- Inks, Coatings, Adhesives & Sealants (ICAS)

- Ferrosilicon Market

Ferrosilicon Market Size, Share, and Growth Forecast, 2026 - 2033

Ferrosilicon Market by Form (Lumps, Granules, Powder), Application (Deoxidizer, Inoculant, Others), End-User (Carbon & Other Alloy Steel, Stainless Steel, Electric Steel, Cast Iron, Others), and Regional Analysis for 2026 - 2033

Ferrosilicon Market Share and Trends Analysis

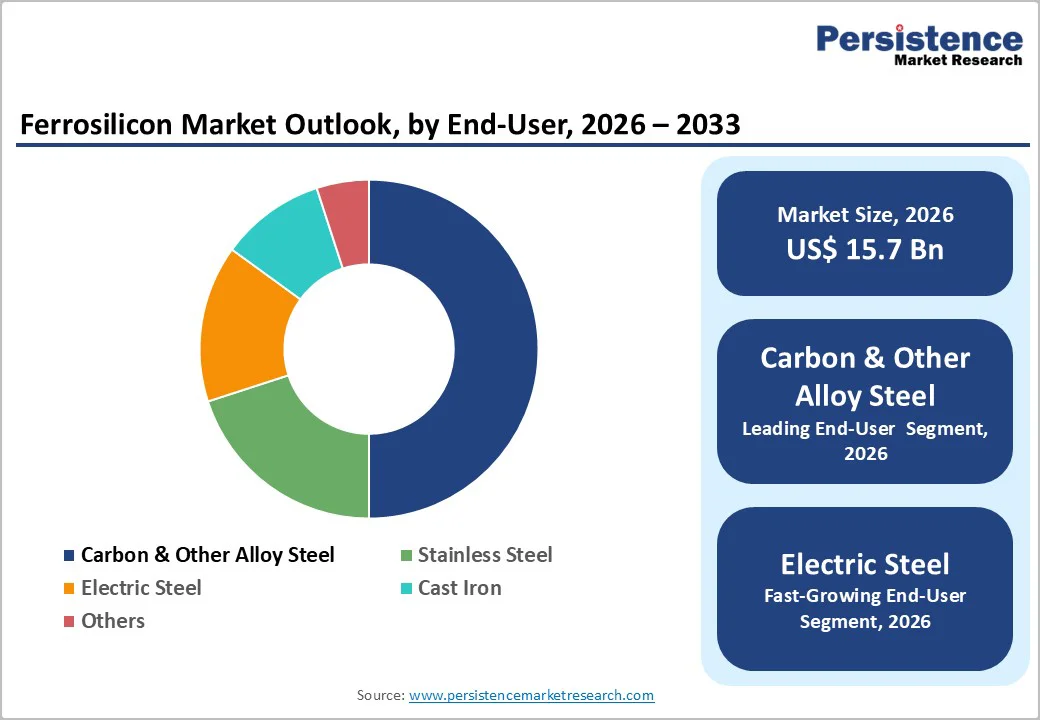

The global ferrosilicon market size is likely to be valued at US$ 15.7 billion in 2026, and is projected to reach US$ 20.9 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033. Persistent steel output gains, accelerating adoption of electric arc furnace (EAF) technology, and heightened requirements for alloy and specialty steels propel this trajectory. Construction projects demand structural grades with predictable tensile properties, automotive manufacturers specify advanced high-strength steels for lightweighting and safety, and energy infrastructure relies on corrosion-resistant materials for extended service life.

Procurement teams should recognize these sector-specific dynamics when planning ferrosilicon supply agreements to align grade specifications with end-use performance targets. Ferrosilicon (FeSi) functions as both a deoxidizer and inoculant in steelmaking and foundry operations, directly influencing final product quality, mechanical strength, and casting yield. Operators who optimize FeSi dosing rates can reduce slag volumes, improve metal cleanliness, and achieve tighter control over carbon and silicon content. This precision translates into fewer rejects, lower rework costs, and enhanced customer satisfaction.

