- Inks, Coatings, Adhesives & Sealants (ICAS)

- Sealant Web Film Market

Sealant Web Film Market Size, Share, and Growth Forecast, 2026 - 2033

Sealant Web Film Market By Thickness (16–35 microns, >50 microns, Others), Material (Polypropylene (PP), Polyethylene (PE), Others), Application, and Regional Analysis for 2026 - 2033

Sealant Web Film Market Size and Trends Analysis

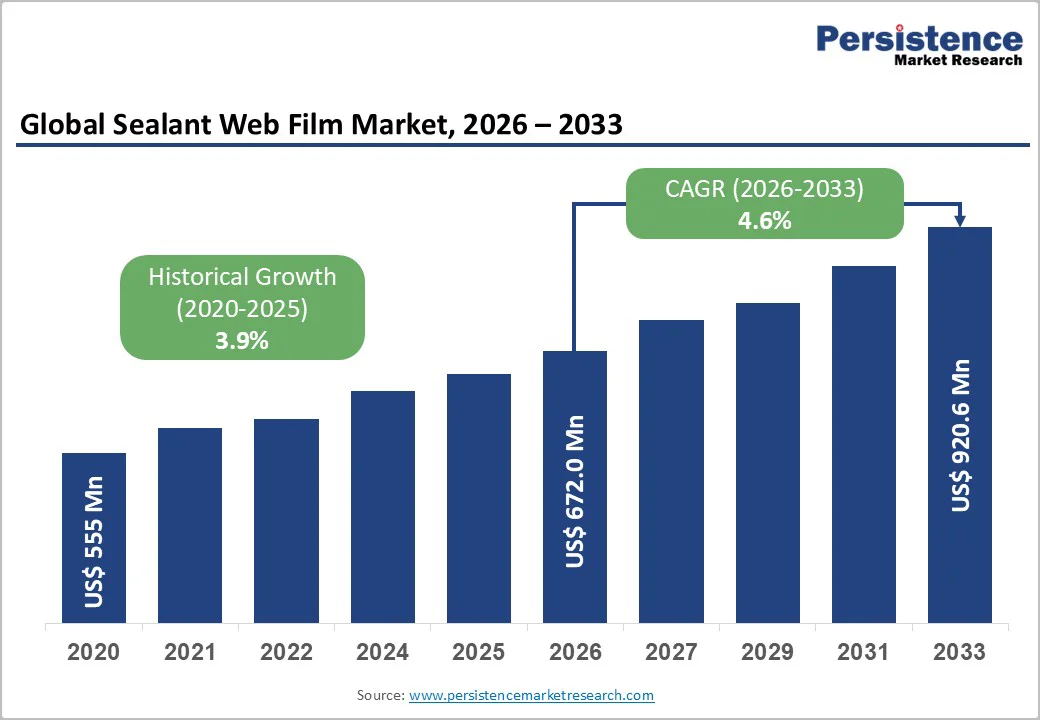

The global sealant web film market size is projected to reach US$672.0 million in 2026 and rise to US$920.6 million by 2033, reflecting a 4.6% CAGR from 2026 to 2033, driven by rising food-packaging volumes, rapid expansion of value-added pouch formats, and strong adoption of recyclable all-polyolefin structures worldwide.

Advances in PE and PP sealant formulations, including low-seal-initiation-temperature (SIT) chemistries and bio-based alternatives, strengthen market momentum. Increasing automation across modern pouching lines improves uptake, while raw-material volatility and regulatory shifts toward recyclability remain key risk factors.

