- Semiconductor Materials & Components

- Silicon Photonics Market

Silicon Photonics Market Size, Share, and Growth Forecast 2026 - 2033

Silicon Photonics Market by Component (Photodetectors, Optical Waveguides, Wavelength-Division Multiplexing (WDM) Filters, Lasers, Optical Modulators), Product (Transceivers, Active Optical Cables, Optical Multiplexers, Optical Attenuators, Others), Application (Data Center and High Performance Computing, Consumer Electronics, Healthcare & Life Sciences, Aerospace, Defense and Security, Automotive, Others), Regional Analysis, 2026 - 2033

Silicon Photonics Market Size and Trend Analysis

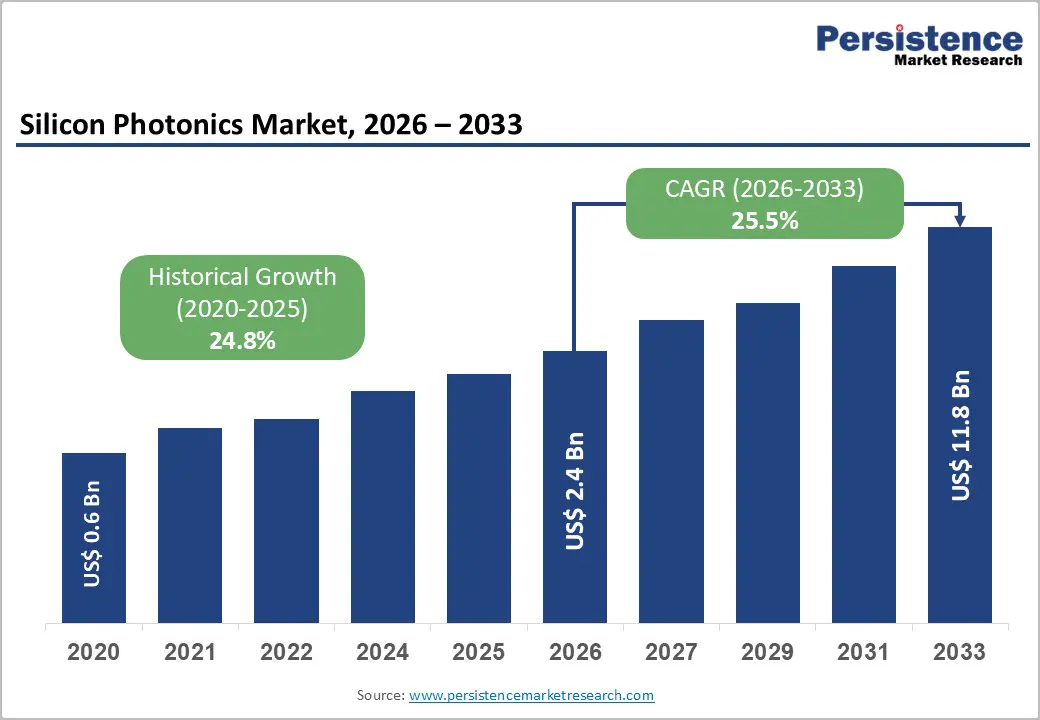

The global silicon photonics market size is likely to be valued at US$ 2.4 billion in 2026 and is expected to reach US$ 11.8 billion by 2033, growing at a CAGR of 25.5% during the forecast period from 2026 to 2033.

Strong demand for high-bandwidth, energy-efficient interconnects in data centers and high-performance computing, together with rapid advances in photonic integrated circuits, is accelerating adoption.