Key Industry Highlights

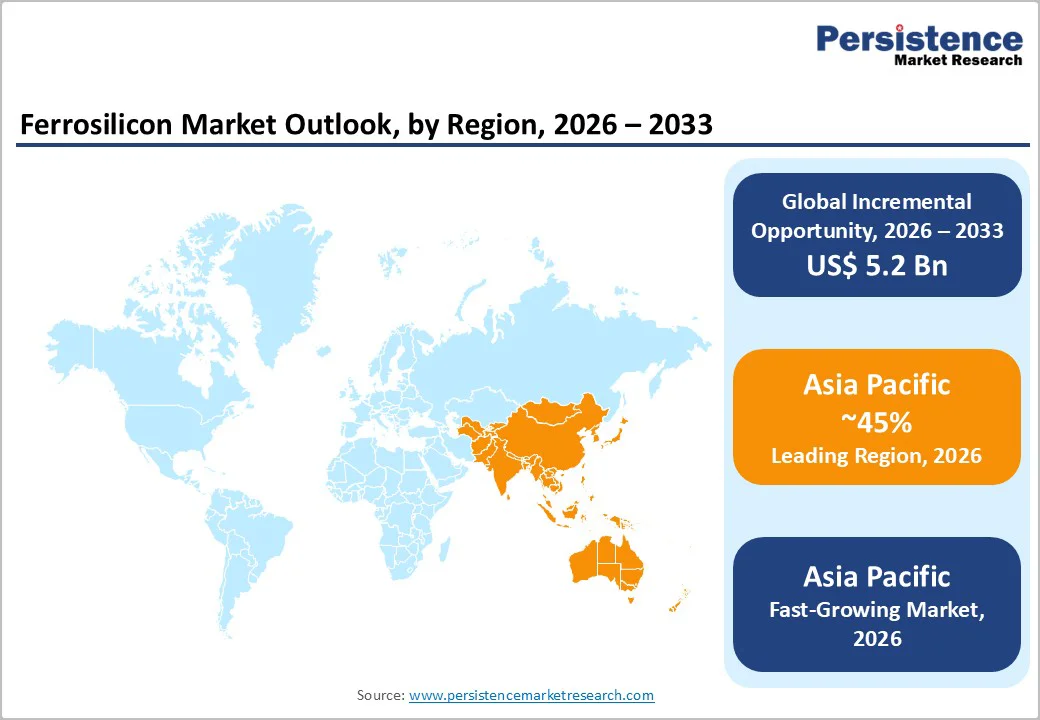

- Dominant Region: Asia Pacific is expected to lead with an estimated 45% of the ferrosilicon market revenue share, supported by well-established steel and alloy production infrastructure.

- Fastest-growing Market: Asia Pacific is estimated to be the fastest-growing market through 2033 due to the rising demand for premium ferrosilicon in electric vehicles (EVs) and renewable energy.

- Leading End-User: Carbon and other alloy steel producers are anticipated to account for around 50% of the revenue share in 2026, as a result of high demand for deoxidation and alloying in industrial steel applications.

- Fastest-growing End-User: Electric steel is set to be the fastest-growing end-user segment through 2033, aided by renewable energy expansion and surging EV motor production.

| Key Insights | Details |

|---|---|

|

Ferrosilicon Market Size (2026E) |

US$ 15.7 Bn |

|

Market Value Forecast (2033F) |

US$ 20.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth in Global Steel Production and Infrastructure Investment

Global steel production growth has heightened the demand for essential alloying elements that improve deoxidation and refine grain structures during furnace processes. Steelmakers achieve desired mechanical strength and uniformity in high-volume batches through these inputs. Production scale-ups make such materials standard procurement items for consistent quality control. Operators should audit alloy blends against current output targets to optimize yield rates and minimize rejects in expanding facilities.

