- Food Ingredients & Additives

- Soy Granules Market

Soy Granules Market Size, Share, and Growth Forecast, 2026 - 2033

Soy Granules Market By Product Type (Textured Soy Granules, Others), Nature (Organic Soy Granules, Conventional Soy Granules), Form (Dried Soy Granules, Cooked Soy Granules), End-use Industry (Food and Beverage, Others), and Regional Analysis for 2026 - 2033

Soy Granules Market Size and Trends Analysis

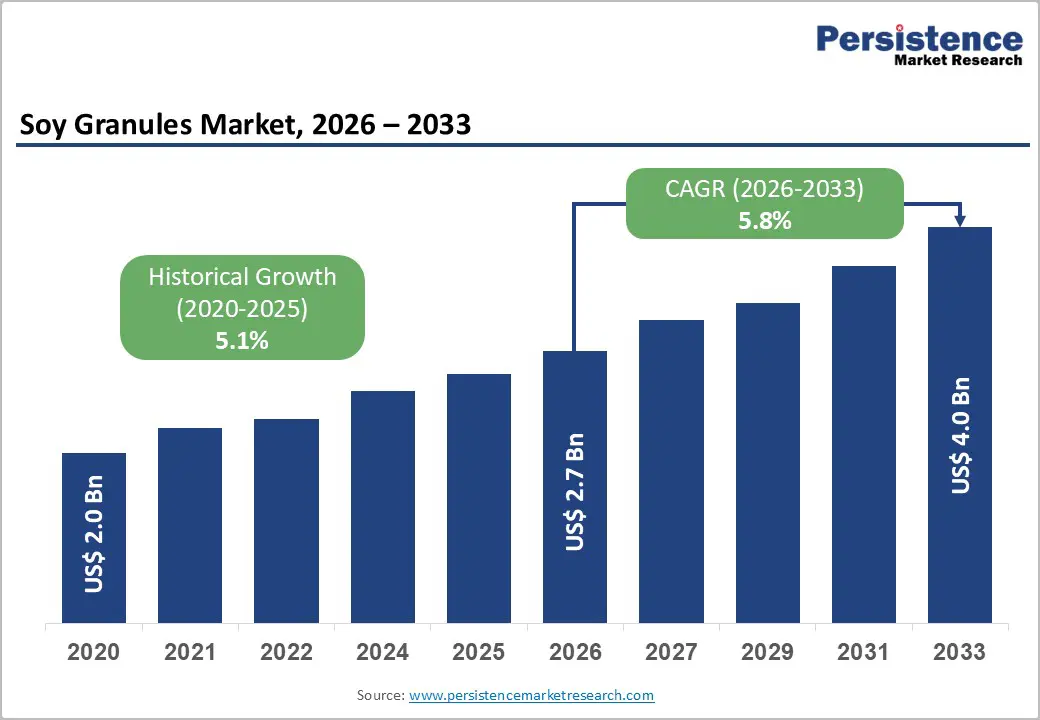

The global soy granules market size is likely to be valued at US$2.7 billion in 2026, and is expected to reach US$4.0 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by the increasing prevalence of plant-based protein consumption, rising demand for meat alternatives in vegan diets, and advancements in textured vegetable protein processing.

Growing demand for nutritious, versatile soy granules, especially in food and beverage and nutritional supplements, is driving adoption across different demographics. Advances in organic and textured formulations are further boosting uptake by offering more sustainable, high-protein options. Increasing recognition of soy granules as critical for affordable nutrition in emerging regions remains a major driver of market growth.

Key Industry Highlights:

