- Inks, Coatings, Adhesives & Sealants (ICAS)

- High Temperature Sealants Market

High Temperature Sealants Market Size, Share, and Growth Forecast, 2026 - 2033

High Temperature Sealants Market by Chemistry Type (Silicone, Epoxy and Others Type (Cadmium Telluride, Copper Indium Gallium Selenide, Amorphous Silicon and Others), Application (Electrical and Electronics Transportation, Industrial, Construction and Others) and Regional Analysis for 2026 - 2033

High Temperature Sealants Market Size and Trends Analysis

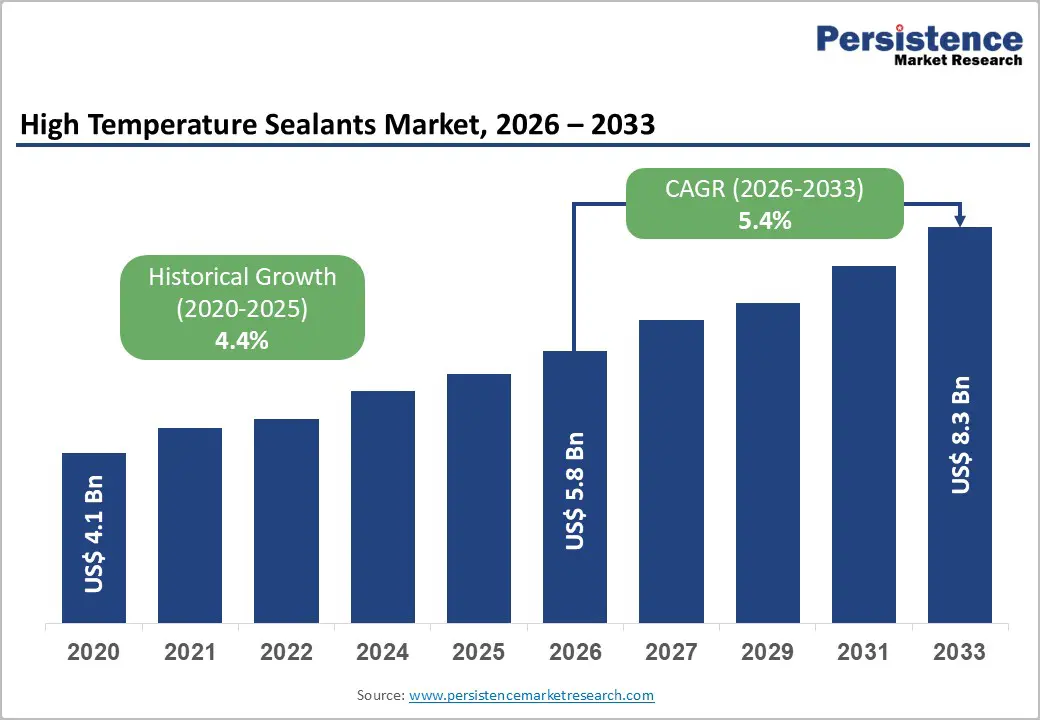

The global high-temperature sealants market is expected to reach US$ 5.8 billion in 2026 and US$ 8.3 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market is driven by automotive manufacturers expanding thermal-sealing requirements for electric-vehicle battery packs and power electronics, the aerospace industry deploying advanced dynamic seals capable of withstanding temperatures exceeding 300°C, and industrial equipment manufacturers requiring reliable sealing in high-temperature operating environments.

Key Industry Highlights:

- Leading Chemistry Type: Silicone dominates with 62.7% market share, driven by its thermal stability and broad applicability; Epoxy and advanced polymers are the fastest-growing at a 6.2% CAGR, driven by superior adhesion and specialized chemical resistance.