Infrastructure investments accelerate usage by requiring robust, long-span steel for transportation networks, energy installations, and city developments. These applications demand reliable tensile properties and seamless weldability from proven additives. World crude steel output hit 166.1 million tons across reporting nations in March 2025, marking a 2.9% year-on-year increase that signals robust project pipelines. Procurement teams gain by locking in forward contracts for alloy supplies and aligning specifications with regional build cycles to secure cost stability amid rising volumes.

Fluctuations in Raw Material and Energy Prices

Fluctuations in raw material and energy prices create cost instability across the production chain, directly influencing operational planning and pricing strategies. Core inputs such as quartz, iron ore, and coke are exposed to global commodity cycles, trade policies, and supply disruptions, which limits cost predictability. Energy intensity remains high across smelting and furnace operations, making electricity price volatility a critical concern. Power tariffs often vary due to regulatory revisions, fuel price changes, and grid availability, creating uneven production economics across regions. This instability weakens margin control and complicates long-term supply agreements with downstream industries.

Price volatility also affects capital allocation and capacity utilization decisions. Producers face challenges in maintaining consistent output when input costs rise sharply, leading to production curtailments or delayed expansion plans. Procurement teams encounter difficulty in negotiating fixed-price contracts, which shifts risk exposure across the value chain. End-user industries are known to respond by delaying purchases or seeking alternative materials during periods of elevated pricing pressure. Such conditions reduce demand visibility and weaken supplier–customer alignment.

Premium and Low-Impurity Ferrosilicon Grades

Premium and low?impurity ferrosilicon grades are increasingly central as steelmakers and alloy producers tighten quality and performance standards for advanced applications. High?value sectors such as automotive, electrical and renewable energy steels require consistent silicon recovery and minimal contaminants to improve yield, reduce defects and support lean operational frameworks. Buyers now emphasise traceability, stable specifications and documented chemistry control, strengthening procurement relationships with reliable suppliers. This trend shifts commercial focus toward value?added products, enabling producers of cleaner grades to command differentiated pricing and long?term supply contracts.

Environmental and regulatory requirements are increasingly shaping sourcing strategies, driving demand for low?impurity ferrosilicon. Cleaner inputs minimize slag formation, lower energy consumption during melting, and contribute to more sustainable steel production. Consistent chemistry reduces operational disruptions, scrap generation, and rework, supporting efficiency and cost optimization across production lines. Steelmakers and alloy producers prioritize suppliers who can deliver documented quality, traceability, and reliable supply to meet stringent compliance and performance standards.

Category-wise Analysis

Form Insights

Lumps are poised to dominate, with a forecasted market share of 45% in 2026, due to their widespread use in large-scale steelmaking operations, ease of handling in blast furnaces, and high silicon recovery rates that ensure efficient alloying and cost-effective production. Their consistent quality and performance make them the preferred choice for integrated steel plants, supporting long-term procurement strategies and operational reliability. Steelmakers value lump ferrosilicon for its ability to minimize production losses and streamline bulk steelmaking processes, reinforcing its position as the leading segment globally.

Powdered ferrosilicon is estimated to be the fastest-growing segment from 2026 to 2033, propelled by increasing adoption in foundry inoculation and specialized steel applications. Precise dosing and uniform distribution improve metallurgical consistency, reduce defects, and minimize scrap generation. Its fine particle size supports operational efficiency and high-quality output, making it essential for technologically advanced steel and alloy processes. Producers capable of delivering high-purity powder grades are well-positioned to capture this growth opportunity and meet evolving industry demands.

Application Insights

Deoxidizers are anticipated to secure around 55% of the ferrosilicon application market share in 2026, driven by their essential role in oxygen removal during steel production, which enhances surface finish, mechanical strength, and overall steel integrity. Steelmakers increasingly rely on ferrosilicon deoxidizers to maintain consistent quality, reduce defects, and optimize yield across high-performance applications such as automotive components, construction materials, and heavy machinery. This critical function positions deoxidizers as the leading contributor to global ferrosilicon demand and underscores their importance in modern steelmaking processes.

