- Inks, Coatings, Adhesives & Sealants (ICAS)

- Polysulfide Sealants Market

Polysulfide Sealants Market Size, Share, and Growth Forecast 2026 - 2033

Polysulfide Sealants Market by Form (One Component, Two Component), Application (High - and Low-Rise Building Structures, Civil Engineering, Commercial, Automotive Sealings, Aircraft Components, Marine Sealings, Other), and Regional Analysis for 2026 - 2033

Polysulfide Sealants Market Size and Trend Analysis

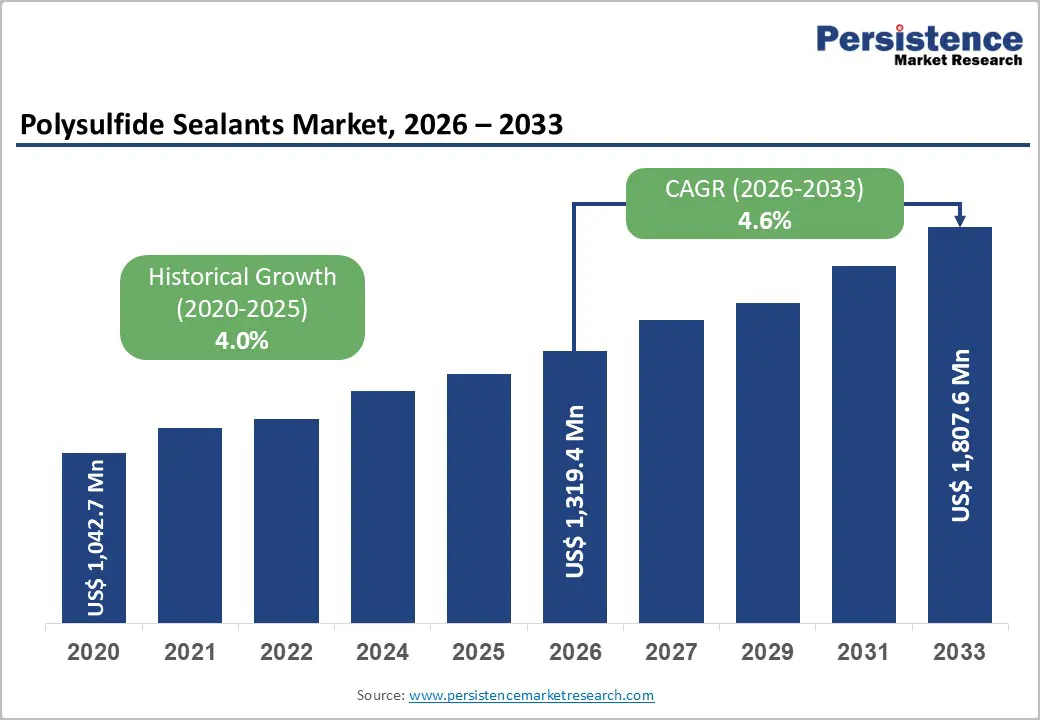

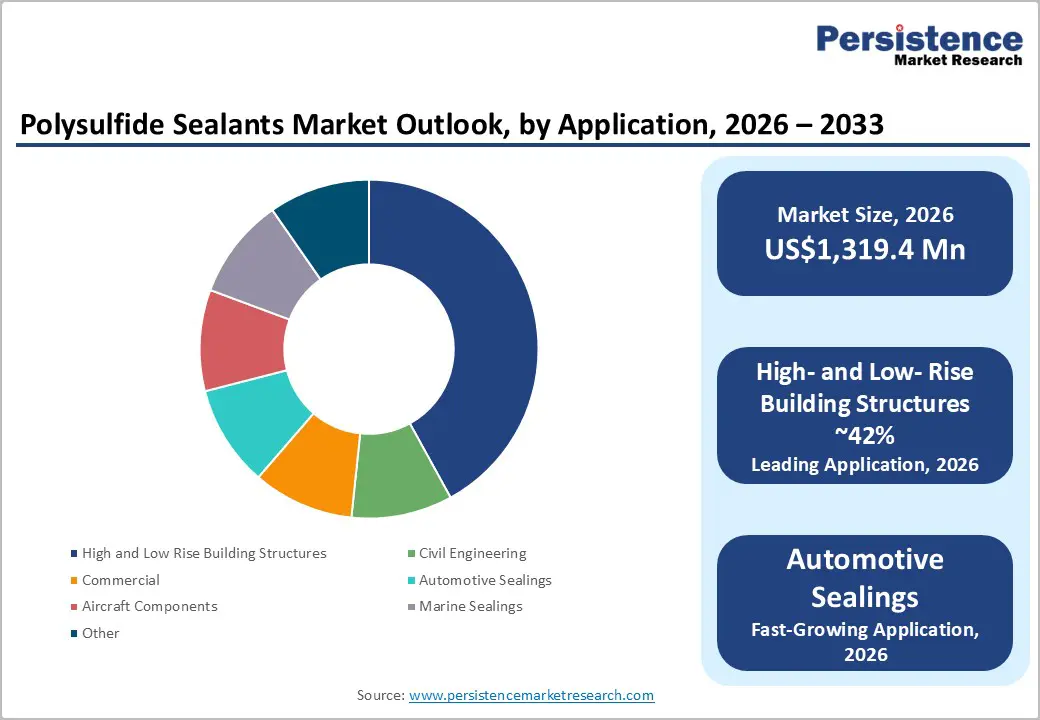

The global polysulfide sealants market size is supposed to be valued at US$ 1,319.4 Mn in 2026 and is projected to reach US$ 1,807.6 Mn by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