Key Industry Highlights:

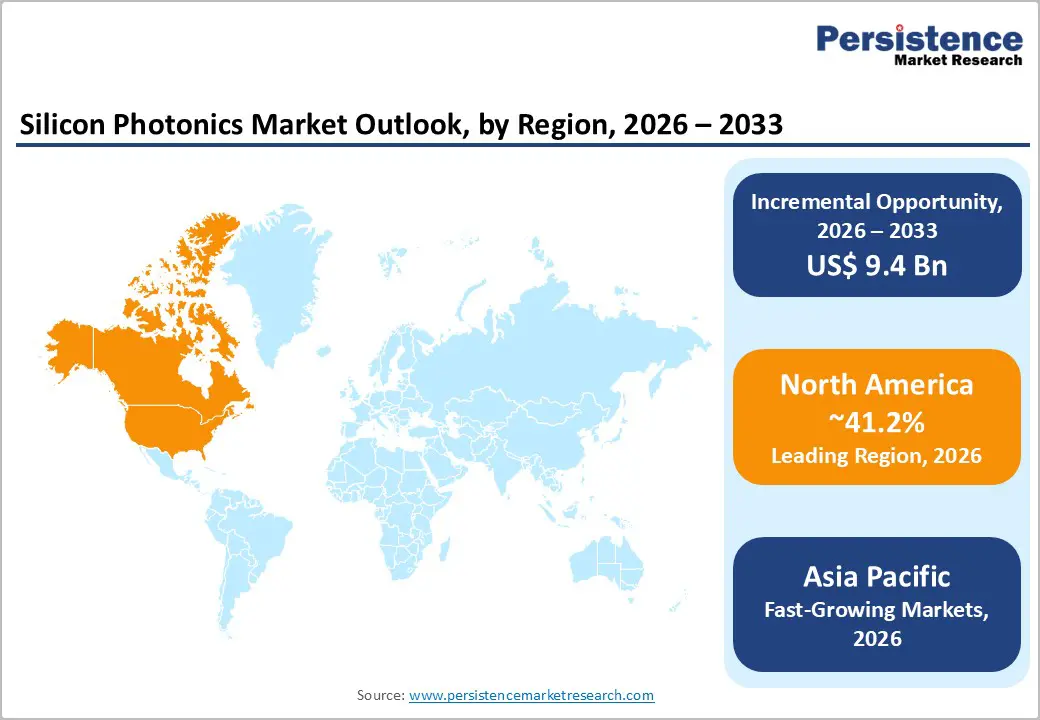

- Leading Region: North America is the Dominant regional market for silicon photonics, holding 41.2% share, driven by a robust presence of U.S. cloud service providers, semiconductor firms, and photonics manufacturers.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region in the silicon photonics market with rising CAGR of 30.7%, supported by robust semiconductor manufacturing capabilities and increasing investments in digital infrastructure.

