- Testing, Inspection, & Certification

- Electronic Security Market

Electronic Security Market Size, Share, and Growth Forecast, 2026 – 2033

Electronic Security Market by Component (Hardware, Software, Services), Security Type (Video Surveillance, Access Control, Intrusion Detection, Fire & Life Safety, Biometrics, Alarm Systems, Integrated Security Systems), End-User (Residential, Commercial & Enterprise, Industrial & Manufacturing, Government & Public Infrastructure, Transportation & Logistics, Banking & Financial Institutions, Healthcare, Education), and Regional Analysis for 2026-2033

Electronic Security Market Share and Trends Analysis

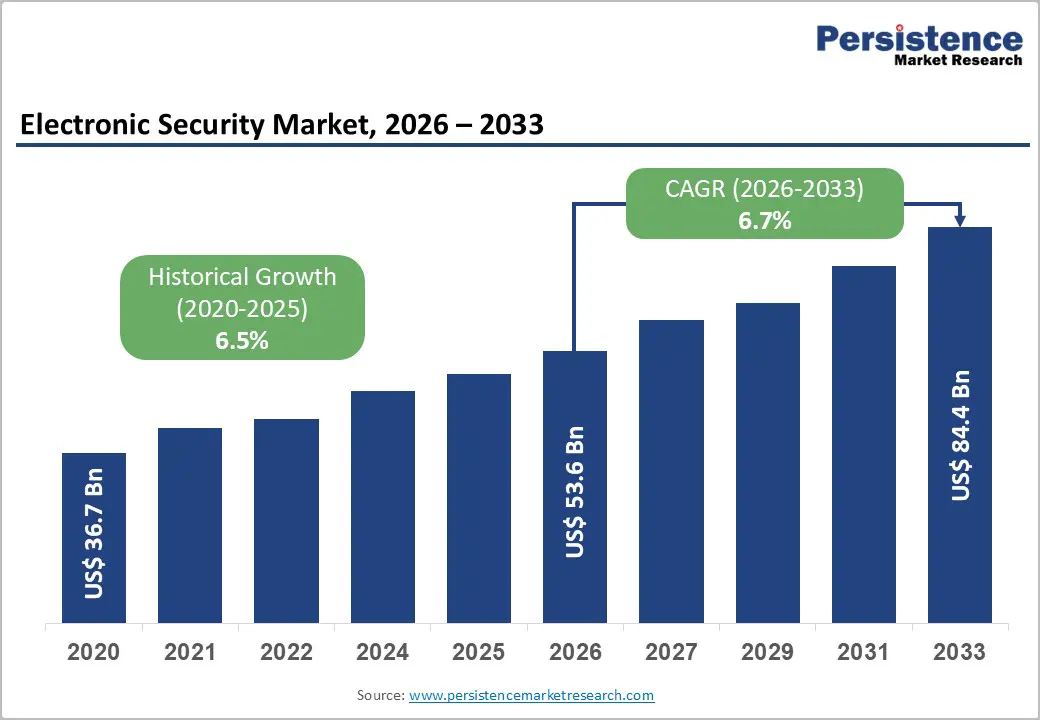

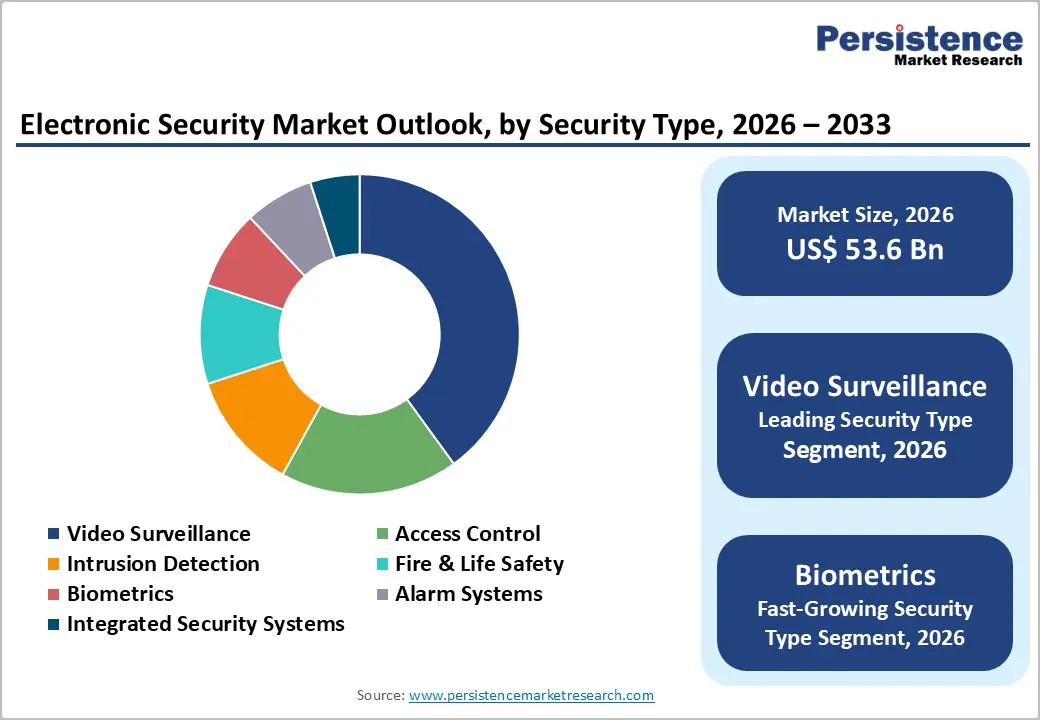

The global electronic security market size is likely to be valued at US$ 53.6 billion in 2026, and is projected to reach US$ 84.4 billion by 2033, growing at a CAGR of 6.7% during the forecast period 2026−2033. Growth is driven by increasing adoption of integrated security solutions across commercial and public infrastructure, enhancing operational reliability and threat mitigation.

Expansion of urban centers and critical infrastructure projects has intensified the need for sophisticated surveillance and access control systems, prompting investment in high-precision technologies. Technological integration, such as AI-based analytics and IoT-enabled monitoring, has enhanced real-time decision-making and improved the efficiency of security management. Regulatory frameworks mandating safety compliance and cybersecurity standards have accelerated deployment across industrial, transportation, and government sectors. Rising awareness of asset protection among commercial enterprises and residential users has contributed to the steady adoption of electronic security components and software solutions. Advancements in biometric authentication and cloud-based surveillance platforms have increased scalability and accessibility, enabling small and medium enterprises to implement robust security protocols.