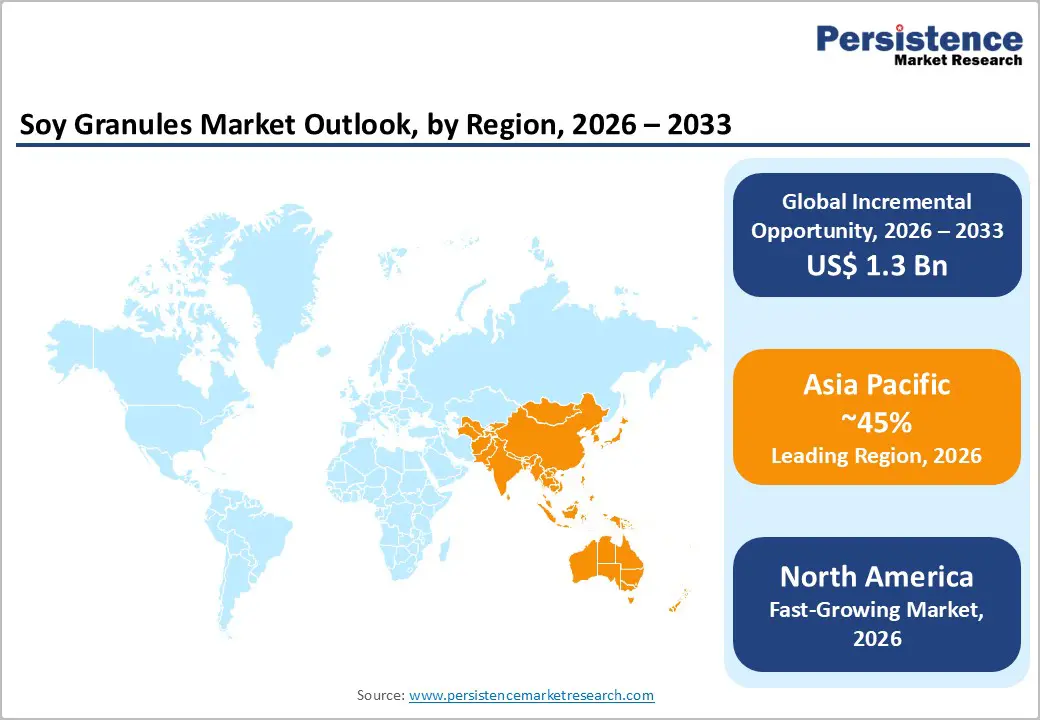

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by abundant soybean production, high vegetarian populations, and strong food processing in India and China.

- Fastest-growing Region: North America, fueled by vegan trends, rising health consciousness, and growing investments in plant-based foods in the U.S.

- Dominant Product Type: Textured soy granules, to hold approximately 50% of the market revenue, as they mimic meat texture effectively in substitutes.

- Leading Form: Dried soy granules account for over 60% of the market revenue, due to longer shelf life and ease of storage.

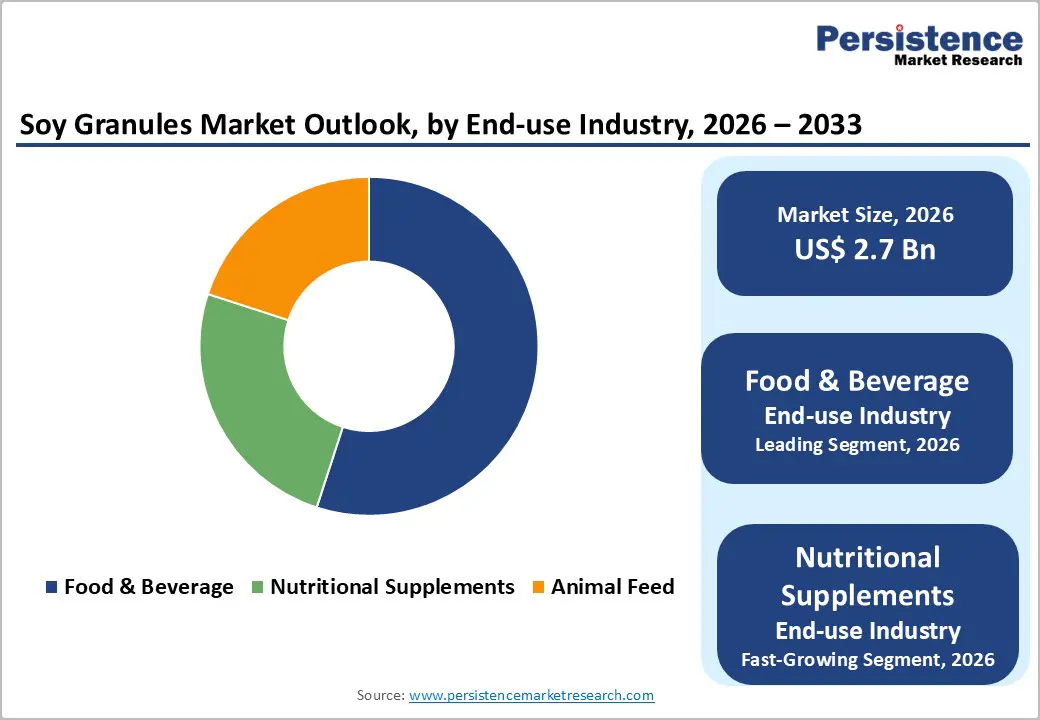

- Leading End-use Industry: Food and beverage, to contribute nearly 55% of the market revenue, due to extensive use in meat analogs and snacks.

