- Non-food Packaging

- Silicone Release Liners Market

Silicone Release Liners Market Size, Share, and Growth Forecast, 2026 - 2033

Silicone Release Liners Market by Liner Type (Paper, Film, Others), Coating Type (Single-Side Coated, Double-Side Coated, Others), Application, and Regional Analysis for 2026 - 2033

Silicone Release Liners Market Size and Trends Analysis

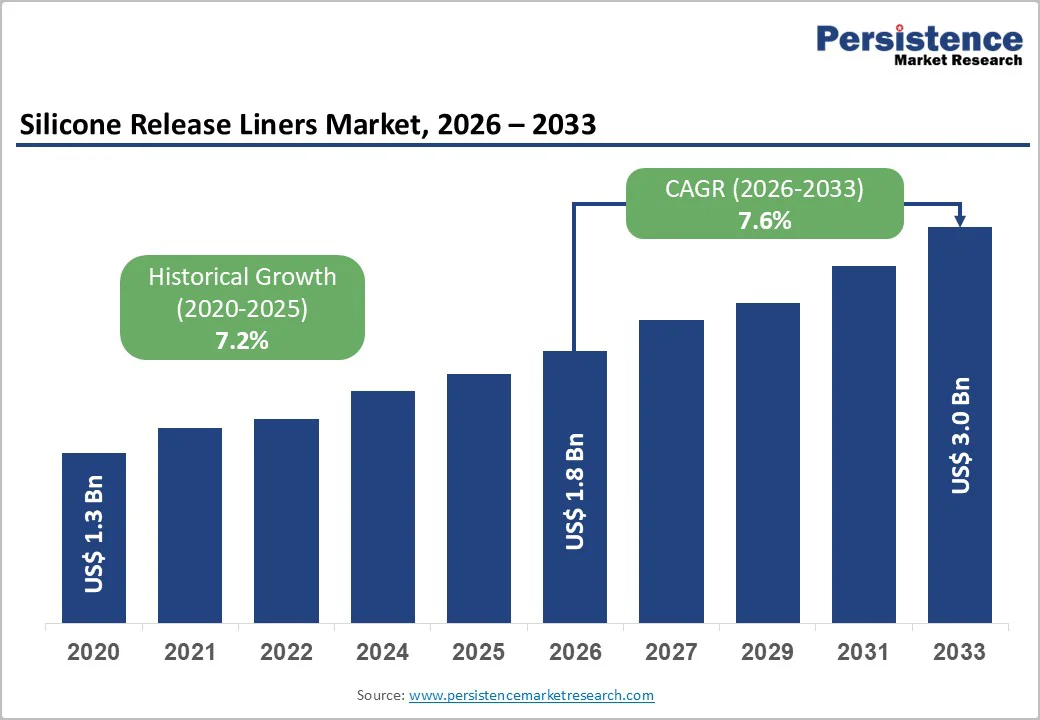

The global silicone release liners market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$3.0 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033, driven by accelerating adoption across electronics, hygiene, and medical applications, where premium silicone liners deliver consistent release performance and regulatory compliance.

Key growth enablers include the substitution of conventional liners with silicone-coated substrates for high-performance pressure-sensitive adhesives, rising volumes of labels and tapes linked to packaging and healthcare demand, and ongoing technical upgrades such as double-sided, premium, and controlled-release coatings.

