- Semiconductor Materials & Components

- Silicon Capacitors Market

Silicon Capacitors Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Silicon Capacitors Market by Technology (MOS, MIS, Deep-Trench, MIM), Capacitance Range (Low (pF to nF), Medium (nF to µF), High (µF and above)), End-user (Consumer Electronics, Automotive Electronics, IT & Telecommunications, Aerospace & Defense, Industrial, Other), and Regional Analysis for 2026 - 2033

Silicon Capacitors Market Size and Trend Analysis

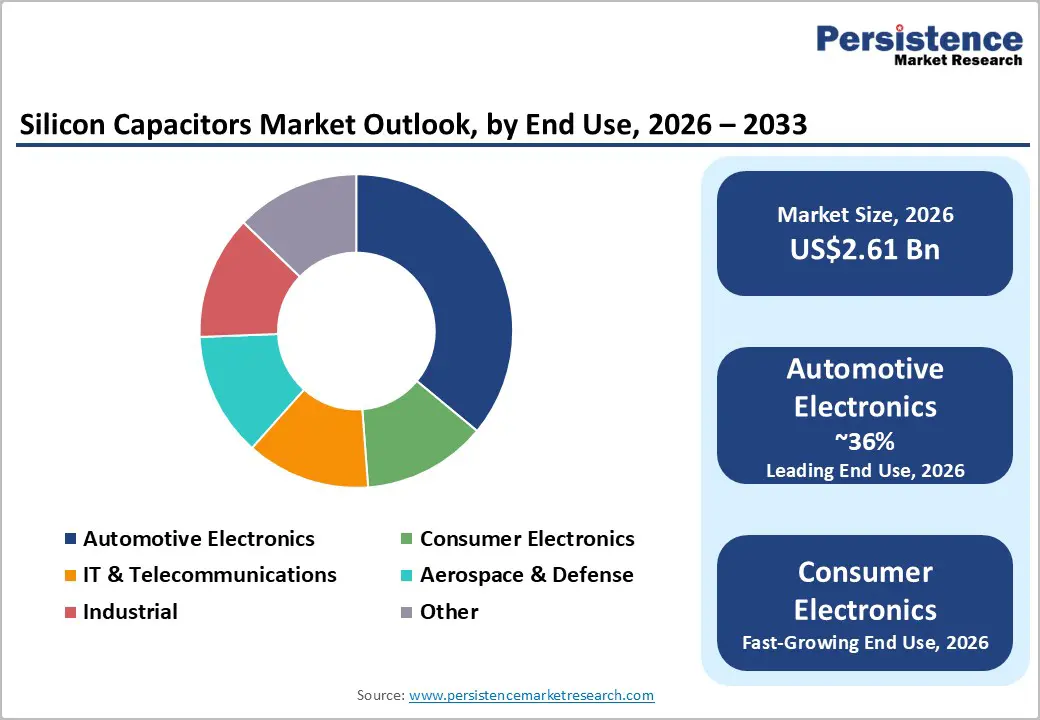

The global silicon capacitors market size is likely to be valued at US$ 2.6 billion in 2026 and is projected to reach US$ 4.5 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

The primary driver is surging demand for miniaturized, high-performance components in the electronics and automotive sectors. Advancements in 5G infrastructure and electric vehicles (EVs) require capacitors with superior thermal stability and high-frequency performance, outperforming traditional types. Integration with System-on-Chip (SoC) designs further accelerates adoption in wearables and IoT devices, enhancing power management and signal integrity.

