- Technology

- Security Analytics Market

Security Analytics Market Size, Share, and Growth Forecast 2026 - 2033

Security Analytics Market by Solution (Security Analytics Software and Services), by Applications (Network Security Analytics, Endpoint Security Analytics, Application Security Analytics, Cloud Security Analytics and Others), and End- user (BFSI, IT & Telecom, Government & Défense, Retail, Healthcare, Education and Others) and Regional Analysis for 2026 - 2033

Security Analytics Market Size and Trend Analysis

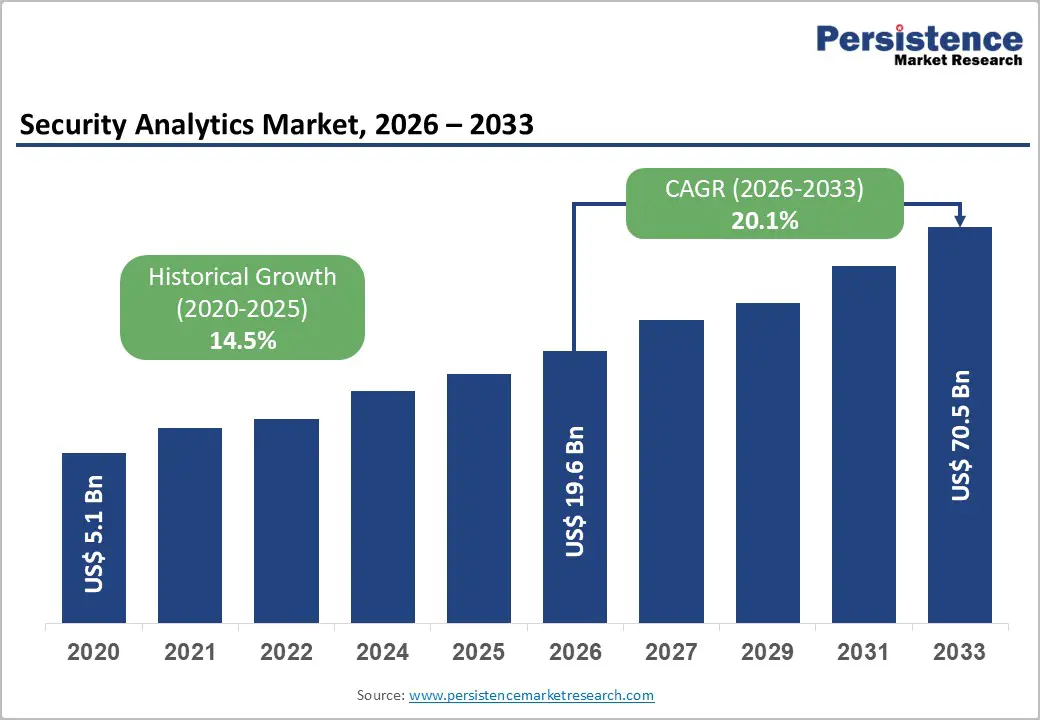

The global Security Analytics Market size was valued at US$ 19.6 Bn in 2026 and is projected to reach US$ 70.5 Bn by 2033, growing at a CAGR of 20.1% between 2026 and 2033.

Market growth is fundamentally driven by the escalating sophistication of cyber threats, regulatory compliance mandates including GDPR, HIPAA, PCI-DSS, and CCPA, combined with critical demand for real-time threat detection and automated incident response capabilities. Organizations are rapidly transitioning to AI-powered security analytics platforms, zero-trust architecture implementations, and SIEM/SOAR-integrated ecosystems to reduce mean time to detection.