Key Industry Highlights

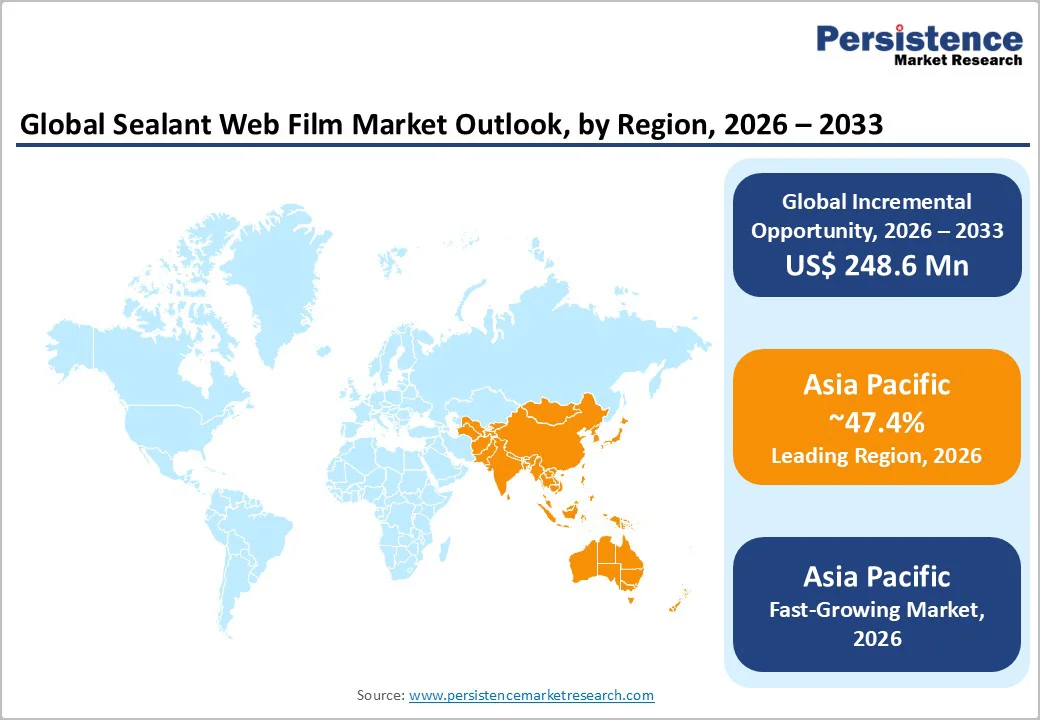

- Leading Region: Asia Pacific, to account for approximately 47.4% of the global demand in 2026, driven by large-scale flexible-packaging consumption in China, India, and ASEAN markets.

- Fastest-growing Region: Asia Pacific is likely to record the highest CAGR, supported by rapid urbanization, packaged-food penetration, and expanding investments in co-extrusion and mono-material film lines.

- Investment Plans: Strong capacity expansion across APAC and North America, including UFlex’s 2024 installation of multilayer PE film lines in India, Indorama Ventures’ 2023 resin-grade upgrades in Thailand, and Charter Next Generation’s 2023 PE capacity expansion in the U.S., all directed toward recyclable mono-material PE and PP packaging.