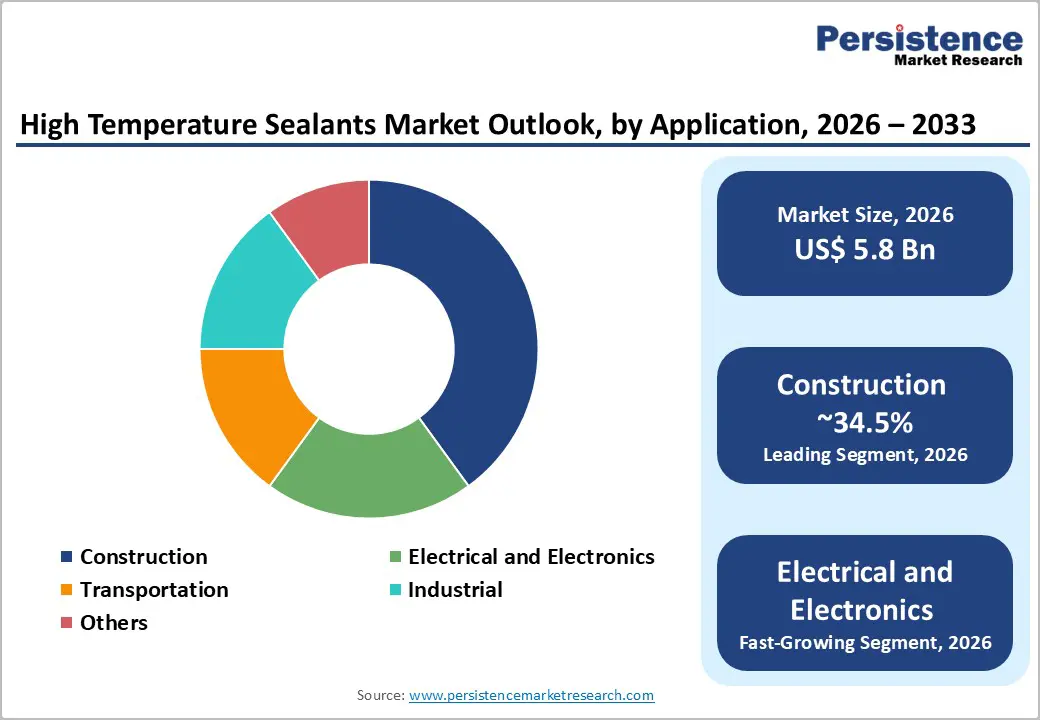

- Dominant Application: Construction maintains 34.5% market share through building sealing requirements; Electrical and electronics represent the fastest growing at 6% CAGR, driven by EV thermal management and semiconductor packaging complexity.

