- Food Ingredients & Additives

- Aquaculture Market

Aquaculture Market Size, Share, and Growth Forecast, 2025 - 2032

Aquaculture Market By Species Type (Finfish, Crustaceans, Others), Environment Type (Freshwater, Marine), End-user, and Regional Analysis for 2025 - 2032

Aquaculture Market Size and Trends Analysis

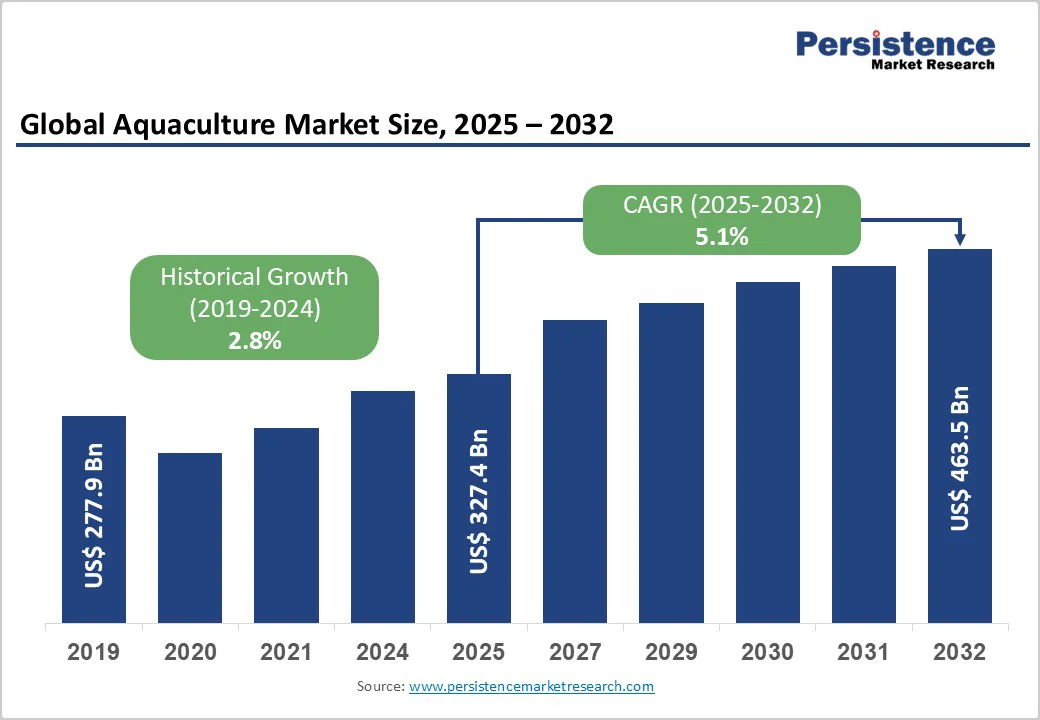

The global aquaculture market size is likely to be valued at US$327.4 Billion in 2025 and is expected to reach US$463.5 Billion by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by rising seafood consumption, technological advancements in farming systems, and policy initiatives promoting sustainable protein sources.

With capture fisheries nearing their limits, aquaculture now provides over half of global aquatic food, driven by regulatory support, feed innovation, and product diversification, solidifying its role as a cornerstone of the global food system.

