- Testing, Inspection, & Certification

- Integration Security Service Market

Integration Security Service Market Size, Share, and Growth Forecast, 2026 - 2033

Integration Security Service Market by Component Type (Solution, Services), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Security Type (Network Security, Cloud Security, Application Security, Data & Identity Security, OT/IoT Security, Misc.), End Use Industry (BFSI, Government & Defense, Healthcare & Life Sciences, IT & Telecom, Manufacturing & Industrial, Retail & E-Commerce, Energy & Utilities, Misc.) and Regional Analysis for 2026 - 2033

Integration Security Service Market Size and Trends Analysis

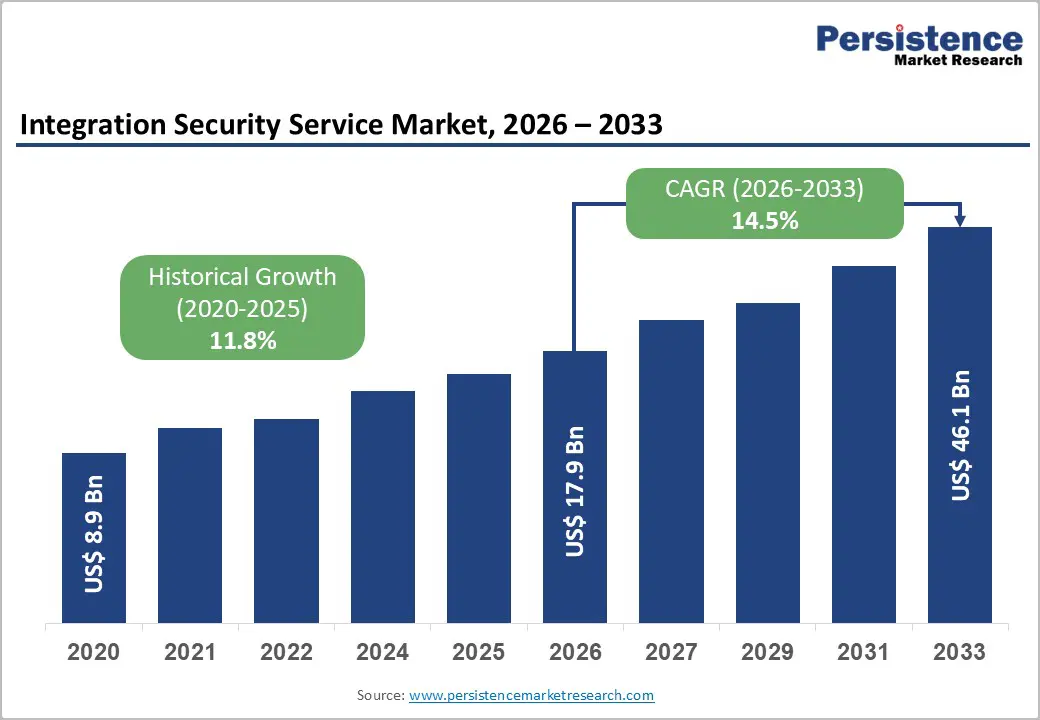

The Global Integration Security Services Market size was valued at US$ 17.9 billion in 2026 and is projected to reach US$ 46.1 billion by 2033, growing at a CAGR of 14.5% between 2026 and 2033. This substantial expansion is driven by escalating cyber threats across digital infrastructure, mandatory regulatory compliance frameworks, and the accelerated adoption of cloud computing and Internet of Things (IoT) technologies across enterprises.

The market's momentum reflects the fundamental shift from siloed security approaches to integrated, multi-layered defense strategies that unify network, application, data, and identity protection. With financial services, government agencies, and IT sectors facing sophisticated attack vectors, organizations are prioritizing comprehensive security integration services that provide unified visibility, centralized threat management, and seamless interoperability across diverse technology environments.