| Key Insights | Details |

|---|---|

| Soy Granules Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$4.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Health Awareness and Demand for Plant-based Proteins

Rising health consciousness among consumers is significantly driving the demand for plant-based proteins, including soy granules. People are increasingly aware of the links between diet and wellness, focusing on nutrition that supports heart health, muscle maintenance, weight management, and immune function. Plant proteins, such as soy, are naturally low in saturated fat, cholesterol-free, and rich in essential amino acids, making them a preferred alternative to animal-derived proteins. This shift is reinforced by growing adoption of flexitarian, vegetarian, and vegan diets, where plant-based proteins form a primary source of nutrition.

The global trend toward functional foods and nutritionally enhanced products has fueled the integration of soy granules into snacks, meat alternatives, cereals, and beverages. According to recent market estimates, over 45% of the global consumers now actively seek plant-based protein options as part of a balanced diet. This increased preference is particularly evident in urbanized regions where lifestyle diseases and diet-related health concerns are more prevalent.

Consumer Acceptance and Taste Challenges

Consumer acceptance and taste challenges are the major restraints for the soy granules market. While soy is nutritionally rich and versatile, many consumers perceive its flavor and texture as less appealing compared to traditional animal proteins. The natural beany taste and slightly grainy texture of soy granules can make them less desirable in certain applications, such as ready-to-eat meals, baked goods, and meat analogs. This sensory barrier can reduce repeat consumption, limiting market penetration, particularly among populations unfamiliar with plant-based proteins.

Cultural food preferences play a significant role. In regions where soy consumption has historically been low, consumers may be hesitant to adopt soy-based products due to unfamiliarity with its taste or preparation methods. This hesitancy can slow the adoption of soy granules in mainstream food products, despite their health benefits. In a consumer survey on novel and plant-based proteins, 75% of respondents said they were open to trying soy protein, but 25% were not, indicating a significant portion of consumers still hesitate, often due to sensory concerns such as taste and texture.

Manufacturers often attempt to mitigate these challenges through flavor masking, seasoning, and product formulation, but these strategies can increase production costs and limit scalability. Taste perception remains a critical barrier, particularly in markets where consumers prioritize flavor and texture over health benefits.

Innovation in Textured and Organic Delivery Platforms

Innovation in textured and organic soy granule delivery platforms is transforming the global protein landscape by addressing two major challenges, meat mimicry and sustainability barriers. Textured platforms are engineered to achieve a fibrous structure, reducing reliance on binders and enabling realistic meat analogs in granules. Innovations, such as high-moisture extrusion, steam texturization, fiber alignment, and hybrid blending, significantly improve mouthfeel and reduce crumbling, lowering formulation costs for brands and consumer campaigns.

Progress in organic platforms, including certified dried granules, cooked ready-meals, supplement powders, and feed pellets, supports more clean-label nutrition by minimizing pesticides, the diet’s first line of defense against residues. These formats eliminate GMOs, enhance bioavailability, and allow versatile use without processing aids, making them highly suitable for mass vegan programs. New technologies such as enzymatic debittering, bio-fortification, and VLP-based coating further enhance flavor and nutrient response.

Category-wise Analysis

Product Type Insights

Textured soy granules are projected to dominate the market, capturing approximately 50% of revenue in 2026. Their popularity stems from a meat-like texture, high rehydration capacity, and versatility, making them a preferred choice for plant-based analogs. Textured soy granules provide a fibrous bite, deliver nutritional value, and offer cost-effectiveness, making them ideal for large-scale food applications. Cargill Inc. remains a key player, leveraging its R&D expertise and innovation centers to develop advanced textured soy protein products tailored for meat substitutes and functional foods.