The market's expansion is primarily driven by increasing demand from the aerospace sector, where polysulfide sealants offer superior fuel resistance and durability, and by robust infrastructure development in emerging economies. As global construction activity accelerates and aircraft manufacturing reaches new production heights, polysulfide sealants remain the material of choice for sealing applications requiring exceptional chemical resistance, flexibility, and long-term performance across diverse substrates, including metals, glass, and composites.

Key Industry Highlights:

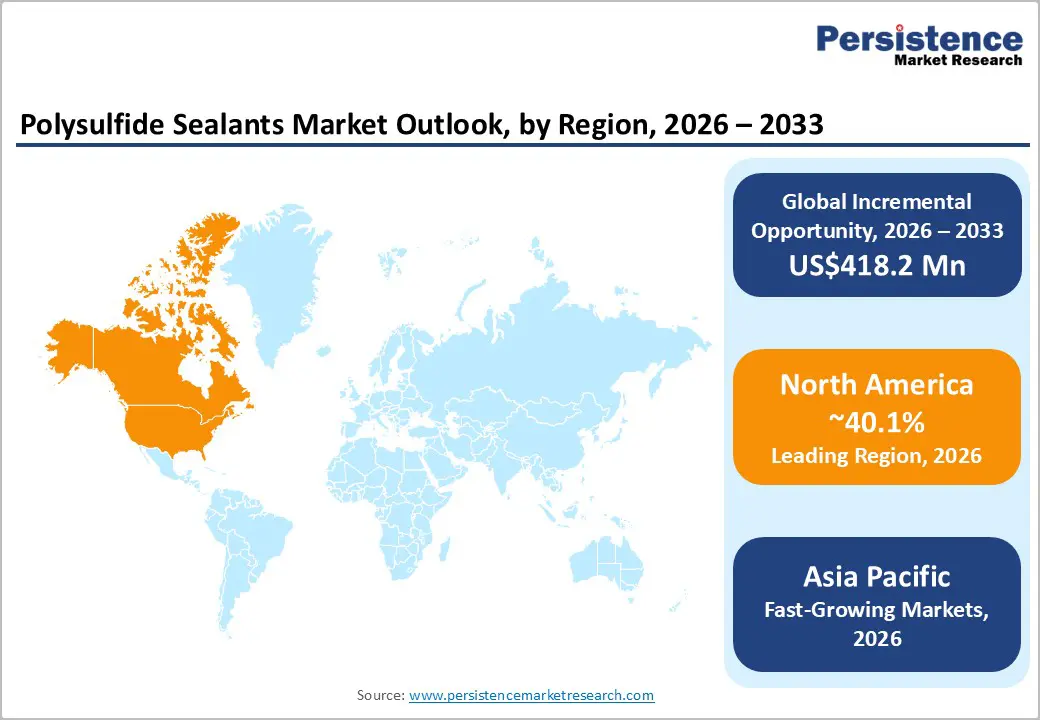

- Leading Region: North America commands the largest share, of 40.1%, of the global polysulfide sealants market, driven by established aerospace manufacturing infrastructure, stringent construction standards, and advanced regulatory frameworks supporting the adoption of high-performance sealants.

