- Transportation & Logistics

- Air Cargo Security Screening Systems Market

Air Cargo Security Screening Systems Market Size, Share, and Growth Forecast for 2025 - 2032

Air Cargo Security Screening Systems Market by Size of Screening Systems (Small Cargo, Break and Pallet Cargo and Oversized Cargo), by Technology (X-Ray, Explosive Detection System (EDS) and Explosive Trace Detection (ETD)), Application (Narcotics Detection, Metal & Contraband Detection and Explosives Detection) and Others and Regional Analysis for 2025 - 2033

Air Cargo Security Screening Systems Market Size and Trends

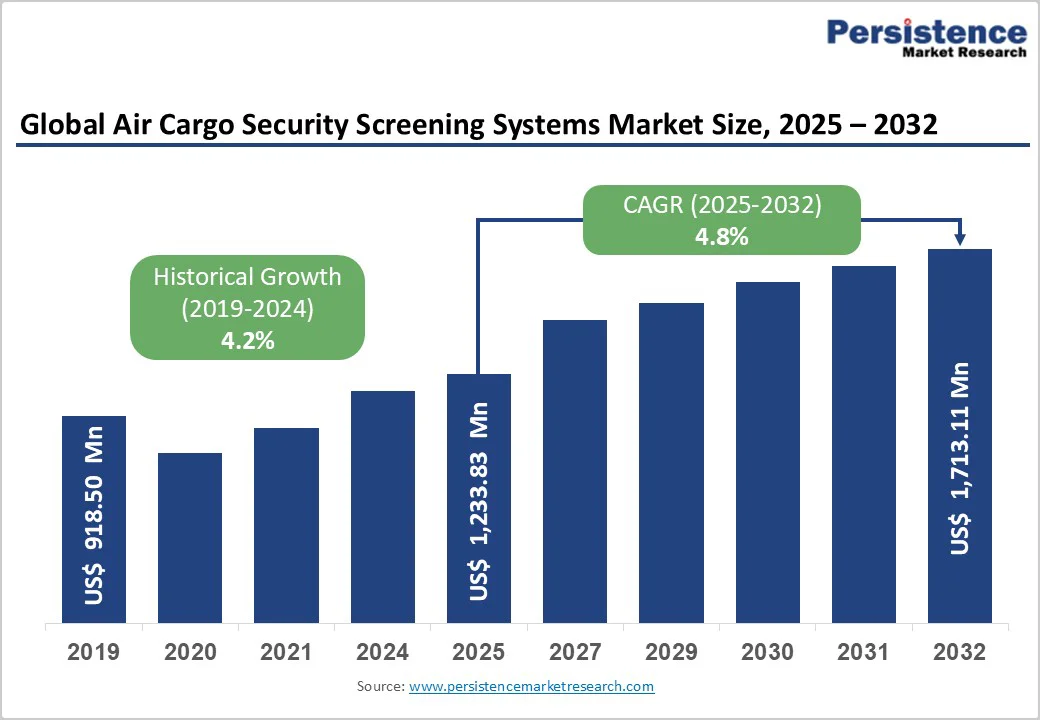

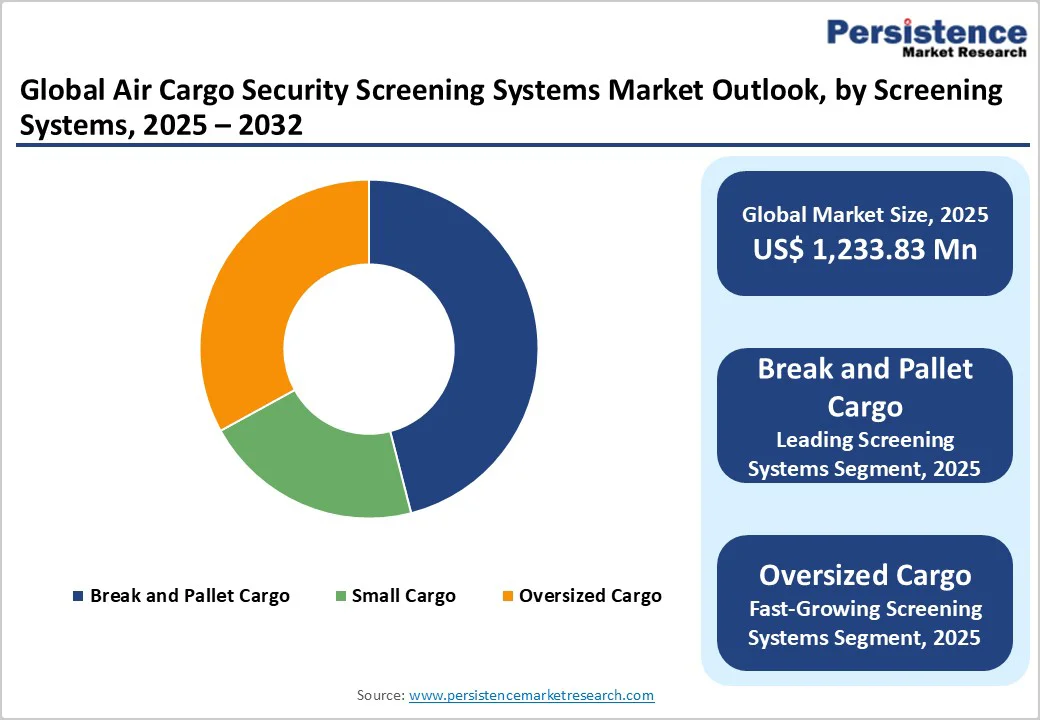

The global air cargo security screening systems market size is valued at US$1,233.83 million in 2025 and is projected to reach US$1,713.11 million, growing at a CAGR of 4.8% between 2025 and 2032.

The market's expansion is fundamentally driven by mandatory full-scale cargo screening requirements established by agencies including the Transportation Security Administration (TSA) and European Civil Aviation Conference (ECAC), combined with technological advancement in automated threat detection systems.