Key Market Highlights

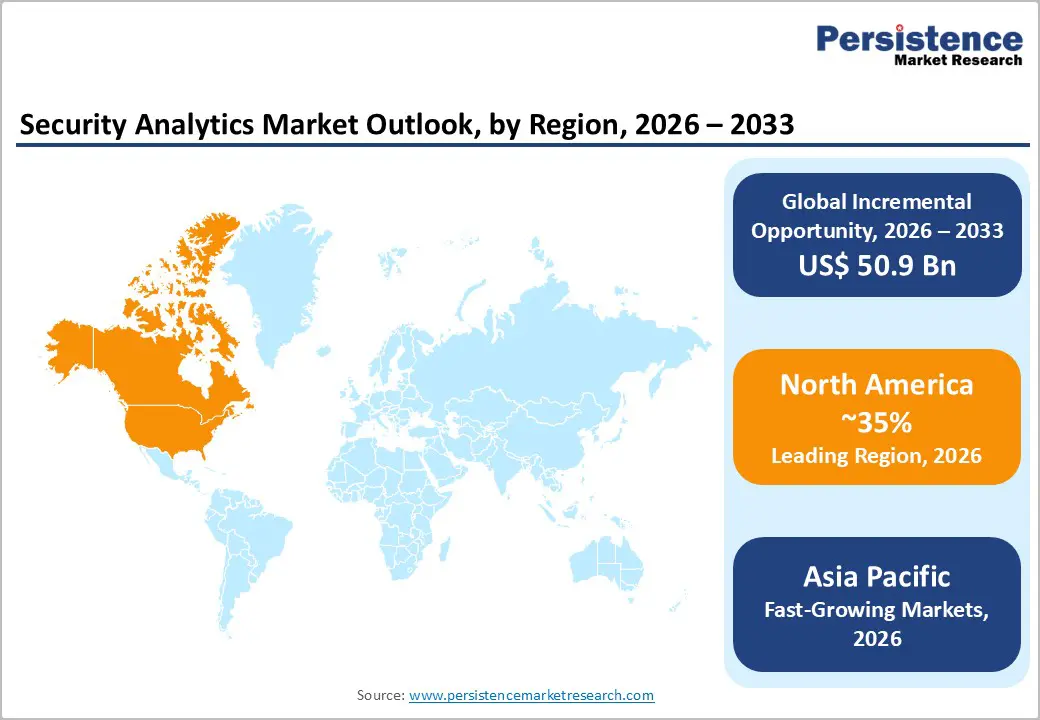

- Leading region: North America dominates the Security Analytics Market with approximately 35% global revenue share, driven by early adoption of advanced technologies, concentration of leading vendors, stringent regulatory requirements including HIPAA, CCPA, and PCI-DSS, and substantial enterprise investments in threat detection and response infrastructure.

- Fastest growing region: Asia Pacific is the fastest-growing regional market, expanding at 24% CAGR, fueled by rapid digital transformation across China and India, increasing government cybersecurity mandates, cloud infrastructure expansion, and rising cyber threat awareness among enterprises and government organizations.

- Dominant segment: Security Analytics Software, particularly SIEM, UEBA, and NDR solutions, dominates with approximately 67% of market revenue, anchored by foundational importance in comprehensive threat detection, regulatory compliance, and continuous security monitoring across enterprise infrastructure.

- Fastest growing segment: Cloud security analytics is the fastest-growing application segment, achieving 22% CAGR, driven by 94% multi-cloud adoption, emerging CSPM platforms, cloud-native SIEM solutions, and increasing demand for unified visibility across diverse cloud environments from major cloud providers.

- Key market opportunity: Extended Detection and Response (XDR) integration with SOAR platforms and managed security services expansion offers substantial growth opportunities as organizations seek comprehensive incident response automation, continuous threat hunting, and outsourced SOC capabilities, reducing operational complexity and skill requirements.

| Key Insights | Details |

|---|---|

|

Security Analytics Market Size (2026E) |

US$ 19.6 Bn |

|

Market Value Forecast (2033F) |

US$ 70.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

20.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

14.5% |

Market Dynamics

Market Growth Drivers

Proliferation of Advanced, AI-Powered Threat Detection and Automated Response Capabilities

Organizations are increasingly deploying machine learning and artificial intelligence-driven security analytics platforms to detect anomalies, predict threats, and automate responses at scale. Research indicates that AI-integrated security analytics solutions reduce false positives by over 60% and improve anomaly detection accuracy by more than 30%, directly enhancing security operations centre (SOC) efficiency. Advanced technologies, including User and Entity Behaviour Analytics (UEBA), network traffic analysis (NTA), and extended detection and response (XDR) platforms, are enabling organizations to identify sophisticated attacks, including advanced persistent threats (APTs), zero-day exploits, and insider threats that would evade traditional signature-based defenses. The average organization adopting comprehensive AI-powered security analytics platforms reports reducing mean time to detect from 207 days to approximately 48 days, while simultaneously cutting mean time to respond and substantially improving incident containment effectiveness across its entire infrastructure footprint.

Zero Trust Architecture Adoption and Regulatory Compliance Mandates

The global shift toward zero trust architecture, driven by regulatory requirements, cloud infrastructure complexity, and sophisticated attack methodologies, is compelling organizations across all verticals to invest heavily in continuous monitoring, behavioural analytics, and identity verification platforms. NIST SP 800-207 framework and industry standards are codifying zero trust principles of "never trust, always verify" and "continuous monitoring," requiring organizations to implement security analytics as core infrastructure. Regulatory pressures from GDPR in Europe, CCPA in California, HIPAA in healthcare, PCI-DSS in payments, and emerging state-level data privacy laws across North America are mandating comprehensive log aggregation, threat detection, and audit trails that SIEM and security analytics platforms uniquely provide. Over 70% of enterprises plan to adopt zero trust architecture by 2026, with 74% already integrating SIEM with Security Orchestration, Automation and Response (SOAR) platforms, directly fuelling the expansion of the Security Analytics Market as organizations prioritize this critical capability.