Key Industry Highlights

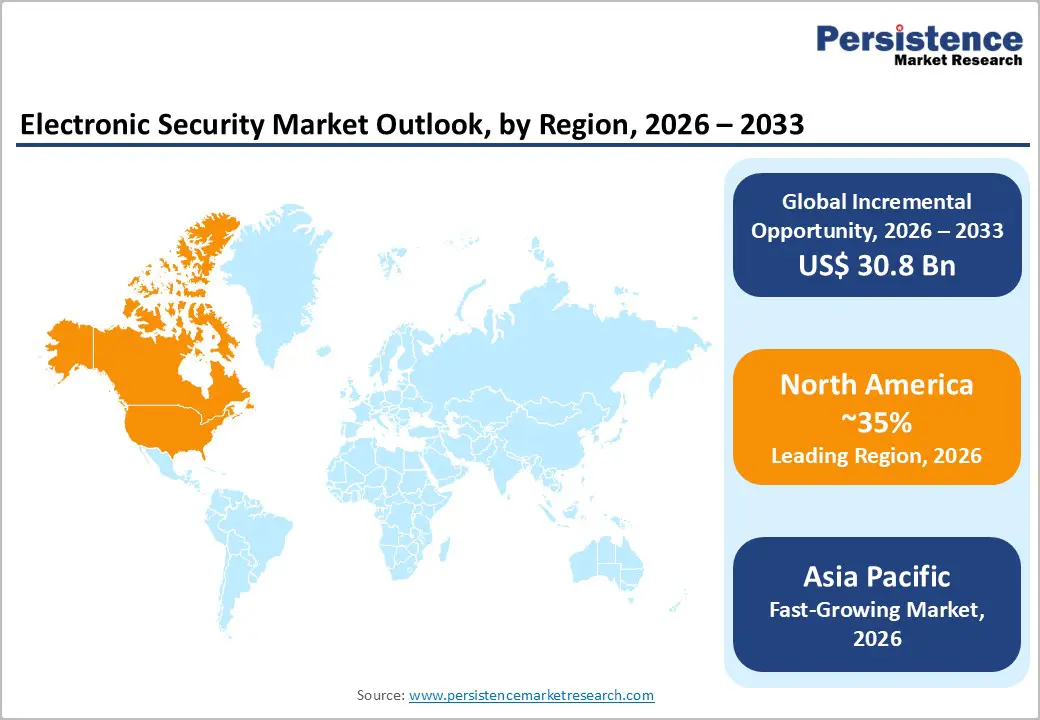

- Dominant Region: In 2026, North America is expected to hold about 35% market share, supported by massive infrastructure investments and strong federal security initiatives in the United States.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, driven by smart city programs, large-scale surveillance adoption in China, and infrastructure upgrades in India.

- Leading Security Type: Video surveillance is expected to dominate with over 40% share in 2026, enabled by increasing adoption of high-resolution cameras and AI-enabled analytics.

- Fastest-growing Security Type: Biometrics is projected to be the fastest-growing segment during 2026–2033, on account of rising demand for contactless identification and advances in recognition technologies.

- December 2025: Lumina surpassed 50,000 deployments of AI-enabled video surveillance cameras, reinforcing its market leadership in intelligent security solutions.

| Key Insights | Details |

|---|---|

| Electronic Security Market Size (2026E) | US$ 53.6 Bn |

| Market Value Forecast (2033F) | US$ 84.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancement and Digital Transformation

Rapid innovation in sensor technologies, cloud computing, and artificial intelligence has significantly transformed security solutions, enabling real-time threat detection, predictive analytics, and remote monitoring. Integration of Internet of Things (IoT) devices allows seamless connectivity across surveillance cameras, access points, and alarm systems, creating cohesive security networks with minimal latency. Advanced biometric authentication methods, including facial recognition and fingerprint scanning, have strengthened access management, reducing the risk of unauthorized entry. Digital transformation initiatives in enterprise and infrastructure environments have accelerated the adoption of software-defined security, providing scalable, customizable, and cost-efficient solutions that align with organizational growth strategies.

Cloud-based management platforms have streamlined data collection, storage, and analysis, enabling centralized oversight across multiple sites. Enhanced cybersecurity protocols integrated with electronic security systems mitigate risks from digital threats, safeguarding critical assets and sensitive information. Automation in monitoring and alert systems reduces dependence on human intervention and improves response times during security incidents. Emerging trends such as video analytics, machine learning, and mobile-enabled management are driving higher operational efficiency and situational awareness. Organizations are increasingly leveraging these digital tools to ensure regulatory compliance, improve operational transparency, and optimize resource allocation.

Privacy Concerns and Regulatory Hurdles

Electronic security solutions often rely on extensive data collection, including video surveillance, access logs, and biometric identifiers. The aggregation of sensitive information creates potential vulnerabilities, exposing organizations to breaches, identity theft, and misuse of personal data. Rising public awareness of digital privacy has amplified scrutiny on how data is stored, processed, and shared. Stringent regulatory frameworks, such as the General Data Protection Regulation (GDPR) in Europe, impose stringent compliance requirements and impose significant penalties for violations, which can increase operational costs and delay the deployment of security systems. Research by PwC indicates that 85% of organizations experienced challenges in aligning security infrastructure with evolving data protection regulations, highlighting the practical difficulties in maintaining both security efficiency and legal compliance.