Key Highlights of the Air Cargo Security Screening Systems Market

- Technology Segment Leadership: Explosive Detection Systems dominate the market with 43.2% share, supported by their proven reliability in identifying high-risk materials. X-ray and ETD technologies complement this segment by enabling layered screening solutions that address diverse air cargo and logistics security requirements.

- Size Segmentation Dynamics: Break and pallet cargo screening leads with 47.9% market share (US$591 million), driven by rising international trade volumes and adoption of automated inspection systems capable of efficiently handling large, mixed cargo shipments.

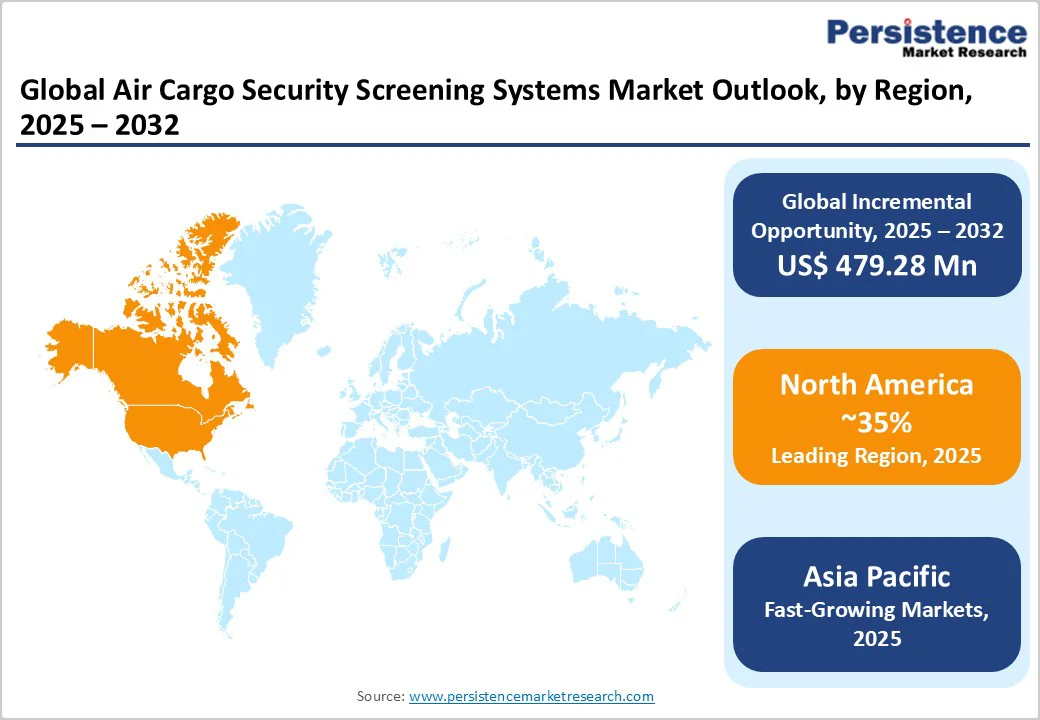

- Regional Market Structure: North America commands 35% global share, supported by strong regulatory compliance and technological leadership, while Asia-Pacific emerges as the fastest-growing region at 5.5% CAGR, fueled by expanding infrastructure investments in China and India and increasing regulatory harmonization across regional economies.