Key Market highlights

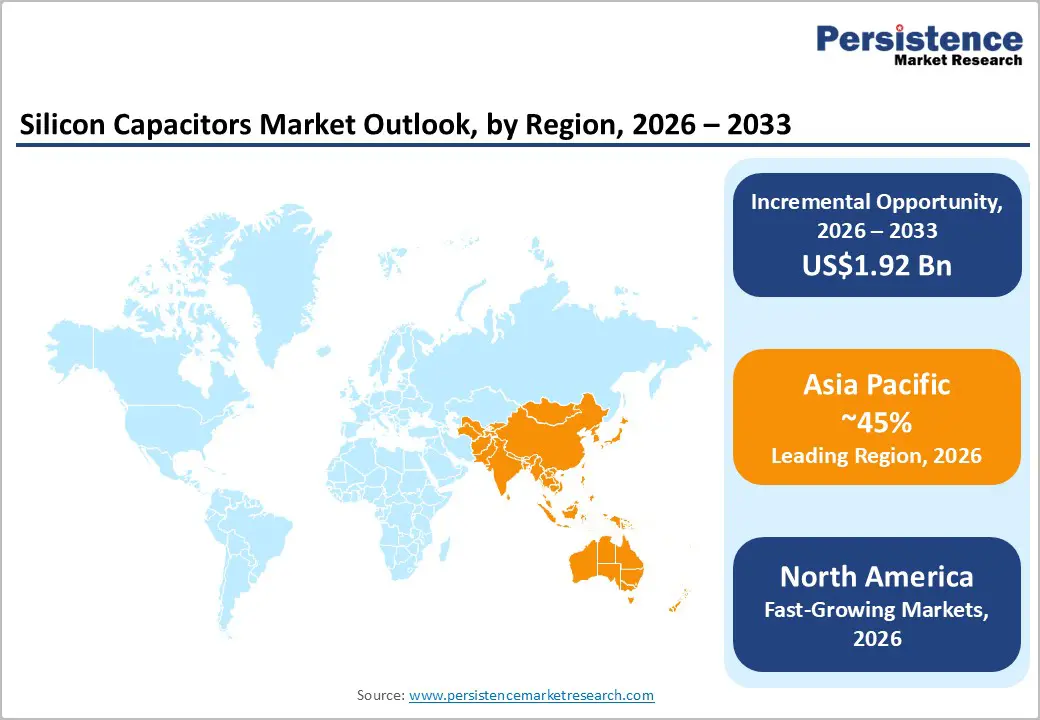

- Regional Leader: Asia Pacific dominates the silicon capacitors market, accounting for over 45% of the market share, driven by concentrated electronics manufacturing in China, Japan, South Korea, and Taiwan.

- Fastest-Growing Region: North America emerges as the fastest-growing regional market, driven by the CHIPS and Science Act, which allocates US$ 50 billion for semiconductor manufacturing incentives, and rising defense-sector demand for high-reliability components.

- Leading Segment: The Deep-Trench technology segment leads with 42% market share, attributed to superior capacitance density achieved through three-dimensional structures and compatibility with standard CMOS fabrication processes, enabling semiconductor integration.

- Fastest-Growing Segment: Automotive Electronics is the fastest-expanding end-use category, driven by electric vehicle electrification, battery management system sophistication, ADAS deployment, and automotive OEM requirements for AEC-Q-qualified components that meet stringent reliability and thermal specifications.

- Key Market Opportunities: Aerospace and defense applications present substantial opportunities, with ESA's ARTES programme funding space-qualified components and Airbus expanding procurement of silicon capacitors for orbital applications requiring extreme reliability and radiation tolerance.

| Key Insights | Details |

|---|---|

| Silicon Capacitors Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 4.5 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.2% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Drivers - Expanding 5G Network Infrastructure and High-Frequency Applications

The global rollout of 5G networks has created an unprecedented demand for silicon capacitors optimized for high-frequency performance. According to the Global System for Mobile Communications Association (GSMA), 5G connections are projected to exceed 1.8 to 2 billion by 2025, necessitating substantial investments in infrastructure. Silicon capacitors provide superior performance in 5G base stations due to their low equivalent series resistance (ESR), minimal signal loss, and stable capacitance across a wide temperature range.

In 2024, a leading South Korean electronics manufacturer, Samsung Electro-Mechanics, introduced high-capacity silicon capacitors specifically designed for 5G base stations, enhancing energy storage and signal reliability. The growth of the Internet of Things (IoT) market further supports this trend, with IoT device connections expected to reach 30 billion units by 2026. Each IoT device requires multiple miniaturized capacitors, making silicon technology the ideal solution for space-constrained applications.

Rise of Electric Vehicles and Automotive Electronics

The automotive industry's shift towards electrification is driving significant growth in the market for silicon capacitors, which offer excellent voltage handling and thermal resilience. Electric vehicle (EV) production has seen exponential growth, with global EV sales surpassing 14 million units in 2024, a 25% increase compared to the previous year, according to the International Energy Agency (IEA). Silicon capacitors are crucial for EV battery management systems, power conversion circuits, and regenerative braking systems due to their outstanding reliability at high temperatures and their ability to manage rapid charge-discharge cycles. In December 2024, TSMC and ROHM Semiconductor announced a strategic partnership to develop GaN-on-silicon technology for automotive power devices, with a focus on onboard chargers and inverters used in electric vehicles.

Furthermore, Advanced Driver-Assistance Systems (ADAS) utilize multiple silicon capacitors in sensor modules, radar systems, and electronic control units. Modern vehicles may contain over 150 capacitor units across various subsystems.