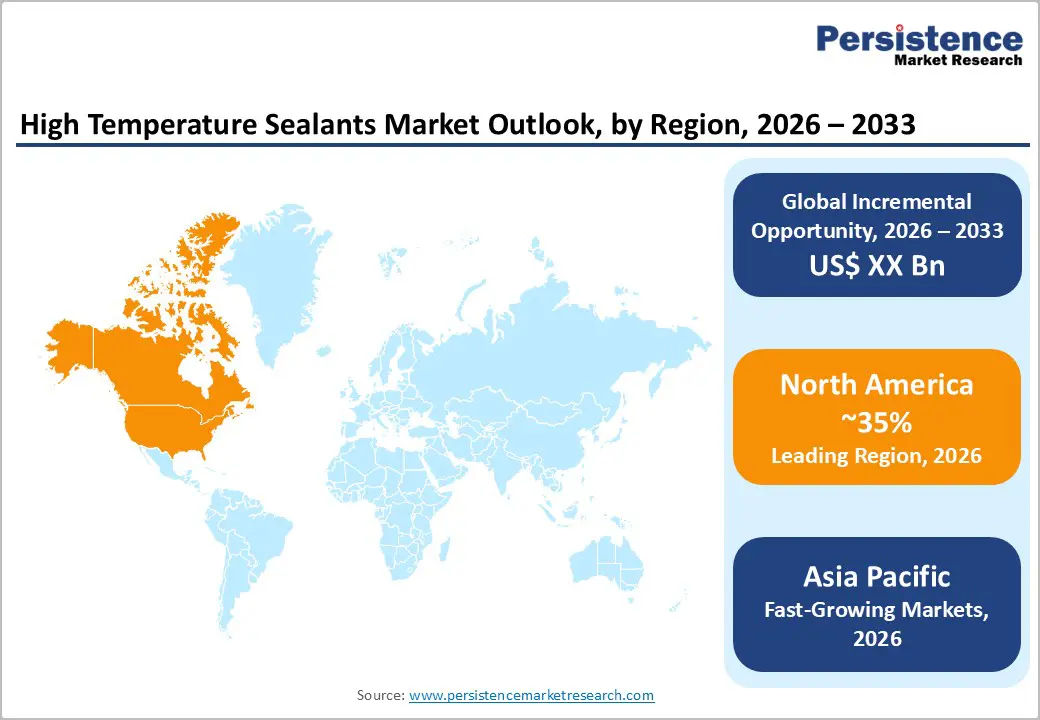

- Regional Market Dominance and Growth: North America maintains 35% global market share driven by aerospace and automotive leadership; Asia-Pacific demonstrates fastest regional growth at 7% CAGR, expanding from 30% current share to 38% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 60% market share (3M, Henkel, Dow, Arkema leading); Thermal-conductivity advancements achieving 5-8 W/m·K in silicone formulations; Temperature capability extending to 300°C+ for aerospace applications; Sustainability integration with bio-based and low-VOC formulations.

| Key Insights | Details |

|---|---|

| High Temperature Sealants Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 8.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.4% |

Market Dynamics

Drivers - Automotive Electrification and Electric Vehicle Thermal Management Requirements

Electric vehicle proliferation, with global EV sales growing 25% annually and reaching 13 million units in 2026, establishes proportionate thermal sealing demand. Battery thermal management criticality, with lithium-ion battery packs operating optimally within 15-35°C temperature range and requiring advanced sealants preventing thermal runaway and maintaining performance, drive specification requirements. High-voltage electronics expansion, with EV powertrains incorporating 300-400V battery systems and complex power conversion electronics generating 2-4 kW heat dissipation, necessitates robust thermal sealing solutions.

Charging infrastructure acceleration, with 5-10 million global EV charging stations deployed by 2033, requiring high-temperature seal integration in charging connectors and power-delivery equipment, and establishing supporting demand. ADAS integration complexity, with advanced driver assistance systems incorporating thermal sensors and control modules requiring specialized high-temperature sealing, expands application diversity.

Aerospace and Defense Sector Thermal Performance Requirements

Jet engine performance advancement, with modern aircraft engines operating at 600-700°C core temperatures requiring dynamic seals capable of withstanding sustained thermal exposure, establishes high-performance sealing demand. Military aircraft specification complexity, with defense applications requiring extreme temperature tolerance exceeding 500°C and durability validation spanning 10,000+ flight hours, drives premium sealant development. Hypersonic vehicle development, with next-generation aircraft testing programs evaluating sustained flight at Mach 5+ speeds, creating aerodynamic heating reaching 1,000°C+ surface temperatures, establishes emerging sealing application requirements.

Commercial aerospace expansion, with global commercial aircraft production projected to reach 11,000+ deliveries through 2033, requiring comprehensive sealing system integration, and establishing a volume demand foundation. Supply chain validation, with OEM qualification processes requiring extensive testing and documentation, establishing barriers limiting supplier participation and supporting premium positioning.

Restraints - High Material Costs and Performance-Price Tradeoff Complexity

Premium raw material costs, with specialty elastomers, polyimides, and fluoropolymers commanding 15-25% price premiums versus standard sealant materials, constrain market penetration in price-sensitive applications. Manufacturing complexity escalation, with advanced formulations requiring precision mixing, controlled curing, and extensive quality assurance increasing production costs 20-30% versus commodity sealants. Performance validation requirements, with aerospace and defense specifications demanding comprehensive testing (thermal cycling, chemical resistance, mechanical property validation) consuming 12-18 months and US$ 500K+ per formulation limiting new entrant participation. Competitive pressure from substitutes, with alternative sealing technologies (metal gaskets, composite seals, novel polymers) offering comparable performance at lower costs, creating pricing pressure.

Application-specific customization, driven by diverse industry requirements that demand tailored formulations, increases engineering overhead and limits standardization benefits. Regulatory compliance costs, with REACH, RoHS, and equivalent regulations requiring extensive documentation and reformulation investments adding 5-10% to development budgets.

Application-Specific Technical Complexity and Integration Challenges

Material compatibility concerns, with high-temperature sealants requiring compatibility assessment across multiple substrates (metals, ceramics, polymers, composites), limit universal applicability and create engineering complexity. Temperature-cycling degradation, with thermal stress inducing material fatigue and property degradation over extended operational cycles, requiring sophisticated design considerations and safety margins. Chemical resistance validation, with diverse operational environments (acidic, alkaline, organic solvents, oxidative atmospheres) creating specific sealing requirements limiting solution transferability across applications.

