- Inks, Coatings, Adhesives & Sealants (ICAS)

- Firestopping Sealants Market

Firestopping Sealants Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Firestopping Sealants Market By Product Type (Elastomeric, Intumescent), Material (Silicone, Acrylic), End-user (Residential, Commercial, Industrial), and Regional Analysis for 2025 - 2032

Firestopping Sealants Market Size and Trends Analysis

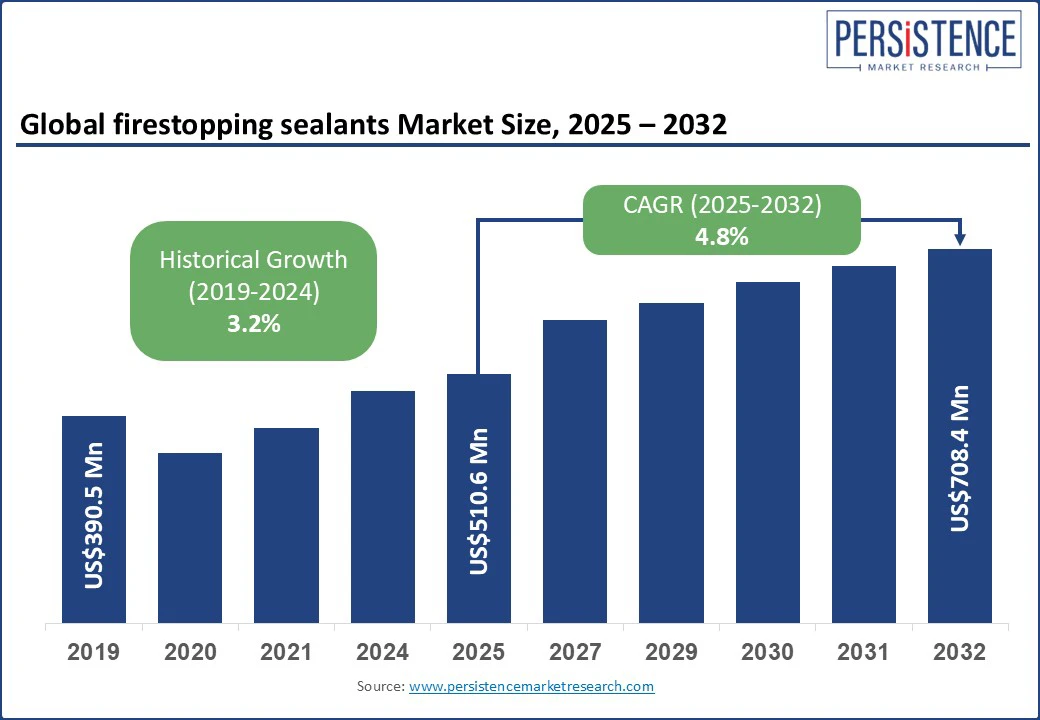

The global firestopping sealants market size is projected to rise from US$ 510.6 Mn in 2025 to US$ 708.4 Mn by 2032. It is anticipated to witness a CAGR of 4.8% during the forecast period from 2025 to 2032. The firestopping sealants market growth is driven by increasingly strict fire safety codes and rising awareness around passive fire protection. Manufacturers are developing new formulations, such as intumescent and elastomeric variants, as sustainability targets prompt a shift toward low-VOC solutions.

Key Industry Highlights:

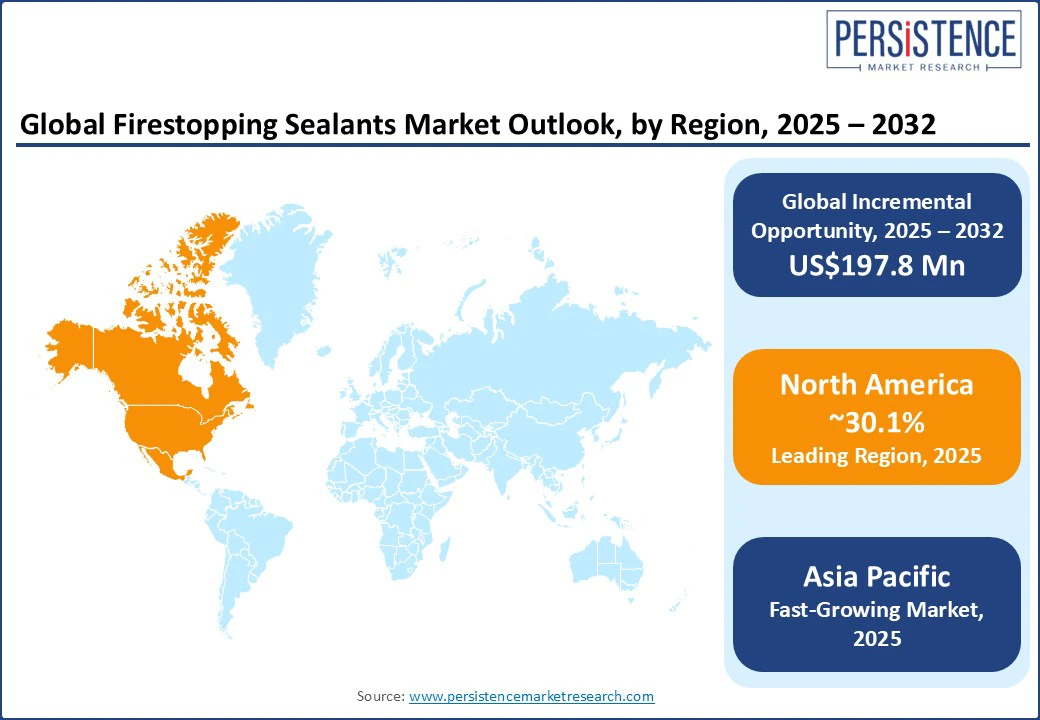

- Leading Region: North America with around 30.1% share in 2025, bolstered by increasing construction of data centers and healthcare facilities, propelling high-performance fire protection requirements.

- Fastest-growing Region: Asia Pacific, spurred by government-funded infrastructure projects, including airports and metros, which are mandating certified passive fire protection systems.

- New Product Launch: Specified Technologies Inc. introduced its Made in the U.S. SpecSeal Cast-In Firestop Device (CID). It is a sleeve, a firestop, and a watertight seal rolled into a single device.

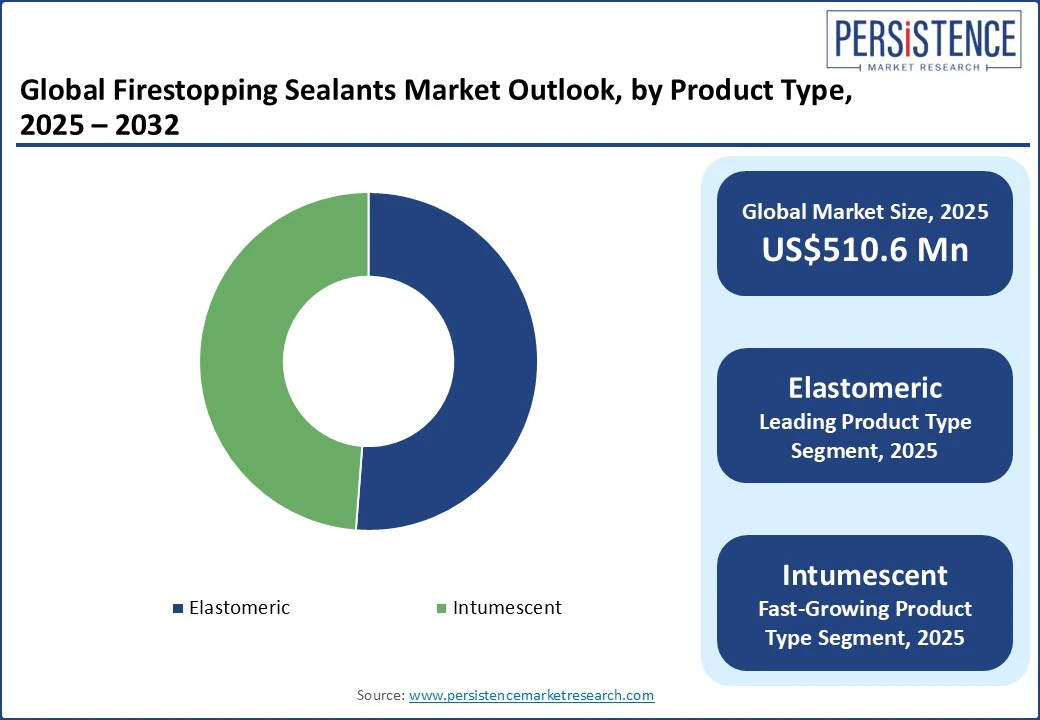

- Dominant Product Type: Elastomeric sealants are expected to account for approximately 51.2% market share in 2025, supported by their high durability in seismic zones, which makes them ideal for earthquake-prone regions.