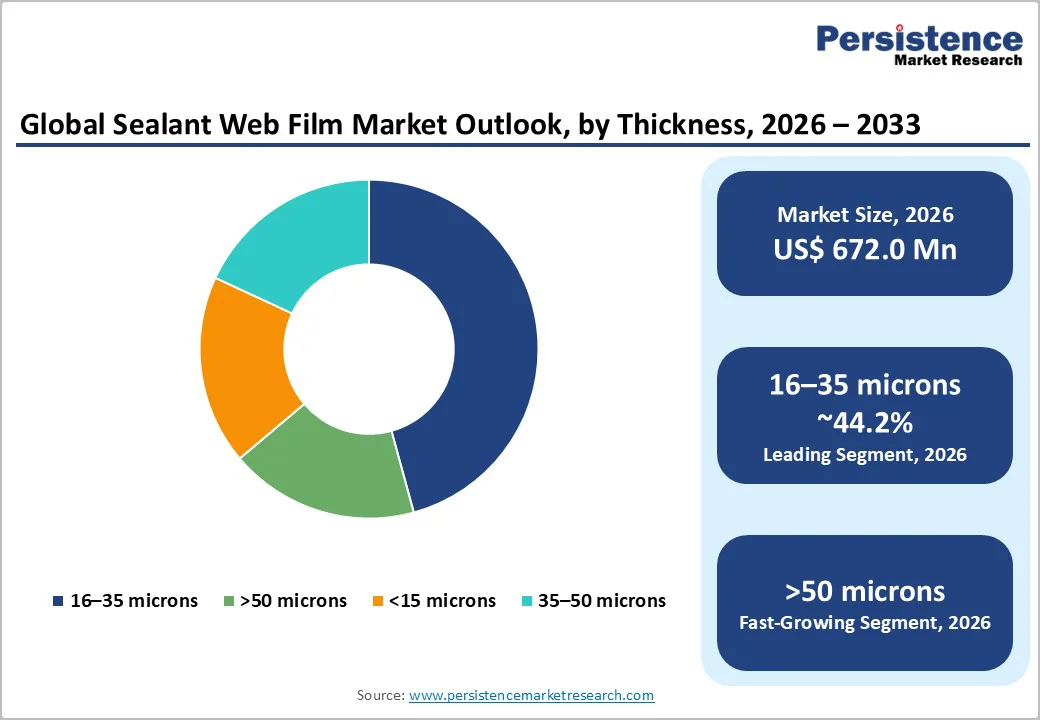

- Dominant Thickness: 16–35 microns, to hold about 44.2% market share in 2026, driven by widespread use in HFFS/VFFS lines, reliable low-SIT sealing, and strong adoption across snack, dry-food, and everyday consumer-goods packaging.

- Leading Material: Polypropylene (PP) is likely to hold approximately 32.4% share in 2026, supported by its high-speed sealing stability, stiffness, and strong performance in duplex and triplex laminations for food, confectionery, and personal-care packaging.

| Key Insights | Details |

|---|---|

|

Sealant Web Film Market Size (2026E) |

US$672.0 Mn |

|

Market Value Forecast (2033F) |

US$920.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Growth of Flexible Food Packaging and Pouch Formats

Global demand for packaged foods and convenience formats continues to expand, and flexible pouches now represent one of the fastest-growing packaging categories. Sealant web films serve as the essential inner-seal layer, ensuring heat-seal reliability, machinability, and shelf-life stability on both HFFS and VFFS equipment. Adoption accelerates as converters seek materials with low SIT, strong hot-tack performance, and wider processing windows that enable stable sealing at high line speeds. Food and beverage applications account for roughly 38% of the total sealant web film consumption, making it the market’s largest end-user.

Material Innovation: Polypropylene Dominance and Polyolefin Recyclability

Polypropylene maintains a leading material share due to its superior melting point, stiffness, and sealing robustness at high machine speeds. Ongoing innovation in PP grades, including co-extruded sealant layers and enhanced low-temperature sealing variants, widens its application scope. The global shift toward mono-material polyolefin structures (all-PE or all-PP) also strengthens demand, as brands redesign packaging to comply with recyclability guidelines. The combination of high technical performance and growing circularity requirements establishes a durable, long-term growth runway for PP- and PE-based sealant webs.

Evolving Regulatory and Retailer Requirements

Retailers and regulators continue tightening packaging rules to reduce waste and increase recyclability. As a result, converters transition toward structures compatible with established recycling streams, such as all-PE and mono-PP designs, and explore bio-based alternatives in select applications. Specifications increasingly mandate downgauging to reduce resin consumption without compromising seal strength, encouraging the use of advanced sealant web formulations that enable lighter constructions and cost efficiency.

Barrier Analysis - Raw-material Price Volatility and Feedstock Supply Constraints

Sealant web films are heavily dependent on polyolefin resins whose pricing is linked to naphtha and ethane feedstocks. Periodic price spikes place pressure on film producers and converters, limiting margins and slowing procurement cycles. Specialty sealant resins with unique characteristics, such as low-SIT modifiers or EVOH tie layers, are particularly vulnerable to lead-time fluctuations. These supply uncertainties prompt manufacturers to carry additional safety stock, raising working-capital requirements and exerting short-term pressure on production schedules.

Technical Complexity of Recyclable and Bio-Based Structures

Engineering recyclable mono-material structures while maintaining seal strength, peelability, and barrier properties is technically challenging. Trade-offs between recyclability and performance often extend development cycles and increase formulation costs. High-sensitivity applications such as retort and modified-atmosphere packaging require stringent validation, and food-contact approval processes further prolong commercialization timelines for new materials. These constraints slow the replacement rate of incumbent multilayer structures.