- Application Focus: Explosives detection maintains dominance with 45.7% share, while narcotics detection records the fastest growth due to heightened global drug trafficking concerns and demand for multi-threat detection capabilities.

- Strategic Technology Evolution: AI-driven threat detection, CT-based automated screening, and Screening-as-a-Service (SaaS) business models are reshaping market operations. The TSA’s US$100-120 million contract with Smiths Detection exemplifies major public investment in next-generation security infrastructure.

- Regulatory Environment: The TSA’s August 2023 Certified Cargo Screening Program enhancement and IATA’s December 2024 Air Cargo Device Assessment Program establish unified international standards, accelerating technology adoption and global market expansion.

| Key Insights | Details |

|---|---|

| Air Cargo Security Screening Systems Market Size (2025E) | US$ 1,233.83 million |

| Market Value Forecast (2032F) | US$ 1,713.11 million |

| Projected Growth (CAGR 2025 to 2032) | 4.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Drivers - Rising Popularity of Water Sports and Leisure Activities

The air cargo security screening market is experiencing substantial growth driven by unprecedented e-commerce expansion generating explosive increases in air freight volumes requiring enhanced security protocols. The International Air Transport Association (IATA) forecasts global air cargo revenue will exceed $169 billion by 2026, reflecting sustained industry growth momentum. Air freight capacity increased by 11.3% globally, with European air freight demand rising 11.2% year-over-year in 2024.

The Middle East e-commerce market hit $1,888 billion in 2024 and is projected to grow at 21.58% CAGR through 2033, creating substantial cargo screening demand in the region. The rapid expansion of cross-border e-commerce, particularly accelerated by pandemic-driven digital commerce adoption, is generating unprecedented cargo shipment volumes requiring efficient yet thorough security screening.

Stringent Regulatory Mandates and National Security Imperatives

Government agencies worldwide are implementing increasingly stringent air cargo security regulations requiring mandatory screening of all commercial freight. The Transportation Security Administration (TSA) enhanced its Certified Cargo Screening Program in August 2023, expanding participation to include more air cargo shippers in the secure supply chain while streamlining shipment speed and reducing additional screening requirements. In the United States, holding 88.20% of North American market share in 2024, the ongoing emphasis on national security drives continuous investment in full-scale air cargo screening infrastructure.

According to industry reports, 76% of terrorism-related fatalities in Western nations occurred in the United States in 2023, underscoring security imperatives driving screening technology adoption. IATA initiated the Air Cargo Device Assessment Program in December 2024 to authenticate tracking devices, data loggers, and sensors according to industry safety standards, ensuring integrity of valuable shipments.

Restraint - High Capital Investment and Installation Costs

Advanced air cargo screening systems require substantial capital investments, with CT-based explosive detection systems costing significantly more than conventional X-ray equipment, creating financial barriers for smaller freight operators and emerging market facilities. High installation costs combined with ongoing maintenance requirements create operational expenditure pressures, particularly affecting independent cargo screening facilities and regional airports with limited capital budgets.

The financial burden of acquiring, installing, and maintaining state-of-the-art screening equipment can delay technology adoption and create competitive disadvantages for operators unable to make these investments. Budget constraints at smaller airports and cargo facilities may result in continued reliance on legacy screening technologies, creating security vulnerabilities and operational inefficiencies.

Technical Complexity and Skilled Manpower Requirements

The operation and maintenance of sophisticated screening systems require specialized technical expertise and trained personnel, creating workforce challenges particularly in emerging markets. Shortage of skilled screeners capable of interpreting complex imaging outputs and operating advanced detection equipment affects operational efficiency and security effectiveness. Training requirements for personnel operating CT scanners, explosive trace detection equipment, and automated threat recognition systems create ongoing operational costs.