Restraints - High Manufacturing Costs and Capital-Intensive Production

The silicon capacitor industry, despite favorable market conditions, encounters significant challenges due to complex manufacturing processes that require specialized equipment and expertise. This results in high production costs, limiting market adoption. Producing silicon capacitors involves advanced semiconductor technologies and strict quality control, especially for critical aerospace and automotive applications. Techniques like deep-trench MOS and MIM capacitors require specialized etching equipment and clean room environments.

Initial capital investments to establish silicon capacitor production lines can exceed US$50 million, creating substantial barriers for new market entrants. The complex multi-layer deposition processes and stringent quality control requirements also contribute to higher per-unit manufacturing costs, limiting adoption in price-sensitive applications and consumer electronics segments where cost competitiveness remains paramount.

Competition from Established Ceramic Capacitor Technologies

Multilayer ceramic capacitors (MLCCs) hold a leading position in many applications due to their established manufacturing processes, extensive supplier networks, and cost advantages. In March 2025, KYOCERA AVX introduced the world's first MLCC capable of delivering 47 μF in a 0402-inch package, highlighting ongoing innovation in ceramic technology.

The global passive component market is estimated to be worth around $47.4 billion in 2025, with ceramic capacitors being the predominant solution. The established supply chains, proven reliability in standard applications, and decades of performance data provide MLCCs with substantial competitive advantages. Silicon capacitors face challenges in overcoming performance skepticism and must clearly demonstrate their value propositions to replace the well-established ceramic technologies in mainstream applications.

Opportunity - Integration with Renewable Energy Systems and Power Management

The rapid transition to renewable energy infrastructure presents significant opportunities for silicon capacitors in power conversion and energy storage applications. The Solar PV Panels Market continues to grow swiftly, with global installed capacity projected to exceed 1,000 GW by 2024. Silicon capacitors are crucial components in DC/DC converters, inverters, and maximum power point tracking (MPPT) systems within solar installations, offering superior performance compared to electrolytic alternatives.

In October 2025, KYOCERA AVX launched the commercial-grade KGP Series stacked multilayer ceramic capacitors, specifically designed for alternative energy applications, including solar power supplies and control circuits. The energy storage systems for grid stabilization, industrial uninterruptible power supply (UPS) applications, and residential battery backup solutions are increasingly specifying silicon capacitors due to their extended operational lifespans and minimal degradation characteristics.

Aerospace and Defense Applications Requiring Extreme Reliability

The aerospace and defense sectors offer significant growth opportunities for silicon capacitors due to their stringent reliability requirements in extreme environmental conditions. The European Space Agency (ESA) funds microelectronics research on space-qualified passive components through its ARTES program, recognizing the superior performance of silicon capacitors in radiation environments. Major aerospace manufacturers, including Airbus, have increased their procurement of silicon-based capacitors for space-grade printed circuit boards, as these components demonstrate unmatched durability in orbital environments where temperature fluctuations can exceed 200°C.

Silicon capacitors exhibit exceptional stability under thermal cycling, vibration, and shock conditions, as outlined in MIL-STD-883 specifications. The rising deployment of satellite constellations, modernization programs for military avionics, and deep-space exploration missions create a sustained demand for ultra-reliable passive components. This positions silicon capacitors as critical enabling technologies in the industry.

Category-wise Analysis

Technology Insights

Deep-trench technology holds a dominant position in the silicon capacitors market, with approximately 42% market share. This is largely due to its ability to achieve exceptional capacitance density through three-dimensional trench structures etched into silicon substrates. Deep-trench capacitors typically have depths ranging from 2,000 to 5,000 nanometers and widths between 50 and 200 nanometers, enabling capacitance values that are unattainable with planar designs.

Murata Manufacturing, after acquiring IPDiA, has established itself as a leader in deep-trench MOS capacitor technology, providing outstanding performance levels for RF and microwave applications. Metal-Insulator-Metal (MIM) capacitors that utilize high-k dielectric materials, such as hafnium oxide, achieve thicknesses ranging from 2 to 6 nanometers. These capacitors offer excellent linearity and low voltage coefficients, which are essential for precision analog circuits and timing applications.

Capacitance Range Insights

The high capacitance range (µF and above) commands approximately 43% of the market share, driven by demanding applications in power management, energy storage, and automotive electronics. High-capacitance silicon capacitors meet critical needs in electric vehicle (EV) battery management systems, where rapid charge-discharge cycles and compact form factors are essential. KYOCERA AVX's achievement of 47 μF in miniature 0402-inch packages exemplifies technological advancements that enable higher capacitance without a corresponding increase in size.