The integration of advanced technologies, such as cloud-based monitoring and IoT-enabled devices, introduces additional regulatory and technical complexities. Organizations must ensure secure data transmission, encryption standards, and access controls while satisfying regional and international legal mandates. Noncompliance can lead to reputational damage, financial penalties, and operational interruptions, limiting adoption rates in risk-averse sectors. These constraints drive decision-makers to adopt conservative investment strategies, slowing the expansion of sophisticated electronic security deployments in sensitive environments. Companies often prioritize regulatory alignment over technological upgrades, which can hinder innovation and limit system capabilities in sectors requiring rapid security scalability.

Integration of AI and IoT Technologiesis

The convergence of artificial intelligence (AI) IoT technologies is transforming electronic security by enabling real-time intelligence and predictive capabilities. Smart sensors, cameras, and access points connected via IoT networks generate vast volumes of data that AI algorithms can analyze in real time to detect anomalies, unauthorized access, or potential threats. This capability allows organizations to shift from reactive measures to proactive risk management, reducing response times and improving operational efficiency. AI-driven analytics optimize surveillance coverage and resource allocation, ensuring critical areas receive continuous monitoring while minimizing false alarms. The ability to process and interpret data from multiple devices simultaneously enhances situational awareness across facilities of all scales.

The synergy between AI and IoT also drives scalability and adaptability in security operations. Cloud-based AI platforms connected to IoT devices support centralized control and remote monitoring, enabling rapid deployment of new security protocols across multiple locations. Machine learning models improve over time, refining threat detection and adapting to evolving patterns of activity. Integration with building management and operational systems allows predictive maintenance of security infrastructure, lowering downtime and operational costs. Organizations gain actionable insights from historical and real-time data, enhancing decision-making and strategic planning.

Category-wise Analysis

Component Insights

Hardware is expected to account for approximately 55% of the electronic security market revenue in 2026, reflecting its central role in physical security deployments. Hardware components such as cameras, sensors, access control devices, and intrusion detection modules constitute the foundation of all integrated security systems. Organizations prioritize high-quality hardware to ensure reliability, durability, and operational continuity. Adoption is reinforced by regulatory mandates on physical security across the industrial, transportation, and government sectors. Hardware innovation, including high-definition cameras, wireless connectivity, and energy-efficient designs, supports increased procurement across commercial and residential installations. Continuous investment in advanced hardware solutions enhances system resilience, reducing risk exposure and operational downtime.

Software is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by the integration of AI, analytics, and cloud-based management platforms. Software enables real-time monitoring, predictive analytics, and automated alerts, enhancing overall system effectiveness. Organizations increasingly rely on centralized software platforms to consolidate data from multiple hardware devices, improving decision-making and operational oversight. Scalable software solutions enable deployment in diverse environments, from small enterprises to large industrial complexes, supporting rapid adoption. Continuous updates, cybersecurity enhancements, and interoperability with IoT devices expand functionality and create recurring revenue opportunities for software providers.

Security Type Insights

Video surveillance is poised to dominate, with a forecast market share of around 40% in 2026, driven by its versatility for deterrence, evidence gathering, and operational oversight. The adoption of high-resolution cameras and intelligent video analytics enables detailed activity monitoring, supporting organizations in risk mitigation and incident investigation. Integration with AI enables automated detection of unusual behavior, reducing reliance on manual monitoring. Growing consumer confidence stems from the visible presence of cameras in public and private spaces, which reinforces perceptions of safety. Cost-effective IP-based solutions accelerate deployment across retail, transportation, and commercial facilities. Preventive adoption increases in high-risk environments, providing both strategic insights and regulatory compliance support.

