- Processed Food

- Soy Sauce Market

Soy Sauce Market Size, Share, and Growth Forecast, 2025 - 2032

Soy Sauce Market By Product Type (Light Soy Sauce, Dark Soy Sauce) Process (Blended Soy Sauce, Brewed Soy Sauce), Distribution Channel, and Regional Analysis for 2025 - 2032

Soy Sauce Market Size and Trends Analysis

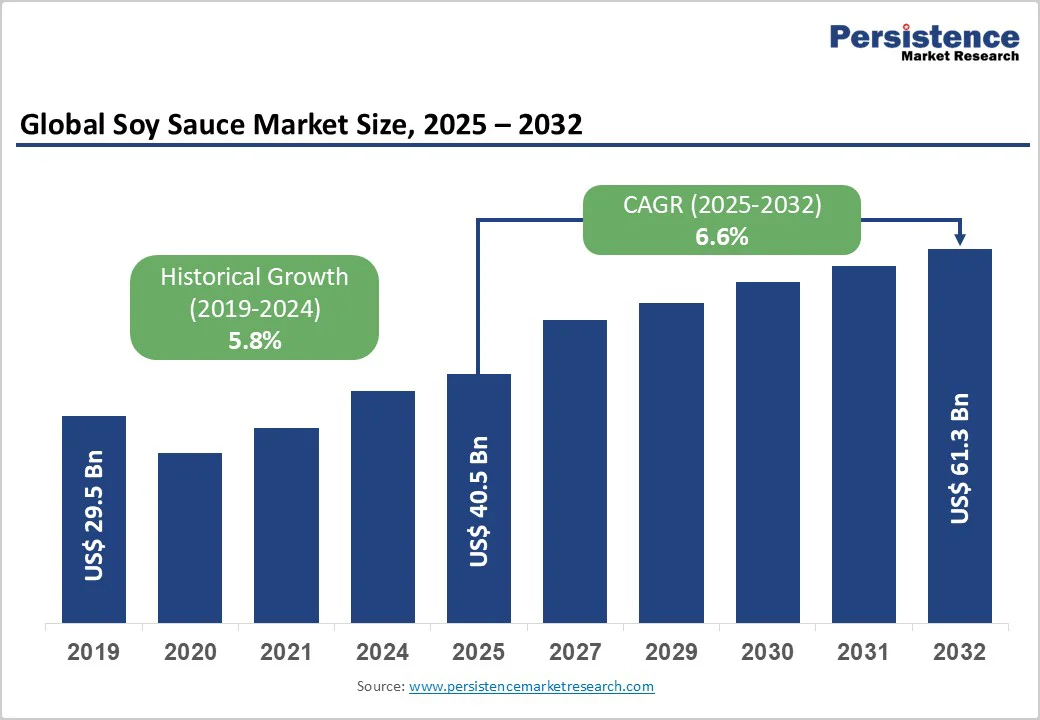

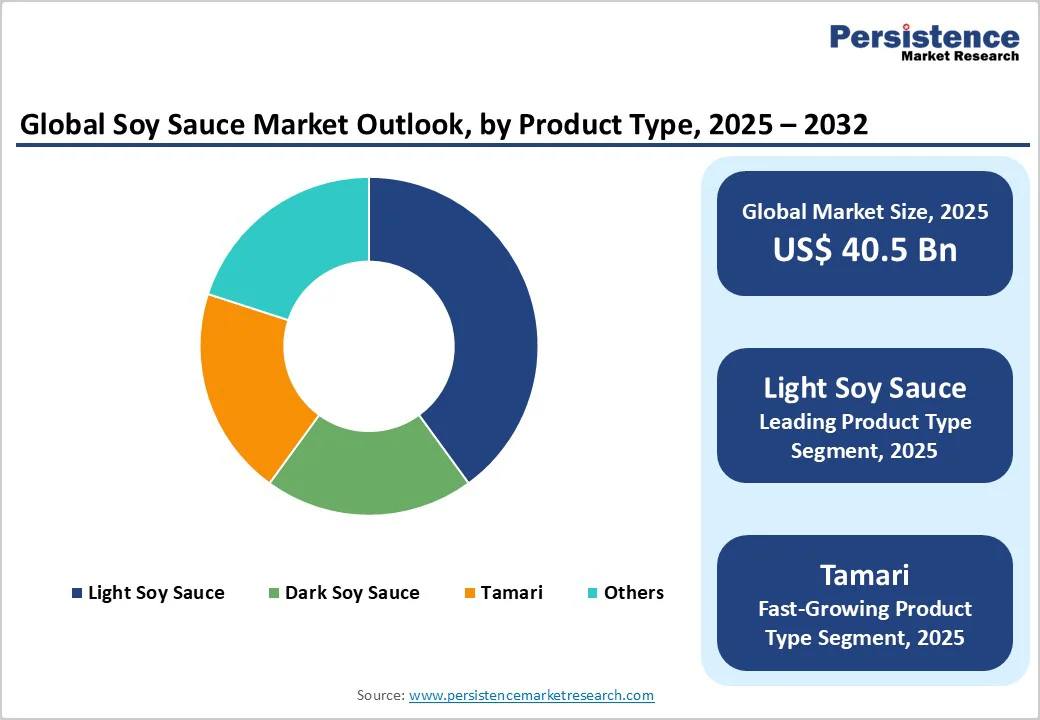

The global soy sauce market size was valued at US$40.5 billion in 2025 and is projected to reach US$40.5 billion by 2032, growing at a CAGR of 6.6% between 2025 and 2032, driven by the globalization of Asian cuisines, the premiumization of soy-based condiments, and expanding distribution through foodservice and e-commerce channels.

The Asia Pacific region dominates, holding over 60% of both production and consumption. The market remains fragmented, with global leaders securing less than 20% of total revenue. Competitive advantage now depends on scale, brand strength, and distribution efficiency.

Key Industry Highlights

- Leading Region: Asia Pacific accounts for approximately 60% of global revenue, driven by China, Japan, and Southeast Asia.

- Fastest-growing Region: Europe, with the rapid adoption of premium and imported soy sauces, particularly in Germany, the U.K., France, and Spain.

- Investment Plans: Expansion in automation, R&D, e-commerce distribution, and overseas market penetration by major players such as Foshan Haitian, Kikkoman, and Lee Kum Kee.

- Dominant Type: Light Soy Sauce holds more than 40% of the market share, favored for versatility in cooking and seasoning.

- Dominant Distribution Channel: Retail (Supermarkets/Hypermarkets) holds nearly 51% of global revenue, driven by household consumption.

| Key Insights | Details |

|---|---|

|

Soy Sauce Market Size (2025E) |

US$40.5 Bn |

|

Market Value Forecast (2032F) |

US$61.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Globalization of Asian Cuisines and Foodservice Expansion and Premiumization

The rising popularity of Asian food in North America, Europe, and Latin America has driven soy sauce penetration beyond traditional households. The growth of pan-Asian restaurants, online delivery platforms, and private-label offerings ensures steady consumption. As more restaurants use soy sauce in marinades, sauces, and ready meals, the overall market sustains mid-single-digit growth.