Key Industry Highlights:

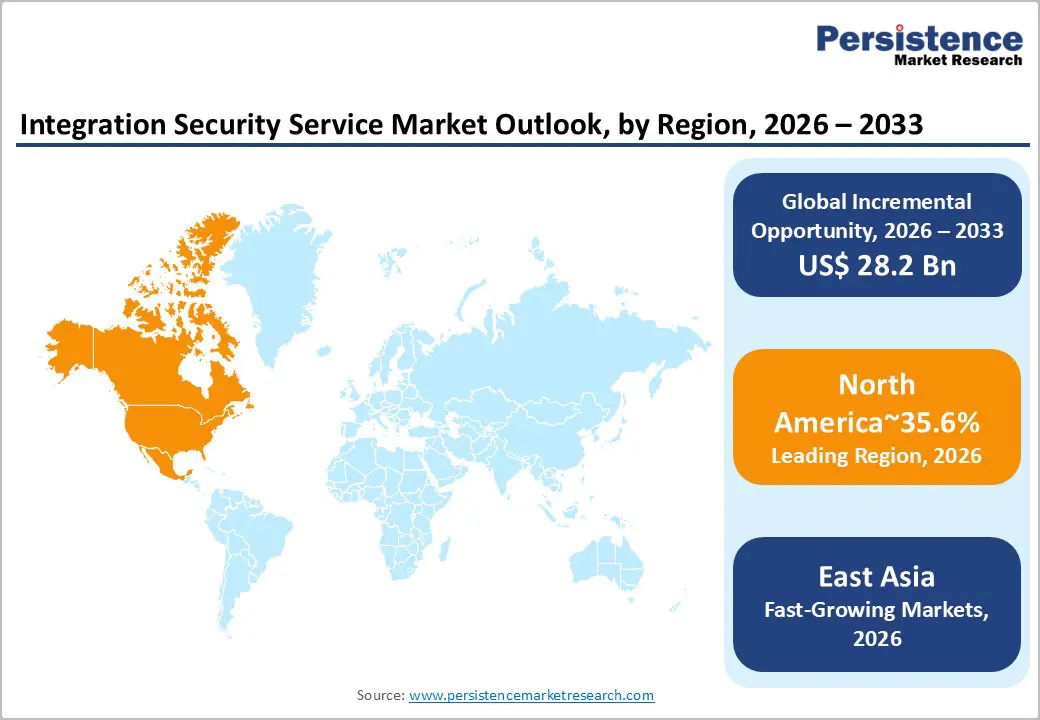

- Regional Leadership: North America leads the global Integration Security Services Market with 35.6% share, supported by advanced cybersecurity maturity, strong regulatory frameworks, and extensive enterprise IT and cloud infrastructure investments.

- Strong European Presence: Europe holds 24% share, driven by GDPR and data privacy mandates, collaborative threat intelligence initiatives, and a mature managed security services ecosystem across financial and industrial sectors.

- High-Growth East Asia Market: East Asia accounts for 20% share and remains a rapidly expanding region, powered by rapid digitalization, government-backed cybersecurity programs, industrial automation, and critical infrastructure protection in China, Japan, and South Korea.

- Leading Component Type: Services dominate with 62.6% share, enabled by consulting, integration, managed services, and ongoing operational support for complex multi-layered security architectures.