Key Industry Highlights

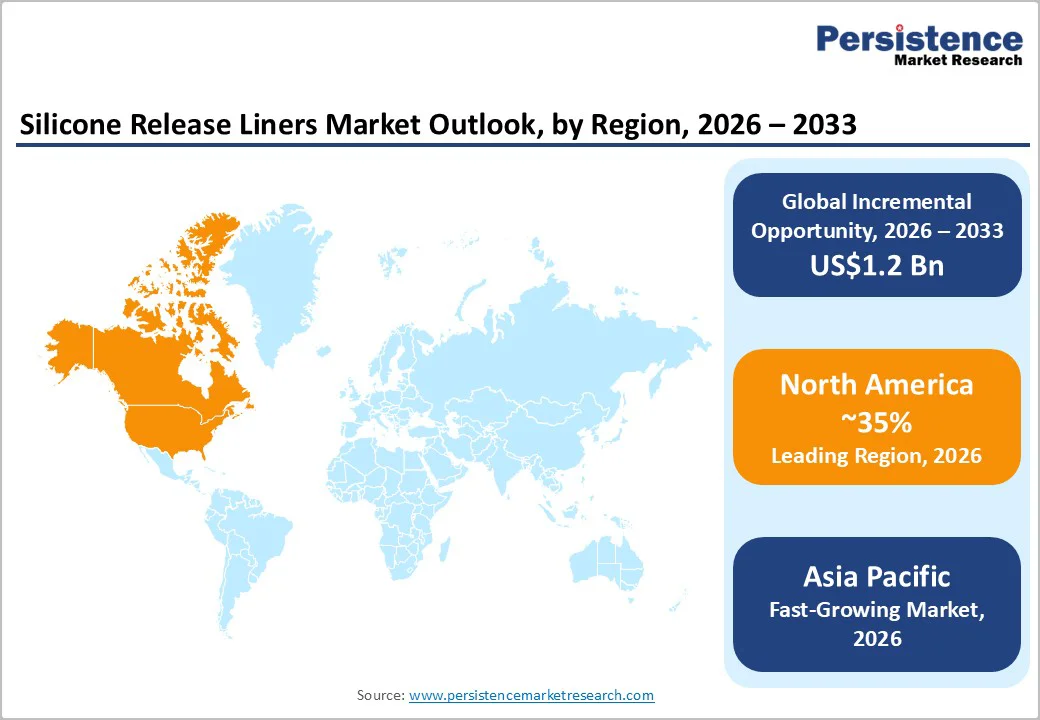

- Leading Region: North America is projected to account for approximately 35% of global market share, supported by a mature converting ecosystem, strong medical device manufacturing, and high demand for premium, validated release liner solutions across labels, tapes, and healthcare applications.

- Fastest-growing Region: Asia Pacific, projected to register the highest growth rate during the forecast period, driven by the rapid expansion of electronics manufacturing, rising consumer goods output, and increasing hygiene and medical product consumption across China, India, and Southeast Asia.

- Investment Plans: Ongoing investments focus on advanced silicone coating technologies, solvent-free and UV-curable systems, liner recycling infrastructure, and localized manufacturing capacity, particularly in North America and Europe for medical-grade liners, and in the Asia Pacific for electronics and high-volume labeling applications.

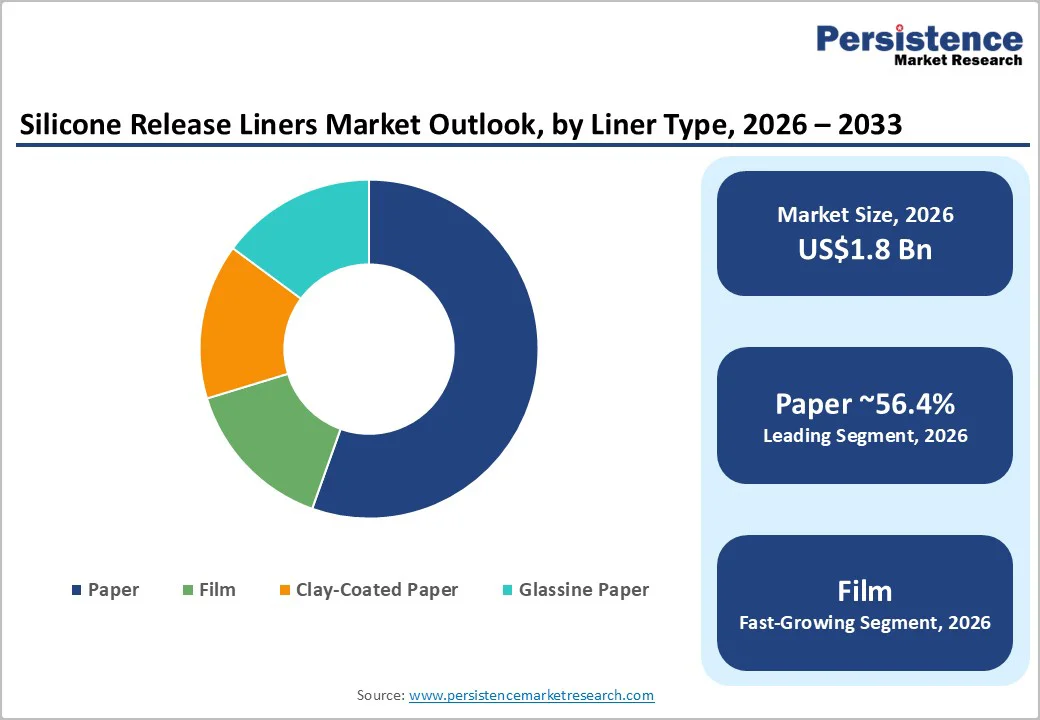

- Dominant Liner Type: Paper liners are expected to account for approximately 56.4% of the market share, driven by cost efficiency, established recyclability pathways, and widespread use in labels, hygiene products, and general-purpose tapes.