Inoculants are expected to be the fastest-growing segment during the 2026-2033 forecast period, supported by rising cast iron production, advanced casting techniques, and automotive lightweighting initiatives. The segment benefits from high-precision engineering requirements and automated foundry processes that demand improved microstructure control and mechanical properties. Ferrosilicon inoculants reduce porosity, enhance durability, and improve overall component performance, creating a strategic growth opportunity for suppliers targeting evolving metallurgical and industrial applications where quality and efficiency are increasingly decisive.

End-User Insights

Carbon and other alloy steel producers are projected to hold around 50% of the end-user market share in 2026, owing to strong demand from volume-intensive infrastructure, construction, and industrial projects. These steel grades require substantial ferrosilicon input for deoxidation and alloying to achieve mechanical strength, durability, and consistent metallurgical properties. The high consumption in structural steel, pipelines, and heavy machinery positions this segment as the largest end-user, reflecting its critical role in meeting global steel production requirements and sustaining large-scale industrial and infrastructure initiatives.

Electric steel is set to represent the fastest-growing end-user segment through 2033, driven by expanding renewable energy grids and rising production of electric vehicle motors. Ferrosilicon enhances magnetic properties, reduces energy losses, and ensures efficiency in electrical steels used in transformers, motors, and generators. The segment growth is reinforced by stringent efficiency and performance standards, driving adoption of high-quality ferrosilicon grades. Increasing electrification, green energy initiatives, and government mandates for energy-efficient components position electric steel as a high-potential growth opportunity.

Regional Insights

North America Ferrosilicon Market Trends

North America holds a leading position in the ferrosilicon market thanks to its advanced steel and alloy production infrastructure and rigorous manufacturing standards. The United States and Canada produce large volumes of specialty steels and electric steels, which depend on ferrosilicon for deoxidation, alloying, and inoculation. Reliable access to high-grade raw materials, modern smelting technology, and strict quality controls guarantee consistent product performance. Close collaboration between ferrosilicon suppliers and steelmakers streamlines supply chains, cuts costs, and supports vital industries such as automotive, aerospace, and heavy machinery.

Market expansion in North America will persist as investment grows in renewable energy infrastructure, electric vehicles, and advanced electrical steels. The drive for energy-efficient, low-emission steelmaking increases demand for low-impurity ferrosilicon to boost metallurgical performance and minimize operational losses. Industrial modernization, sustainability programs, and regulatory requirements further promote the adoption of premium ferrosilicon grades. Manufacturers should prioritize partnerships with suppliers who offer certified, traceable products to ensure compliance and optimize production outcomes.

Europe Ferrosilicon Market Trends

Europe remains a key ferrosilicon market since it produces high-quality steel and relies on specialized alloys for demanding applications. Germany, France, and Italy run mature steel and foundry ecosystems that use low-impurity ferrosilicon to meet strict mechanical and chemical requirements. Advanced refining practices help producers control alloy chemistry with high precision, which supports performance needs in sectors such as automotive, aerospace, and electrical engineering. Proximity to quality quartz resources and established ferroalloy sites, combined with integrated regional logistics, helps buyers secure dependable supply and consistent batch performance.

Growth prospects improve as Europe accelerates renewable energy deployment, electrification, and energy-efficient manufacturing. Expanding electric vehicle output, stronger demand for advanced electrical steels, and higher-accuracy precision engineering work all increase the need for high-purity ferrosilicon. Environmental and regulatory expectations also push mills toward cleaner grades that can reduce slag generation and lower energy use in smelting and refining operations. For procurement and technical teams, the practical path is to qualify suppliers on impurity control, consistency metrics, and documentation depth, then co-develop grade specifications with steelmakers and technology partners to improve yield, stability, and total cost of ownership.