Consumers are actively shifting toward healthier options, leading to demand for low-sodium, gluten-free, and organic soy sauce variants. Global leaders such as Kikkoman and Lee Kum Kee have expanded their less-salt and allergen-friendly ranges, while also introducing soy-free umami alternatives. These premium variants are priced higher, supporting revenue growth in mature markets where volume expansion is slower. Beyond households, soy sauce is now a staple ingredient for processed food manufacturers producing ready meals, snacks, and seasoning blends. Its natural umami profile makes it a clean-label substitute for synthetic flavor enhancers. This industrial demand ensures large-scale contracts for suppliers, especially those with strong fermentation and quality-control capabilities.

Raw-Material Price Volatility and Regulatory Complexity

Soybean price swings remain one of the largest risks. Trade disputes, climate shocks, or concentrated sourcing often lead to sudden cost spikes. Manufacturers struggle to pass these costs on to price-sensitive consumers, compressing margins. For instance, a 10% rise in soybean prices can reduce gross margins by several percentage points for producers relying on commodity-grade blends.

Labeling requirements for sodium, gluten, and additives differ significantly across regions. Exporters targeting the U.S., the EU, and Japan simultaneously face high compliance costs. Reformulation, packaging changes, and slower product approvals add to structural challenges, particularly for smaller regional brands.

Premium Brewed and Traditional Variants, and Allergen-Free Options

There is a growing consumer appetite for traditionally brewed soy sauces, often perceived as authentic and of higher quality. If brewed products capture even 5% more of global share, it could translate into several hundred million dollars of additional annual revenue by the early 2030s. Health-conscious consumers and those with gluten sensitivities represent a fast-expanding segment. Low-sodium and wheat-free tamari soy sauces already show above-average growth rates. Capturing just 3-4% more share in developed markets could add hundreds of millions of dollars in incremental revenue by 2032.

There is a strong opening for soy sauce producers to move beyond bottled condiments and supply concentrated, clean-label umami systems tailored to food manufacturers. As processors and snack makers pursue natural flavor enhancement and sodium reduction, a ready-to-use soy-based concentrate or seasoning system that delivers consistent umami, color control, and shelf stability becomes a compelling ingredient. Such solutions can replace or reduce reliance on synthetic enhancers while fitting easily into existing manufacturing lines, making them attractive to manufacturers seeking both cleaner labels and simpler formulation workflows.