Market Restraints

Extreme Complexity of Integration and Data Normalization Challenges

Despite strong adoption drivers, security analytics deployment remains constrained by significant technical and organizational barriers, including the complexity of integrating diverse security tools, legacy systems, cloud platforms, and endpoint solutions into cohesive architectures. Organizations struggle with security data normalization, where vast volumes of heterogeneous telemetry streams from firewalls, intrusion detection systems, endpoint detection and response (EDR) agents, cloud access security brokers (CASBs), and third-party integrations must be translated into standardized formats for effective correlation and analysis. The scarcity of experienced security data engineers and SOC analysts further constrains deployment velocity and effectiveness, as specialized expertise is required for platform configuration, threat model development, and ongoing optimization.

High Total Cost of Ownership and Skill Gap Constraints

Security analytics platforms demand substantial capital and operational expenditure, including software licensing, hardware infrastructure, professional services for implementation and integration, and ongoing training for security teams. Organizations report that the total cost of ownership often exceeds initial budgets due to unforeseen integration complexities, extended deployment timelines, and requirements for specialized talent. The critical shortage of qualified security professionals, particularly data scientists and security engineers capable of designing threat models and optimizing machine learning algorithms, creates significant barriers to effective platform deployment, especially in mid-sized organizations with constrained talent budgets.

Market Opportunities

Cloud-Native Security Analytics and Multi-Cloud Visibility Solutions

As organizations increasingly adopt hybrid and multi-cloud architectures, with 94% of enterprises now operating across multiple cloud providers, demand for cloud-native security analytics platforms that provide unified visibility across AWS, Azure, Google Cloud, and on-premises infrastructure is accelerating rapidly. Cloud-native security analytics solutions are growing 25% faster than traditional on-premises deployments, driven by superior scalability, native integration with cloud services, and the ability to monitor dynamic, ephemeral cloud resources and containerized workloads. The Automotive Cybersecurity Market and other verticals increasingly require advanced analytics capabilities for connected vehicle telemetry, manufacturing control systems, and critical infrastructure protection, creating specialized opportunities for vendors developing domain-specific security analytics solutions.

Extended Detection and Response, SOAR Integration, and Managed Security Services Expansion

The convergence of Extended Detection and Response (XDR), Security Orchestration, Automation and Response (SOAR), and threat intelligence platforms is creating comprehensive incident response ecosystems that dramatically improve defensive capabilities and reduce security team workload. XDR platforms that correlate endpoint, network, cloud, and application data are emerging as premium offerings commanding substantial revenue growth, as they provide investigators with a unified context for faster, more accurate threat hunting and incident analysis. Managed Security Analytics Services (MSaaS) are experiencing explosive growth as mid-sized and smaller organizations increasingly outsource threat detection and response to specialized providers, avoiding the need to build and operate expensive in-house SOC infrastructure.

Category wise Insights

Solution Analysis

Security analytics software dominates the security analytics market, accounting for an estimated 67% of total revenue, driven by the dominant positioning of SIEM, UEBA, network detection and response (NDR), and endpoint detection and response (EDR) platforms. The software segment encompasses both cloud-based solutions, which are experiencing 25% faster adoption growth than on-premises deployments, and on-premises systems, prevalent among large enterprises with established data centre infrastructure and specific data residency requirements. Services, including professional services, consulting, integration and deployment, support and maintenance, and managed security analytics services, represent approximately 25% of market value, with the managed services component experiencing the fastest growth as organizations increasingly outsource SOC operations and threat detection to specialized providers.