Non-textured soy granules are expected to be the fastest-growing segment from 2026 to 2033, driven by high protein content, neutral taste, and broad applicability in clean-label, high-protein products such as nutritional bars, dairy alternatives, beverages, and fortified snacks. These granules offer superior solubility and functional properties compared with traditional textured forms, aligning with modern health-focused trends. Growing consumer demand for high-protein, low-carbohydrate, and plant-based functional foods is accelerating adoption in both mainstream and premium markets, particularly in North America and Europe. Scoular supplies custom soy protein isolate ingredients, which can be processed into non-textured granules optimized for water holding, emulsification, and texture enhancement, increasingly used by manufacturers in clean-label, high-protein food formulations.

Nature Insights

Conventional soy granules dominate the market, accounting for an estimated 70-75% share globally. Their leadership is driven by lower production costs, large-scale availability, and widespread use in mass food processing, including ready meals, snacks, and meat alternatives. Food manufacturers prefer conventional variants due to stable supply chains and price competitiveness. ADM produces large volumes of conventional textured soy protein products (including granules) that are widely used by food manufacturers in plant-based meat alternatives, snacks, and ready meals due to their cost-effectiveness and reliable supply. ADM’s soy protein network supplies textured soy products to 90+ countries, underscoring how conventional soy ingredients maintain leadership through high-volume production and broad industrial adoption.

Organic soy granules represent the fastest-growing segment, due to their clean-label appeal and expanding use in premium supplements. Its pesticide-free profile makes it ideal for targeted health, reducing concerns. Continuous innovations in certified sourcing are further strengthening their purity, driving rapid adoption across North America and Europe, where demand for non-GMO, organic proteins is accelerating. NOW Real Food® Organic Textured Soy Protein (T.S.P.) is the healthy vegetarian alternative to meat. This unflavored and versatile vegetable protein is non-GMO and perfect for vegetarian burgers, chili, stews, soups, and casseroles. NOW Real Food® Organic T.S.P. Granules are made entirely from organic soybeans with no chemical additives and are an excellent source of protein.

Form Insights

Dried soy granules are anticipated to lead the market, holding approximately 60% of the share in 2026, driven by extended shelf life, bulk storage programs, and strong global demand for convenient proteins. Their dominance continues as manufacturers expand dry mixes. Rising adoption of cooked, ready forms and expanded feed campaigns highlight the growing focus on convenience. Fortune Soya Granules and Nutrela Soya Granules are widely available dried soy granule products used both by consumers and food manufacturers as a high-protein, shelf-stable base ingredient. These granules typically contain around 50% protein and can be stored for over 12 months under dry conditions, making them suitable for large-scale production, storage programs, and long distribution chains.

Cooked soy granules are likely to be the fastest-growing segment, due to strong momentum in ready-to-eat and expanding inclusion of pre-hydrated options in meals. The growing shift toward time-saving, microwaveable platforms, along with better softness, accelerates the adoption. Advancements in retort packaging and the continued progress of flavored cooked variants entering consumer trials drive market growth. ICAR-National Soybean Research Institute (NSRI) and the Indian Institute of Millets Research (IIMR) are actively working to develop ready-to-eat (RTE) soy-based food products that require minimal preparation, such as high-protein soy + millet halwa, soy upma, and soy cookies. These products are being formulated so they can be prepared simply by adding hot water, offering microwaveable, time-saving options that appeal to health-conscious and convenience-seeking consumers.

End-use Industry Insights

The food and beverage segment is expected to dominate the market, contributing nearly 55% of revenue in 2026, as it remains the primary end-use segment for meat extenders, large recipe programs, and management of diverse formulations requiring versatile proteins. Their strong integration, trained chefs, and ability to handle high-volume or specialty blends drive higher consumption. Food & beverage sectors are leading textured rollouts and administering emerging organic trials. Simran Nutri Foods’ Gempro Soya Protein Granules are a widely used textured soy protein (TSP) in the food & beverage industry, particularly for meat extenders and meat analog formulations. Food manufacturers incorporate these granules into products such as plant-based burgers, sausages, hot dogs, and vegetarian ready meals because, when rehydrated, they deliver a fibrous, meat texture that closely mimics conventional meat. Made from defatted, clean, non-GMO soy flour, Gempro granules also enhance protein content while maintaining neutral taste, allowing their use in soups, sauces, snacks, and prepared foods without altering flavor profiles.