In data centers, telecommunications infrastructure, and industrial automation systems, there is an increasing specification of high-capacitance silicon components for power supply decoupling due to their superior ripple-current handling and low equivalent series resistance (ESR). The medium-capacitance range (nF to µF) is used in RF front-end modules, signal coupling, and high-speed digital interfaces, while low-capacitance values (pF to nF) are used in precision timing circuits and high-frequency filters.

End-user Insights

Automotive electronics is the leading end-use segment, holding approximately 36% of the market share. This growth is driven by the convergence of electrification and autonomous driving technologies. Modern electric vehicles contain over 3,000 passive components, with silicon capacitors being essential for mission-critical systems, including battery management, powertrain control, and safety systems. According to the Semiconductor Industry Association (SIA), the semiconductor content per vehicle has risen to about $600 in 2024, with passive components accounting for 15-20% of the total electronic component value. Advanced Driver Assistance Systems (ADAS) require capacitors that can operate reliably in temperatures ranging from -40°C to +150°C, a specification that silicon technology easily meets.

Furthermore, there is strong demand for silicon capacitors in consumer electronics such as smartphones, wearables, and Internet of Things (IoT) devices, where the need for miniaturization enhances silicon's high volumetric efficiency. The IT and telecommunications sector also benefits from 5G infrastructure deployments and the expansion of data centers, which require capacitors with exceptionally high-frequency performance and effective thermal management capabilities.

Regional Insights

North America Silicon Capacitors Market Trends

North America leads in silicon capacitor innovation, bolstered by strong R&D and early adoption of advanced electronics. The U.S. accounts for the largest share, driven by over $800 billion in annual aerospace and defense spending, according to the Department of Defense. At APEC 2025, Vishay Intertechnology presented a roadmap for SiC MOSFET technology, focusing on traction inverters and charging infrastructure. Strict automotive safety standards, such as FMVSS, create ongoing demand for high-reliability silicon capacitors. The regulatory framework also promotes environmental compliance, with the EPA encouraging electric vehicle adoption through incentives.

Companies like MACOM Technology Solutions and Skyworks Solutions are advancing silicon capacitor integration in RF semiconductor platforms. Furthermore, collaborations between academic institutions like MIT and Stanford University and industry partners focus on next-generation dielectric materials, ensuring continued innovation in this sector.

Europe Silicon Capacitors Market Trends

Europe’s silicon capacitors market is expanding rapidly, driven by stringent automotive electrification policies and renewable energy initiatives. Germany leads regional demand, producing over 4 million vehicles annually. The EU Green Deal, targeting a 55% emissions reduction by 2030, accelerates EV adoption and the need for advanced power electronics. ROHM Semiconductor’s PMIC integration into automotive SoC designs, scheduled for mass production in 2025, underscores this trend.

Regulatory compliance with RoHS and REACH shapes component specifications across supply chains. The UK, France, and Spain contribute through aerospace programs, telecom upgrades, and industrial automation. ESA’s satellite projects and the Galileo system require space-qualified capacitors with high radiation tolerance. Despite strong demand from industrial IoT and Industry 4.0, Europe faces challenges due to limited semiconductor manufacturing capacity and reliance on Asian suppliers.

Asia Pacific Silicon Capacitors Market Trends

Asia Pacific dominates the market for silicon capacitors, with 45% market share, supported by strong semiconductor manufacturing and electronics ecosystems. China, Japan, South Korea, and Taiwan account for over 70% of global electronics production, with TSMC operating the world’s most advanced foundry facilities. Japan’s automotive leaders are increasingly adopting silicon capacitors in electric and hybrid vehicles for energy storage and regenerative braking.

China’s large-scale 5G rollout, which is expected to exceed 3 million base stations by 2024, drives demand for high-frequency capacitors, while South Korean firms, led by Samsung Electro-Mechanics, invest heavily in advanced passive components. ASEAN countries such as Thailand, Vietnam, and Malaysia serve as key hubs for automotive and consumer electronics manufacturing, supported by foreign investment and integrated supply chains. India’s electronics sector, boosted by the Production Linked Incentive (PLI) scheme, offers significant growth potential despite ongoing infrastructure development.