Applications Analysis

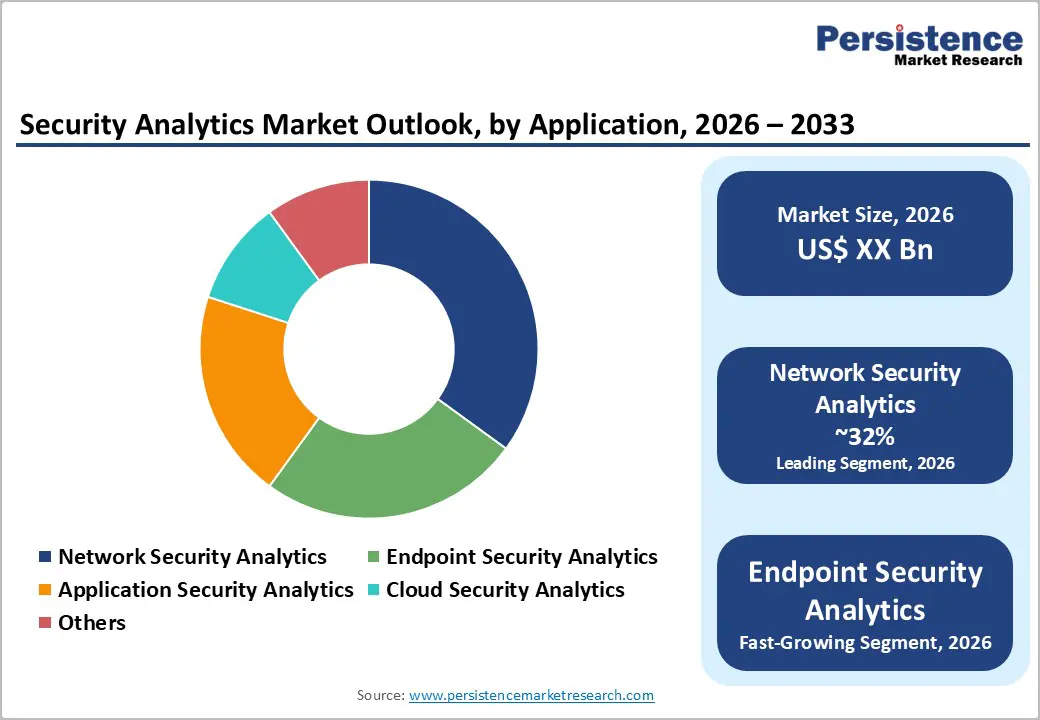

Network security analytics maintains the leading position within applications, capturing an estimated 32% of demand, as network traffic analysis, intrusion detection, and threat correlation across network infrastructure remain foundational to comprehensive security posture assessment. Endpoint Security Analytics represents the second-largest segment, at approximately 25%, driven by explosive growth in remote work, bring-your-own-device (BYOD) policies, and IoT device proliferation, creating vast endpoint diversity that requires advanced behavioural analytics and anomaly detection. Cloud Security Analytics is the fastest-growing application segment, projected to achieve 22–25% CAGR, fueled by accelerated cloud adoption, the 94% prevalence of multi-cloud environments, and emerging platforms like Cloud Security Posture Management (CSPM) and cloud-native SIEM.

End-User Analysis

The BFSI (Banking, Financial Services, and Insurance) sector dominates the Security Analytics Market, commanding an estimated 52% of enterprise adoption and revenue share, driven by stringent regulatory requirements (GLBA, PCI-DSS, SOX), handling of high-value financial assets, and persistent targeting by sophisticated cybercriminals and state-sponsored actors. Regulatory frameworks mandate continuous transaction monitoring, fraud detection, and comprehensive audit logs that security analytics platforms uniquely provide, making them effectively mandatory infrastructure in BFSI environments. IT & Telecom enterprises represent the second-largest segment at approximately 18%, pursuing security analytics for network infrastructure protection, 5G deployment security, and software-defined networking (SDN) protection.

Regional Insights

North America Security Analytics Market Trends

North America, led by the United States, dominates the global Security Analytics Market with approximately 35% of worldwide revenue, anchored by early adoption of advanced cybersecurity technologies, the concentration of major security analytics vendors (IBM, Cisco, Splunk, Broadcom, Sumo Logic), and stringent regulatory frameworks including HIPAA, GLBA, PCI-DSS, and CCPA. The U.S. security analytics market is estimated to have reached US$ 3.48 billion in 2024 and is projected to grow at a CAGR of 16.2% through 2033, driven by aggressive AI adoption, federal cybersecurity initiatives, and enterprise investments in comprehensive threat detection ecosystems.

The region's advanced technology ecosystem, venture capital support, and robust martech infrastructure create continuous innovation in AI-powered threat detection, behavioural analytics, and automated incident response capabilities. Federal initiatives, including the Cybersecurity and Infrastructure Security Agency (CISA) directives and Executive Order 14028 establishing cybersecurity mandates for federal agencies and contractors, further accelerate enterprise adoption of security analytics platforms across both public and private sectors, positioning North America as the largest market by value through the forecast period.