- Leading Application: Labels are estimated to represent over 38.7% of market share, supported by sustained growth in packaged goods, logistics, pharmaceuticals, and traceability-driven labeling applications.

| Key Insights | Details |

|---|---|

| Silicone Release Liners Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Demand from Pressure-Sensitive Labels and Tapes (Packaging and Logistics)

Labels and self-adhesive tapes account for the largest application cluster for silicone release liners, driven by strong demand across fast-moving consumer goods, logistics, and brand protection applications. Labels alone account for more than 38.7% of total release liner demand, reflecting their widespread use across food, beverage, pharmaceutical, and industrial packaging applications.

As packaging formats shift toward pressure-sensitive labels for shorter production runs, customization, and variable data printing, converters increasingly require liners that deliver uniform release performance across diverse substrates and high-speed converting lines.

This trend is reinforcing demand for higher-grade silicone-coated liners. The broader release liner industry is projected to grow at a mid-single-digit rate, positioning silicone-based liners as a higher-growth subsegment due to their superior functional performance.

Growth in Medical and Hygiene Products Requiring Stringent Performance Standards

Medical and hygiene applications such as sterile labels, diagnostic test strips, wound-care products, medical tapes, and sanitary goods require liners with controlled release, chemical inertness, and traceability. Silicone release liners meet these requirements by preserving adhesive integrity during sterilization and extending shelf life.

Medical applications are among the fastest-growing segments within the market, supported by rising healthcare expenditure, increased diagnostic testing, growth in wearable medical devices, and expanding use of single-use healthcare products.

Advances in cleanroom coating processes and low-extractable silicone formulations have further enabled adoption in regulated environments, creating a premium segment characterized by higher average selling prices and stronger margins.

Rising Adoption of Film-Based and Specialty Liners for Electronics and Advanced Applications

Although paper-based liners remain dominant, film liners made from materials such as polyethylene terephthalate and polyolefins are gaining traction in applications requiring dimensional stability, moisture resistance, and ultra-smooth release surfaces. Electronics assembly, display manufacturing, and specialty tape production increasingly rely on filmic liners to support automated processes and tight tolerance requirements.

Film liners typically command higher prices and exhibit faster growth rates than paper-based alternatives. This structural shift is contributing to upward pressure on average selling prices and encouraging manufacturers to invest in advanced coating technologies capable of delivering precise and repeatable release properties.

Barrier Analysis - Raw Material Price Volatility and Energy-Intensive Manufacturing

Silicone fluids, specialty additives, and substrate materials such as paper pulp and polymer films are exposed to commodity price volatility. These fluctuations directly affect production costs for silicone release liners, particularly when converters face limitations in passing costs downstream due to competitive pricing pressure from label and tape manufacturers.

The coating and curing processes used in liner manufacturing are energy-intensive, making operating costs sensitive to regional electricity and fuel prices. In recent cycles, raw material price volatility has led to 6-12% increases in unit operating costs, prompting manufacturers to rely on long-term supply contracts and to optimize portfolios toward higher-value products.

Regulatory Pressure Related To Recycling and Sustainability

Increasing regulatory focus on packaging waste reduction and recyclability presents challenges for silicone-coated liners, particularly multi-material constructions and silicone-on-film systems that are not easily recyclable. Extended producer responsibility frameworks and packaging waste regulations may increase compliance costs and restrict the use of certain liner formats in markets with limited recycling infrastructure.

In regions where collection and recycling systems are underdeveloped, converters may face 1-3% additional compliance-related costs. These pressures necessitate ongoing investments in recyclable coatings, liner separation technologies, and sustainable material innovations.

Opportunity Analysis - Development of Recyclable and Bio-Based Liner Systems

Sustainable liner solutions represent a significant growth opportunity. Paper-based liners continue to dominate the market, accounting for approximately 56.4% of total demand, creating a large installed base suitable for sustainability-driven upgrades.

Transitioning even 10-15% of conventional paper liner demand toward certified recyclable or bio-based silicone systems could unlock an incremental US$100-200 million market opportunity over the next five to seven years. Innovations in waterborne and solvent-free silicone coatings, along with compatibility with existing paper recycling streams, enable manufacturers to meet brand owner sustainability targets while capturing premium pricing.

Expansion of Specialty Coatings for Medical And Electronics Applications

Specialty release coatings tailored for medical diagnostics, wearable electronics, and advanced display manufacturing offer strong margin expansion potential. As device miniaturization and precision assembly requirements intensify, demand for liners with tightly controlled release profiles continues to rise.