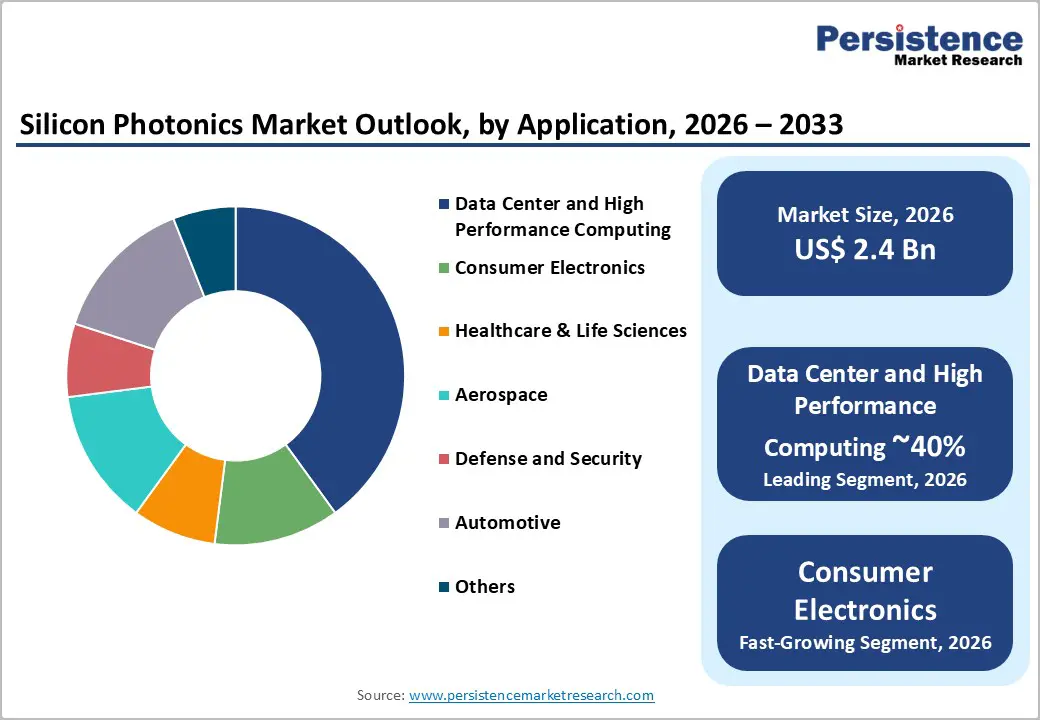

- Leading Segment: Data Center and High-Performance Computing (HPC) account for about 40% of global silicon photonics demand, dominating the photonic integrated-circuit market. Data-center interconnects are the primary drivers of silicon photonics optical-receiver shipments.

- Fastest-Growing Segment: Within products, silicon photonics transceivers form the fastest-growing segment, capturing roughly 28.3% of CAGR value as they replace discrete optics in short-reach and data-center-interconnect applications requiring dense, low-power optical I/O.

- Key Market Opportunity lies in co-packaged optics and photonic converged switches, where integrating switching silicon and photonics can significantly reduce power consumption for 51.2 Tb/s platforms, substantially lowering data-center operating costs while enabling scalable AI-ready network fabrics.

| Key Insights | Details |

|---|---|

| Silicon Photonics Market Size (2026E) | US$ 2.4 billion |

| Market Value Forecast (2033F) | US$ 11.8 billion |

| Projected Growth CAGR (2026 - 2033) | 25.5% |

| Historical Market Growth (2020 - 2025) | 24.8% |

Market Dynamics

Drivers - AI Workloads and Expanding Data Centers Intensify Demand for High-Bandwidth, Energy-Efficient Silicon Photonics Interconnect Solutions

The strongest growth driver for the silicon photonics market is the rapid expansion of cloud infrastructure, AI computing needs, and high-performance data-center architectures. Every new generation of AI servers requires several 800 Gb/s optical transceivers, and technology roadmaps already indicate a shift toward 1.6 Tb/s and even higher-capacity links later this decade. These extreme bandwidth levels cannot be met cost-effectively or efficiently using traditional electrical interconnects.

Silicon photonics enables high-density optical input/output with much lower power consumption per bit, reducing cooling loads that typically represent 40% of total data-center energy use. In addition, the integration of photonic circuits inside switches and transceivers reduces equipment size and enables higher-radix switch designs. As hyperscale cloud platforms and HPC operators continue to scale network capacity, silicon photonics is becoming a core technology supporting future bandwidth, latency, energy-efficiency, and system-scalability requirements.

Government Funding and Public-Private Partnerships Accelerate Global Development of Advanced Silicon Photonics Manufacturing and Innovation Ecosystems

Government policies and public-private initiatives are providing strong support for the expansion of silicon photonics. In the United States alone, state and federal programs have committed more than US$ 300 million to photonics manufacturing institutes and university-industry partnerships focused on telecom, defense, and advanced computing.

Similar initiatives across Europe and Asia are investing in pilot production lines, advanced packaging technologies, and design platforms that strengthen the regional integrated-photonics supply chain. These programs help lower market-entry barriers for fabless companies, improve access to CMOS-compatible foundries, and encourage the development of standardized platforms. This ecosystem support accelerates the transition of silicon photonics from research to commercial deployment in areas such as data communications, sensing, and quantum technologies. Over time, these coordinated efforts create a stable innovation environment that promotes technology maturity, cost reduction, and wider adoption across multiple industries.