Europe Security Analytics Market Trends

Europe is experiencing steady market expansion underpinned by rigorous GDPR compliance requirements, accelerating digital transformation initiatives, and growing recognition of behavioural analytics for insider threat detection and for implementing zero-trust architectures. Key economies, including Germany, the U.K., France, and Spain, are prioritizing security infrastructure investment to protect critical infrastructure, financial systems, and citizen data. The region's regulatory environment, emphasizing data protection, privacy, and security governance, creates strong incentives for comprehensive security analytics adoption, particularly in BFSI, healthcare, and government sectors bound by GDPR, eIDAS, and sector-specific compliance frameworks.

The region experiencing accelerated adoption of cloud-native security analytics as enterprises modernize legacy infrastructure and implement hybrid cloud architectures compatible with EU data protection regulations. NIST Zero Trust framework adoption and European regulatory harmonization on cybersecurity labelling and data protection are expected to create standardized security analytics requirements, benefiting vendors that demonstrate compliance with evolving EU standards and frameworks, positioning the region for sustained moderate growth throughout the forecast period.

Asia Pacific Security Analytics Market Trends

Asia Pacific is the fastest-growing regional market for security analytics, projected to expand at a CAGR potentially exceeding 24% through 2033, driven by the rapid digitalization of economies across China, India, and Southeast Asia, the massive expansion of cloud infrastructure, and increasing cybersecurity investments by governments and enterprises responding to rising threat activity. China accounts for the largest share of the APAC market, driven by domestic vendors innovating rapidly in cloud security, 5G networks, and government cybersecurity mandates, while India is the fastest-growing market segment as digital transformation and government cloud initiatives accelerate adoption of security analytics platforms.

The region's manufacturing advantages in electronics and cloud infrastructure development, combined with the emergence of specialized domestic vendors addressing regional threat landscapes, regulatory frameworks, and language requirements, are enabling rapid market expansion. Government cybersecurity initiatives, increasing cross-border data flows, and rising regional cybersecurity incidents are further incentivizing enterprise investment in comprehensive security analytics solutions, positioning the Asia Pacific as a critical growth engine for the global market.

Competitive Landscape

The security analytics market is moderately consolidated, with major global leaders including IBM, Cisco Systems, Broadcom Inc., Hewlett Packard Enterprise, and specialized vendors such as Sumo Logic, SecureWorks, Securonix, Juniper Networks, FireEye, Gurucul, and Alert Logic competing across diverse segments and customer profiles.

Market leaders differentiate through breadth of product portfolios spanning SIEM, UEBA, EDR, XDR, and threat intelligence integration; depth of AI/ML capabilities for automated threat detection and response; and strategic partnerships with cloud providers, consultants, and managed service providers. Consolidation through M&A remains active, with vendors acquiring specialized capabilities in UEBA, behavioral analytics, and cloud security to enhance integrated platform offerings.

Key Market Developments

- In June 2025, Cisco Systems, Inc. unveiled comprehensive AI-ready data center and workspace initiatives, integrating advanced security analytics with scalable infrastructure to support enterprise AI adoption and accelerate digital transformation across healthcare, finance, and government sectors.

- In August 2024, Fortinet, Inc., a prominent cybersecurity company, announced that it had acquired Next DLP, a company that operates in insider risk and data protection. The strategic move is expected to strengthen Fortinet’s position in the integrated DLP and standalone enterprise data loss prevention (DLP) market.

Companies Covered in Security Analytics Market

- IBM Corporation

- Cisco Systems, Inc.

- Hewlett Packard Enterprise

- Broadcom Inc.

- Sumo Logic, Inc.

- SecureWorks Corp.

- Juniper Networks

- FireEye, Inc.

- Securonix

- Gurucul

- Alert Logic

- Other Key Players

Frequently Asked Questions

The global Security Analytics Market is projected to reach approximately US$ 70.5 billion by 2033, expanding from US$ 19.6 billion in 2026, representing a compound annual growth rate (CAGR) of 20.1% between 2026 and 2033.

Key demand drivers include escalating cyber threat sophistication, regulatory compliance mandates (GDPR, HIPAA, PCI‑DSS, CCPA), widespread adoption of AI/ML‑powered threat detection, critical need for zero trust architecture implementation, accelerated cloud and multi‑cloud adoption.

Network Security Analytics currently leads the application segment with approximately 32% market share, driven by foundational importance in network threat detection, intrusion prevention, and comprehensive infrastructure visibility.

North America, particularly the United States, dominates the global Security Analytics Market with approximately 35% of worldwide revenue, driven by early technology adoption, concentration of major vendors, stringent regulatory frameworks, and substantial enterprise investments in comprehensive threat detection and response infrastructure.

Major players include IBM Corporation, Cisco Systems, Inc., Hewlett Packard Enterprise, Broadcom Inc., Sumo Logic, Inc., and Stellar Cyber.