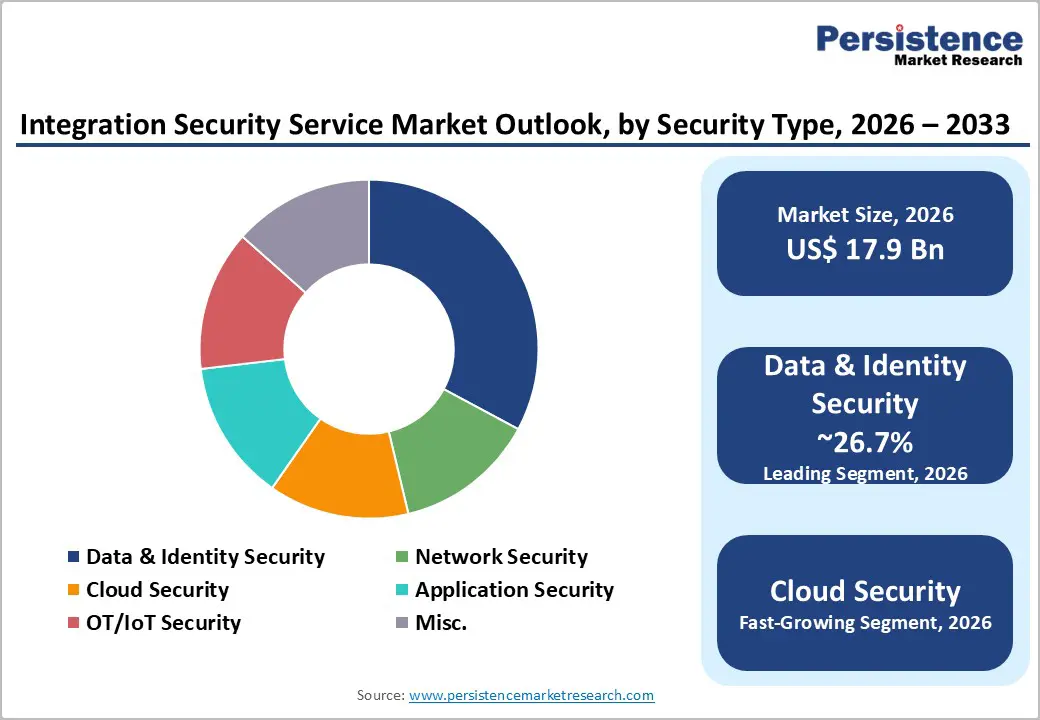

- Leading Security Type: Data & Identity Security holds 26.7% share, reflecting stringent data protection regulations, high-profile data breach risks, and critical identity management requirements across BFSI, government, and enterprise sectors.

| Key Insights | Details |

|---|---|

|

Integration Security Service Market Size (2026E) |

US$ 17.9 Bn |

|

Market Value Forecast (2033F) |

US$ 46.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.8% |

Market Dynamics

Growth Drivers

Digital Transformation and Connectivity Infrastructure Expansion

The exponential growth in internet connectivity and digital infrastructure directly propels the Integration Security Services Market as organizations confront expanding attack surfaces across increasingly complex IT ecosystems. According to ITU estimates, global internet usage has expanded rapidly, reaching around 6 billion users in 2025, up from 60 percent in 2020, with nearly 1.3 billion people coming online between 2020 and 2025, reflecting accelerated digital adoption worldwide.

India's telecom sector exemplifies this transformation, recording a subscriber base of 1.21 billion and a tele-density of 86.09 percent as of June 2025, while internet subscribers reached 979 million. Broadband adoption has accelerated sharply over the last decade, expanding from 149.75 million connections in 2016 to 979 million in 2025. Data consumption continues to surge, supported by 4G and rapidly expanding 5G networks, with 5G already contributing nearly a quarter of total wireless data usage in FY25.

This unprecedented connectivity expansion, combined with gross telecom revenue rising from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, creates massive security integration requirements as enterprises must protect distributed networks, mobile endpoints, cloud workloads, and IoT devices simultaneously, driving sustained demand within the Integration Security Services Market.

Financial Sector Digital Evolution and Asset Protection Requirements

The rapid digitalization and asset expansion across global financial services sectors necessitates sophisticated integrated security architectures to protect increasingly valuable digital assets and sensitive customer data. India's banking, financial services, and insurance (BFSI) sector expanded 50 times in market capitalization to reach US$ 1 trillion in 2025 from US$ 20.28 billion in 2005, now contributing 27 percent to the country's GDP. Life insurance AUM reached US$ 693 billion and mutual fund AUM rose to US$ 844 billion by March 2025.

In Europe, the financial and insurance activities sector generated €0.9 trillion in value added in 2022 and employed nearly 5 million people across almost 867,000 enterprises. The European banking sector held total assets of €43.6 trillion in 2023, with loans outstanding at €26.8 trillion and total deposits from businesses and households at €17.3 trillion.

China's banking and insurance sectors demonstrated robust growth, with total banking assets reaching RMB 467.3 trillion, up 7.9 percent year-on-year as of Q2 2025, and insurance assets growing 9.2 percent to RMB 39.2 trillion. This massive financial asset concentration, combined with digital transformation initiatives and online banking proliferation, creates critical security integration demands as institutions must protect customer data, transaction systems, and regulatory compliance frameworks simultaneously, substantially benefiting the Integration Security Services Market.