Restraints - Complex Fabrication Processes, Integration Challenges, and Yield Issues Continue to Slow Commercial Scaling of Silicon Photonics Technologies

Although silicon photonics benefits from CMOS compatibility, the overall fabrication and packaging process remains technically challenging. Integrating III-V lasers with silicon, managing heat, and achieving low-loss optical coupling all create yield and reliability concerns. Industry assessments show that adjustments in yield expectations and average selling prices have resulted in more cautious shipment forecasts for silicon photonics products during the mid-2020s.

These technical hurdles can raise production costs, extend qualification timelines, and slow the shift from conventional discrete optical components, particularly in cost-sensitive telecom markets. For many operators, the need for predictable performance and long-term reliability makes them cautious when adopting newer integrated approaches. As manufacturing processes mature and packaging techniques improve, these challenges will gradually ease. However, in the near term, they continue to act as a restraint, limiting the speed at which silicon photonics can scale in high-volume, price-competitive environments.

Lack of Unified Standards and Limited Interoperability Across Platforms Restrict Broad Adoption of Silicon Photonics Products

The lack of complete standardization across silicon photonics platforms, packaging methods, and control electronics remains a barrier to widespread adoption. Although organizations such as IEEE and several industry alliances are defining standards for 400G, 800G, and next-generation interconnects, variations still exist in modulation formats, thermal tuning strategies, and device-control protocols. This inconsistency increases system-integration complexity for equipment manufacturers and hyperscale operators, who must verify performance and interoperability across products from different vendors.

Limited standardization also slows the development of unified design and testing frameworks, delaying product-release cycles and reducing opportunities for economies of scale. Since cost reduction is crucial for accelerating market penetration, especially in telecom and access networks, the current fragmentation moderates the pace of adoption. As standardization efforts advance and multivendor interoperability improves, these challenges are expected to decline, supporting broader commercialization of silicon photonics.

Opportunity - AI-Driven Data Centers Create Strong Opportunities for Next-Generation Optical Interconnects and Co-Packaged Silicon Photonics Solutions

The shift toward AI-optimized infrastructure is creating major growth opportunities for silicon photonics suppliers. Modern AI clusters rely on tens of thousands of interconnected GPUs, pushing bandwidth requirements for rack-to-rack communication into tens of terabits per second. Silicon-photonics-based co-packaged optics and converged switch architectures allow switching, routing, and optical functions to be tightly integrated into a single platform. This enables significantly lower energy consumption, with next-generation 51.2 Tb/s switches achieving more than 50% power reduction compared with traditional pluggable optics.

Such improvements directly support hyperscalers’ sustainability goals and reduce total operational costs. As data-center designs transition toward 800G, 1.6T, and emerging multi-terabit optical links, suppliers offering advanced transceivers, co-packaged optics, and photonic switching solutions are positioned for strong demand. These capabilities are particularly valuable in AI mega-data centers, where performance, density, and energy efficiency are top priorities.

Growing Adoption of Silicon Photonics in LiDAR, Healthcare Diagnostics, and Sensing Unlocks New Multi-Industry Market Potential

Beyond data-center and telecom uses, silicon photonics is gaining momentum in industries that depend heavily on compact and accurate sensing technologies. Photonic integrated circuits enable solid-state LiDAR systems for advanced driver-assistance applications, and tightening safety regulations across North America, Europe, and Asia are accelerating their adoption. In healthcare and life sciences, silicon photonics supports high-precision biosensing, medical imaging, and optical-coherence-tomography systems due to its sensitivity and ability to integrate multiple optical functions on a single chip.

Increasing public and private funding for medical diagnostics, smart mobility, and sensor innovation is further boosting demand. As companies adapt high-volume silicon-photonics manufacturing processes, originally developed for data-center applications-to these adjacent markets, they gain opportunities to deliver scalable, low-cost, and high-performance sensing solutions. These cross-industry applications significantly broaden the long-term growth potential of the technology.

Category-wise Analysis

By Component Insights

Transceiver-focused building blocks, especially lasers and optical modulators, represent the largest share of silicon photonics revenue. Lasers alone are estimated to contribute nearly 35% of total market value. Their importance stems from the critical role high-quality light sources and high-speed modulators play in enabling 400G and 800G data-center connections and advanced coherent-telecom systems. As hyperscale operators increasingly deploy dense optical interconnects, demand for advanced laser and modulator components continues to rise faster than for more mature components such as basic waveguides and photodetectors. This ongoing need for performance improvement is expected to further strengthen the leadership position of lasers and modulators within the component landscape.