The lack of digital infrastructure required to support advanced screening systems in developing regions constrains market penetration. Integration challenges with existing cargo handling systems and the complexity of achieving regulatory certification for new screening configurations create technical barriers limiting market expansion.

Opportunity - Screening-as-a-Service (ScaaS) Business Models

Screening-as-a-Service models are gaining traction, enabling logistics firms to leverage high-end security infrastructure without heavy upfront capital investments. This service-based approach allows smaller cargo handlers and regional facilities to access advanced screening technologies through operational expense models rather than capital purchases. ScaaS ensures even smaller logistics players can access advanced screening technologies while maintaining regulatory compliance.

The model creates recurring revenue opportunities for screening equipment providers and service operators while expanding addressable market to price-sensitive segments. Strategic partnerships between technology providers and logistics firms implementing ScaaS frameworks can accelerate market penetration in emerging economies where capital constraints limit technology adoption.

Integration of Artificial Intelligence and Advanced Analytics

AI-driven imaging, real-time data analytics, and machine learning integration are revolutionizing cargo screening, significantly improving detection accuracy and operational efficiency. Integration of Big Data analytics with screening systems enables pattern recognition, predictive threat assessment, and automated decision support, reducing screening times while enhancing security outcomes. Collaborations between technology developers, logistics firms, and regulatory bodies focused on data-sharing and real-time monitoring systems can enhance security outcomes while streamlining regulatory compliance.

Companies developing AI-enabled screening solutions capable of autonomous threat detection and automated clearance for low-risk cargo create competitive differentiation and premium pricing opportunities. The convergence of screening technology with cloud computing, IoT connectivity, and advanced analytics platforms establishes new service models and recurring revenue streams beyond traditional equipment sales.

Category-wise Analysis

By Size of Screening Systems Insights

Break and pallet cargo screening systems dominate the market with a 47.9% share in 2024. Their leadership is driven by the widespread use of palletized shipments in international freight and the need for efficient, high-volume inspection. Equipped with advanced X-ray, explosive detection, and automated inspection technologies, these systems ensure compliance with stringent security standards while maintaining throughput efficiency.

Growth is further fueled by rising global trade and e-commerce expansion generating large-scale cargo movement. Meanwhile, small cargo screening is expanding rapidly due to express courier and parcel demand, supported by CT-based automated systems, while oversized cargo screening leverages mobile X-ray and trace detection technologies to address complex inspection requirements for non-standard cargo.

Technology Insights

Explosive Detection Systems (EDS) lead the market with a 43.2% share in 2025, driven by regulatory mandates enforcing automated explosive detection in air cargo screening. EDS leveraging computed tomography (CT) delivers 3D volumetric imaging for accurate, automated threat identification. Systems certified to ECAC Standard 3 and 3.1 provide high throughput and reliability for express logistics and large-scale cargo operations.

Next-generation dual-view, dual-energy X-ray with full 3D CT defines the technological frontier, enhancing processing speed without compromising precision. Meanwhile, conventional X-ray systems remain the most widely used for primary inspection, complemented by Explosive Trace Detection (ETD) devices that identify trace explosive residues, enabling efficient, layered security workflows combining automated and manual verification.

Application Insights

Explosives detection dominates the market with a 45.7% share, valued at approximately US$565 million in 2025, reflecting the aviation industry’s highest security priority-preventing in-flight detonation threats. Incidents such as the 2010 cargo bomb plot have accelerated global adoption of advanced screening systems capable of detecting both traditional and improvised explosive devices (IEDs). Regulatory bodies worldwide enforce strict compliance standards, positioning explosive detection as a non-negotiable requirement for all air cargo operations.

In contrast, narcotics detection represents the fastest-growing application segment, fueled by escalating international drug trafficking and law enforcement initiatives targeting air freight routes. Integrated multi-threat screening technologies now enable simultaneous detection of explosives, narcotics, and contraband, advancing toward comprehensive, full-spectrum cargo security solutions.

Regional Market Insights

North America Cargo Security Screening Systems Market Trends - Market Leadership and Regulatory Framework

North America leads the global air cargo security screening market with a 35% share, in 2025. The United States accounts for 88.2% of the regional market, driven by stringent TSA mandates requiring 100% screening of all cargo transported on passenger aircraft.

The region’s expansive air logistics network, including major international airports and trade hubs, demands high-performance, compliant screening systems utilizing X-ray, EDS, and ETD technologies to ensure secure and efficient cargo movement.