Market Restraining Factors

Integration Complexity and Legacy System Compatibility Challenges

Organizations face significant technical and operational barriers when implementing integrated security solutions across heterogeneous IT environments containing legacy systems, proprietary protocols, and incompatible security technologies. The financial sector particularly struggles with this challenge, as evidenced by Latin America's banking sector confronting costly, inefficient legacy systems unable to support real-time payments and requiring core modernization through incremental, API-first approaches.

The European banking sector's structural transformation, with the number of credit institutions falling to 5,304 driven by digitalization and efficiency-focused restructuring, highlights the operational complexity of security integration during technology transitions. Organizations must balance maintaining operational continuity while migrating to integrated security architectures, often requiring custom integration development, extensive testing, and phased deployment strategies that increase project timelines and total cost of ownership.

Key Market Opportunities

Aerospace and Defense Sector Security Modernization Initiatives

The substantial expansion and technological advancement within global aerospace and defense sectors creates significant opportunities for the Integration Security Services Market through critical infrastructure protection, sensitive data security, and operational technology safeguarding requirements. According to the Aerospace, Security and Defence Industries Association of Europe (ASD), the European aerospace and defence industry achieved an overall turnover of €325.7 billion in 2024, representing a 10.1 percent year-on-year increase and a 24.4 percent share of the global A&D market. Employment grew by 6.9 percent in 2024, adding over 71,000 new jobs and bringing the total workforce to nearly 1.103 million employees.

The European defence industry demonstrated robust growth with turnover reaching €183.4 billion in 2024, reflecting a 13.8 percent year-on-year increase, driven by heightened geopolitical tensions and renewed focus on strategic autonomy. Employment in the sector expanded significantly to 633,000, an 8.6 percent increase compared to 2023. Research and development investment reached €25.2 billion, a 9.4 percent rise year-on-year, with military initiatives accounting for 61 percent of R&D spending.

The U.S. aerospace and defense industry generated nearly 995 billion in total business activity in 2024, contributing $443 billion in economic value and supporting over 2.2 million workers with average wages of $115,000. India's defence budget reached US 67.4 billion in 2020-21, with defence exports growing over 700 percent between 2016-17 and 2018-19. These investments in advanced technologies, manufacturing capabilities, and digital systems require comprehensive integrated security solutions protecting classified information, supply chain networks, and operational systems, creating substantial addressable opportunities within the Integration Security Services Market.

Information and Communication Services Digital Infrastructure Expansion

The substantial growth in information and communication services infrastructure across global markets presents transformative opportunities for the Integration Security Services Market through comprehensive protection of digital services, data centers, and cloud computing environments. According to the European Commission (Eurostat), the information and communication services sector represented a major pillar of the EU business economy in 2022, comprising around 1.4 million enterprises, employing nearly 7.2 million people, and generating approximately €667 billion in value added, accounting for 6.6 percent of total EU business economy value added.

Computer programming, consultancy, and related activities dominated the sector, Ireland recorded the highest share of business economy value added from this sector at 19.3%, followed by Cyprus at 15.5 percent, while Germany emerged as the largest contributor. The sector exhibited notably high productivity levels, with apparent labour productivity reaching €92,800 per person employed, significantly above the EU business economy average. This concentration of high-value digital infrastructure, cloud services, software development, and data processing facilities requires sophisticated integrated security frameworks addressing application security, API protection, data encryption, and multi-tenant isolation, positioning the sector as a critical growth catalyst within the Integration Security Services Market.

Category-wise Analysis

Component Type Insights

Services dominate the Global Integration Security Services Market with 62.6% market share in 2026, reflecting the critical importance of professional expertise, implementation support, and managed services in delivering effective integrated security architectures. The services segment encompasses consulting, integration, deployment, training, and managed security services that address the complexity of unifying disparate security technologies, customizing solutions for specific organizational requirements, and maintaining optimal security postures over time.

The services segment's leadership position stems from the specialized expertise required to design multi-layered security frameworks, the ongoing operational support needed to manage integrated platforms, and the continuous threat monitoring essential for modern cybersecurity effectiveness. Organizations increasingly adopt managed security services models where third-party providers assume responsibility for security operations, threat detection, incident response, and compliance management, leveraging economies of scale and specialized talent unavailable to individual enterprises.

