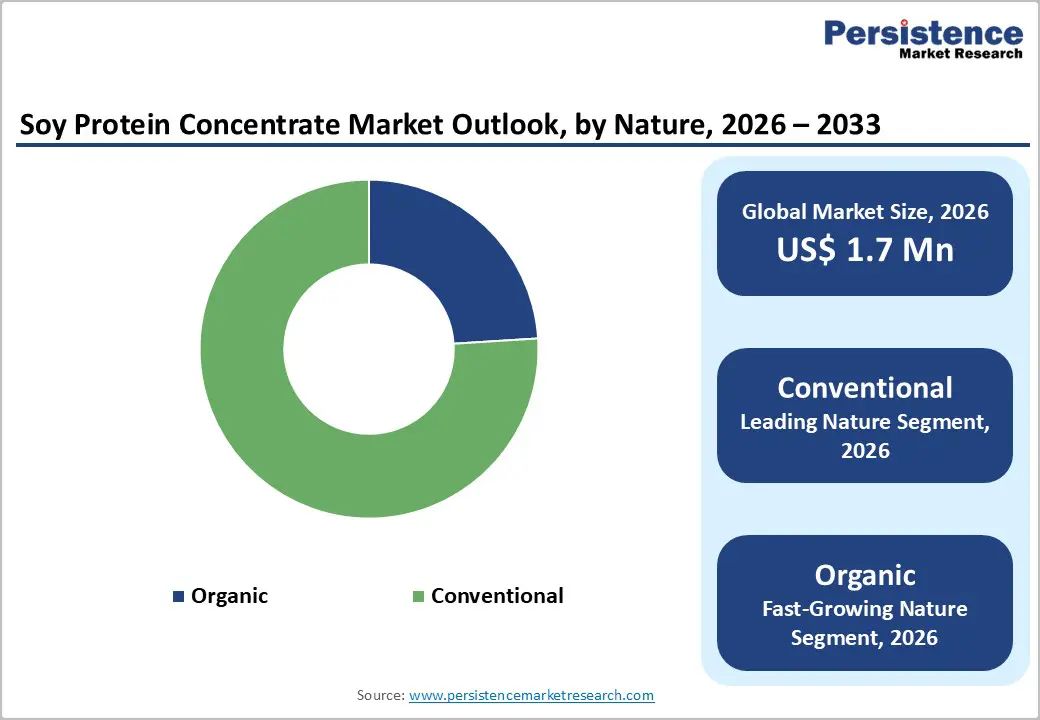

The global soy protein concentrate market size is expected to be valued at US$ 1.7 million in 2026 and projected to reach US$ 3.1 million by 2033, growing at a CAGR of 9.2% between 2026 and 2033.

The growth is primarily driven by the exponential surge in the plant-based protein sector and the intensifying consumer focus on nutritional density. As global dietary patterns shift toward flexitarianism, soy protein concentrate (SPC) has emerged as a critical functional ingredient owing to its high protein content (typically 65%-70%) and its ability to enhance texture in meat analogues. Furthermore, the expansion of the aquaculture industry, which increasingly utilizes SPC as a sustainable alternative to fishmeal, is providing a robust secondary growth engine.

Key Industry Highlights:

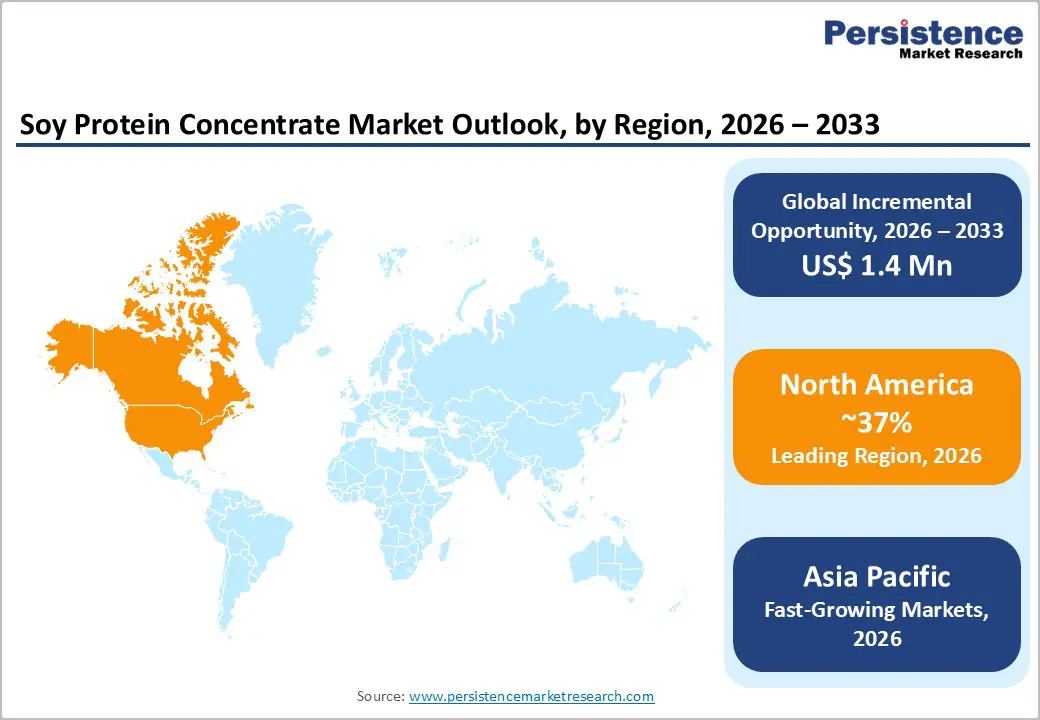

- Leading Region: North America held a 37% market share in 2025, supported by robust soybean production, advanced processing infrastructure, and a mature plant-based food industry.

- Fastest-Growing Region: Asia-Pacific is the fastest-growing regional market, driven by the rapid expansion of the aquaculture industry and rising protein demand in China and India.

- Dominant Segment: The conventional nature segment accounted for 76% of the market in 2025 due to its cost-effectiveness and widespread use in mass-market applications.

- Fastest-Growing Segment: The Organic segment is experiencing the highest CAGR, driven by clean-label consumerism and

- rising demand for non-GMO and chemical-free protein sources.

- Key Market Opportunity: The development of highly soluble SPC for the Sports Nutrition and Beverages sector presents a significant high-margin growth avenue for global manufacturers.

| Key Insights | Details |

|---|---|

|

Global Soy Protein Concentrate Market Size (2026E) |

US$ 1.7 Bn |

|

Market Value Forecast (2033F) |

US$ 3.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Dynamics

Driver - Rising Adoption of Plant-Based Diets and Meat Alternatives

The primary driver of the soy protein concentrate marke is the global shift toward plant-based nutrition, driven by health consciousness and environmental sustainability. According to the International Food Information Council (IFIC), a significant proportion of consumers actively seek clean-label protein sources that provide a complete amino acid profile. SPC is highly valued in the production of meat analogues, such as plant-based burgers and sausages, because it provides the necessary fibrous texture and water-binding capacity required to mimic animal muscle. Major food manufacturers are increasingly reformulating products to replace synthetic additives with functional plant proteins. This trend is particularly pronounced in developed economies, where the vegan and flexitarian populations are expanding, necessitating large-scale procurement of high-quality soy concentrates.

Restraints - Sensitivity to Raw Material Price Volatility and Trade Geopolitics

The market faces significant barriers due to the volatility of soybean prices, which are influenced by climatic conditions and international trade tensions. For instance, the United States Department of Agriculture (USDA) has noted that soybean prices can fluctuate significantly depending on harvest yields in the U.S. and Brazil. Furthermore, retaliatory tariffs and geopolitical friction between major exporting and importing nations can disrupt supply chains overnight. Since Soy Protein Concentrate requires intensive processing, any increase in raw commodity prices or energy costs for extraction plants directly affects manufacturers' profit margins, potentially slowing the rate of new capacity installations in price-sensitive regions.

Opportunity - Technological Innovations in Clean-Label Extraction Processes

Manufacturers have a vast opportunity to gain market share by investing in green extraction technologies, such as aqueous alcohol wash and membrane-based separation. These methods eliminate the need for harsh chemical solvents, aligning with the clean-label trend where consumers demand minimal processing. For example, Ingredion Incorporated and Bunge Limited are focusing on processes that preserve the natural integrity of the soy protein while removing the beany off-flavors that have traditionally hindered consumer acceptance. Developing SPC with improved sensory profiles, specifically neutral taste and white color, will unlock massive potential in the premium bakery and confectionery segments, where soy protein can be used to fortify breads and snacks without compromising the final product's flavor.

Category-wise Analysis

Form Insights

The dry/powder segment held the leading position in the soy protein concentrate market in 2025, accounting for approximately 74%. The dominance of this segment is justified by the superior shelf-stability and logistical advantages of powdered proteins. In industrial food processing, the powder form is highly versatile, allowing for precise dosing in dry-mix applications such as bakery products, meat extenders, and protein supplements. Furthermore, the dry/powder form is the industry standard for Animal Feed and aquaculture, where it is blended into pellets. While the Liquid segment is growing, driven by the surge in plant-based milk and high-protein beverages, the inherent ease of storage and longer shelf life of the powder form ensure its continued dominance in the global marketplace.

Nature Insights

The conventional segment led in 2025, accounting for 76% share. This dominance is primarily due to the established global supply chains for conventional soybeans and to significantly lower production costs relative to organic varieties. For large-scale applications such as Animal Feed and mass-market food processing, the cost-effectiveness of conventional SPC is the deciding factor. However, the Organic segment is the fastest-growing category. According to the Organic Trade Association (OTA), consumer demand for chemical-free and non-GMO products is increasing at double-digit rates. Health-conscious consumers in developed regions are willing to pay a premium for organic-certified plant proteins, prompting brands to launch premium lines of organic soy-fortified products.