Opportunity Analysis - Downgauging and Lightweighting Expansion

Brand owners continue to prioritize material reduction across flexible packaging lines. A 5 to 8% reduction in average film gauge for food pouches, combined with improved sealant performance, can unlock an incremental US$20–40 million value pool over a seven-year horizon. Premium low-gauge sealant webs that maintain seal strength despite reduced thickness deliver strong opportunities for film producers who invest in advanced additive packages and co-development programs with converters.

Emerging Markets and Rigid-To-Flexible Conversion

Asia Pacific and select Latin American markets display rapid conversion of rigid and glass packaging toward flexible pouches for cost, logistics, and shelf-life advantages. This shift is especially pronounced in ready-to-eat foods, sauces, dairy spouted pouches, and refrigerated categories. With Asia Pacific accounting for approximately 48% of global demand, expanding capacity in India, China, and ASEAN countries offers substantial volume upside. Adoption of recyclable all-PE pouch designs accelerates growth as local brands modernize packaging to match global sustainability standards.

Category-wise Analysis

Thickness Insights

The 16–35 micron band maintains leadership, anticipated to hold 44.2% of market share, as it offers an effective balance between seal reliability, mechanical strength, and material efficiency. This range is extensively adopted in stand-up pouches, fin-seal wrappers, and duplex or triplex laminated structures that require consistent low-SIT performance. Its compatibility with both HFFS and VFFS systems helps converters achieve stable machinability, reduced seal failures, and high line speeds across food, beverage, and personal care packaging operations.

Many global converters, including those supplying major FMCG brands, rely on this gauge for dry snacks, fresh produce packs, and powdered product pouches due to its predictable pinhole resistance and uniform hot-tack behavior. Growing automation in flexible packaging lines reinforces this preference. Pouching operations in Asia and Europe have increasingly standardized on the 16–35 µm range to ensure throughput consistency during 24/7 production cycles. High-speed snack packaging lines, for instance, routinely use 20–30 µm sealant webs to support rapid sealing at 300–500 packs per minute without compromising edge integrity.

The above 50 micron thickness segment records the fastest expansion due to its suitability for applications requiring enhanced durability and barrier uniformity. Heavy-fill food pouches such as large-format rice bags, pet food retort pouches, and institutional sauce packages increasingly specify thicker sealant layers to withstand intense sealing pressure, weight load, and mechanical handling. Industrial and agrochemical packaging formats, including fertilizer refill packs and construction chemical sachets, also utilize >50 µm films for added strength and puncture resistance. Sterilizable and retort-grade medical packaging represents another growth area where thicker films help maintain seal integrity under high-temperature processing.

Co-extrusion investments across China, India, and Southeast Asia have improved the production efficiency of this thickness class. Manufacturers are installing wider die-headlines and advanced MDO technology to tailor sealant structures for durability-centric applications. These upgrades support faster adoption in segments requiring both robustness and specific functional performance, driving an above-average CAGR for >50 µm films.

Material Insights

Polypropylene is anticipated to dominate, expected to hold a market share of 32.4%, due to its proven thermal stability, stiffness, and strong sealing performance across diverse high-speed packaging environments. It remains integral to laminated structures for snacks, bakery goods, dry foods, and premium confectionery applications. PP-based sealant webs deliver reliable hot-tack strength, narrow temperature-window sealing, and dimensional stability needed in flow-wrap formats operating at high throughput rates.

In vertically form-fill-seal packaging for pasta, pulses, or sugar, PP helps maintain package shape and prevents deformation when filled under rapid cycles. Converters producing duplex and triplex laminates frequently rely on BOPP-PP sealant combinations for their compatibility with metallized and barrier layers. PP’s ability to achieve down-gauging without major loss of performance keeps it cost-effective. Regional case examples include major snack manufacturers in India and Indonesia using PP-based webs for lightweight pillow packs, and European confectionery brands adopting PP structures for shelf-stable chocolate bars to maintain crisp seal profiles during distribution.