Category-wise Analysis

Product Type Insights

Light soy sauce remains the dominant product type globally, capturing over 40% of market share due to its versatility in both home and professional kitchens. Its mild flavor profile allows it to be used for seasoning, dipping, and cooking across diverse cuisines, making it particularly popular in China, Southeast Asia, and increasingly in Western markets. Manufacturers prioritize light soy in standard retail SKUs and industrial formulations because of high repeat purchase rates. Retailers often pair light soy with value packs or family-size bottles, further solidifying its position as a mass-market staple.

Tamari, traditionally a wheat-free soy sauce, and premium dark variants are gaining traction in value terms. Growth is driven by rising gluten-free and allergen-conscious consumer segments, increased interest in authentic Asian cuisine, and the willingness of consumers to pay more for premium quality and artisanal brewing processes. In Europe and North America, these variants are seeing higher adoption in gourmet restaurants, specialty retail stores, and online marketplaces. Value-added marketing emphasizing traditional fermentation, organic certification, and heritage branding is accelerating adoption, making these products the fastest-growing segment globally.

Process Insights

Blended soy sauces continue to dominate in volume, accounting for the majority of mass-market sales. They are favored due to their cost-effectiveness, consistent flavor, and scalable production, which makes them ideal for supermarkets, private-label products, and food processors. Blended varieties also allow manufacturers to meet the price-sensitive segment of the market, especially in developing countries, where affordability drives consumption. Their industrial appeal lies in standardized taste and shelf-stability, which is essential for processed foods and packaged meals.

Traditionally brewed soy sauces are the fastest-growing segment in value terms. Their fermentation-based production enhances flavor complexity and perceived quality, attracting premium buyers and professional chefs. Growth is particularly strong in developed regions such as Japan, Europe, and North America, where consumers associate brewed soy sauce with authenticity and craftsmanship. Retail strategies often involve small-batch or heritage-label products, sometimes bundled in gift packs or premium packaging, which allows manufacturers to command higher selling prices.

Distribution Channel Insights

Retail channels, including supermarkets, hypermarkets, and convenience stores, continue to be the largest distribution segment, accounting for nearly 51% of global revenue. Retail dominance is supported by consistent household demand, wide product availability, and competitive promotions. Supermarkets often stock multiple varieties, including light, dark, and premium options, allowing for cross-selling and brand differentiation. Private-label soy sauces also gain significant traction in retail, particularly in Europe and North America.

Online and foodservice channels are the fastest-growing, driven by changing consumer behavior and professional demand. E-commerce platforms facilitate access to specialty and artisanal soy sauces, catering to health-conscious and gourmet consumers. Foodservice channels, including pan-Asian restaurants, cloud kitchens, and catering operations, drive institutional demand, often requiring larger pack sizes and industrial-grade formulations. Growth in online sales is further accelerated by digital marketing, subscription models, and partnerships with meal-kit providers. The combination of these channels is reshaping distribution strategies for global manufacturers, enabling them to reach niche markets efficiently.

Regional Insights

North America Soy Sauce Market Trends - Premiumization and Health-Driven Innovation Fuel U.S. Specialty Growth

North America, while a smaller proportion of the soy sauce market, represents a high-value segment due to premiumization and specialty product demand. The U.S. is the largest contributor, with soy sauce sales projected to exceed US$5.5 Billion by 2025. Growth is primarily driven by the expansion of Asian cuisine restaurants, increased awareness of healthier alternatives (such as low-sodium or gluten-free options), and rising online sales through specialty food platforms.

The regulatory environment encourages innovation, as companies comply with FDA sodium labeling and allergen disclosure requirements. As a result, premium tamari, organic, and low-sodium products are increasingly common. The competitive landscape includes global giants like Kikkoman and Lee Kum Kee, which dominate both retail and foodservice channels, while smaller brands like Aloha Shoyu focus on niche regional markets. Strategic opportunities exist in e-commerce expansion, private-label partnerships, and tailored products for health-conscious consumers.

Europe Soy Sauce Market Trends - Fusion Cuisine and Regulatory Compliance Drive European Market Expansion

Europe is a mid-sized but fast-growing market, reflecting a combination of mature retail systems and expanding fusion cuisine adoption. Germany and the U.K. lead in retail demand for imported and premium soy sauces, while France and Spain are seeing significant growth in restaurant and foodservice channels. Consumer interest in gourmet cooking, health-conscious choices, and global flavors is a major growth driver.