- Leading Material: Silicone-based firestopping sealants record nearly 62.4% share in 2025, fueled by their ability to maintain integrity under extreme temperatures and meet strict fire endurance standards.

|

Global Market Attribute |

Key Insights |

|

Firestopping Sealants Market Size (2025E) |

US$ 510.6 Mn |

|

Market Value Forecast (2032F) |

US$ 708.4 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Dynamics

Driver - Mandatory Compliance Checks Boost Use in Key Penetration Areas

The surging demand for fire safety in both new constructions and renovation projects drives growth in the firestopping sealants market. In urban centers, the strict enforcement of building codes such as the 2024 International Building Code (IBC) update in the U.S. and the revised National Building Code of India (NBC 2023) now requires more detailed fire containment strategies. These focus particularly on cable trays, duct penetrations, and expansion joints. This shift has made passive fire protection products, including sealants, mandatory during inspection.

In aging structures, retrofitting for fire compliance is becoming a necessity. Governments in Europe and Asia Pacific are allocating funds toward fire safety renovations in hospitals, schools, and public buildings following a series of high-profile fire incidents. The U.K. government’s Building Safety Fund, launched in 2020, for example, has received various top-ups, totaling nearly £4.5 Bn (US$5.72 Bn). In new construction, the growth of high-density infrastructure demands pre-emptive passive fire protection planning, thereby spurring the market.

Restraint - Sealant Shrinkage Raises Reliability Concerns in Long-term Fire Protection

Shrinkage in firestopping sealants, primarily those made from latex or water-based acrylics, has become an increasing concern in construction projects requiring long-term fire protection. These materials tend to shrink up to 25% as they cure in environments with low humidity or high temperature variations. This shrinkage often creates gaps or pulls the sealant away from the substrate, hindering its ability to maintain an air-tight and fire-resistant barrier over time. Hence, contractors are increasingly cautious about using latex-based sealants in high-risk zones such as penetrations around piping, cable trays, and joints in multi-story buildings.

A few manufacturers have started developing hybrid formulations that combine acrylic with elastomeric agents to reduce shrinkage while maintaining paintability and ease of application. These developments, however, still struggle with gaining traction in legacy buildings where quick-dry and budget-friendly latex products remain popular. In regions with fluctuating weather conditions, contractors now conduct more rigorous field testing and third-party inspections to prevent shrinkage-related failures.

Opportunity - LEED and BREEAM Standards Encourage Halogen-free Sealant Development

The rise of green building certifications, including Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM), is encouraging manufacturers to re-engineer firestopping sealants with a focus on sustainability. These certifications require strict limits on indoor air pollutants, including VOCs. Hence, manufacturers are now investing in low-VOC and halogen-free formulations that can still meet fire-resistance standards.

Hilti and 3M, for instance, have released sealants that meet both fire code requirements and green building standards such as LEED v4. It rewards products with Environmental Product Declarations (EPDs) and low chemical emissions. In Asia Pacific, various companies based in Japan are introducing silicone-based sealants with recyclable packaging and reduced solvent use. This shows a broad trend where even packaging choices are under scrutiny. These shifts are not just regulatory-backed, as building owners and developers are seeking full transparency about a product’s environmental footprint as part of ESG reporting.

Category-wise Analysis

Product Type Insights

Based on product type, the market is bifurcated into elastomeric and intumescent. Among these, the elastomeric sealants segment will likely account for nearly 51.2% of the firestopping sealants market share in 2025 due to their superior flexibility and ability to maintain fire-resistance performance under powerful joint movement. In high-rise buildings, hospitals, and data centers, structural joints expand, contract, or vibrate over time. Elastomeric sealants adapt to these shifts without cracking or detaching. It is essential in seismic zones or large commercial buildings where joint movement is frequent.

Intumescent sealants are gaining impetus owing to their preference in applications where passive fire protection must account for penetrations involving plastic pipes, cables, or other combustible components. These sealants expand when exposed to heat, forming a char that seals gaps and prevents fire, smoke, and toxic gases from passing through. This feature is effective in modern commercial or industrial buildings, where mixed-material systems are common. The preference also stems from their ability to maintain fire integrity in dynamic scenarios involving combustible materials.

Material Insights

By material, the market is trifurcated into silicone, acrylic, and others (polyurethane). Out of these, the silicone segment is predicted to hold approximately 62.4% of the share in 2025, owing to its exceptional thermal stability and long-term elasticity, even when exposed to extreme heat. It is capable of withstanding continuous temperatures up to 250°C and short-term exposure beyond 300°C without degradation. This property is beneficial in settings such as mechanical rooms or industrial plants, where thermal cycling is frequent.

Acrylic is expected to witness considerable growth backed by its cost-efficiency and ease of use in static applications, including drywall assemblies and small pipe penetrations. Acrylic-based sealants are water-based, making them easy to clean and apply without specialized tools. This drastically reduces installation time and labor costs. Their compliance with green building standards is another key factor pushing demand. They adhere well to materials such as gypsum, concrete, and wood, making them ideal for visually sensitive areas.