Polyethylene gains momentum as the fastest-growing material category due to global sustainability policies and the surge in demand for mono-material, recyclable flexible packaging. Modern LDPE and LLDPE grades offer improved toughness, impact resistance, and better clarity, helping brand owners transition away from multi-material laminates. All-PE pouch formats, popular for frozen foods, liquids, and personal care refill packs, demonstrate increasing adoption across North America, Europe, and APAC. Flexible packaging suppliers have introduced PE sealant webs with enhanced low-temperature seal initiation, enabling energy-efficient sealing and reducing cycle times.

Design-for-recycling guidelines from organizations such as CEFLEX and the U.S. Plastics Pact further support PE growth. Recyclable PE monoweb solutions used in detergent refill pouches and high-barrier food products often incorporate MDO-PE layers combined with LLDPE sealants. As large retailers and FMCG companies commit to 100% recyclable packaging portfolios, PE-based structures are becoming a preferred choice in new product developments, reinforcing the segment’s rapid growth trajectory.

Regional Insights

North America Sealant Web Film Market Trends - Sustainability and Automation Drive Mono-Material Adoption

North America represents a high-value market for sealant web films, driven by widespread adoption of flexible packaging across food, beverage, medical, and industrial sectors. The region benefits from a large installed base of automated form-fill-seal equipment and strong consumer demand for convenience and single-serve formats. The U.S. leads with high per-capita flexible-packaging consumption and broad availability of advanced sealant formulations.

Specialty solutions, including peelable films, high-temperature grades, and PCR-compatible materials, are increasingly adopted as converters seek technical differentiation. Sustainability mandates further reinforce growth. California’s SB 54, for instance, targets a 25% reduction in single-use plastics by 2032, accelerating adoption of mono-material PE and PP structures, while retailers such as Walmart promote recyclable packaging via How2Recycle’s Store Drop-Off program.

North America also serves as a testing ground for next-generation materials due to its combination of stringent processing standards and sustainability commitments. The U.S. offers the largest revenue potential, particularly in premium food packaging and sterile medical-device pouches. Extended Producer Responsibility (EPR) laws in Oregon and Colorado incentivize recyclable design, prompting film manufacturers to optimize laminates and sealant layers.

Companies providing validated food-contact compliance and recyclability testing, such as APR’s “Design Guide Certified” materials, gain competitive advantages. Notable investments include Charter Next Generation’s 2023 PE film capacity expansion in Wisconsin and Berry Global’s 2024 launch of its Entour mono-PE film series, designed for high-speed sealing, highlighting North America’s role as both a high-value and innovation-driven market for sealant web films.

Europe Sealant Web Film Market Trends - Regulatory Pressure Spurs Recyclable Sealant Innovation

Europe remains a major value contributor to advanced sealant web films, driven by strict food-safety requirements, retailer-led sustainability mandates, and broad adoption of flexible and hybrid paper-based structures. Germany, the U.K., France, and Spain generate most regional demand, each with distinct priorities. Germany shows strong momentum in high-barrier and sterilizable applications, while the U.K. and France lead the shift toward recyclable mono-material pouches.

EU-wide regulatory alignment heavily shapes material innovation. The revised 2023–2024 PPWR proposal sets binding rules for recyclability, minimum recycled content, and design-for-recycling, encouraging converters to replace mixed laminates with mono-PE and mono-PP structures. Paper-based barrier solutions also accelerate, supported by CEFLEX’s 2023 “Designing for a Circular Economy” guidelines, which define recyclability and performance requirements for sealant layers and interfaces.

The region emphasizes solutions that balance downgauging, machinability, barrier performance, and recyclability. PE and PP sealant formulations continue advancing, while emerging bio-based options, such as PLA-compatible sealant coatings, gain traction in premium organic foods. Hybrid paper–film structures, requiring sealants tailored to fiber substrates, see growing adoption in Northern Europe as retailers commit to fiber-first formats. Industry examples include Mondi’s 2023 launch of a mono-PE stand-up pouch for dry foods and Amcor’s 2024 rollout of its AmPrima mono-PE recyclable film family, underscoring Europe’s leadership in sustainability-driven innovation and reinforcing sustained demand for high-barrier, recyclable sealant web films.