Solutions represent the fastest-growing component within the Integration Security Services Market, encompassing security platforms, integration tools, orchestration software, and unified management consoles that enable organizations to consolidate security operations and automate threat response. The accelerated adoption of solutions reflects advancing technology maturity, declining platform costs, and the strategic shift toward self-service security management capabilities supported by artificial intelligence and automation.

Security Type Insights

Data & Identity Security commands the largest share of the Global Integration Security Services Market at 26.7% in 2026, reflecting the fundamental importance of protecting sensitive information assets and verifying user identities across increasingly distributed digital environments. This segment encompasses data loss prevention, encryption, tokenization, identity and access management, privileged access management, and multi-factor authentication technologies that form the foundation of enterprise security architectures.

The segment's market leadership stems from stringent data protection regulations, high-profile data breach consequences, and the proliferation of remote work environments requiring robust identity verification. The financial services sector's massive asset concentration, with China's banking assets reaching RMB 467.3 trillion and European banking assets totaling €43.6 trillion, creates critical data protection requirements safeguarding customer information, transaction records, and financial analytics.

Cloud Security represents the fastest-growing security type within the Integration Security Services Market, driven by accelerated cloud migration initiatives, multi-cloud adoption strategies, and the transition of critical workloads to public, private, and hybrid cloud environments. Organizations require integrated cloud security solutions addressing infrastructure protection, workload security, cloud access security brokerage, and cloud-native application protection across diverse cloud platforms.

Regional Insights and Trends

North America Market Trend

North America dominates the Global Integration Security Services Market with 35.6% share, driven by advanced cybersecurity maturity, stringent regulatory frameworks, substantial technology investments, and concentrated presence of leading security vendors and sophisticated enterprise customers. The region benefits from established security operations centers, widespread adoption of zero-trust architectures, and proactive threat intelligence sharing mechanisms supporting comprehensive integrated security deployments.

The U.S. aerospace and defense industry's substantial economic footprint, generating nearly $995 billion in total business activity in 2024 and contributing $443 billion in economic value, demonstrates the scale of critical infrastructure requiring sophisticated security integration.

North America's B2B eCommerce sector continues growing substantially in absolute dollar terms despite slight share decline, reflecting ongoing digital transformation efforts, widespread adoption of eProcurement solutions, and continued dominance of advanced manufacturing, distribution, and service industries.

Canada's e-commerce market reached an estimated US$ 89.4 billion in 2024, projected to grow to around US$ 104 billion by 2029, accounting for 6.1 percent of total retail sales. The region's competitive advantages include robust enterprise IT infrastructure, high cybersecurity spending as percentage of IT budgets, mature managed security services market, and collaborative public-private partnerships addressing critical infrastructure protection, positioning North America for sustained market leadership through advanced threat detection capabilities, comprehensive compliance frameworks, and continuous security innovation investments.

East Asia Market Trend

East Asia represents 20% of the Global Integration Security Services Market, characterized by rapid digitalization, massive manufacturing base protection requirements, government-led cybersecurity initiatives, and substantial investments in 5G infrastructure, smart city projects, and industrial automation requiring comprehensive security integration. The region's growth trajectory reflects strategic emphasis on technological sovereignty, domestic security platform development, and protection of critical industrial and governmental systems.

China's banking and insurance sectors demonstrated robust growth and stability as of Q2 2025, with total banking assets reaching RMB 467.3 trillion, up 7.9 percent year-on-year, and insurance assets growing 9.2 percent to RMB 39.2 trillion.

The Asia-Pacific region's dominance in B2B eCommerce, accounting for 77.9 percent of total GMV in 2017 and increasing to an estimated 80.0% in 2026, reflects accelerating digital transformation, strong manufacturing base, and rising cross-border trade requiring integrated solutions protecting payment gateways, supply chain platforms, and trading networks. East Asia's competitive landscape features government-backed cybersecurity companies, domestic cloud security platforms, and strategic partnerships between technology vendors and critical infrastructure operators, positioning the region for accelerated market growth driven by digital economy expansion, critical infrastructure protection mandates, and technology localization initiatives through 2033.