Regional Insights

North America Firestopping Sealants Market Trends - Strict Fire Safety Norms Strengthen Growth

In 2025, North America is estimated to account for around 30.1% of the market share, as it thrives on stringent building codes implemented by the Occupational Safety and Health Administration (OSHA), International Building Code (IBC), and National Fire Protection Association (NFPA). These norms span residential, commercial, and high-risk industrial sectors, encouraging widespread adoption of reliable firestop systems. The surge in city infrastructure, healthcare buildings, data centers, and transportation facilities adds additional demand for unique firestop sealants.

The U.S. firestopping sealants market is poised to show steady growth due to constant research and development activities by leading companies. In January 2024, for example, Hilti launched a new line of sealants with reduced Volatile Organic Compound (VOC) content. It aims to cater to sustainability requirements and comply with strict environmental norms. A key market trend is the role of direct distribution, as most of the sealants manufactured in the U.S. are procured directly by large contractors and industrial clients.

Asia Pacific Firestopping Sealants Market Trends - Smart City Projects in China Fuel Demand for High-performance Sealants

Asia Pacific is considered one of the most dynamic markets, spurred by large-scale infrastructure projects and strict building safety codes in specific countries. China leads both in terms of volume and development. This growth is attributed to the country's ongoing development of smart cities, tech parks, and high-rise commercial infrastructure. Domestic players are becoming competitive, utilizing localized manufacturing and region-specific product development to undercut global brands on pricing.

India is emerging as a key market due to the increasing construction of hospitals, IT campuses, airports, and mass housing projects under government initiatives such as the Smart Cities Mission and the Pradhan Mantri Awas Yojana (PMAY). In addition, local regulators are tightening fire safety codes, primarily for commercial and high-density residential buildings, further augmenting demand for compliant and certified sealants. Vietnam, Indonesia, and the Philippines are witnessing a surge in commercial real estate and manufacturing facilities, which is boosting demand.

Europe Firestopping Sealants Market Trends - Germany’s Retrofitting Spurs Growth in Public Infrastructure Projects

Europe is being propelled by the ongoing push for fire safety upgrades in both new and existing buildings. Strict enforcement of EU-wide and national building codes is taking hold across commercial and residential sectors. Germany is leading due to retrofitting efforts across public infrastructures. These include schools, hospitals, and high-rise housing blocks that were built before modern fire regulations came into effect. New projects are also specifying novel intumescent sealants, backed by their performance in passive fire protection.

Material shortages and price inflation are, however, posing a challenge across Europe. The delivery of certified firestopping sealants in the region can take 12 to 16 weeks, compared to the four to six weeks seen in pre-pandemic years. Regulatory complexity is another factor transforming the market. U.K.-based manufacturers must comply with both - U.K. Conformity Assessed and EU CE marking regulations. This compliance requirement has compelled companies to split production lines and inventory management, reducing efficiency and shrinking available stock.

Competitive Landscape

The global firestopping sealants market has a fragmented structure, with no single player dominating the field. While established companies, including 3M, Hilti, Tremco, and H.B. Fuller hold noticeable shares, the market is populated by various regional and mid-sized firms that excel in specific geographies or applications. This fragmentation fuels intense competition, especially in developing countries where price sensitivity and local compliance requirements influence procurement.

Strategic partnerships and joint ventures are becoming relevant among regional players aiming to extend their footprint and technical capabilities. Leading players are also focusing on the development of novel intumescent formulations and eco-friendly sealants with low VOC emissions.

Key Industry Developments

- In October 2024, FSi Promat launched a reformulated PyroPro HPE sealant to support healthy working practices in the construction industry. The firm upgraded the formula to help protect contractors and installers while maintaining its fire performance.

Companies Covered in Firestopping Sealants Market

- 3M Company

- BASF SE

- Hilti Group

- Specified Technologies, Inc. (STI)

- Fosroc, Inc.

- Tremco Incorporated

- H.B. Fuller Company

- Promat International

- RPM International Inc.

- Nelson Firestop (Emerson Electric Co.)

- Pecora Corporation

Frequently Asked Questions

The firestopping sealants market is projected to reach US$510.6 Mn in 2025.

Rising renovation activities in aging infrastructure and a surge in high-rise construction worldwide are the key market drivers.

The firestopping sealants market is poised to witness a CAGR of 4.8% from 2025 to 2032.

Collaborations with certification bodies and government incentives for energy-efficient buildings represent key market opportunities.

3M Company, BASF SE, and Hilti Group are among the key market players.