North America also leads in technological innovation, supported by initiatives such as the TSA-Smiths Detection US$100-120 million contract for advanced CT scanners and AI-based screening collaborations between Leidos and Rapiscan Systems. Continuous R&D investments, robust regulatory frameworks, and proactive security modernization sustain regional market leadership.

Europe Cargo Security Screening Systems Market Trends - Regulatory Harmonization and Market Development

Europe accounts for approximately 25% of the global air cargo security screening market, supported by stringent EU regulations and expanding trade volumes. Regional air freight capacity has grown 7.9% annually, with demand up 11.2%, driving sustained investment in screening infrastructure.

The European Civil Aviation Conference (ECAC) enforces standardized certification under EDS Standard 3 and 3.1, ensuring uniform detection performance and compliance across member states.

Major logistics hubs such as Frankfurt, Amsterdam, and London Heathrow anchor regional screening operations, supported by leading manufacturers like Smiths Detection with strong local presence. Europe’s growing focus on sustainability and operational efficiency influences procurement toward energy-efficient, integrated screening systems that combine cargo security, tracking, and supply chain visibility for optimized logistics performance.

Asia Pacific - Rapid Market Expansion and Regional Leadership

Asia Pacific represents the fastest-growing region in the global air cargo security screening market, holding a 35.0% share in 2024 and projected to record the highest CAGR of 5.5% through 2034. Rapid economic expansion, rising international trade, and increasing air cargo volumes are driving strong demand for advanced security solutions.

Key economies China, India, and Japan are strengthening aviation security infrastructure to address terrorism, smuggling, and contraband risks.

Governments across the region are enforcing stringent regulatory standards aligned with global aviation security frameworks, fueling adoption of next-generation screening technologies. Robust infrastructure investments, manufacturing modernization, and foreign direct investment (FDI) in security systems are creating localized supply chains and accelerating regional responsiveness, positioning Asia-Pacific as the primary engine of global market growth.

Competitive Landscape

Manufacturers of Air Cargo Security Screening Systems are taking several initiatives to expand their businesses. They strategically focus on innovative and technologically advanced products that meet end consumer needs. This includes developing new technologies in Air Cargo Security Screening Systems for watersports and recreational activities.

The market structure supports both volume-oriented strategies targeting mainstream recreational users and premium differentiation approaches focusing on performance enthusiasts and luxury segments. Regional specialists and emerging electric PWC manufacturers create fragmented competition in niche segments, particularly for specialized applications and sustainable alternatives.

Key Industry Developments

- In July 2025, Taiga Motors Inc., a Canadian manufacturer of electric powersports vehicles, announced a strategic partnership with Aqua superPower, the world’s leading marine fast-charging network provider. The collaboration aims to accelerate the electrification of marine transportation by combining Taiga’s innovative electric watercraft with Aqua superPower’s expanding global charging infrastructure.

- In April 2025, Yamaha Motor Co., Ltd. announced that its subsidiary, Yamaha Motor Australia Pty Ltd., had signed a purchase agreement with subsidiaries of BRP Inc., Canada, to acquire 100% of the shares of Telwater Pty Ltd., an Australian aluminum boat manufacturer. The completion of the acquisition remains subject to the necessary regulatory approvals, including competition law clearances and related permits.

Companies Covered in Air Cargo Security Screening Systems Market

- L-3 Communications Security & detection system

- Nuctech Company

- Gilardoni S.P.A.

- Costruzioni Elettroniche Industriali Automatismi S.p.A.

- Smiths Detection

- Rapiscan System

- Implant Sciences Corporation

- Safran Identity and Security SAS

- American Science and Engineering, Inc.

- Others Key Players

Frequently Asked Questions

The air cargo security screening systems market is set to reach US$ 1,233.83 Mn in 2025.

Growing consumer interest in marine leisure activities such as jet skiing, wakeboarding, and water racing is driving strong demand for Air Cargo Security Screening Systems globally.

The air cargo security screening systems industry is estimated to rise at a CAGR of 6.2% through 2032.

The growing global emphasis on sustainability and emission reduction presents a major opportunity for electric and hybrid-powered PWCs. Advancements in battery density, charging infrastructure, and lightweight materials are enabling manufacturers to introduce eco-friendly models.

Nuctech Company, Gilardoni S.P.A., Smiths Detection and Rapiscan Systemare a few leading players.