Key Industry Highlights

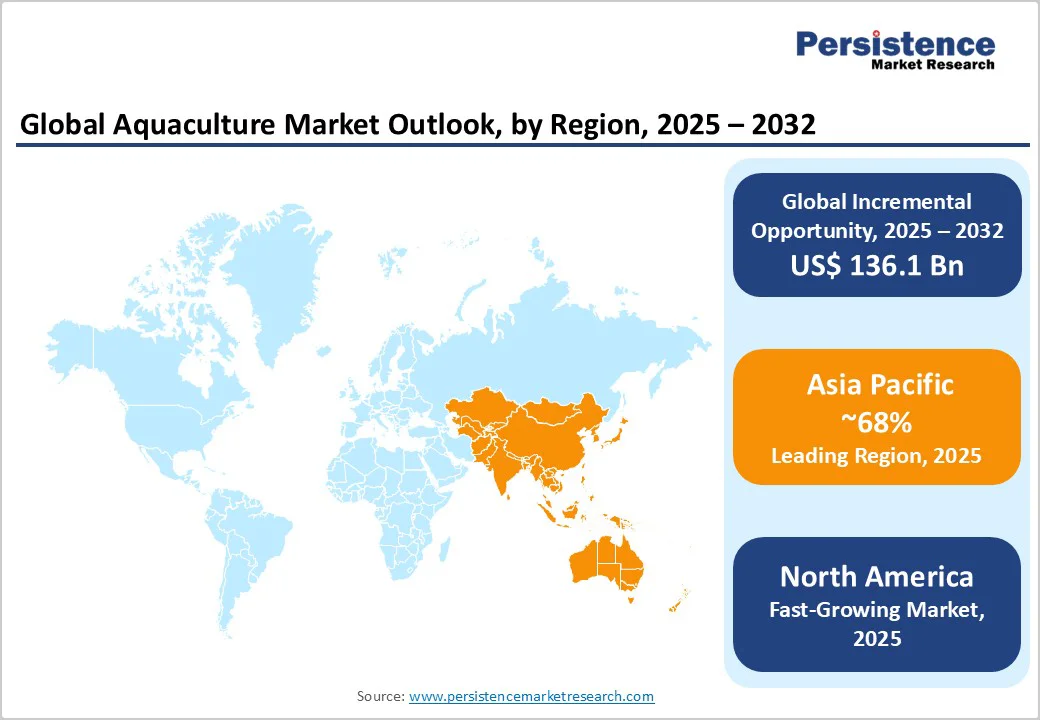

- Leading Region: Asia Pacific dominates the market, accounting for over 68% of global production value in 2025, driven by China, India, and ASEAN nations through large-scale coastal and freshwater farming initiatives.

- Fastest-Growing Region: North America is expected to register the highest growth rate, supported by technological advancements in land-based recirculating aquaculture systems (RAS), increasing venture capital investment, and policy support for sustainable offshore farming.

- Investment Plans: Between 2024 and 2025, the industry recorded over US$2.5 Billion in announced expansions and financing, led by projects such as Atlantic Sapphire’s Miami Bluehouse expansion (US$300 Million), EIB’s €200 Million (US$233 Million) investment in European aquaculture, and new AI-driven farming projects across Asia and North America.

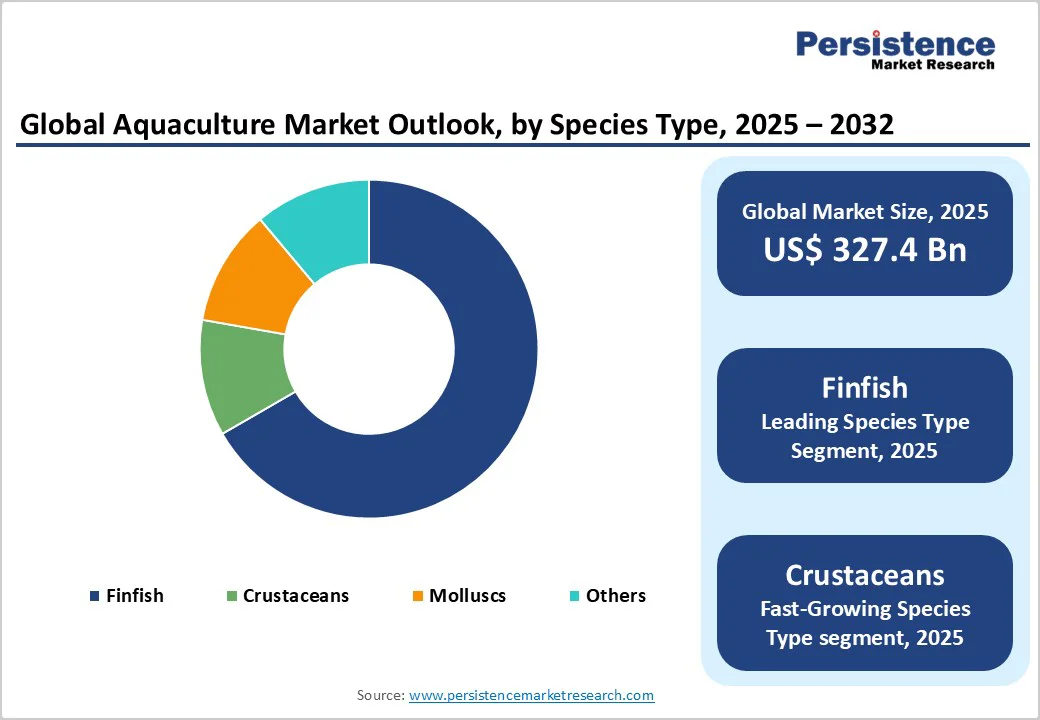

- Dominant Species: Finfish remains the largest category, representing over 59% of total aquaculture market value, supported by strong global demand for salmon, tilapia, and carp.

