- Marine

- Maritime Security Market

Maritime Security Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Maritime Security Market by Type (Products, Services), Security Type (Port Security, Vessel Protection, Coastal Surveillance, Maritime Surveillance, Others), End-User (Shipping Companies, Government, Port Authorities, Others), and Regional Analysis for 2025 - 2032

Maritime Security Market Size and Forecast

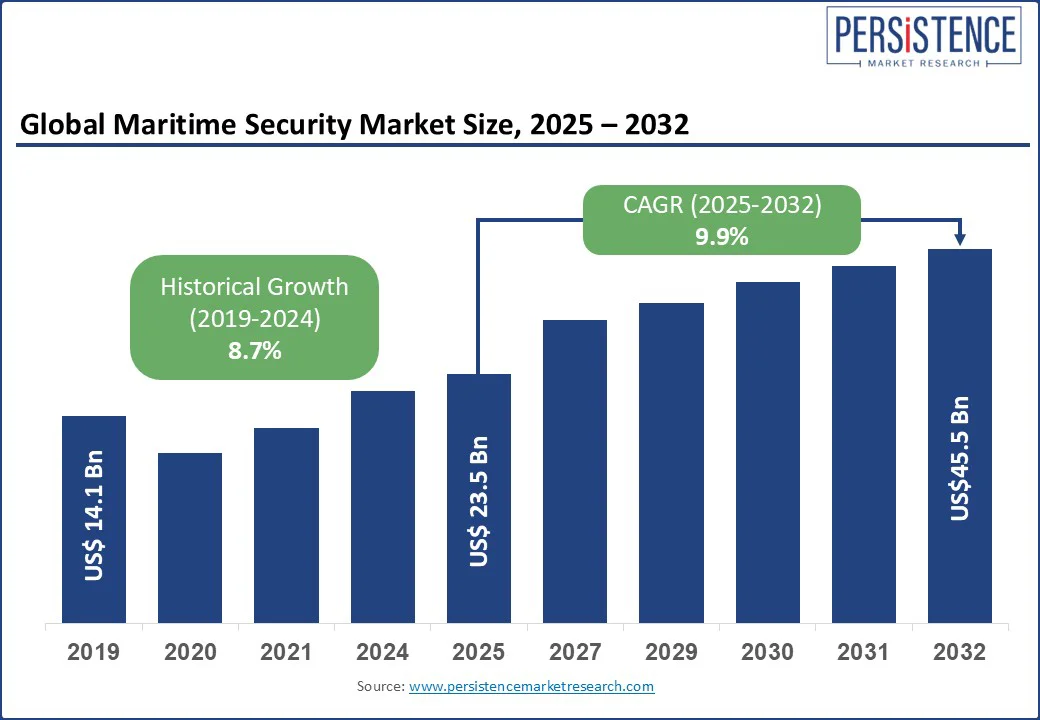

The global Maritime Security Market is set for robust growth, valued at US$ 23.5 billion in 2025 and projected to reach US$ 45.5 billion by 2032, with a compound annual growth rate (CAGR) of 9.9% during the forecast period. This market is critical to ensuring the safety and security of global maritime trade, which accounts for over 80% of international commerce by volume, according to the United Nations Conference on Trade and Development (UNCTAD).

The Maritime Security Market is facing rising threats of piracy, terrorism, smuggling, and cyber-attacks, coupled with increasing global trade and regulatory mandates for maritime safety, which are driving demand for advanced security solutions. The industry is characterized by technological advancements in surveillance systems, cybersecurity measures, and integrated security platforms, with key players investing heavily in innovation to address evolving threats and comply with international regulations such as the International Ship and Port Facility Security (ISPS) Code.