Integration coordination, with thermal sealing representing one component within complex multi-system assemblies, requires coordination across design disciplines and supply chains, extending development timelines. Failure consequence severity, with seal failure in critical applications (engine systems, aerospace, high-pressure equipment), creates catastrophic consequences, establishing risk aversion and conservative material selection.

Opportunity - Electric Vehicle Battery Thermal Management System Integration

EV battery module cooling systems, with thermal management representing a critical safety and performance requirement for 100+ million vehicles reaching market through 2033, establish a massive addressable opportunity. Thermal interface material advancement, with emerging thermally conductive sealants achieving 3-8 W/m·K thermal conductivity, enabling optimized heat dissipation from battery cells to heat sinks, justifies premium positioning.

Manufacturing automation integration, with automated sealant dispensing systems achieving precision application (±0.5mm tolerance), supporting high-volume battery pack assembly, establishes production scale-up potential. Supply-chain consolidation, with automotive OEMs standardizing thermal sealant specifications across platforms, enabling single-supplier relationships and reducing engineering complexity, supports adoption acceleration.

Advanced Aerospace Hypersonic and Reusable Vehicle Programs

Hypersonic vehicle development, with next-generation military and commercial hypersonic programs creating sustained funding and procurement for extreme-temperature sealing solutions capable of withstanding 1,000°C+ surface conditions, establishes specialized high-value demand. Reusable launch vehicle advancement, with commercial space companies developing reusable rocket systems requiring thermal protection system integration and advanced sealing for multi-flight operations, creates an emerging application segment.

Military aircraft modernization, with global military aviation programs committing US$ 50-100B+ to next-generation aircraft development incorporating advanced thermal management systems, establish defense procurement foundation. Additive manufacturing integration, with advanced aerospace designs incorporating additive manufacturing techniques that create complex geometries and require specialized sealing solutions, establishes an emerging technical requirement.

Category-wise Analysis

Chemistry Type Insights

The silicone chemistry segment holds 62.7% market share, driven by proven thermal stability and broad application versatility. Silicone sealants maintain integrity from -55°C to +250°C, offering superior thermal cycling resistance critical for automotive, aerospace, and industrial systems. Their wide chemical compatibility with oils, fuels, and process fluids supports multi-industry adoption. Exceptional elasticity allows stress absorption during thermal expansion, ensuring long-term sealing reliability. Mature manufacturing processes enable consistent quality, scalable production, and cost efficiency, while RoHS-compliant and eco-friendly formulations support regulatory compliance. Silicone’s adaptability across transportation, construction, and heavy industry reinforces market leadership.

The epoxy and advanced polymer segment is the fastest growing, expanding at 8% CAGR through 2033. Growth is driven by improved high-temperature performance (200-250°C), superior adhesion to metals and composites, enhanced chemical resistance, and added structural reinforcement benefits. Aerospace, defense, and specialty industrial applications increasingly favor these advanced chemistries, accelerating adoption.

Application Insights

Construction applications hold 34.5% market share, driven by extensive building envelope and structural sealing needs across varied climates. Modern facades require weather-resistant sealants that maintain performance from -40°C to +60°C, while window and glazing systems depend on flexible sealants that accommodate 5-10% thermal movement and prevent water ingress. Mandatory joint sealing in concrete, metal, and hybrid structures, combined with strict building codes, ensures steady demand across thousands of projects. High-performance sealants also improve energy efficiency, reducing heat loss by 20-30%, supporting premium specifications. Massive global construction spending sustains volume leadership.

Electrical and electronics applications are the fastest-growing segment, expanding to 6.4% CAGR through 2033. Growth is driven by EV battery thermal management, advanced semiconductor packaging, high-power electronics in renewables and 5G infrastructure, and rising adoption of high-conductivity thermal interface sealants, with IoT proliferation further expanding demand.

Regional Insights

North America High Temperature Sealants Market Share

North America commands approximately 35% of global High Temperature Sealants market share, valued at approximately US$ 1.86 billion in 2026 with projections approaching US$ 2.7 billion by 2033. The United States represents dominant regional market contributor, accounting for 82% of North American market value, driven by aerospace leadership and automotive innovation concentration.