Biometrics is estimated to be the fastest-growing segment from 2026 to 2033, fueled by demand for accurate, contactless identification. Continuous improvements in facial, fingerprint, and iris recognition technologies enhance processing speed and verification reliability, making these systems suitable for high-volume applications. Expansion of digital commerce and mobile transactions drives the integration of biometrics for secure authentication, supporting seamless user experiences. Enterprises and retail environments adopt biometrics to reduce friction during customer and employee access, strengthening operational efficiency. Growth in cloud-based platforms and mobile solutions enables scalable deployment, extending applications beyond physical premises into virtual and hybrid environments.

End-User Insights

Commercial & enterprise segments are likely to be the leading segments, accounting for 35% of the electronic security market share in 2026, driven by extensive requirements for asset protection, employee safety, and regulatory compliance. Large-scale office complexes, industrial sites, and corporate campuses require integrated solutions combining access control, video surveillance, and alarm systems. Digitalization enables centralized monitoring and real-time reporting, simplifying management across multiple locations. Scalable deployments allow organizations to optimize investment while expanding coverage as operational needs evolve. Technology-enabled delivery, such as AI-assisted alerts and automated response protocols, improves incident management and enhances overall workplace safety, driving adoption across sectors.

Healthcare is expected to be the fastest-growing segment from 2026 to 2033, driven by the need to protect patients, staff, and sensitive data. Hospitals, clinics, and long-term care facilities increasingly adopt solutions that comply with privacy regulations and maintain clinical credibility. Provider referrals and successful implementation in flagship facilities encourage broader adoption across networks. Remote monitoring and integrated access management improve operational efficiency and enable continuity of care in off-site or home-based care environments. Reducing security incidents and safeguarding critical assets enhance financial efficiency, support investment in advanced systems, and maintain patient trust and regulatory compliance.

Regional Insights

North America Electronic Security Market Trends

By 2026, North America is expected to lead with an estimated 35% of the electronic security share, supported by advanced technological infrastructure and substantial investments in critical infrastructure protection. The United States dominates through federal initiatives for homeland security and widespread adoption in commercial sectors, while Canada contributes via smart city developments in major urban centers. High penetration of AI-enhanced systems, integration of cybersecurity with physical security, and compliance with stringent federal regulations drive system upgrades. Deployment of integrated video surveillance, access control, and predictive analytics improves operational efficiency, threat detection, and incident mitigation across large-scale facilities and urban environments.

Competitive dynamics reinforce regional leadership, with established players leveraging strong R&D capabilities, extensive distribution networks, and strategic acquisitions. Capital flows toward innovation-focused startups, supporting the development of advanced, scalable, and AI-driven solutions. Partnerships between technology providers and system integrators enable integrated platforms that enhance monitoring, access control, and emergency response. Municipal and private-sector adoption aligns with regulatory frameworks and urban resilience goals. Investments in intelligent infrastructure, cloud-based monitoring, and automated response systems strengthen security readiness throughout commercial, industrial, and public-sector facilities.

Europe Electronic Security Market Trends

Europe holds a significant position in the market for electronic security through emphasis on data privacy and public safety across member states. Germany leads with advanced manufacturing facilities and smart factory deployments, integrating AI-enabled surveillance and access control systems. France prioritizes the protection of transportation hubs, government facilities, and urban centers with video analytics and intrusion detection solutions. Urban initiatives deploy IoT-connected devices to enable smart buildings, energy-efficient monitoring, and operational oversight. Regulatory frameworks, including the GDPR, enforce compliance while encouraging adoption of integrated security platforms. Investments in digital infrastructure and operational technology modernization drive demand for solutions that combine real-time monitoring, access management, and incident response.

Technology partnerships and targeted investments accelerate the deployment of scalable, AI-driven, and cloud-based solutions. Collaboration between local providers and global integrators enhances access to advanced platforms for commercial, industrial, and public applications. Expansion of financial hubs, healthcare networks, and logistics operations increases demand for frictionless security systems. Advanced analytics improve threat detection, predictive maintenance, and operational efficiency, reducing downtime and resource inefficiency. Public initiatives support adoption in critical infrastructure, while enterprises focus on interoperable systems integrating physical security with cybersecurity. Automated deployments in industrial and commercial facilities optimize monitoring, enhance workforce efficiency, and align with evolving operational standards.