Market Dynamics

Drivers

- Rising Maritime Threats: The increasing prevalence of piracy, terrorism, and illegal trafficking is a primary driver of the maritime security market. According to the International Maritime Bureau (IMB), 115 piracy and armed robbery incidents were reported globally in 2023, with Southeast Asia and the Gulf of Guinea being high-risk areas. These threats necessitate advanced security solutions, including surveillance systems, drones, and counter-piracy technologies, to protect vessels and ports. For instance, the Nigerian Navy has expanded its maritime patrols and deployed armed escort services to secure the Gulf of Guinea. Similarly, Singapore invested in AI-based port surveillance to strengthen maritime threat detection.

- Growth in Global Maritime Trade: The expansion of global trade, particularly through maritime routes, drives demand for robust security measures. UNCTAD reports that global maritime trade volumes grew, with containerized trade expected to increase annually through 2030. This growth amplifies the need for enhanced port security, vessel protection, and surveillance systems to mitigate risks associated with high-traffic maritime routes, particularly in strategic chokepoints such as the Strait of Malacca and the Suez Canal. For instance, Malaysia and Indonesia have increased joint naval patrols in the Strait of Malacca, while Egypt has deployed advanced radar and monitoring systems to secure the Suez Canal.

- Regulatory Mandates and Technological Advancements: Stringent international regulations, such as the ISPS Code, mandate enhanced security measures for ports and vessels. Additionally, advancements in technologies such as artificial intelligence (AI), unmanned aerial vehicles (UAVs), and satellite-based surveillance are transforming maritime security. For instance, AI-powered analytics can detect suspicious activities in real-time with up to 90% accuracy, according to industry studies, driving the adoption of integrated security platforms by governments and port authorities.

Restraints

- High Implementation Costs: The development and deployment of advanced maritime security systems, such as radar systems, drones, and cybersecurity platforms, involve significant costs, often exceeding those for large-scale projects. These high costs can deter smaller ports and shipping companies, particularly in developing regions, from adopting cutting-edge solutions, limiting market growth in cost-sensitive markets.

- Complex Regulatory Compliance: The maritime security market faces challenges due to varying international and regional regulations. Compliance with standards such as the ISPS Code and regional frameworks requires significant investment in infrastructure and training, which can be a barrier for smaller operators. Additionally, interoperability issues between different security systems can hinder seamless implementation, slowing market expansion.

Opportunities

- Advancements in Cybersecurity Solutions: The rising threat of cyber-attacks on maritime infrastructure, such as port management systems and vessel navigation, presents significant opportunities. The maritime industry reported a 400% increase in cyber incidents from 2019 to 2023, according to the International Maritime Organization (IMO). This has spurred demand for cybersecurity solutions, including AI-driven threat detection and blockchain-based secure communication systems, fostering innovation and market growth.

- Expansion in Emerging Markets: The growing maritime trade in emerging economies, particularly in the Asia Pacific and Africa, offers substantial opportunities. For instance, India’s Sagarmala Project aims to modernize 12 major ports, with investments exceeding, driving demand for advanced security systems. Similarly, Africa’s increasing role in global trade is boosting investments in coastal and port security, creating a lucrative market for security providers.

Market Insights

By Type

Products, including radar, sonar, and advanced surveillance systems for port security, due to their widespread deployed in ports and on vessels.

Services, including maintenance, training, and consulting, are the fastest-growing segment, driven by the need for ongoing support and system upgrades for maritime defense.

By Security Type

Maritime surveillance holds the largest market share at 35.6% in 2024, driven by the widespread adoption of radar, satellite, and drone-based systems for real-time threat detection.

Automatic Identification System (AIS) is used by 80% of major shipping nations for real-time vessel tracking. Maritime cybersecurity is the fastest-growing segment, fueled by rising cyber threats to maritime infrastructure

By End-User

Government agencies hold the largest share at 45% in 2025, due to their role in securing coastlines and enforcing maritime security regulations. The U.S. Navy and Coast Guard alone invested in naval security systems in 2024.

Port authorities are the fastest-growing end-user segment, driven by increasing port modernization and port security upgrades in response to rising global trade security demands.