Aerospace dominance, with major aerospace OEMs (Boeing, Lockheed Martin, Northrop Grumman) and tier-1 suppliers concentrating development and manufacturing in North America establishing specification leadership. EV electrification leadership, with Tesla, GM, Ford, and emerging EV manufacturers establishing North American production capacity driving proportionate thermal sealing demand. Automotive supply-chain concentration, with 70%+ of North American vehicle manufacturing incorporating thermal management systems requiring high-temperature sealing, establish volume foundation.

Europe High Temperature Sealants Market Share

Europe represents approximately 23% of global High Temperature Sealants market share, valued at approximately US$ 1.39 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 70% of European market value, reflecting automotive manufacturing concentration and industrial equipment specialization.

Automotive manufacturing leadership, with German automakers (Mercedes-Benz, BMW, Audi, Volkswagen) driving thermal management innovation and establishing specification standards. Industrial equipment specialization, with German, Swiss, and Italian manufacturers leading chemical processing and power generation equipment innovation requiring advanced thermal sealing. Sustainability focus, with EU environmental directives and circular economy principles driving development of recyclable and low-VOC high-temperature sealants. Building renovation programs, with EU-funded modernization initiatives retrofitting millions of buildings requiring advanced facade and structural sealing.

Asia Pacific High Temperature Sealants Market Analysis

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 38% by 2033. The region valued at approximately US$ 1.7 billion in 2026 is anticipated to reach US$ 3.0 billion by 2033, representing fastest-growing regional market with estimated CAGR of 7%.

Manufacturing scale-up, with China, India, and Vietnam establishing comprehensive automotive and electronics manufacturing capacity driving proportionate thermal sealing demand. EV proliferation acceleration, with China selling 7+ million EVs annually and emerging manufacturers ramping production, establishing a dominant market opportunity. Industrial equipment modernization, with chemical processing, power generation, and petroleum refining industry expansion across the Asia-Pacific, is creating thermal sealing requirements. Construction boom persistence, with urbanization continuing across emerging markets and creating massive building facade and structural sealing demand.

Competitive Landscape

The global high temperature sealants market demonstrates moderate consolidation with established specialty chemical suppliers and regional manufacturers maintaining competitive positions. The top 10 suppliers, including 3M Company, Henkel AG, Dow Inc., Arkema, Wacker Chemie, Sika AG, H.B. Fuller, PPG Industries, Illinois Tool Works, and specialized high-performance sealant manufacturers, collectively control approximately 55% of global market share, reflecting technology leadership, manufacturing scale, and aerospace/automotive relationships. Market structure reflects bifurcation between multinational chemical companies offering comprehensive sealant portfolios and specialized manufacturers focusing exclusively on high temperature sealing technology development.

Key Industry Developments:

- In October 2024, A Sweden-based cable manufacturing company, Roxtec, introduced a new tank boundary sealing solution for the maritime sector. It has been already used in refining the Royal Navy's HMS Protector. The seal can be installed around existing cables or pipes without special tools. It is ideal for high pressure, fire-rated to A-60, dust-tight, and vibration.

- In May 2024, KRAIBURG TPE, based in South Korea, introduced Thermoplastic Elastomers (TPEs) with EPDM adhesion for automotive sealing systems and exterior applications. These are formulated for automotive exterior parts with UV resistance and can be used in glass run channels and sealing profiles.

Companies Covered in High Temperature Sealants Market

- Dow Corning Corporation

- Wacker Chemie AG

- Henkel AG & Co. KGaA

- Sika AG

- 3M Company

- Bostik SA

- H.B. Fuller

- PPG Industries Inc.

- CSW Industrials Inc.

- Illinois Tool Works Company

- Soudal N.V.

- Others Key Players

Frequently Asked Questions

The High Temperature Sealants market is estimated to be valued at US$ 5.8 Bn in 2026.

The key demand driver for the High Temperature Sealants market is the rapid growth of high-temperature industrial applications requiring reliable thermal resistance, durability, and safety compliance.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global High Temperature Sealants market.

Among the Application type, Construction holds the highest preference, capturing beyond 34.5% of the market revenue share in 2026, surpassing other Application type.

The key players in High Temperature Sealants are Dow Corning Corporation, Wacker Chemie AG, Henkel AG & Co. KGaA, Sika AG, 3M Company.