Competitive Landscape

The global silicon capacitors market is moderately consolidated, with leading players holding about 60% share through technological innovation and integrated manufacturing. Murata Manufacturing, strengthened by its acquisition of IPDiA, leads globally with proprietary deep-trench technology. Competition focuses on enhancing capacitance density, miniaturization, and meeting stringent requirements for automotive and aerospace applications. Companies adopt vertical integration, combining semiconductor fabrication and materials expertise to develop advanced dielectric solutions. Strategic alliances, such as the ROHM-TSMC partnership, accelerate technology development and scale-up. Emerging models emphasize application-specific customization, offering co-engineering support for power management design and thermal simulation.

Key Market Developments:

- March 2025: KYOCERA AVX unveiled the world's first multilayer ceramic chip capacitor delivering industry-highest 47μF capacitance in 0402-inch size, advancing miniaturization capabilities for space-constrained applications.

- July 2024: Samsung Electro-Mechanics announced the introduction of 16V multilayer ceramic capacitors for automotive ADAS applications, achieving world-record capacitance density, coupled with 2000V-rated capacitors designed for high-voltage electric vehicle battery management systems and power conversion modules requiring extreme reliability in automotive environments.

- December 2024: ROHM Semiconductor and TSMC announced a strategic partnership for the development and volume production of gallium nitride power devices using GaN-on-silicon process technology, targeting electric vehicle onboard chargers and inverters with mass production planned.

Top Companies in the Silicon Capacitors Market

- Murata Manufacturing Co., Ltd. (Kyoto, Japan) commands market leadership through its comprehensive passive components portfolio and acquisition of IPDiA, which brought proprietary deep-trench silicon capacitor technology. The company's vertically integrated operations span materials development, semiconductor fabrication, and advanced packaging, enabling rapid innovation cycles. Murata's silicon capacitors serve critical applications in 5G infrastructure, automotive ADAS systems, and aerospace electronics, with products qualified to stringent reliability standards including AEC-Q200 and space-grade specifications.

- KYOCERA AVX (Fountain Inn, U.S.) distinguishes itself through continuous advancement of multilayer capacitor technologies and extensive application engineering support. The company's recent achievement of 47μF in 0402 package size demonstrates industry-leading miniaturization capabilities. KYOCERA AVX maintains strong positions in automotive, industrial, and telecommunications markets, with broad product portfolios spanning tantalum, ceramic, and film capacitor technologies. The company's global manufacturing footprint and technical support infrastructure provide competitive advantages in serving multinational customers.

- Vishay Intertechnology (Malvern, U.S.) leverages its diversified discrete semiconductor and passive component portfolio to address power electronics applications. The company's strategic expansion into SiC MOSFET technology complements its capacitor offerings for EV charging infrastructure and renewable energy systems. Vishay's comprehensive product range includes high-voltage aluminum capacitors, power film capacitors, and specialized tantalum technologies, providing integrated solutions for demanding power management applications. The company emphasizes reliability and automotive qualification, serving tier-one suppliers and OEMs globally.

Companies Covered in Silicon Capacitors Market

- Murata Manufacturing Co., Ltd.

- MACOM Technology Solutions

- Skyworks Solutions Inc.

- KYOCERA AVX

- Vishay Intertechnology

- Empower Semiconductor

- Microchip Technology

- ROHM Semiconductor

- TSMC

- KEMET

- Samsung Electro-Mechanics

Frequently Asked Questions

The global silicon capacitors market is valued at US$ 2.6 billion in 2026 and is projected to reach US$ 4.5 billion by 2033, expanding at a CAGR of 8.2% during the forecast period.

The silicon capacitors market is primarily driven by accelerating electric vehicle adoption and ADAS system deployments requiring high-reliability capacitors, alongside expanding 5G network infrastructure necessitating components with superior high-frequency performance and miniaturization capabilities.

Deep-Trench technology dominates with approximately 42% market share, attributed to its exceptional capacitance density achieved through three-dimensional trench structures etched into silicon substrates and compatibility with standard CMOS fabrication processes.

Asia Pacific leads the silicon capacitors market with over 45% share, driven by concentrated electronics manufacturing in China, Japan, South Korea, and Taiwan, alongside aggressive 5G deployment exceeding 3 million base stations and rapidly scaling electric vehicle production.

Significant opportunities exist in aerospace and defense applications, with the European Space Agency's ARTES programme funding space-qualified components and Airbus expanding procurement for orbital applications requiring extreme reliability, radiation tolerance, and temperature stability.

Leading market participants include Murata Manufacturing Co., Ltd., KYOCERA AVX, Vishay Intertechnology, ROHM Semiconductor, TSMC, Samsung Electro-Mechanics, Skyworks Solutions, MACOM Technology Solutions, and Microchip Technology, among others.