Asia Pacific Ferrosilicon Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 45% of the ferrosilicon market share, propelled by high steel production volumes, rapid industrialization, and extensive infrastructure development. The market benefits from abundant raw materials such as quartz and high-silicon iron ores, enabling cost-efficient production and a stable supply chain. China and India dominate regional demand due to strong automotive, construction, and electrical steel sectors, while ongoing investments in high-purity and low-impurity ferrosilicon production support stringent quality requirements. Integration of upstream mining with downstream steelmaking enhances operational efficiency and market resilience.

Asia Pacific is also projected to be the fastest-growing market through 2033, driven by increasing adoption of premium ferrosilicon grades for advanced automotive, electric vehicle, and renewable energy applications. Expansion of foundries, casting operations, and industrial machinery manufacturing in South Korea and Southeast Asia fuels demand. Government initiatives promoting electrification, urbanization, and sustainable steel production, combined with technological modernization and proximity to raw materials, position the market as a strategic hub for both growth and innovation in ferrosilicon supply.

Competitive Landscape

The global ferrosilicon market structure is moderately consolidated, with the top five producers commanding approximately 45% of the total revenue share. Leading entities such as China Minmetals Corporation, Elkem ASA, Ferroglobe PLC, Eurasian Resources Group (ERG), and OM Holdings Ltd. leverage their capacity for large-scale output alongside reliable product consistency. These companies secure their dominance through direct access to premium quartz and silicon deposits, integrated smelting facilities, and robust distribution channels. Buyers benefit from partnering with these established suppliers to ensure supply stability and consistent material specifications across multiple sites.

Competition hinges on energy availability, production technology, and purity levels. Manufacturers with sophisticated refining processes and rigorous quality controls can deliver low-impurity and specialty grades that satisfy strict metallurgical standards. Operations that prioritize energy efficiency and vertical integration with raw material sources lower production costs and boost margins. Procurement teams should evaluate suppliers based on their technical capabilities and energy resilience to mitigate price volatility and quality risks in long-term contracts.

Key Industry Developments

- In November 2025, Kazakhstan launched EkibastuzFerroAlloys plant in Pavlodar region with a US$ 177 million investment, designed for 240,000 tons of high-grade FeSi75 annually using four 94.5 MVA furnaces. The eco-friendly facility achieves 99.8% gas cleaning, creates 800 jobs, and targets exports to 52 countries to boost the nation's ferroalloy leadership.

- In November 2025, the European Union (EU) imposed three-year safeguard measures on ferroalloy imports such as ferro-silicon and ferro-manganese via country-specific tariff-rate quotas (TRQs) at 75% of 2022-2024 averages. Out-of-quota volumes face duties if below thresholds, protecting EU producers whose market share fell from 38% to 24% amid 17% import surge. .

- In October 2025, Elkem ASA partially curtailed ferrosilicon production at its Rana plant in Norway and its Iceland facility due to challenging market conditions and heightened uncertainty from potential EU safeguard measures on ferroalloy imports. The cutbacks led to temporary layoffs and mainly affected standard FeSi output.

Companies Covered in Ferrosilicon Market

- China Minmetals Corporation

- Elkem ASA

- Ferroglobe

- Eurasian Resources Group

- OM Holdings Ltd.

- Finnfjord AS

- DMS Powders.

- AMG CHROME.

- SAKURA FERROALLOYS

- Tata Steel

Frequently Asked Questions

The global ferrosilicon market is projected to reach US$ 15.7 billion in 2026.

Rising steel production, demand for high-purity alloys, and growth in automotive, renewable energy, and construction sectors drive the market.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Expansion of low-impurity and premium-grade ferrosilicon for advanced steel, electric vehicles, and renewable energy applications represents key market opportunities.

Some of the key market players include China Minmetals Corporation, Elkem ASA, Ferroglobe, and Eurasian Resources Group.