Regional Insights

North America Maritime Security Market Trends

North America holds a dominant 35% share of the global maritime security market in 2025,

- United States- The U.S. dominates due to strong defense funding, advanced surveillance infrastructure, and AI-powered maritime drones. In 2023, 10,000 tons of illicit cargo were intercepted along vulnerable coastlines.

- Canada- Canada enhances Arctic and Atlantic security through satellite surveillance, RADARSAT systems, and NATO collaborations. Investments focus on radar upgrades and joint defense efforts under NORAD to monitor maritime threats.

- Mexico- Mexico prioritizes port and coastal security in Veracruz and Manzanillo. It combats smuggling via naval patrols, automated vessel monitoring systems, and enhanced inspections at key Pacific and Gulf ports.

Europe Maritime Security Market Trends

- United Kingdom: The UK leads the European market, driven by its strategic maritime position and investments in port security and cybersecurity. The adoption of AI-based surveillance and unmanned systems is increasing, supported by government initiatives to enhance maritime safety.

- Germany: Germany’s robust shipping industry and focus on green port initiatives drive demand for advanced security solutions, particularly in maritime surveillance and vessel protection.

- France: France’s naval modernization and focus on securing Mediterranean trade routes are boosting investments in integrated security systems, including drones and radar technologies.

Asia Pacific Maritime Security Market Trends

Asia Pacific holds a 28% share of the global maritime security market in 2025,

- China: China dominates the Asia Pacific market with a significant share in 2024, driven by its massive maritime trade (over 4 billion tons annually) and investments in the Belt and Road Initiative. The adoption of advanced surveillance and cybersecurity systems is rising to protect strategic maritime routes.

- India: India’s growing maritime trade and the Sagarmala Project drive demand for port and coastal security solutions, with investments in radar and drone-based systems increasing.

- Japan & Other APAC Countries: Japan’s advanced maritime R&D and focus on securing trade routes, along with rising investments in Southeast Asia, support growth in maritime surveillance and vessel protection systems.

Competitive Landscape

The maritime security market is highly competitive, driven by technological innovation, strategic defense contracts, and regional risk mitigation. General Dynamics leads in the U.S. with autonomous surveillance drones and AI-driven threat detection, enhancing coastal defense. Thales Group plays a key role in Europe, providing integrated naval command and radar systems across NATO fleets. Elbit Systems supports Asia Pacific and the Middle East with drone surveillance and maritime C4ISR technologies. Leonardo S.p.A. focuses on real-time maritime monitoring systems tailored for the Mediterranean and African regions. These firms leverage advanced tech, cross-border collaborations, and government partnerships to strengthen global maritime safety.

Key Developments

- 2024: Kongsberg Group launched an AI-powered maritime surveillance system, improving threat detection accuracy by 15%.

- 2023: Raytheon Technologies introduced a cybersecurity platform for port management systems, reducing cyber risks by 20%.

- 2023: Thales Group partnered with a leading port authority to deploy drone-based coastal surveillance systems, enhancing monitoring efficiency.

Companies Covered in Maritime Security Market

- Kongsberg Group

- Raytheon Technologies

- Thales Group

- Elbit Systems

- Others

Frequently Asked Questions

The market is expected to grow from US$ 23.5 billion in 2025 to US$ 45.5 billion by 2032, with a CAGR of 9.9%.

Services lead with a 62.4% share in 2024 and are the fastest-growing segment, driven by outsourcing and system integration needs.

Maritime surveillance dominates with a 35.6% share, driven by advanced radar and satellite technologies.

Governments hold a 45.3% share and are the fastest-growing, driven by increased security budgets and modernization programs.

North America leads, while Asia Pacific is the fastest-growing region, driven by China and India’s expanding maritime trade.

Kongsberg Group, Raytheon Technologies, Thales Group, and Elbit Systems are leading players, focusing on innovative surveillance and cybersecurity solutions.