- Fastest Growing Region: Asia-Pacific emerges as the fastest-growing regional market, with India leading expansion through smart city initiatives and urban housing programs, supported by China's infrastructure modernization and Southeast Asia's accelerating industrialization, creating substantial demand for building construction and civil engineering sealants.

- Dominant Segment: Two-component polysulfide sealants represent the dominant segment within the Form category, commanding 67% market share due to superior performance control, non-sag properties enabling vertical application, and excellent adhesion to diverse substrates in high-rise and low-rise building structures, civil engineering projects, and aerospace fuselage sealing applications.

- Fastest Growing Segment: Insulated glass unit secondary sealing applications represent the fastest-growing segment within the Building & Construction category, driven by global energy efficiency mandates, retrofit demand, and polysulfide capability to enhance thermal performance by up to 30%, creating sustained demand from residential and commercial property owners pursuing energy cost reduction.

- Key Market Opportunity: Development and commercialization of low-volatile organic compound (VOC) polysulfide formulations represent the primary market opportunity, as stringent environmental regulations across North America and Europe drive market demand for sustainable sealants meeting LEED certification and regulatory compliance requirements while maintaining superior fuel resistance and durability characteristics required by aerospace and infrastructure applications.

| Key Insights | Details |

|---|---|

| Polysulfide Sealants Market Size (2026E) | US$ 1,319.4 Mn |

| Market Value Forecast (2033F) | US$ 1,807.6 Mn |

| Projected Growth CAGR (2026 - 2033) | 4.6% |

| Historical Market Growth (2020 - 2025) | 4.0% |

Market Dynamics

Drivers - Aerospace Production Expansion and Fuel Tank Sealing Demand

The rapid expansion of global aerospace production continues to drive growth in the polysulfide sealants market. Modern commercial aircraft, including advanced platforms such as the Boeing 787 and Airbus A350, require highly specialized fuel-tank sealing systems engineered to endure extreme temperature fluctuations and persistent exposure to aviation fuels. Polysulfide-based formulations, exemplified by PPG’s P/S 890®F Class A and PR-1740 Class B solutions, provide exceptional fuel resistance and elastomeric performance, exceeding the capabilities of competing sealant technologies.

Furthermore, PPG Industries’ US$380 million investment in a new aerospace sealants facility in North Carolina reflects strong confidence in the sector’s long-term demand outlook. As global aircraft deliveries continue to rise, manufacturers increasingly rely on lightweight, high-performance sealants to enhance fuel efficiency and reduce overall operational costs.

Infrastructure Expansion and Building Envelope Performance Requirements

The Building and Construction Sealants Market continues to grow strongly, with polysulfide sealants playing a critical role in high-performance structural applications. Rapid urbanization across developing regions, particularly India, China, and Southeast Asia, is driving substantial demand for durable construction materials. Polysulfide sealants deliver superior performance in insulated glass unit (IGU) secondary sealing, forming long-lasting, watertight barriers that preserve structural integrity for over two decades. Civil engineering projects, including tunnels, underpasses, and bridge systems, increasingly rely on these sealants for their resistance to water, fuels, and salts.

Rising global infrastructure development further amplifies demand, as polysulfide sealants provide excellent bond strength to concrete and reinforcement materials, ensuring reliable performance under thermal stress, dynamic loads, and chemical exposure. Growing urbanization, combined with Europe’s stringent energy-efficiency standards, continues to expand the market for polysulfide-based sealing solutions.

Restraints - Stringent Environmental Regulations and VOC Emission Compliance

Increasingly stringent environmental regulations across the European Union and North America are imposing tighter limits on volatile organic compound (VOC) emissions from construction materials. Traditional polysulfide sealants, which contain sulfur-based compounds, release VOCs during application and curing, creating significant compliance challenges for manufacturers serving premium construction markets that prioritize LEED certification and related sustainability standards. As regulatory bodies restrict the use of high-VOC sealants in large-scale building projects, market penetration has declined in regions with strict environmental oversight.