Nutritional supplements are likely to be the fastest-growing segment, driven by their strong wellness presence and expanding role in plant-based powders. They offer convenient, quick, and accessible dosing, attracting users who prefer shake-based, low-calorie consumption formats. Increased outreach programs, fitness focus, and wider availability of routine and premium granules further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. AS IT IS soy protein isolate, a plant-based protein powder providing ~27 g soy protein per serving, lactose-free, and suitable for shakes or meal supplementation. Its clean, additive-free formulation appeals to consumers seeking low-calorie, high-protein options for daily wellness and fitness routines.

Regional Insights

North America Soy Granules Market Trends

North America is projected to be the fastest-growing region, driven by the region’s advanced vegan infrastructure, strong research and development capabilities, and high public awareness of the benefits of plant protein. Distribution systems in the U.S. and Canada provide extensive support for consumption programs, ensuring wide accessibility of soy granules across food, supplement, and feed applications. The increasing demand for textured, convenient, and easy-to-incorporate forms is further accelerating adoption, as these formats enhance versatility and reduce barriers associated with imports.

Technological advancements in soy granules, such as enhanced texturization stability, improved organic-grade processing, and targeted nutrient fortification, are drawing strong investment interest from both public institutions and private companies. Government-led nutrition programs and health-focused awareness campaigns are also encouraging soy-based consumption as part of meat-reduction strategies, cholesterol management, and the rising flexitarian lifestyle. These supportive initiatives are helping sustain long-term market demand. Increasing development of cooked soy blends and application-specific formulations, especially for dietary supplements and specialized food uses, is also broadening the overall application scope of soy granules and accelerating market expansion.

Europe Soy Granules Market Trends

Europe is driven by increasing awareness of sustainable benefits, strong retail systems, and government-led wellness programs. Countries such as Germany, France, and the U.K. have well-established nutrition frameworks that support routine incorporation and encourage adoption of innovative granule delivery methods, including soy granules. These natural formulations are particularly appealing for food populations, eco-conscious consumers, and supplement users, improving compliance and coverage rates.

Technological advancements in soy granule development, such as enhanced texturization, source-targeted delivery, and improved organic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for granules against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, ready-to-cook options is aligned with the region’s focus on preventive health and reducing meat intake. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in extrusion and novel variants to increase efficacy.

Asia Pacific Soy Granules Market Trends

Asia Pacific is projected to lead with a market share of 45% in 2026, driven by rising protein awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting granule campaigns to address traditional diets and emerging vegan needs. Soy granules are particularly attractive in these regions due to their local sourcing, ease of processing, and suitability for large-scale food drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-process soy granules, which can withstand challenging climatic conditions and minimize waste dependence. These innovations are critical for reaching remote markets and improving overall nutritional coverage. Growing demand for food & beverage, supplements, and animal feed applications is contributing to market expansion. Public-private partnerships, increased agro expenditure, and rising investments in texturization research and manufacturing capacity are further accelerating growth. The convenience of granule delivery, combined with improved texture and reduced risk of deficiency, positions soy granules as a preferred choice.

Competitive Landscape

The global soy granules market features competition between established agro-processors and emerging plant-based brands. In North America and Europe, NOW Health Group and Davert lead through strong R&D, distribution networks, and retail ties, bolstered by innovative grades and wellness programs. In Asia Pacific, Patanjali Foods Ltd advances with localized solutions, enhancing accessibility. Textured delivery boosts versatility, reduces dependence on animal protein, and enables mass formulations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand sourcing, and speed commercialization. Organic formulations solve purity issues, aiding penetration in health-focused areas.

Key Industry Developments

- In January 2024, DuPont de Nemours, Inc. launched a new line of soy-based meat alternatives, targeting the growing demand for plant-based proteins.

- In March 2023, Archer Daniels Midland Company announced the expansion of its soy protein production facility in Illinois to meet the growing demand for plant-based proteins. This expansion aims to increase production capacity and enhance the company's product offerings in the soy granules market.

Companies Covered in Soy Granules Market

- Patanjali Foods Ltd.

- NOW Health Group

- Davert

- Sita Shree Food Products

- Mahakali Foods

- MDH Spices

Frequently Asked Questions

The global soy granules market is projected to reach US$2.7 billion in 2026.

The rising prevalence of plant-based protein consumption and demand for meat alternatives are key drivers.

The soy granules market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Advancements in textured and organic delivery platforms are the key opportunities.

Patanjali Foods Ltd, NOW Health Group, Davert, Sita Shree Food Products, and Mahakali Foods are the key players.