Suppliers capable of delivering validated, low-extractable formulations can access regulated procurement channels where qualification cycles are long, but price sensitivity is lower. This segment is expected to grow at a 7-9% CAGR, reinforcing its role as a key driver of value creation within the broader market.

Category-wise Analysis

Liner Type Insights

Paper liners are anticipated to remain the dominant segment, holding a revenue share of 56.4% in 2026, due to their cost-effectiveness, established recyclability pathways, and compatibility with a broad range of pressure-sensitive adhesives and converting processes. Their widespread use across primary and secondary labels, hygiene backings, and general-purpose industrial tapes supports consistently high-volume demand.

Specialty paper variants, such as glassine liners used in premium food and pharmaceutical labels and clay-coated kraft liners used in logistics and shipping labels, provide enhanced surface smoothness, silicone anchorage, and dimensional stability.

These attributes allow paper liners to remain competitive even as alternative substrates gain traction. Leading producers continue to invest in lighter-basis-weight papers, improved silicone holdout, and higher recycled-fiber content, reinforcing paper’s leadership while aligning with circular-economy and brand-owner sustainability goals.

Film liners are likely to be the fastest-growing liner type, driven by rising demand from electronics manufacturing, high-speed label converting, and moisture-sensitive applications. Materials such as polyethylene terephthalate (PET) and polyolefin films offer superior dimensional stability, tear resistance, and moisture barriers, enabling thinner liner constructions and compatibility with automated dispensing and precision die-cutting systems.

These liners are increasingly used in electronic component labeling, battery assembly tapes, optical films, and specialty industrial tapes where consistency and cleanliness are critical. Growth is strongest in Asia-Pacific electronics manufacturing hubs, particularly in display panels, semiconductor packaging, and consumer electronics assembly.

Film liner adoption is expected to outpace the market average, supported by higher-value applications and tighter performance requirements.

Application Insights

Labels are estimated to constitute the largest application segment, accounting for more than 38.7% of revenue share in 2026. Strong consumption of packaged food and beverages, pharmaceuticals, personal care products, and e-commerce shipments continues to drive volume growth. The expansion of variable data printing, track-and-trace labeling, and brand authentication labels further supports demand for high-quality silicone liners.

Silicone-coated liners enable clean release, stable adhesive transfer, and consistent performance at high converting speeds, making them essential for pressure-sensitive label production. Common applications include food packaging labels, pharmaceutical compliance labels, logistics barcodes, and retail branding labels, reinforcing the segment’s structural dominance.

Medical applications are the fastest-growing end-use segment, supported by aging populations, increasing diagnostic testing volumes, and the expanding use of wearable, disposable, and minimally invasive medical devices. Silicone release liners are critical in products such as wound dressings, transdermal drug delivery patches, diagnostic test strips, surgical tapes, and electrode pads, where precise release force and material inertness are required.

These liners help preserve adhesive performance during sterilization and extend the shelf life. High qualification and validation requirements create substantial barriers to entry, favoring established suppliers with proven regulatory compliance. As a result, medical applications offer higher margins, longer contract cycles, and stable demand growth compared to conventional industrial uses.

Regional Insights

North America Silicone Release Liners Market Trends - Healthcare-Driven Premium Liners and Regulatory-Led Margin Expansion

North America is anticipated to lead, accounting for approximately 35% of global silicone release liner demand in 2026, supported by a mature converting ecosystem, high per-capita consumption of labels and pressure-sensitive tapes, and a strong medical device manufacturing base. The United States dominates regional demand, driven by healthcare, packaged goods, logistics, labeling, and specialty tape applications.

Companies such as 3M, Avery Dennison, and Berry Global maintain large-scale coating and converting operations in the U.S., reinforcing regional self-sufficiency. Recent investments by Avery Dennison in medical-grade label materials and liner optimization reflect rising demand for validated release liners used in pharmaceuticals and diagnostics.

Growth momentum is further supported by increased automation in label converting and selective reshoring of electronics and medical component assembly, particularly in the Midwest and Southeast U.S. Regulatory oversight from the FDA and EPA raises qualification and compliance thresholds, increasing switching costs for end users and favoring established suppliers with strong quality systems.

This environment supports demand for premium, double-sided coated and controlled-release liners, positioning North America as the most attractive region globally for margin expansion and value-added liner solutions.

Europe Silicone Release Liners Market Trends - Sustainability-Led Paper Liners and Circular Economy Compliance

Europe represents a significant and structurally mature market, shaped by regulatory harmonization, advanced converting capabilities, and strong sustainability mandates.