Asia Pacific Sealant Web Film Market Trends - Rapid Growth Fueled by Policy and Consumption

Asia Pacific is the largest and fastest-growing market for sealant web films, accounting for about 47.4% of global demand. Growth is propelled by rapid urbanization, rising disposable incomes, and expanding modern retail channels that increase flexible-packaging consumption. China and India contribute the highest incremental volumes, while ASEAN countries show the fastest percentage growth. Demand expands across snacks, ready meals, sauces, frozen foods, home-care refills, and pharmaceuticals, reflecting the region’s broadening packaged-goods landscape.

China leads by scale, supported by a dense converter base and sustainability-driven policies such as the 2020 China Plastic Pollution Control Plan, which restricts non-recyclable plastics in key cities and encourages adoption of recyclable PE- and PP-based packaging. India posts the fastest CAGR among major APAC markets, driven by packaged-food penetration and organized retail expansion. Regulatory actions, including the 2022 ban on select single-use plastics and amendments to the Plastic Waste Management Rules mandating EPR, push brands toward recyclable mono-material formats.

Sustainability commitments from global FMCG companies further accelerate the transition. Unilever’s pledge to use 100% recyclable or reusable packaging by 2025 has increased adoption of all-PE refill pouches across Southeast Asia, boosting demand for advanced PE sealant webs. Investment momentum remains strong, with developments such as Indorama Ventures’ 2023 resin-grade upgrades in Thailand and UFlex’s 2024 commissioning of multi-layer PE film lines in India to support recyclable pouch production.

Growing recycling mandates, robust converter ecosystems, and massive consumer markets collectively position Asia Pacific as the dominant growth engine for sealant web films over the coming decade.

Competitive Landscape

The global sealant web film market is moderately concentrated among global film manufacturers and specialty resin suppliers, with a diverse base of regional technical mills serving localized demand. Leading players capture the majority of premium value through broad material portfolios, advanced co-extrusion capabilities, and strong technical-service infrastructure. Competition centers on sealing performance, recyclability, downgauging efficiency, and food-contact compliance. Barriers to entry include high capital requirements for multi-layer extrusion, testing facilities, and regulated-market certifications. Companies that combine innovation with sustainability credentials maintain a clear competitive advantage.

Winning strategies focus on advancing low-temperature sealant technologies, enabling mono-material recyclable laminates, and building upstream partnerships for PCR and specialty resin development. Companies that offer strong regulatory support, technical service, and co-development programs with converters gain a sustained advantage. Sustainability alignment and downgauging solutions remain central to competitive positioning.

Key Industry Developments

- In March 2025, TOPPAN Holdings completed the acquisition of Sonoco Thermoformed & Flexible Packaging business, integrating its high-performance thin-film plastic operations into TOPPAN’s sustainable films portfolio.

- In December 2024, Berry Global, in collaboration with VOID Technologies, launched a new high-performance polyethylene (PE) film for pet-food packaging. The film uses VOID’s VO+™ voiding technology to deliver strength, puncture resistance, and recyclability in an all-PE format.

Companies Covered in Sealant Web Film Market

- Amcor plc

- Mondi Group

- Berry Global

- UFlex Ltd.

- Charter Next Generation (CNG)

- Sealed Air Corporation

- Constantia Flexibles

- Plastopil Flexible Packaging

- Oben Group

- ProAmpac

- Coveris

- Clondalkin Group

- Huhtamaki

- Cosmo Films

- Jindal Poly Films

- Toray Plastics

- Winpak Ltd.

- Polyplastics Industries

- Glenroy Inc.

- Flex Films (Flex Americas)

Frequently Asked Questions

The market size is estimated to reach US$672.0 million in 2026.

By 2033, the sealant web film market is projected to reach US$920.6 million, supported by rising adoption of mono-material structures and strong flexible packaging demand.

Major trends include the shift toward recyclable mono-PE and mono-PP laminates, increased use of downgauged films, adoption of PCR-compatible sealant layers, and strong regulatory influence from global recycling mandates (EU PPWR, India PWM Rules, U.S. EPR frameworks).

By thickness, the 16–35 micron segment leads with 44.2% share, widely used in HFFS and VFFS applications.

The sealant web film market is projected to grow at a CAGR of 4.6% between 2026 and 2033.