Manufacturers also face enhanced scrutiny from agencies such as the U.S. Environmental Protection Agency, which enforces strict VOC content limits and mandates high capture and control efficiencies, often requiring costly pollution-control investments or formulation changes. Furthermore, toxicity concerns with certain curing agents in traditional polysulfide systems are prompting research into alternative chemistries that may improve overall performance.

Competition from Alternative Sealant Technologies and Performance Limitations

Silicone and polyurethane sealants present significant competitive challenges to polysulfide formulations due to their superior UV resistance, broader application versatility, and faster curing characteristics. Silicone sealants, which account for over 34% of the global adhesives and sealants market, dominate the insulated glass and general construction segments, while polyurethane sealants offer faster application cycles and easier cleanup, making them suitable for time-sensitive projects.

Polysulfide sealants exhibit weaker UV aging resistance, often causing surface degradation under prolonged sunlight, limiting their suitability for exposed-frame curtain wall systems. Competition is further intensified by advances in silicone-based technologies, including greater temperature tolerance and improved UV performance. Innovations such as Wacker Chemie AG’s GENIOSIL® XB hybrid series also expand the range of alternatives, while the higher complexity of two-component polysulfide systems continues to hinder adoption in markets prioritizing ease of installation.

Opportunity - Energy-Efficient Building Standards and Insulated Glass Unit Growth

The growing global focus on reducing building energy consumption is driving increased demand for high-performance insulated glass units (IGUs) with superior thermal insulation. Polysulfide sealants, used as secondary seals in IGU production, can enhance thermal performance by up to 30%, resulting in notable energy savings for residential and commercial buildings. Strengthening building codes, tax incentives, and mandatory energy certifications continue to support sustained demand for premium sealing materials. Retrofit and renovation activities in developed economies further drive market growth, as aging facades and windows are replaced with modern IGU systems using polysulfide compounds.

The expanding IGU market creates significant opportunities for polysulfide sealants, which offer excellent gas retention and long-term durability. Strict European energy-efficiency standards and rapid capacity expansion across the Asia-Pacific reinforce adoption, benefiting manufacturers that can provide cost-efficient formulations and regional technical support.

Marine Sealings and Underwater Applications in Coastal Infrastructure

The marine sealants market presents a substantial growth opportunity for polysulfide formulations, given their exceptional water resistance and chemical stability in demanding underwater and coastal infrastructure environments. Polysulfide resins maintain strong adhesion and flexibility under continuous immersion, salt exposure, and hydrostatic pressure, conditions that quickly degrade many alternative chemistries. Increasing investments in port modernization, offshore structures, and coastal protection projects across Asia-Pacific and the Middle East are expanding demand for marine-grade polysulfide sealants.

Nouryon B.V.’s 2024 expansion of its Thioplast™ line, featuring improved elongation and low-temperature flexibility, further supports adoption in marine applications. This segment faces limited substitution threats, as few alternatives match polysulfides’ combined fuel resistance, durability, and long-term performance. Companies developing formulations optimized for underwater curing and for adhesion to substrates such as fiberglass, aluminum, and marine-grade steel are well positioned to capture this growing market.

Category-wise Analysis

Form Insights

Two-component polysulfide sealants dominate the market, with an approximately 67% share in 2026, driven by superior performance control and application flexibility relative to one-component alternatives. Within the two-component category, gun-grade formulations command 60% of the segment due to their non-sag properties, enabling vertical and overhead application in high-rise and low-rise building structures, civil engineering projects, and aircraft fuselage sealing. Gun-grade products like Sika® Polysulphide Gun Grade and Arbokol AG2 provide excellent adhesion to concrete, metal, and composite substrates while accommodating cyclic movement through high elongation properties. The aerospace industry's stringent qualification requirements, including compliance with SAE International specifications such as AMS3281D for fuel tank sealants, effectively mandate two-component systems due to their superior fuel resistance and thermal-cycling performance.

Pour-grade or self-leveling formulations capture the remaining two-component market share, serving horizontal floor joint applications, roadway sealing, and expansion joints in structures subjected to vehicular traffic. One-component, moisture-cure polysulfide sealants constitute a niche segment that benefits from faster application and reduced site mixing, although their limited performance envelope restricts adoption to applications with moderate environmental stress.

Application Insights

High- and low-rise building structures constitute the largest application segment, accounting for approximately 42% of the market in 2026, reflecting extensive use of polysulfide sealants in walls, flooring systems, and insulated-glass installations. Within this category, insulated glass units exhibit strong growth, driven by building codes that increasingly mandate energy-efficient envelope systems that require durable secondary sealing to maintain thermal performance over long service lives.