Europe Market Trend

Europe accounts for 24% of the Global Integration Security Services Market, supported by stringent data protection regulations including GDPR, comprehensive cybersecurity directives, collaborative defense initiatives, and mature managed security services ecosystems emphasizing privacy-by-design principles and cross-border threat intelligence sharing. The region's market characteristics reflect strong regulatory enforcement, high security awareness, and established partnerships between government agencies, critical infrastructure operators, and security service providers.

The European financial and insurance activities sector generated €0.9 trillion in value added and employed nearly 5 million people across almost 867,000 enterprises in 2022, demonstrating high productivity with a wage-adjusted labor productivity ratio of 236.1 percent. The European banking sector held total assets of €43.6 trillion in 2023, with loans outstanding at €26.8 trillion and deposits at €17.3 trillion, requiring sophisticated security integration protecting customer data and transaction systems.

The information and communication services sector comprised around 1.4 million enterprises, employed nearly 7.2 million people, and generated approximately €667 billion in value added. Europe's competitive advantages include harmonized regulatory frameworks facilitating cross-border security services, advanced threat intelligence sharing through ENISA and other EU agencies, strong privacy protection culture, and collaborative research initiatives advancing security technologies, positioning the region for sustained growth aligned with digital sovereignty objectives and critical infrastructure protection imperatives through 2033.

Competitive Landscape

The Global Integration Security Service Market is characterized by a moderately consolidated and competitive environment, where a handful of large, established technology and cybersecurity firms dominate alongside skilled niche providers. Leading players leverage extensive R&D resources, broad service portfolios, and global delivery capabilities to drive market share, while smaller specialists compete on depth of expertise and customized integration solutions. IBM Corporation, Cisco Systems, Inc., Symantec Corporation, Microsoft Corporation, Trend Micro, Inc., and Sophos Group plc are among the foremost providers shaping the competitive dynamics with comprehensive security integration services spanning cloud security, identity management, threat intelligence, and managed security offerings.

These incumbents benefit from deep enterprise relationships and cross platform integration competencies that reinforce their positioning in large scale digital transformation and hybrid IT environments. Consolidation trends continue as large vendors pursue strategic partnerships and acquisitions to enhance service portfolios and accelerate innovation, though opportunities remain for agile players addressing specific industry verticals or advanced threat niches.

Key Industry Developments

- On November 3, 2025, Cisco introduced multi-customer management capabilities within Cisco Security Cloud Control, enabling Managed Service Providers (MSPs) to efficiently deploy and manage Hybrid Mesh Firewall and other security services, streamline operations, reduce costs, and accelerate delivery of advanced managed security solutions.

- On June 18, 2025, IBM launched industry-first software integrating watsonx.governance and Guardium AI Security, providing enterprises with a unified solution for AI governance and security, enabling risk management, compliance validation, and automated protection of agentic AI systems at scale.

Companies Covered in Integration Security Service Market

- Symantec Corporation

- IBM Corporation

- Cisco Systems, Inc.

- Trend Micro, Inc.

- Sophos Group plc

- Optiv Security

- Microsoft Corporation

- CGI Group Inc

- DynTek Inc.

- Honeywell International Inc.

Frequently Asked Questions

The global Integration Security Service Market is projected to be valued at US$ 17.9 Bn in 2026.

The Data & Identity Security segment is expected to account for approximately 28.9% of the Global Integration Security Service Market by Security Type in 2026.

The market is expected to witness a CAGR of 14.5% from 2026 to 2033.

The Integration Security Services Market growth is driven by accelerated digital transformation, rapid expansion of internet and connectivity infrastructure, widespread 4G/5G adoption, and the need to secure increasingly valuable digital assets and sensitive data across BFSI, enterprise, and cloud environments.

The key market opportunities in the Integration Security Services Market lie in Aerospace & Defense modernization and protection of critical infrastructure, along with the expansion of digital and cloud-based services in the Information & Communication sector requiring advanced integrated security solutions.

The key market players in the Integration Security Service Market are Symantec Corporation, IBM Corporation, Cisco Systems, Inc., Trend Micro, Inc., Sophos Group plc, and Optiv Security.