By Product Insights

Among products, silicon-photonics-based transceivers dominate the market, accounting for around 60% of total revenue. Industry leaders have shipped millions of photonic integrated circuits for transceivers since the mid-2010s, demonstrating the maturity and scalability of this segment. Silicon-photonics transceivers are widely used in data-center interconnects, metro networks, and short-reach links where high bandwidth density, improved energy efficiency, and compact design are essential. As networks transition from 100G and 200G toward 400G, 800G, and beyond, the shift to co-packaged optics and on-board optical solutions significantly favors silicon photonics over traditional discrete optical modules. These newer designs enable more efficient integration, lower power consumption, and better scalability. Consequently, transceivers are expected to remain the core revenue-generating product category for silicon photonics vendors in the medium term.

By Application Insights

Data Center and High-Performance Computing (HPC) continues to be the leading application area, representing approximately 40% of global silicon photonics demand. The broader photonic integrated-circuit market is already dominated by data-center and HPC workloads, with data-center interconnects driving most silicon photonics optical-receiver shipments. Hyperscale cloud operators are building larger campuses and distributed edge facilities that require multi-terabit, low-latency optical interconnects. Enterprise and government HPC facilities add further demand as they upgrade to next-generation architectures. Compared with telecom access networks, consumer electronics, or smaller niche applications, data centers offer much larger deployment volumes and faster technology-refresh cycles. This consistently strong demand makes the data-center segment the main commercial engine for silicon photonics and is expected to maintain its leadership through the forecast period.

Regional Insights

North America Silicon Photonics Market Trends

North America remains the largest regional market for silicon photonics, supported by the strong presence of U.S. cloud service providers, semiconductor companies, and photonics manufacturers. The region hosts many of the world’s largest hyperscale data centers, and the transition toward 800G and emerging 1.6T optical connectivity is driving continuous demand for advanced silicon-photonics transceivers and switching platforms. Federal and state programs have invested more than US$ 300 million in integrated-photonics institutes and research centers that focus on packaging innovation, heterogeneous integration, and device design.

Regulatory attention on energy efficiency and digital-infrastructure resilience further encourages the use of low-power optical interconnects. Canada also contributes through active support for photonics start-ups and investments in autonomous-vehicle and sensing technologies. Together, these factors reinforce North America’s position as a global leader in both adoption and innovation across data-communication, defense, and sensing applications using silicon photonics.

Europe Silicon Photonics Market Trends

Europe represents a steadily expanding market for silicon photonics, driven by strong research ecosystems and coordinated regulatory support. Key countries such as Germany, France, the Netherlands, and the U.K. host leading photonics institutes and multi-project wafer programs that provide foundry access for start-ups, SMEs, and academic groups. These initiatives accelerate innovation across telecom, datacom, and sensing applications. The European Union’s digital-strategy and semiconductor programs prioritize advanced photonics, with funding directed toward pilot manufacturing lines, packaging facilities, and quantum-communication testbeds built on silicon-photonics platforms.

On the demand side, Europe’s data-center footprint is growing due to cloud adoption, 5G expansion, and increasing edge-computing needs, especially in Frankfurt, London, Amsterdam, and Paris. Regulatory frameworks such as the European Green Deal promote energy-efficient technologies, driving interest in silicon-photonics-based interconnects. Telecom operators upgrading metro and long-haul networks to 400G/800G coherent systems are also evaluating integrated photonics, supporting strong regional growth.

Asia Pacific Silicon Photonics Market Trends

Asia Pacific is the fastest-growing region in the silicon photonics market, driven by strong semiconductor manufacturing capabilities and expanding digital-infrastructure investments. Major economies including China, Japan, South Korea, and Taiwan host globally significant foundries and advanced photonics-packaging centers that support large-scale production of photonic integrated circuits. Rapid investments in cloud data centers, 5G deployments, and AI computing clusters are increasing demand for high-speed optical interconnects where silicon photonics provides energy-efficient and scalable solutions.