Civil engineering applications, including tunnels, underpasses, bridges, and roadway joints, form the second-largest segment, supported by the ability of polysulfide sealants to accommodate cyclic movement while preserving waterproof integrity under varying loads and temperatures. Although aircraft components account for a smaller volume share, they command premium prices due to stringent qualification requirements and critical safety needs, such as fuel-tank sealing, for which polysulfide formulations provide unmatched fuel resistance. Royal Adhesives and Sealants has achieved SAE qualification for lightweight polysulfide aircraft sealants with specific gravity below 1.05, delivering approximately 35% weight reduction while meeting AMS3281D Type 3 Class B specifications.

Regional Insights

North America Polysulfide Sealants Market Trends

North America retains a leading position in the polysulfide sealants market, supported by a well-established aerospace manufacturing base, stringent construction standards, and strong adoption of advanced technologies. The U.S. remains at the forefront of aerospace sealant innovation, with major producers such as PPG Industries operating sophisticated facilities across strategically important locations. The aerospace sector, primarily concentrated in California, Washington, and Arizona, accounts for nearly one-quarter of global aircraft production and generates sustained demand for specialized, high-performance sealants.

Regulatory frameworks, including FMVSS and MIL-spec standards, further mandate the use of premium sealants in structural glazing and safety-critical applications, reinforcing regional market strength. PPG’s expansion of its Shildon aerospace sealants capacity enhances supply capabilities for both domestic and international markets. Additionally, ongoing infrastructure renewal and energy-efficiency retrofits continue to support construction-sector demand, while environmental regulations in states such as California drive the development of low-VOC formulations and encourage continued product innovation.

Europe Polysulfide Sealants Trends

Europe is a highly regulated market where stringent building material standards and strong sustainability commitments continue to drive demand for premium polysulfide sealants. The region benefits from robust market fundamentals, supported by advanced energy-efficiency regulations and a mature construction chemicals industry focused on high-performance, environmentally compliant sealing solutions. Germany leads regional innovation, with companies such as Wacker Chemie AG, Sika AG, and Henkel AG & Company, KGaA maintaining sophisticated research and development capabilities dedicated to performance optimization and sustainability.

Henkel’s €20 million investment in 2024-2025 to modernize its Bopfingen facility further underscores this focus by expanding capacity for advanced adhesive technologies and sustainable raw materials. Germany, the U.K., and France demonstrate particularly strong adoption due to Energy Performance of Buildings Directive (EPBD) requirements, while Europe’s emphasis on low-VOC, eco-friendly formulations positions the region as a leading center for next-generation polysulfide sealant innovation.

Asia-Pacific Polysulfide Sealants Market Trends

The Asia-Pacific region is the fastest-growing market, driven by rapid urbanization, robust infrastructure investment, and expanding manufacturing activity across emerging economies. The region’s construction boom is driving substantial demand for polysulfide sealants across residential, commercial, and large-scale civil engineering projects, including bridges, tunnels, and transportation networks. China and India show strong momentum, with India’s Smart Cities Mission supporting the adoption of advanced waterproofing sealants and high-performance building envelope systems.

Regional and global manufacturers are increasing local production capacity, including Dow’s expansion of silicone intermediates in Zhangjiagang and Wacker Chemie AG’s new silicone plant in Nanjing. The insulated glass unit market is also expanding rapidly, driven by domestic demand and export opportunities. Japan further contributes through rising automotive demand for advanced sealants in electric vehicle applications.

Competitive Landscape

The polysulfide sealants market reflects a moderately consolidated competitive structure, with regional and global players differentiating through technology, product performance, and specialization. Major multinational companies, including PPG Industries, 3M Company, Sika AG, and Henkel AG & Co. KGaA, lead the aerospace and premium construction segments through strong distribution networks and advanced research capabilities. Market leaders focus on developing low-density formulations for aerospace weight reduction, low-VOC products to meet environmental regulations, and rapid-cure systems that enhance production efficiency. Emerging manufacturers and specialty suppliers compete through cost optimization and localized technical support. The competitive landscape is driven by continuous innovation in formulation chemistry, application systems, and sustainability features.