The region’s strict EU regulations on additives, sodium levels, and allergen labeling create both a barrier to entry and an opportunity for established manufacturers who can harmonize formulations across multiple markets. International brands continue to dominate the premium space, while private-label soy sauces expand their presence in supermarkets. Investments are focusing on e-commerce distribution, partnerships with gourmet retailers, and marketing that emphasizes product quality, authenticity, and sustainability.

Asia Pacific Soy Sauce Market Trends - Traditional Brewing and Scale Secure APAC’s Global Market Leadership

Asia Pacific is the largest global market, contributing approximately 60% of total revenue. China is the largest producer and consumer, offering both mass-market and premium options. Japan is a hub for traditionally brewed soy sauces, with brands like Kikkoman and Yamasa anchoring the premium segment. Southeast Asia, including Indonesia and Vietnam, is significant both for production and rising domestic consumption. India is an emerging market, driven by urbanization and increased exposure to Asian cuisines.

The region benefits from low manufacturing costs, large-scale production facilities, and deeply embedded culinary traditions. Leading players, such as Foshan Haitian, are investing in automation, research and development, and export capabilities. Key drivers include rising disposable income, urbanization, and increasing adoption of international cooking styles at home. Regional competition is intense, but market opportunities exist in premium, low-sodium, and gluten-free products, as well as in online and institutional channels. Brewed soy sauces are expanding fastest in value terms. Their authentic fermentation process commands higher price points and appeals to premium buyers and chefs.

Competitive Landscape

The global soy sauce market is fragmented, with the top five players capturing less than 20% of total revenue, leaving room for regional, specialty, and private-label brands, especially in retail channels. Market leaders like Kikkoman, Lee Kum Kee, and Foshan Haitian dominate premium segments, utilizing strong brand equity, global reach, and large-scale production. Regional brands and private labels thrive in local markets, particularly in Southeast Asia, India, and the U.S. Competition is driven by brand recognition, production efficiency, diverse product offerings (low-sodium, gluten-free), and innovation in packaging and fermentation.

Price sensitivity shapes purchases in developing regions, while premium quality and heritage appeal to consumers in North America, Europe, and Japan. Leading brands focus on premiumization with organic and health-conscious options, invest in e-commerce and exports, and prioritize sustainability through R&D and eco-friendly packaging. Heritage marketing reinforces brand trust, supporting premium pricing and long-term growth.

Key Industry Developments

- In March 2024, Foshan Haitian, China’s largest soy sauce producer, filed for a major listing in Hong Kong to raise over US$1 Billion. The funds are aimed at expanding production capacity, automation, and global distribution channels.

- In November 2024, Lee Kum Kee initiated a premium product campaign in Europe, targeting gourmet home chefs and upscale restaurants, strengthening its market presence in Germany, the U.K., and France.

- In June 2023, Sempio Foods in South Korea entered a technology partnership with a local fermentation research institute to enhance quality consistency and reduce production time for its premium tamari products.

- In September 2024, Yamasa Corporation expanded its European distribution network, opening a regional logistics center in Rotterdam to support faster delivery of premium brewed soy sauces.

Companies Covered in Soy Sauce Market

- Kikkoman Corporation

- Foshan Haitian Flavouring & Food Co., Ltd.

- Lee Kum Kee

- Yamasa Corporation

- Sempio Foods Company

- Shibanuma Soy Sauce Co., Ltd.

- Koon Chun Sauce Factory Ltd.

- Pearl River Bridge (Guangdong PRB Bio-Tech Co., Ltd.)

- Higeta Shoyu Co., Ltd.

- Marukin Shoyu Co., Ltd.

- ABC President Indonesia (Heinz ABC)

- Jiajia Food Group Co., Ltd.

- Masan Consumer Corporation

- Bourbon Barrel Foods

- Bluegrass Soy Sauce Co.

- Amoy Food Ltd.

- Hormel Foods (House of Tsang)

- Aloha Shoyu Company

- ConAgra Brands, Inc.

- Nestlé S.A.

Frequently Asked Questions

The soy sauce market size is projected to be US$40.5 Billion in 2025.

By 2032, the market is expected to reach US$61.3 Billion.

Key trends in the soy sauce market include rising demand for premium and traditionally brewed variants and the growth of gluten-free and low-sodium soy sauces.

Light soy sauce is the leading type, accounting for over 40% of market share globally.

The soy sauce market is projected to grow at a CAGR of 6.6% from 2025 to 2032, driven by premiumization, online sales, and industrial adoption.

Some of the major players include Foshan Haitian Flavouring & Food Co., Ltd., Kikkoman Corporation, Lee Kum Kee, Yamasa Corporation, and Sempio Foods.