In India and leading ASEAN countries, government-backed digital programs and expanded fiber-optic networks are laying the foundation for broader adoption of silicon photonics in telecom and data-center environments. Additionally, regional electronics and consumer-device manufacturers are exploring silicon-photonics-based solutions for LiDAR, sensing, and short-reach interconnects. These combined drivers position Asia Pacific as a major engine of volume growth, manufacturing innovation, and cost-optimized silicon-photonics development.

Competitive Landscape

The silicon photonics market is moderately concentrated, with a mix of large incumbent semiconductor and networking vendors alongside specialized photonics players and foundries. Companies such as Intel Corporation, Cisco Systems, Inc., Broadcom Inc., IBM Corporation, GlobalFoundries U.S. Inc., and Lumentum Operations LLC play pivotal roles across transceivers, switches, design platforms and manufacturing services. Many leaders focus on co-packaged optics, high-speed transceivers, and photonic integrated circuit roadmaps aimed at 800G and beyond. Strategic partnerships between device makers, foundries, and packaging houses are common, while start-ups differentiate through novel modulators, lasers, and application-specific PICs. Overall, competition is intensifying as vendors race to meet hyperscale, telecom, and sensing requirements with higher integration, lower power, and more cost-effective solutions.

Key Developments:

- In January, 2024: Intel Corporation advanced its co-packaged optics strategy by expanding availability of silicon-photonics-based high-radix switch platforms targeting AI and cloud data centers.

- In October, 2023: Coherent Corp. announced new 1.6 Tb/s-class silicon photonics transceivers designed for next-generation data-center interconnects and AI cluster connectivity, highlighting rapid performance scaling in PIC-based modules.

- In December, 2023: InnoLight Technology reported achieving 1.6 Tb/s transfer speeds in its latest silicon-photonics-enabled transceivers, underscoring growing commercial readiness of ultra-high-speed modules for hyperscale networks.

Companies Covered in Silicon Photonics Market

- Cisco Systems, Inc.

- Intel Corporation

- MACOM

- Lumentum Operations LLC

- Juniper Networks

- GlobalFoundries U.S. Inc.

- IBM Corporation

- Broadcom Inc.

- Hamamatsu Photonics K.K.

- Synopsys, Inc.

- OSCPS Motion Sensing Inc.

- Marvell Technology, Inc.

- Coherent Corp.

- Infinera Corporation

- InnoLight Technology

- Ayar Labs

- STMicroelectronics

Frequently Asked Questions

The global silicon photonics market is expected to reach around US$ 11.8 billion by 2033, growing from approximately US$ 2.4 billion in 2026 at a forecast CAGR of about 25.5% over 2026-2033.

Key demand drivers include explosive bandwidth requirements from cloud and AI data centers, the shift toward 800G and 1.6T optical links, and tightening energy‑efficiency regulations that favor low‑power photonic interconnects.

The Data Center and High Performance Computing segment leads the market, accounting for an estimated over 40% share of global revenue as hyperscale operators deploy silicon‑photonics‑based transceivers and switches for high‑capacity, energy‑efficient interconnects.

North America holds the largest market share, supported by the presence of major hyperscale cloud providers, networking OEMs, and integrated‑photonics research institutes, as well as strong public‑sector investments in photonics manufacturing and R&D.

A major opportunity lies in co‑packaged optics and converged photonic switches for AI‑centric data centers, where integrating optics with switching silicon can dramatically reduce power consumption and enable scalable, high‑bandwidth network fabrics.

Prominent players include Cisco Systems, Inc., Intel Corporation, Broadcom Inc., IBM Corporation, Lumentum Operations LLC, GlobalFoundries U.S. Inc., Marvell Technology, Inc., Hamamatsu Photonics K.K., Synopsys, Inc., and emerging innovators such as Coherent Corp., Infinera Corporation, InnoLight Technology, Ayar Labs and STMicroelectronics.