Key Market Developments

- October 2025: Henkel Adhesive Technologies and Dow announced expanded collaboration to accelerate decarbonization across adhesive portfolios, introducing low-carbon feedstocks and renewable electricity into hot melt adhesive production processes, targeting a 20-40% reduction in product carbon footprint and supporting Science-Based Targets Initiative (SBTi) compliance objectives for industrial sustainability.

- December 2024: Arkema Group completed the acquisition of Dow's flexible packaging laminating adhesives business, generating approximately US$250 million in annual sales with operations at five production facilities across Italy, the United States, and Mexico, significantly expanding Bostik's portfolio in the attractive flexible packaging adhesives market.

- October 2024: Henkel AG & Company, KGaA, announced a €20 million investment program spanning 2024 and 2025 to expand and modernize its adhesives production facility in Bopfingen, Germany, focusing on advanced hotmelt and polyurethane formulations utilizing sustainable alternative raw materials.

Top Companies in Polysulfide Sealants Market

- PPG Industries, Inc. (Pittsburgh, U.S.) maintains market leadership through a comprehensive aerospace sealants portfolio, including P/S 890®F Class A, PR-1740 Class B, and PR-1782® Class B Low Density formulations serving fuel tank and fuselage sealing applications. The company's global manufacturing footprint, including facilities in Shildon, England, and Mojave, California, positions PPG to serve EMEA, Americas, and Asia-Pacific markets through established application support centers and customized packaging solutions.

- 3M Company (St. Paul, U.S.) offers advanced polysulfide aerospace sealants, including AC-380, AC-735, AC-770, and AC-251 products engineered for quick-curing, low-density performance, optimizing aerospace manufacturing efficiency. The company's specialization in manganese dioxide-cured formulations and corrosion-inhibitive sealant technologies supports expanded adoption in commercial and military aircraft production.

- Henkel AG & Company, KGaA (Düsseldorf, Germany) operates a diversified adhesives and sealants business serving construction, automotive, aerospace, and industrial manufacturing sectors through its Adhesive Technologies division. The company's €20 million modernization program at its Bopfingen, Germany, facility targets capacity expansion for advanced adhesive formulations, including sustainable alternatives to traditional raw materials. Henkel's regional manufacturing network, including the Monterrey, Mexico facility, inaugurated in Q2 2024, provides strategic positioning to serve North American aerospace and automotive customers requiring localized technical support and supply chain reliability.

Companies Covered in Polysulfide Sealants Market

- PPG Industries, Inc.

- 3M Company

- Sika AG

- Henkel AG & Company, KGaA

- H.B. Fuller Company

- Arkema

- Toray Fine Chemicals

- Nouryon B.V.

- Dow Inc.

- Wacker Chemie AG

- BASF SE

Frequently Asked Questions

The global polysulfide sealants market is projected to reach US$ 1,807.6 Million by 2033, expanding from US$ 1,319.4 Million in 2026, representing a compound annual growth rate of 4.6%, driven by increasing aerospace production, infrastructure development in emerging markets, and growing demand for energy-efficient building solutions.

Primary market drivers include sustained aerospace production expansion requiring fuel-resistant sealants, rapid infrastructure development across India, China, and Southeast Asia, energy efficiency mandates driving insulated glass unit adoption, electric vehicle manufacturing expansion requiring advanced sealing solutions, and marine industry demands for corrosion-resistant sealants in harsh maritime environments.

High and low-rise building structures represent the largest application segment, commanding approximately 42% of total market value, with particular growth driven by insulated glass secondary sealing applications addressing global energy efficiency requirements and retrofit demand in developed economies.

Asia-Pacific emerges as the fastest-growing regional market, driven by India’s smart city initiatives, urban housing programs, and manufacturing expansion, complemented by China's infrastructure modernization and Southeast Asia's accelerating industrialization.

Development and commercialization of low-volatile organic compound (VOC) polysulfide formulations represents the primary market opportunity, as stringent environmental regulations across North America and Europe create demand for sustainable sealants meeting regulatory compliance and green building certification requirements while maintaining superior performance characteristics.

Leading market participants include PPG Industries, Inc., 3M Company, Sika AG, Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema, Toray Fine Chemicals, Nouryon B.V., Dow Inc., Wacker Chemie AG, and BASF SE, collectively representing significant global market share across diverse application segments.