- Leading End-user: Commodity production accounts for nearly 65% of the total market revenue in 2025, driven by large-scale operations targeting domestic and export markets.

| Key Insights | Details |

|---|---|

| Aquaculture Market Size (2025E) | US$327.4 Bna |

| Market Value Forecast (2032F) | US$463.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Seafood Demand and Protein Transition

Global seafood demand is rising as populations grow and consumers seek healthier proteins. FAO data shows aquaculture output reached 131 million tonnes in 2022, surpassing capture fisheries for the first time and accounting for over half of global fish consumption.

Expanding middle classes in Asia and protein-focused diets in Western markets are driving this growth. These trends reinforce aquaculture’s position as a sustainable growth sector, fostering economies of scale in feed production, processing, and cold-chain logistics.

Technological Advancements and Operational Efficiency

Modern aquaculture technologies such as Recirculating Aquaculture Systems (RAS), automated monitoring, and precision feeding are boosting efficiency and sustainability. Digitalization, IoT monitoring, and AI analytics optimize feeding and water quality, while advanced biofiltration reduces waste.

These innovations have improved yields, feed efficiency, and disease control, delivering 10-20% productivity gains, lower mortality, and enhanced traceability, making aquaculture more cost-effective, investment-friendly, and aligned with global sustainability goals.

Regulatory and Sustainability Shifts Favoring Aquaculture

Governments and global agencies increasingly view aquaculture as vital for food security, employment, and sustainable resource use. The FAO’s Blue Transformation initiative targets a 35% rise in production by 2030 through better governance and investment.

Stricter fishery quotas and growing adoption of ASC and BAP certifications promote compliance and market access, while regulatory momentum enables green financing and drives investment in traceability and low-carbon systems.

Barrier Analysis - High Feed and Input Cost Inflation

Feed accounts for 60-70% of aquaculture production costs, making it the sector’s biggest expense. Rising prices for fishmeal, soybean meal, and essential oils are squeezing margins, with a 10% cost increase potentially cutting profits by 4-5%.

Volatile feed and energy prices, along with logistics challenges, hurt smaller producers. To offset risks, companies pursue vertical integration, alternative feeds, and diversified sourcing, though feed volatility remains a key constraint on growth.

Disease, Environmental, and Regulatory Risks

Disease outbreaks and environmental degradation pose major challenges for aquaculture. Pathogens such as white spot syndrome in shrimp and sea lice in salmon cause severe production and revenue losses. Nutrient discharge and ecosystem impacts have prompted stricter regulations, raising capital costs and delaying expansion.

Producers now face the dual burden of sustaining profitability while investing in biosecurity, vaccination, and monitoring, making effective disease and environmental risk management critical to long-term sustainability.

Opportunity Analysis - Expansion in Emerging Economies

Rapid growth in aquaculture is expected across Southeast Asia, South Asia, Africa, and parts of Latin America due to favorable climatic conditions, supportive policies, and rising domestic seafood consumption. As traditional markets in Europe and North America mature, these regions are projected to account for a significant share of incremental demand, equivalent to an estimated US$30 Billion opportunity by 2032.

Public-private partnerships, government subsidies, and export-oriented strategies are catalyzing capacity expansion. Nations such as India, Indonesia, and Vietnam are also investing heavily in shrimp and tilapia production, creating scalable models for other developing markets.

Value-Added and Premium Product Development

Consumers in mature economies are gravitating toward certified, traceable, and ready-to-eat seafood. Premium segments such as organic shrimp, sashimi-grade salmon, and sustainably sourced shellfish are gaining traction. Value-added aquaculture products, processed, frozen, or packaged seafood, offer higher margins compared to bulk fish sales.

The value-added category is expected to grow at a 7 to 8% CAGR through 2032, outpacing the broader market. Producers focusing on processing, branding, and packaging innovation can capture this high-margin segment. Certification and origin labeling further enhance competitiveness in export markets.

Technological Convergence and Alternative Feed Development

Precision aquaculture combining IoT, AI, robotics, and big data analytics represents a major investment frontier. Digital sensors and machine learning models are enhancing water management, early disease detection, and feed efficiency. At the same time, alternative feed technologies, such as insect meal, algae-based protein, and agricultural by-products, are reducing dependence on fishmeal.

These advances have the potential to cut feed costs by 15-20% and reduce carbon intensity, aligning production with environmental, social, and governance (ESG) standards. The technological convergence of aquaculture and agri-tech is expected to redefine competitiveness across the next decade.

Category-wise Analysis

Species Type Insights

Finfish remains the largest segment in global aquaculture, accounting for about 59% of the total market share. Key species include carp, salmon, tilapia, and catfish, with carp production dominating in China and India due to mature pond-culture systems.