Asia Pacific Electronic Security Market Trends

Asia-Pacific is projected to be the fastest-growing market for electronic security between 2026 and 2033, driven by rapid urbanization, government-led smart city programs, and an expanding industrial base. China drives volume through large-scale surveillance deployments in transportation hubs, commercial centers, and public spaces, while India focuses on upgrading infrastructure across commercial and industrial facilities. Japan emphasizes high-tech integrations, combining AI, IoT, and biometrics in commercial and public applications. Population density pressures, rising foreign investments in manufacturing, and initiatives promoting digital economy development create a strong demand for advanced security solutions. Enterprises increasingly prioritize scalable, technology-enabled systems across multiple sectors.

Regulatory evolution toward national security standards facilitates faster adoption across the region. Local champions collaborate with international entrants through joint ventures and partnerships, enhancing access to advanced technologies and project expertise. Capital inflows support deployment of scalable solutions, technology transfer, and R&D activities targeting industrial, healthcare, and commercial applications. Cloud-based platforms, remote monitoring, and AI-assisted surveillance systems enhance operational efficiency and risk mitigation. The expansion of smart infrastructure projects, transportation networks, and industrial complexes drives ongoing demand, while governments and private enterprises adopt standardized frameworks for compliance, safety, and operational oversight.

Competitive Landscape

The global electronic security market is moderately consolidated, with top players accounting for an estimated 45% of total revenue. Companies such as Honeywell International Inc., Johnson Controls, Bosch Sicherheitssysteme GmbH, and Axis Communications AB lead through continuous innovation, offering advanced solutions in video surveillance, access control, intrusion detection, and AI-enabled monitoring. These players maintain competitive positioning by forming technological partnerships, investing in research and development, and expanding their presence across high-demand geographies. Large-scale deployments in commercial, industrial, and critical infrastructure sectors reinforce market dominance.

Fragmentation persists among regional and niche service providers catering to cost-sensitive applications, small and medium enterprises, and localized requirements. These players differentiate through tailored offerings, flexible deployment options, and customer-centric services. Emerging technology trends such as IoT integration, cloud-based monitoring, and AI-assisted analytics present opportunities for both established and smaller companies to enhance service offerings. Strategic alliances, joint ventures, and acquisitions are common approaches to accessing new markets and broadening solution portfolios.

Key Industry Developments

- In October 2025, Sony Electronics unveiled the industry’s first video?compatible camera authenticity solution for news organizations and broadcasters to verify that footage was captured by an actual camera rather than AI?generated content, initially supporting five models with expansion plans by 2026.

- In October 2025, Keeper Security introduced an innovative biometric login solution with passkeys to enhance user authentication and replace traditional passwords. The upgrade is designed to improve security and usability for individuals and enterprises by combining biometric factors with modern cryptographic passkey technology.

- In September 2025, Amazon launched the Blink Arc Outdoor Camera 2K, a weather-resistant security camera featuring high-resolution 2K video, enhanced motion detection, and improved night vision. The device integrates with the Blink and Amazon Alexa ecosystems, offering customizable alerts and cloud storage options for home security users.

Companies Covered in Electronic Security Market

- Honeywell International Inc.

- Johnson Controls.

- Bosch Sicherheitssysteme GmbH

- Axis Communications AB.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd

- Tyco International Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

Frequently Asked Questions

The global electronic security market is projected to reach US$ 53.6 billion in 2026.

Rising security threats, increased adoption of smart infrastructure, regulatory compliance requirements, and growing integration of AI and IoT technologies are driving the market.

The market is poised to witness a CAGR of 6.7% from 2026 to 2033.

Integration of AI and IoT technologies, expansion of smart city and digital infrastructure projects, and rising demand for scalable, cloud-based security solutions are creating new market opportunities.

Some of the key market players include Honeywell International Inc., Johnson Controls, Bosch Sicherheitssysteme GmbH, and Axis Communications AB.