Region-wise Insights

North America Soy Protein Concentrate Market Trends and Insights

North America is the dominant regional market, accounting for 37% of the market in 2025. The region's leadership is anchored by the United States, a major producer of soybeans. The American Soybean Association notes that the domestic soy processing infrastructure is highly advanced, with companies such as ADM and Cargill Inc. operating state-of-the-art extrusion and concentration facilities. Innovation in this region is driven by a mature meat-alternative ecosystem, where Silicon Valley startups and established food giants collaborate to create next-generation plant-based products.

Furthermore, the regulatory framework in North America, overseen by the FDA, provides clear guidelines for labeling plant-based proteins, fostering consumer trust. The presence of a massive fitness and sports nutrition culture in the U.S. and Canada ensures a steady demand for protein-fortified snacks and supplements. Strategic investments in clean-label technology and a strong focus on sustainability, such as regenerative farming practices promoted by the United Soybean Board, further solidify North America's position as a global innovation hub for the soy protein concentrate marke.

Europe Soy Protein Concentrate Market Trends and Insights

The European market is characterized by stringent regulations regarding GMO labeling and a profound consumer shift toward non-animal proteins. Countries such as Germany, the U.K., and France are at the forefront of the European Green Deal, which aims to reduce the food system's environmental footprint. This has led to a significant increase in the adoption of non-GMO Soy Protein Concentrate in the bakery and meat-substitute sectors. European consumers are particularly sensitive to the origin of their food, leading to a rise in locally sourced soy initiatives across the EU.

Regulatory harmonization through the EFSA ensures high safety standards, which have boosted the use of SPC in Pharmaceuticals and specialized clinical nutrition. The region is also a major center for aquaculture innovation, particularly in the Nordic countries, where SPC is extensively used in salmon feed. The European market is expected to remain a premium segment, focusing on high-purity, sustainable, and ethically sourced concentrates that meet the rigorous requirements of the Farm to Fork strategy.

Asia Pacific Soy Protein Concentrate Market Trends and Insights

Asia-Pacific is the fastest-growing region for the market, driven by rapid urbanization and a burgeoning middle class in China, India, and ASEAN countries. The Food and Agriculture Organization (FAO) reports that Asia accounts for over 90% of global aquaculture production, creating substantial and growing demand for high-quality soy-based feed. As the regional livestock industry modernizes, there is a clear transition from traditional soy meal to more refined Soy Protein Concentrate to improve animal health and production efficiency.

In the human nutrition sector, China and Japan are leading the adoption of soy-based functional foods. In India, rising awareness of protein deficiency among the vegetarian population is driving demand for soy-fortified staples. The regional market benefits from significant manufacturing advantages, including a large soybean cultivation base and expanding processing capacities. With the rapid expansion of e-commerce channels and a growing young population seeking Western-style, high-protein diets, the Asia-Pacific region is poised to outpace all other regions in growth rate over the forecast period.

Competitive Landscape

The soy protein concentrate market is consolidated, with a few global agribusiness giants holding significant influence over the supply chain and processing technology. Major players like ADM, Cargill Inc., and Bunge Limited utilize their vertical integration from soybean crushing to refined ingredient production to maintain a competitive edge. These leaders focus on operational excellence and massive R&D budgets to improve protein purity and sensory profiles. However, the market also features specialized players like Sonic Biochem and Solbar, who differentiate themselves through niche applications and regional expertise. Current strategies focus on geographic expansion into emerging markets and the acquisition of smaller biotech firms to gain access to proprietary extraction methods. The emergence of joint ventures between global ingredient suppliers and local food processors is a key trend aimed at tailoring products to regional taste preferences and regulatory requirements.

Key Developments:

- In December 2025, Bunge Global SA signed an agreement with Solae to acquire IFF’s lecithin, soy protein concentrate, and crush-related assets, significantly expanding its value-added soy ingredients footprint.

- In May 2025, IFC committed $40 million to Astarta to support Ukraine’s first soy protein concentrate production facility, boosting domestic value addition and export potential.

- In May 2025, Bunge introduced a new range of soy protein concentrates at IFFA, targeting formulation challenges such as off-notes, texture inconsistencies, and functional gaps in plant-based foods.

Companies Covered in Soy Protein Concentrate Market

- ADM

- Cargill Inc.

- Kerry Group

- CHS Inc.

- Bunge Limited

- Wilmar International

- Prinova Group LLC

- Sonic Biochem

- Ingredion Incorporated

- Solbar

- Burcon NutraScience Corporation

- Others

Frequently Asked Questions

The global soy protein concentrate market is projected to be valued at US$ 1.7 Bn in 2026.

Rising Adoption of Plant-Based Diets and Meat Alternatives is driving demand for Soy Protein Concentrate market.

The global soy protein concentrate market is poised to witness a CAGR of 9.2% between 2026 and 2033.

Technological Innovations in Clean-Label Extraction Processes is key opportunity for key players in the market.

Leading companies include ADM, Cargill Inc., Kerry Group, CHS Inc., Bunge Limited, Wilmar International, and Others.