In 2025, finfish output contributed over US$160 Billion to market value. Strong consumer demand, selective breeding, and efficient feed formulations continue to drive its dominance. Leading producers such as Mowi ASA and Lerøy Seafood Group in Norway are advancing precision-fed salmon farming through AI-based monitoring to minimize feed waste and mortality.

China’s extensive grass carp and silver carp polyculture systems also maximize resource efficiency and yield. These innovations, supported by global trade networks and traceability frameworks, reinforce finfish leadership across both developed and emerging aquaculture economies.

Crustaceans, including shrimp, prawns, and crabs, and molluscs such as mussels, oysters, and scallops, represent the fastest-growing segment. Rising demand for premium seafood and modernization of farming systems underpin this momentum. India, Vietnam, and Indonesia lead global shrimp exports, supported by improved hatcheries and automated aeration.

Companies such as Charoen Pokphand Foods in Thailand have introduced high-survival shrimp strains and smart feeding technologies. In Europe, Spain and France dominate sustainable mollusc farming, while Chile expands mussel exports to North America. Enhanced biosecurity, real-time disease monitoring, and probiotic water management continue to strengthen productivity and resilience in this segment.

Environment Type Insights

Freshwater aquaculture dominates global production, accounting for about 56% of total revenue in 2025. Its success stems from abundant inland water resources and cost-effective farming methods. Carp and tilapia are the leading freshwater species due to their adaptability and rapid growth rates. China’s Hubei and Guangdong provinces remain major carp producers, while India’s Andhra Pradesh and West Bengal contribute significantly to national output.

In Africa, Egypt has emerged as a key tilapia producer through state-backed investments in pond systems and hatchery expansion. The segment’s stability during global trade disruptions, including the pandemic, underscores its critical role in local food security. Agriculture practices, such as rice-fish farming in Southeast Asia, further enhance rural livelihoods and promote sustainable resource utilization.

Marine and brackish water aquaculture is expanding swiftly, fueled by rising demand for premium species such as Atlantic salmon, sea bass, sea bream, tuna, and cobia. Innovation in offshore cage systems, RAS (Recirculating Aquaculture Systems), and closed-containment designs is improving efficiency and sustainability.

Projects such as SalMar ASA’s Ocean Farm 1 in Norway showcase robotic feeding and environmental monitoring at scale. Chile’s vertically integrated salmon sector, along with Vietnam’s and Indonesia’s sensor-controlled shrimp farms, highlights regional innovation. With government support in regions such as British Columbia and Scotland, marine aquaculture’s CAGR exceeds 6%, driven by export demand, premium pricing, and eco-efficient technologies.

Regional Insights

North America Aquaculture Market Trends - Technological Expansion and Sustainable Growth

North America’s aquaculture industry is mature but advancing through technological innovation and sustainable practices. The regional market is projected to exceed US$95 Billion by 2032, supported by consumer preference for locally sourced, sustainable seafood.

The U.S. remains the regional leader, driven by expanding salmon, catfish, and trout production. Federal and state agencies are easing restrictions on offshore aquaculture to expand capacity while maintaining environmental safeguards.

Canada’s aquaculture sector benefits from government-backed programs promoting sustainable production in Atlantic and Pacific coastal areas. The competitive landscape features integrated operators and new entrants specializing in land-based recirculating aquaculture systems (RAS).

In March 2025, Atlantic Sapphire ASA announced an expansion of its Miami Bluehouse salmon facility, adding 10,000 tons of annual capacity using advanced RAS technology. In January 2025, Nordic Aquafarms received regulatory clearance for its land-based salmon farm in California, marking a key milestone for sustainable U.S. aquaculture.

In mid-2024, Innovasea Systems launched an AI-based monitoring tool to optimize feeding and oxygen management, enhancing production efficiency. Venture capital investment in aquaculture technology, particularly in feed optimization and automated water management, continues to rise across the region.

Europe Aquaculture Market Trends - Regulatory Leadership and Green Innovation

Europe’s aquaculture sector is shaped by strong regulatory oversight, sustainability mandates, and high consumer awareness. The regional market is projected to grow at about 5% CAGR through 2032, with leading countries including Norway, the U.K., France, and Spain. Europe’s salmon farming industry remains a benchmark for sustainability and efficiency, supported by advanced offshore technology and stringent quality standards.

Regulatory harmonization under the EU’s Common Fisheries Policy (CFP) facilitates investment in sustainable aquaculture while ensuring environmental compliance. The EU’s Blue Growth Strategy and Green Deal provide funding for offshore, RAS, and integrated multitrophic aquaculture systems.