Germany, the United Kingdom, France, and Spain remain the leading markets, supported by resilient packaging, pharmaceutical, and industrial manufacturing sectors. Major regional players such as UPM Raflatac, Loparex, and Ahlstrom have expanded investments in recyclable paper liners, glassine alternatives, and low-silicone or silicone-free liner concepts, responding to brand-owner pressure and EU policy direction.

The implementation of the EU Packaging and Packaging Waste Regulation (PPWR) and broader circular economy initiatives has accelerated demand for paper-based liners, mono-material systems, and solvent-free silicone coatings.

For example, UPM Raflatac’s liner recycling collaborations with label converters across Europe have increased recovery rates and reinforced the viability of paper liners. Investment trends increasingly favor energy-efficient coating lines and water-based or UV-curable silicone technologies, positioning sustainability-focused suppliers to maintain competitiveness while meeting stringent environmental compliance requirements across the region.

Asia Pacific Silicone Release Liners Market Trends - Electronics Manufacturing Scale and High-Growth Converting Expansion

Asia Pacific is likely to be the fastest-growing regional market for silicone release liners, driven by the expansion of electronics manufacturing, rising consumer goods output, and growing hygiene and medical consumption.

China leads in overall volume, supported by its dominant electronics assembly, battery manufacturing, and high-volume labeling industries. Local and international suppliers, including Lintec, Nitto Denko, and Toray, supply advanced film liners used in display panels, semiconductor packaging, and high-precision industrial tapes, reinforcing China’s role as a demand center for performance-oriented liners.

Japan remains a technology leader, particularly in premium film liners and advanced silicone coating formulations, supporting export-driven applications in electronics and automotive components.

Meanwhile, India and Southeast Asia (Vietnam, Thailand, and Indonesia) are emerging as high-growth markets due to expanding FMCG production, pharmaceutical manufacturing, and the penetration of hygiene products.

Investments by global label and tape manufacturers in localized converting capacity have increased demand for cost-efficient paper liners and higher-value film liners, positioning Asia Pacific as both a volume-driven and an innovation-enabled growth engine for the global silicone release liners market.

Competitive Landscape

The global silicone release liners market is moderately concentrated, comprising global chemical suppliers, specialty paper manufacturers, and coating specialists alongside regional converters. Leading players capture a significant share of high-value segments, while numerous smaller companies serve local and commodity markets. Competitive positioning is shaped by coating technology, regulatory compliance, and proximity to key converting hubs.

Recent strategic activity has focused on capacity expansion, sustainability initiatives, leadership restructuring, and investment in advanced coating technologies. Companies are prioritizing recyclable liner solutions, medical-grade formulations, and regional expansion, particularly in Asia-Pacific.

Key strategies include product differentiation through controlled-release technologies, sustainability-led innovation, and geographic expansion. Technical service capabilities and long-term supply agreements remain critical competitive differentiators.

Key Industry Developments

- In April 2025, Elkem ASA’s Silicones division introduced two new products in its SILCOLEASE® range for release liners, emphasizing circular-economy features and a higher recycled-silicone content to support sustainability goals for labelstock and tape converters.

- In May 2025, Ahlstrom completed the acquisition of Stevens Point in the U.S., expanding its finishing and coating capabilities and creating a dedicated Performance Materials cluster that includes release liners, improving service breadth in North America.

Companies Covered in Silicone Release Liners Market

- Loparex LLC

- Mondi Group

- Avery Dennison Corporation

- 3M Company

- UPM Raflatac

- LINTEC Corporation

- Sappi Limited

- Gascogne Laminates

- Rayven, Inc.

- Saint-Gobain Performance Plastics

- Mitsubishi Chemical Corporation

- Polyplex Corporation Ltd.

- Siliconature S.p.A.

- Fujiko Co., Ltd.

- Uline

- Ritrama S.p.A.

- Dow Inc.

- Felix Schoeller Group

- Infiana Group

- Glatfelter

Frequently Asked Questions

The global silicone release liners market is estimated to be valued at US$1.8 billion in 2026.

By 2033, the silicone release liners market is projected to reach US$3.0 billion.

Key trends include growing adoption of premium and controlled-release silicone coatings, increasing use of film-based liners in electronics and high-speed converting, rising demand for medical-grade and hygiene applications, and continued focus on recyclable and solvent-free liner solutions to meet sustainability requirements.

Paper liners represent the leading liner type, accounting for approximately 56.4% of global market share, driven by cost efficiency, established recycling infrastructure, and widespread use in labeling and hygiene applications.

The silicone release liners market is expected to grow at a CAGR of 7.6% between 2026 and 2033.

Major players with strong portfolios include Avery Dennison Corporation, 3M Company, Ahlstrom-Munksjö, Loparex (Mativ), and LINTEC Corporation.