In February 2025, Mowi ASA introduced a low-carbon salmon brand sourced from its fully electrified Scottish farms, aligning with EU sustainability goals. In late 2024, Grieg Seafood began pilot testing of autonomous feeding drones to reduce feed waste in Norway’s coastal farms.

The European Investment Bank (EIB) announced new financing worth €200 Million (US$233 Million) in December 2024 to support algae farming and climate-resilient aquaculture infrastructure. Investment trends also highlight growing interest in shellfish production and circular water use systems. While margins are compressed by high operational costs, Europe remains the world’s innovation hub for environmentally responsible aquaculture.

Asia Pacific Aquaculture Market Trends - Global Production Powerhouse and Smart Farming Adoption

Asia Pacific accounts for over 68% of global aquaculture production, dominating both volume and revenue. The regional market, valued at approximately US$230 Billion in 2025, is forecast to surpass US$340 Billion by 2032. China leads global production, followed by India, Indonesia, Vietnam, and Thailand. Growth is supported by government incentives, abundant coastal and freshwater resources, and export-driven strategies.

The Indian shrimp industry has become a major foreign exchange earner, while China continues to pioneer integrated aquaculture-agriculture systems. ASEAN nations are strengthening cold-chain infrastructure and certification systems to enhance competitiveness. Asia’s leadership is reinforced by cost-effective labor, rapid adoption of smart farming technologies, and diversified species portfolios.

In April 2025, Zhejiang Ocean Family Co. launched a smart aquaculture base in Fujian, China, integrating IoT-based feeding and real-time water monitoring. In June 2025, Devi Seafoods Ltd. in India expanded shrimp processing capacity by 30%, targeting growing U.S. and European demand. In 2024, Charoen Pokphand Foods (CPF) introduced blockchain-based traceability systems across its shrimp supply chain in Thailand.

Vietnam’s Ministry of Agriculture announced in late 2024 a national aquaculture modernization plan emphasizing disease control and sustainability certification for export markets. Despite challenges such as disease outbreaks and uneven regulations, Asia Pacific will continue to anchor global aquaculture growth through scale, innovation, and market diversity.

Competitive Landscape

The global aquaculture market is moderately consolidated, with the top 10 players holding 35-40% of market value, while numerous regional producers dominate local species. Industry dynamics favor sustainability, technological integration, and value-chain control.

Market leaders pursue vertical integration across feed, farming, processing, and retail, alongside geographic diversification and innovation in feed and technology. Emerging models such as direct-to-consumer delivery, blockchain traceability, and aquaculture-as-a-service are reshaping competition and enhancing efficiency in the global market.

Key Industry Developments

- In August 2025, DNV introduced an AI-powered fish-farm monitoring technology aimed at reducing operational costs and improving compliance for salmon producers in Norway.

- In July 2025, Grieg Seafood ASA announced the sale of its British Columbia salmon-farming operations to Cermaq Group AS, enabling a strategic shift toward more sustainable production and international repositioning.

Companies Covered in Aquaculture Market

- Mowi ASA

- Thai Union Group PCL

- Nippon Suisan Kaisha Ltd.

- Cooke Aquaculture Inc.

- Charoen Pokphand Foods PCL

- Cermaq Group AS

- Grieg Seafood ASA

- Tassal Group Ltd.

- Huon Aquaculture Group Ltd.

- Nireus Aquaculture S.A.

- Blue Ridge Aquaculture Inc.

- Marine Harvest Canada

- Avramar Group

- Bakkafrost P/F

- AquaChile S.A.

- The Scottish Salmon Company Ltd.

- Lerøy Seafood Group ASA

- Shandong Homey Aquatic Development Co. Ltd.

- Zhangzidao Group Co. Ltd.

- Clearwater Seafoods Inc.

Frequently Asked Questions

The aquaculture market size is estimated at US$327.4 Billion in 2025.

By 2032, the aquaculture market is projected to reach US$463.5 Billion.

Key trends include the adoption of recirculating aquaculture systems (RAS), AI-driven water quality management, growth in sustainable feed formulations, expansion of offshore and land-based aquaculture, and increasing consumer preference for traceable and eco-certified seafood.

The finfish segment leads the global market, accounting for over 59% of total value in 2025, supported by strong demand for species such as salmon, tilapia, and carp. Within the value chain, commodity aquaculture remains the dominant production category.

The aquaculture market is projected to grow at a CAGR of 5.1% between 2025 and 2032.

Major players include Mowi ASA, Thai Union Group PCL, Nippon Suisan Kaisha Ltd., Cooke Aquaculture Inc., and Charoen Pokphand Foods PCL.